‘Financialisation’ has been promoted by heterodox economists as the cause of the iniquities and failures of modern capitalist economies. Now an additional theory has been offered: ‘renterisation’. In a recent long article in the British Financial Times, its well-known economic columnist, Martin Wolf, offered this concept as the explanation of low productivity growth, rising inequality and the mountain of debt in the major economies.

Wolf reckons that capitalism has been “rigged” by monopolistic economic powers. “So why is the economy not delivering? The answer lies, in large part, with the rise of rentier capitalism. In this case “rent” means rewards over and above those required to induce the desired supply of goods, services, land or labour. “Rentier capitalism” means an economy in which market and political power allows privileged individuals and businesses to extract a great deal of such rent from everybody else…. While the finance sector is an important part of this monopolistic development, so that ‘financialisation’ has enabled monopoly sectors to create their own profits (if often illusory) and generate financial crashes, the real enemy of successful capitalism is “the decline of competition”. Wolf then cites all the recent empirical evidence of this ‘renterization’ of capitalism: market concentration; rising monopolistic profit mark-ups and ‘super star’ companies like the FAANGS making “monopolistic profits”.

But does this theory hold as the main reason for poor economic growth, rising inequality and financial crashes? Is it monopoly capitalism that is the cause, not the contradiction of capitalism as a whole? Well, let me remind readers of the empirical evidence for the renterisation theory. I have recounted that in previous posts and the evidence is doubtful at best. For example, you would expect the biggest profit mark-ups to be achieved by the ‘monopoly’ giants – in fact the data show it is the smaller companies that get higher mark-ups.

Again, low productivity growth appears to be much more closely correlated with low investment and in turn with low profitability, not with monopolisation. The biggest slowdown in productivity growth in the US began after 2000, as investment in productive sectors and activity dropped off. It is a fall in the overall profitability of US capital that is driving things rather than any change in monopoly ‘market power’. Again, for example, evidence shows that the ‘rent-seekers’ appear to have played no role in the low investment rate of the Eurozone: it’s just low profitability there. But such evidence is not convenient because it suggests that the cause of low productivity growth is due to contradictions in capitalist accumulation. It is more encouraging to argue that if profits are high, then it’s ‘monopoly power’ that does it, not the exploitation of labour in the capitalist mode of production. And it’s monopoly power that is keeping investment growth low, not low overall profitability.

Brett Christophers from the University of Uppsala in Sweden has published an important piece of work on renterisation (with a book to follow). Christophers rejects the term ‘financialisation’ as a cause of the current malaise in capitalist growth. Finance is too narrow a cause; because rents are being extracted in many other sectors like real estate. Christophers argues that “renterism’ in its various guises is today a significant, even dominant, dynamic, in contrast to during the period preceding the neoliberal turn.” He reckons the British economy “has been substantially rentierized.” Christophers renterization Christophers offers what he calls a hybrid definition of rent that tries to combine Marx’s view of rent coming from the monopoly ownership of a non-produced asset (land, minerals etc) with the mainstream view of “excess payment” over and above efficient production, namely payment above the ‘marginal productivity of labour or capital’.

I’m not sure that this hybrid definition is useful. It appears to fudge the key issue that Marx makes about how rent emerges: namely that it comes from the appropriation of surplus value created in the exploitation of labour in the production of commodities. For Marx, rent comes from the ability of monopoly owners of non-produced assets to retain surplus-value from being merged with the competitive process of capital flows. For Marx, ‘productive capitalists’ as appropriators of surplus value from the exploitation of labour are forced share some of that surplus value with owners of non-produced resources (rent) and finance (interest). Rent and interest are part of total surplus value created in the production of commodities. Value and surplus value must first be created by the exploitation of labour power. Then the surplus value gets redistributed and those with some monopoly power can extract a part of that surplus value in rent. “Excess payment’ over ‘efficiency’ implies that there is an acceptable payment to capitalists for exploiting labour power to benefit productivity and thus ignores these class relations.

Marx considered that there were two forms of rent that could appear in a capitalist economy. The first was ‘absolute rent’ where the monopoly ownership of an asset (land) could mean the extraction of a share of the surplus value from the capitalist process without investment in labour and machinery to produce commodities. The second form Marx called ‘differential rent’. This arose from the ability of some capitalist producers to sell at a cost below that of more inefficient producers and so extract a surplus profit. This surplus profit could become rent when these low cost producers could stop others adopting even lower cost techniques by: blocking entry to the market; employing large economies of scale in funding; controlling patents; and making cartel deals. This differential rent could be achieved in agriculture by better yielding land (nature) but in modern capitalism, it could be through a form of ‘technological rent’; ie monopolising technical innovation.

Undoubtedly, much of the mega profits of the likes of Apple, Microsoft, Netflix, Amazon, Facebook are due to their control over patents, financial strength (cheap credit) and buying up of potential competitors. But the renterization explanation goes too far. Technological innovations also explain the success of these big companies, not just monopoly power. Moreover, by its very nature, capitalism, based on ‘many capitals’ in competition, cannot tolerate any ‘eternal’ monopoly, namely a ‘permanent’ surplus profit deducted from the sum total of profits divided among the capitalist class as a whole. The battle among individual capitalists to increase profits and their share of the market means monopolies are continually under threat from new rivals, new technologies and international competitors. Take the constituents of the US S&P-500 index. The companies in the top 500 have not stayed the same. New industries and sectors emerge and previously dominant companies wither on the vine.

The history of capitalism is one where the concentration and centralisation of capital increases, but competition continues to bring about the movement of surplus value between capitals (within a national economy and globally). The substitution of new products for old ones will in the long run reduce or eliminate monopoly advantage. The monopolistic world of GE and the motor manufacturers of the 1960s and 1990s did not last once new technology bred new sectors for capital accumulation. The world of Apple will not last forever.

‘Market power’ may have delivered rents to some very large companies in the US, but Marx’s law of profitability still holds as the best explanation of the accumulation process. Rents to the few are a deduction from the profits of the many. Monopolies redistribute profit to themselves in the form of ‘rent’ but do not create profit. Profits are not the result of the degree of monopoly or rent seeking, as neo-classical and Keynesian/Kalecki theories argue, but the result of the exploitation of labour. Moreover, rents are no more than 20% of value-added in any major economy; financial profits are even smaller a proportion. Moreover, the rise of renterism in the recent period is really a counteracting factor to the decline in the profitability of productive capital.

There is another definition of a rentier economy based on Marx’s explanation of the division of surplus value into profits, rent and interest that is relevant. There are national economies where the capitalist sector appropriates much surplus value in the form of interest, dividends and profits through non-productive services like finance, insurance, and so-called business services. Britain is one of these ‘rentier’ economies; Switzerland is another – both much more so than the likes of Germany or Japan, or even the US, where the appropriation of surplus value is still predominantly through the direct exploitation of labour power (both domestically and abroad).

As the spoke person for the City of London recently said, “London is the capital of capital”. The City of London delivers a considerable inflow of income to the UK economy through its sale of financial services, bank interest and profits and allied business services. The UK financial sector plus real estate (oligarchs want to live in London) and other business services contributes a much larger proportion of GDP and cross-border income inflows to the balance of payments than most other major economies.

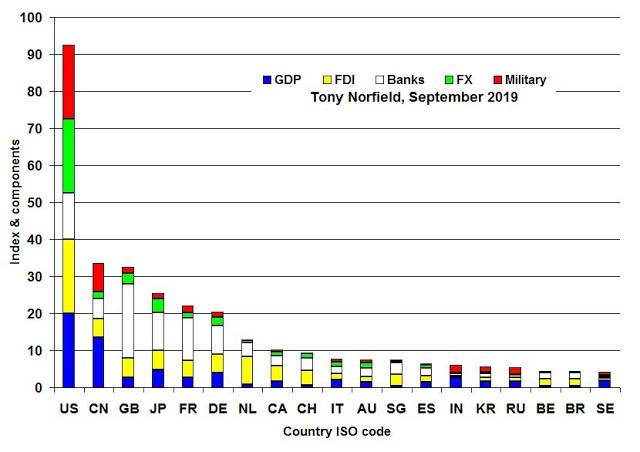

Tony Norfield has developed a power index of imperialist economies and in that index, the US leads, but it is followed by the UK. If you strip out of the index, the military and GDP constituents, Britain is way ahead of all as a rentier economy (at least in absolute dollar terms).

I did a little analysis from the WTO of commercial services exports of different countries. The export of financial, insurance and other business services as well royalties and fees collected could be considered a measure of rentier exports if you like. On this measure global rentier exports totalled $2trn in 2013. The US received export income of $365bn, or 18% of world rentier income; the UK obtained $180bn, or 9%, while Japan received $78bn or 4% and Germany had no cross-border rentier income at all. US GDP in 2013 was $16.7trn, the UK’s was $2.7trn. So the UK received rentier export income equivalent to 7% of its GDP while the US got just 2% of its GDP from rentier exports. In this sense, we can talk about a rentier economy and Britain as the poster child. But that makes Britain particularly vulnerable to financial crashes.

Joseph Stiglitz and Martin Wolf reckon that what is wrong with capitalism is that ‘financialisation’ and monopoly rentier interests have ‘rigged’/ruined the ‘progressive’ features of capitalism, namely its ability to expand the productive forces harmoniously for all. As Wolf puts it: “We need a dynamic capitalist economy that gives everybody a justified belief that they can share in the benefits. What we increasingly seem to have instead is an unstable rentier capitalism, weakened competition, feeble productivity growth, high inequality and, not coincidentally, an increasingly degraded democracy. Fixing this is a challenge for us all, but especially for those who run the world’s most important businesses. The way our economic and political systems work must change, or they will perish.”

But as LSE professor Jerome Roos perceptively pointed out in the British left journal, New Statesman, “By opposing the “bad” capitalism of the unproductive rentier to the “good” capitalism of productive enterprise, however, the conventional liberal narrative overlooks the fact that the two are inextricably entwined. Such thinking relies on an idealised but entirely theoretical version of capitalism that is pure, uncorrupted and far more benign than it is, or has ever been or, in all likelihood, ever will be. The reality is that the concentration of wealth and power in the hands of a few privileged rentiers is not a deviation from capitalist competition, but a logical and regular outcome. In theory, we can distinguish between an unproductive rentier and a productive capitalist. But there is nothing to stop the productive, supposedly responsible businessperson becoming an absentee landlord or a remote shareholder, and this is often what happens. The rentier class is not an aberration but a common recurrence, one which tends to accompany periods of protracted economic decline.(my emphasis)”.

In the past, this blog has posted overwhelming empirical evidence that the key to understanding the movement in productive investment remains in the underlying profitability of capital, not in the extraction of rents by a few market leaders, as Wolf and others suggest. If that is right, the Keynesian/mainstream solution of regulation and/or the break-up of monopolies (even if it were politically possible) will not solve the regular and recurrent crises in production and investment or stop rising inequality of wealth and income.

I am afraid that replying to Wolf or the Keynesians is not providing a modern marxist theory of rent, and is not offering an adequate explanation of the role that rent (differential, technological etc) plays in modern capitalistic economies.

What is needed a theory that will jointly explain the effects to the law of value of the following evolutions in capitalistic mode of production:

a. The R&D, i.e., the production of prototypes (chemical synthesis, musical synthesis, algorithms, software, movies, machine designs etc) is more and more separated from the rest of the production process, and especially from the massive production of commodities.

b. The R&D also attracts a rising portion of the total capital investment, especially given the automatisation or production.

c. Some times, the products of R&D become commodities themselves and enter the market as such. It is well known now that these commodities have some “peculiarities”, namely:

1. they cannot be “consumed”, i.e., the bare no wear through their use, i.e., they don’t loose any of their use-value with time of usage,

2. they suffer from infinite moral devaluation without any IP law protection, since no-one will REPRODUCE them, if one can just copy them, and this morel devaluation slows down with the degree of IP law protection,

3. IP law protection can then lead to monopolies, the fact that they don’t last forever doesn’t mean that their producers do NOT accrue ANY technological/differential rents,

4. they are no-rival and non-inclusive,

5. points 1 and 4 above mean that there is no marxists theory at the moment about how much value these commodities can transfer, if we consider them as “means of production”.

Also, I am quite sceptical about what kind of statistics one needs in order to measure this kind of technological rents.

I have seen statistics about the FAANGS that clearly show very high profit margins.

In addition, FAANGS have clear monopolistic access to the informational resources their networks generate. This is also known as the “network effect”, i.e., the use value of a network increases with the number of subscribers, which, therefore, pushes towards fewer and larger such networks (social, etc).

In short, I fully agree that if there is a (monopolistic) rentier economy, this is capital’s response to the automatisation of production, to the rise of the organic composition of capital and to the resulting tendency of the profit rate to fall. This means that the so-called “rentier” economy is a inherent tendency of the capitalistic mode of production in its modern stage of development, and therefore, it needs to be logically and theoretically derived by the marxists political economy of that mode of production.

Saying that “The companies in the top 500 have not stayed the same” is a very poor argument. It suffices if those 500 change much less or slower than in the past.

I am looking forward to your commenting of Thomas Rotta”s work.

I do not agree with his base argument that knowledge commodities have 0 value because their reproduction is very cheap, because I don’t think the copying or the mass production of a prototype is the same labor as the original production of prototype.

I believe that R&D labor is a particular kind of labor that produces the intellectual representation of a production process and encodes it to some material substrate. This labor is inherently non reproducible, i.e., it is labor that produced a human made resource, similar to natural resources, a resource that suffers only from moral devaluation, via technological competition. The prototype design is not a means of production, in that it doesn’t transfer value to other commodities in the manner a means of production does. Therefore, we need to find a way to connect the labor expanded on its production to the value that such a R&D prototype-as-commodity can realise to the market.

This is an open issue for marxists political economy, and one of great importance.

Dionysios – I agree that a short post cannot do justice to a proper Marxist theory of rent. But this is a blog so there are lots of things left out. I am still planning a post on Rotta et al shortly that I hope can deal with some of your very valuable points 1-5. And I agree with you that Rotta is wrong about knowledge having no value. Mental labour or knowledge is still material and its value can be measured. But more on this soon. As you say theory on this very important in understanding information in capitalist production.

Thanks for you reply, and I am looking forward to a Rotta related article of yours.

I believe that capitalistically employed knowledge labor should produce value because it produces a use-value that is subsequently used in production, i.e., it is used to guide production of goods, as the intellectual representation of the production process that instructs humans or machines, encoded in some material substrate. In other words, R&D labor is not about formal transformations that do not affect the value of end products. However, it is also true that strictly speaking, R&D labor is all about getting a competitive advantage, since anyway the production would not stop without it, i.e., in that respect it functions as other non-productive activities like advertising. So, the biggest challenge is to find out how R&D products transfer value, and how much value they can transfer and/or realise!

In the meantime, I was intrigued by your statement in your previous article that according to the study of J De Loecker and J Eeckhout it is mostly smaller firms that gather higher markups:

“However, there are two things against the ‘market power’ argument, at least as the sole or main explanation of the rise in profits share and profit per unit of production. First, as De Loecker and Eeckhout find, economy-wide, it is mainly smaller firms that have the higher markups – hardly an indicator of monopoly power. ”

from here: https://thenextrecession.wordpress.com/2017/09/05/productivity-profit-and-market-power/

But, I copy-paste from page 44 of this article

Click to access 5d6436733e910486884d1c8f64eee6ebecf1.pdf

of theirs:

“An important conclusion to take away from these alternative measures for average markups is that they are different moments of a much richer distribution of markups. We have documented that the distribution has a fairly constant median, that the upper tail has become a lot fatter, and that within a market, larger firms tend to have higher markups. For example, input weighted markups are lower than sales weighted markups because as market power rises, firms raise prices and sales, but they produces less, and as a result they reduce inputs (employment and materials).”

So, am I missing something?!

The differentiation between what you call R&D and other kind of labor doesn’t present a theoretical challenge to Marxism because it comes from alienation that arises with increasing technical division of labor.

You’re right: R&D is labor force. Just because it is “immaterial” doesn’t mean it isn’t a commodity. That’s because, in capitalism, human beings are commodities too, with a precise cost of reproduction depending on the class it belongs — and that includes scientists and intellectuals.

The distinction between intellectual and manual labor exists since at least Ancient Greece and is not a capitalist invention.

vk could you explain this a little more?:

“…it comes from alienation that arises with increasing technical division of labor”

As the development of the productive forces advance/evolve, complexity of production rises, which increases horizontal (technical) division of labor. To put it in simpler terms, work becomes more vast and complex, even though, from the individual worker’s point of view, working seems to be simpler.

In capitalism, development of productive forces only happen in the direction of rising labor productivity (“output” per worker in money terms). That means that, as horizontal division of labor increases, so does vertical (hierarchical) division of labor: a lot of workers are turned redundant, but an ever tinier elite of workers (who knows how to maintain the new, “high tech”, machines) becomes ever more well-paid than the rest.

This “labor aristocracy” is what many propagandise in the West nowadays as the “immaterial work”, “intellectual work” or, as many liked to denominate in pre-2008 USA, “smart jobs” (as opposed to the sweatshops outsourced to China and India). However, this denomination hides the reality they are still working class, since what determines class are the relations of production, not the technical nature of the job. Hence why, e.g., many workers of the “smart jobs” sector became homeless overnight after the 2008 meltdown.

OK. But all this doesn’t explain how much value the commodities these workers produce have, and how they realise this value in the market.

Mind that there are workers also in advertising or banking but they don’t produce any value.

“a. The R&D, i.e., the production of prototypes (chemical synthesis, musical synthesis, algorithms, software, movies, machine designs etc) is more and more separated from the massive production of commodities.” This is correct and has major consequences for capital accumulation and for the economic situation of the working class in the class struggle. These are modeled in “The Hollow Colossus, chapters two and three.

With regard to R&D, I have analysed and written much on the subject. The 2012 revisions to the SNA which converted R&D from a cost into capital by means of an inputed (fictitious) final sale has inflated IP and led to duplicated depreciation which had had the bizarre outcome of deflating corporate profits when the opposite is the case. Your concerns I woul suggest are misplaced. The question should be posed, what is the effect of the balance between intellectual labour and physical labour on the rate of profit when intellectual labour revalues inputs while devaluing output. Finally the churn of corporations in the Dow Jones for example is increasing rather than decreasing thought this may change after the Crash of 2019.

A lynch-pin of neo-liberal economic assumptions behind all the maths is that no market actor is large enough to affect the market overall. If they are now saying that the market is not like that – why then coach and horses surely?

Thanks. Interesting piece. There were similar concerns raised by David Allen Green (will check later) a noted constitutional lawyer. He pointed out that earlier precedent has been established so that there is no way the Govmt. can get round the Benn Act…..

“””The second form Marx called ‘differential rent’ “””

The concept of “differential rent” was invented by David Ricardo.

More than a century later Karl Marx copied Ricardo’s idea without saying it was Ricardo’s. A plagiarism without discursion.

In addition, since differential rent proves that the Labor-Value Law is not fulfilled, Marx takes a long time to explain the differential rent, making it unintelligible.

Marxists should know that Marx did not invent differential rent, but appropriated it. Showing very little honesty.

Nonsense Marx critiqued Ricardo’s theory of rent in detail https://www.marxists.org/archive/marx/works/1863/theories-surplus-value/ch10.htm

This piece of text is everything Karl Max says about David Ricardo’s Differential Rent Theory…….. In detail?????

…….”””[Secondly:] The Ricardian Theory: Absolute rent does not exist, only a differential rent. Here too, the price of the agricultural products that bear rent is above their individual value, and in so far as rent exists at all, it does so through the excess of the price of agricultural products over their value. Only here this excess of price over value does not contradict the general theory of value (although the fact remains) because within each sphere of production the value of the commodities belonging to it is not determined by the individual value of the commodity but by its value as modified by the general conditions of production of that sphere. Here, too, the price of the rent-bearing products is a monopoly price, a monopoly however as it occurs in all spheres of industry and only becomes permanent in this one, hence assuming the form of rent as distinct from excess profit. Here too, it is an excess of demand over supply or, what amounts to the same thing, that the additional demand cannot be satisfied by an additional supply at prices corresponding to those of the original supply, before its prices were forced up by the excess of demand over supply. Here too, rent comes into being (differential rent) because of excess of price over value, [brought about by] the rise of prices on the better land above the value of the product, and this leads to the additional supply.””””….

Michael Roberts says:

“” Marx critiqued Ricardo’s theory of rent in detail.””

In detail???????????

”More than a century later Karl Marx copied Ricardo’s idea without saying it was Ricardo’s. A plagiarism without discursion….. Showing very little honesty.” Will rojaspedro have the honesty enough to inform us whether he has read Vol.3 of ‘Capital’ ?

Also, how many years in Pedro’s century?

No, I have not read “Capital.”

My parents have forbidden me to read religious books.

”My parents have forbidden me to read religious books.”

Evidently they must have forbidden you also to learn to count.

P.S. 100 years in a century.

… in economy the accounts never leave … excuse me !!!

Marx theory of rent is completely different from Ricardo’s. What may have happened is Marx used the same terminology but that’s it.

How is it different?

Karl Marx uses the same name because his idea is nothing different.

That’s why the lack of honesty.

If I remember well, Lenin in his Imperialism used the word “rentiers” in the characterization of the financial capitalists who have no productive activity whatsoever, but gain immense amount of profits, just because they own money.

Yes

Just found interesting the convergence in terminology between those who all of a sudden discovered that “bad capitalism is bad”, and those who had realized some 100-150 years before already that the financialization of capitalism is inevitable (as are monopolies, even temporary as you developed) and “bad capitalism” is just a consequence of “capitalism being bad” for fundamental reasons.

Again if I remember well, Lenin explains how crises result in individual monopolies and trusts being temporary, and that capitalism inevitably produces a reopening of the market to competition, and the cycle (or more accurately spiral) repeats all over again. I don’t remember if he included revolutions in the means production in that mechanism though.

Thanks for the thorough analysis.

Thank you, very interesting.

Is it not that due to falling profitability from production, especially in IT with “zero marginal costs”, monopolies have to be built to sustain profits? You mention it in one place. Then Wolff’s correlation of bad economic performance and rentier capitalism is correct but the suggested causality goes in the wrong direction (but in fact goes from the former to the latter). Could destroying the monopolies of the FAANGS and others even worsen the state of the economy because overall profitability falls?

The Law of Decreasing Profit Rate is a powerful economic law, but it must be integrated into this correct sequence of laws and economic phenomena. Explanatory sequence of the modes of production until today, in my opinion:

1º.- Law of Concentration of the capital-object. Economies of scale demand and force this concentration. This phenomenon, historical and permanent, drags with it, only initially, to the concentration of the subject-capital (the owners)

2º.-Law of Decreasing Profit Rate.- Monopoly companies capture markets and eliminate small and medium enterprises and their employment. The rate of profit goes up and down for monopolistic and non-monopolistic companies according to the stage of development in which the revolutionary cycle is.

3rd.- Revolutionary cycle. Losing economic subjects (small businessmen and workers) of the concentration of the subject-capital, subjects with a decreasing rate of profit only in the regressive phase of the cycle, cause political ruptures. Rupture is equal to Economic Impulses according to Ragnar Frisch and equal to Revolutionary Impulses according to Rosa Luxemburg. In the progressive phase of the cycle, ownership of productive capital is expanded in number of proprietary individuals. This is the case in (1,789) Revol. French and Capitalism and (1.917-1980) Russian Revolution and Socialism. The Profit Rate grows for all companies in the market in the progressive phase of the cycle.And in the regressive phase (1980- ¿) there is the monopolization of markets, unemployment, and an increasing rate of profits in monopolistic companies and rates decreasing in non-monopolistic. The number of subject owners of capital is reduced (privatization of the Socialist State and the OECD Social State in the twentieth and twenty-first century // European Restoration in the nineteenth century) ,. Succeeding the regressive phase until the new break and the momentum of the next cycle.

Otherwise: the Decreasing Profit Rate, but ONLY of the non-monopolistic subjects and companies, explains and is the origin of the Revolutionary Cycles, but without the thesis of that cycle the advances and setbacks of the modes of production. The thesis of the revolutionary cycle is the thesis of impulses as a current scientific paradigm and factor explaining economic fluctuations.

That said from the point of view of a modest business economist, expressed without flaunting academic formulation and without large doses of empirical evidence. And said with the sole desire to spark the debate and progress of socialist economic science. And the desire to provoke the action, just a little, of a great Marxist macro-economist like M. R.

Greetings,

Funnily this discussion is over a dead issue. Most analysts from Goldman to others speculate that the growth in returns for the S&P 500 over the next five to ten years will be non existent. This means their are no “monopolies” to drive the stock market. As for financialisation the cookies are coming home to roost as the New York FED has to refloat the money markets so hedge funds, other non-bank entities and regional banks (especially Texan banks) can keep their heads above water. The real world is so much more interesting and each time it proves Marx right.

1 .- ‘’ Most analysts from Goldman to others speculate that the growth in returns for the S&P 500 over the next five to ten years will be non existent ’’.

This speculation does not match, nothing gives anything, with this other empirical research work not speculative (linked by Dionysios Perdikis in this article).

Click to access 5d6436733e910486884d1c8f64eee6ebecf1.pdf

And it does not coincide with many other academic works that show that monopolists (oligopolies, in reality) today are increasing their profits.

2.- It does not matter if the Dow Jones index (or the Forbes list of billionaires) suffers or not more and more rotation (it is true that if they rotate) in the names of their companies and component individuals, the factor that determines the existence of concentration and monopoly in the markets is not the existence of the same leading companies but the existence of FEWS AND SCALES and less and less companies. Few and scarce and possessing increasing market power.

3 .- Yes, the growing monopoly will not give value to Wall Street, or any other stock exchange, or anything else, but that is another problem.

Regards

Who knew cookies had roosts?

The aberration in capitalism – as I see it – was the so called golden age. When capitalistic states had to defend their legitimity by creating a competing workers paradise. In the 1970-ies the private capitalists in Sweden had given up a big part of the ownership to the total national ownership to the state (Offentlig sektor orange line) https://ekonomistas.files.wordpress.com/2015/10/image1.png and the state acted as employer as according to Engels, as an ideal total capitalist.

I think that ideal capitalism, where competition forced capitalists to develop higher and higher productivity reached its end at the long depression in the late 19th century. Thereafter we have monopoly capitalism, which could chose the speed of development. At least when they had to in order to defend the survival of their class in the whole capitalistic world.

The Golden Age of Capitalism, 1945-1975, called Les Trente Glorieuse by French economists, has little capitalist and if it has a lot of socialist. Why? Because some countries (all OECD) that multiply by 5 or 6 their State as an economic agent to reach public GDP of 60% of the total, were only applying, in economic rigor, a measure of socialist type. Only that.

In addition, from the point of view of the thesis of the Revolutionary Cycle (also called the subject-capital cycle, the cycle of capital ownership), that period is a progressive phase, of progress, in the revolutionary cycle initiated in 1917. Some brief relevant characteristics of this progressive phase.

a) Growth of the State as an economic agent. From 10% in the first decade of the 20th century to 60/70% of Nordic countries. State equal to new economic subject, equal to Social Property of the socialist model. Equal to extension of the number of owners of the property of the means of production.

b) More Economy: notable improvement of all the variables that affect employees: almost full employment, rising wages, quality public professional training that leads to increases in the Total Productivity of companies, etc …

Withdrawal in the Law of Concentration of Capital-Object. Reduction of monopolies, markets with more competition. Increasing Profit Rate for most of the market.

c) A little politics. Government of progressive parties (socialists, social democrats), extension of social and individual rights: feminism, sexual freedom (May 68), etc …

On the contrary, a regressive phase (from 80 to?) Contains ALL the economic-political elements and variables of the progressive phase walking in the opposite direction. That is, going back, in reactionary regression. Especially the backward elements of the State (its privatization) and the rise, again, of the far-right parties and their reactionary policies.

‘Otherwise: the Decreasing Profit Rate, but ONLY of the non-monopolistic subjects and companies, explains and is the origin of the Revolutionary Cycles, but without the thesis of that cycle the advances and setbacks of the modes of production’

This incomplete phrase should be formulated as follows: without the law of revolutionary cycles (the Rate of Decreasing Profit is insufficient explanation) the advances and setbacks of the modes of production are not explained or understood. The advances and setbacks of the socialist model in the twentieth and twenty-first century and the movements of the capitalist model in the nineteenth century are not understood. The cycles of Kondratiev are the revolutionary cycles of capitalism. Ragnar Frisch (the impulses and their propagations) and Rosa Luxemburg and their revolutionary impulse with phase of progress and regression (in their work Reformation and Revolution) study and theoretically endorse the thesis of the cycle.

Greetings,

I’m no economist, won’t even pretend I know Harpo from Karl (obviously I do but after that it’s still all pretense…).

But I know rent-seeking when I see it, and America has devolved into a state of caste politics in service to wage suppression and net exfiltration of productivity (or as that dangerous mind Will Rogers originally termed it, “trickle up”).

Sprinkle in rent-making patronage (privatization… ), legalized political bribes (super-PACs), winner-takes-all elections (isolates solidarity, favors money), reactionary agitprop & a resurgent Dixie Brahmin (our masters of caste, plantation models, & mint juleps) to divide labour against itself, and we have a perfect recipe for rentier stagnation.

The hoi polloi are slowly catching on, but lack the vernacular for, you know, being pickpocketed by their betters. Abetting in one’s own penury is either masochistic or stupid, so let’s keep up the charade out of vain pride, one more turn at the slot machine aka the voting booth. It helps if my witless principles are stroked nicely, yes that’ll do, lower.