Last Thursday, Mario Draghi, the current head of the European Central bank, soon to be replaced by Christine Lagarde from the IMF, announced a parting gift to banks and financial markets. The ECB decided to reintroduce its bond purchasing programme in order to inject yet more billions into Europe’s banks in order to persuade them to lend onto industry and boost lagging growth.

This was the return of quantitative easing (QE) by the ECB. But this time there was to be no time limit on the E20bn monthly of ECB purchases. It was to be forever – QE to infinity! Also, the ECB would purchase not just the government bonds of debt-ridden Italy, Spain etc but also much riskier assets like corporate bonds.

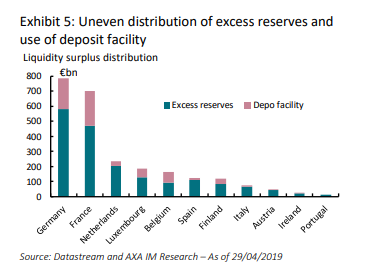

Draghi also announced a new two-tier interest rate system for bank cash reserves held at the central bank. These reserves have spiralled as banks took cash from ECB purchases of government bonds they held, but instead of lending that cash on in loans to the wider economy, the banks just put them back in the central bank as deposits.

The ECB decided the the interest rate was to be held at zero for excess reserves, thus making sure that banks could not lose money if they were forced to offer negative rates to their borrowers. Banks can now also raise funds at negative rates and deposit these funds at the central bank up to six times the required reserve amount and get a zero rate, thus boosting profitability.

This two-tiered idea is seen by some mainstream monetary economists as revolutionary. In effect, the ECB is boosting bank profits with its own capital at risk. Bank profits rise while the ECB buys government bonds at prices which offer negative rates and banks with large excess reserves’ can lend at a profit to those with low reserves. But this ‘revolutionary’ policy is just about the last desperate measure of unconventional monetary policy.

The monetarists are hopeful that boosting bank profitability will lead to an expansion of lending to business and households and get the Eurozone out of its renewing depression. This assumes that the problem is the banks not being prepared to lend because it is not profitable for them. But is that the reason for low loan growth rates and investment? It’s not the supply of money or bank profitability that is the problem, but the demand for loans. Nobody wants to borrow to invest or spend even at zero or negative rates, because revenues and profits are stagnant, inflation and wage growth are low and, above all, export trade has collapsed.

You can take a horse to water (and you can make it a huge lake of water) but you cannot make it drink if it is not thirsty. Even the central bankers, like Draghi, are admitting now that monetary policy has failed. And even supporters of the revolutionary new policy are not confident: “Dual rates is monetary rocket-fuel. In contrast to standard negative rates, to forward guidance, or QE, the marginal effects of these policies are increasingly powerful. I am not convinced that this specific combination of measures will suffice to generate enough demand to create an acceleration in Eurozone activity – but it will help.” Eric Lonergan.

The great new instrument to save capitalism from stagnation or a new slump is fiscal policy. “There are more and more people saying that monetary policy cannot be the only game in town, and if you don’t want more and more monetary policy the only instrument that is left is fiscal policy.” Ex-ECB board member.

Draghi called for action by European governments, particularly those with ‘fiscal space’, eg Germany to run budget deficits and spend. So far, Germany has been reluctant to do so. But if it decides to up the ante fiscally, then we can test the Keynesian solution to capitalist recessions. I’ll make a prediction: that won’t work either.

Thought the ECB has been paying/collecting negative interest rates on bank deposits for awhile. This latest round sees another cut of 10 basis points, no?

As for Eurozone external trade, if I’m reading the Eurostat numbers right, while trade did drop off in June 2019, with numbers below May 2019 and June 2018, through the first 6 months of 2019, trade is up 2.2 percent.

German industrial output is plummeting during this same time frame.

If trade is up 2.2%, then it must either be at a (much) lower aggregate value or it must be an increase in imports thing.

Try looking at the numbers before you draw your conclusions.

Well, you didn’t mention your source, so I assumed you were just small talking because I can’t verify your affirmation.

I’m not a native English speaker. In my language, trade = import + export. You can have a rise in trade by simply rising imports. Not sure if it means the exact same thing in English (unless “trade” is short for “trade balance”).

If it means “trade balance”, then it could simply indicate imports fell at a higher rate than exports (or that exports grew at a higher rate than imports). It means nothing in the context of this post.

“Well, you didn’t mention your source, so I assumed you were just small talking because I can’t verify your affirmation.”

Really? Read it again. I identified the source, Eurostat. You can look it up, and in English, French, or German.

I don’t waste my time and others’ “small talking”– or making up false figures.

Yes, the ecb has been setting its repo rate at below zero and has now reduced it by10bp to 0.5%

But I was referring to its new bond purchase policy and the rate it pays on bank reserves held at the ecb. The ecb will buy bonds from banks that pay negative rates but pay excess reserves at a minimum of zero so the banks will increase profitability as they can raise cash and get paid for it. This is supposedly a revolutionary move.

As for ez external trade balance, you are right that there is still growth. Indeed first estimates for jan-July shows a rise of about 5% although that’s mainly due to slowing imports. But exports are up 3.6%. Intra ez trade is up only 1.9% but still up. The reason for referring to trade is that ez trade growth is slowing as it is everywhere and particularly in Germany where exports are virtually flat and trade surplus is down 8%

The issue isn’t that you referred to trade, or that trade is slowing; it’s that you said export trade has “collapsed,” and that the collapse “above all” is the reason “nobody wants to borrow or invest.” Trade has not collapsed, at least not yet, not like it did in 2009, and when and if it does, that will be a product, not a cause, of the root problem, which is persistent overcapacity, resulting in persistent overproduction.

Michael, your work is great but it would be better if you did more proofreading before posting items that can sometimes be tricky to make sense of because of writing issues that are easy to overcome.

Apologies for any typos etc but I just checked and did not find too many this time. Will try harder.

The metaphor would only make sense if the proverbial horse is alive.

The European Dream is over. Draghi dragged the dead corpse of the European horse to the lake and begun to hysterically shout its lifeless body to drink.

Maybe that’s what buying bonds with negative rates is akin to, a rotting corpse, food for ghouls. Even scavengers must drink.

“Pushing on a string”, is the often chosen description of this policy. Futile is the end result. I’m trying to read about the Reconstruction Finance Corporation which operated from 1932 to 1952. After WWII it was phased out. In the 30s it saved mostly solvent banks with emergency loans, and it bought railroad company debt. Mostly in the 1930s the WPA was the conduit of money, it transferred money directly to workers and families, it was direct job creation, the rate of unemployment dropped from 25% to 9.6%, 1933 to 1937. Keynes also had a solution for perpetual surplus nations, the creation of an International Monetary Clearing Union. This would prevent the race-to-the-bottom in wages that we see with China-US trade. And in the case of Germany, or any surplus-mercantilistic nation, it would require the surplus funds to be invested in the deficit countries. From Paul Davidson’s book The Keynes Solution, page 138: It would encourage creditor nations to “spend these excess credits in three ways: 1.) on the products of any other IMCU member (import more); 2.) on new direct foreign investment in projects in other IMCU member nations (projects, not financial assets); 3.) provide foreign aid similar to the Marshall Plan. And a fourth, maybe, raise wage income in the surplus nation such as increased Earned Income Tax Credits. It’s all about aggregate demand and a balance of income distribution, within each nation and between nations. Direct job creation is a good part of the Green New Deal, some of it targeted to specific low-income communities and geographies. But most of it spent on upgrades and transitions to renewable energy. I’m not sure what Marxists are calling for, but this is state-managed capitalism, and it may lead to the more socialized condition of a world economy. My blog: http://benL88.blogspot.com

Nor would Keneysian fiscal policy work to stop the recession that comes, especially if it is done in ridiculous and meager amounts, nor … will it be carried out. Why not? Public Expenditure (and public company) has been reducing since the 1980s. Because it is precisely the reduction and jarrization of the State, the elimination of a phenomenal competitor in the markets and the corresponding and succulent appropriation of its economic structures and client portfolio what is ongoing since the eighties. How will the capitalist elites allow the increase in public spending today, an increase that, however small and unsatisfactory, they know, will increase the tax revenue to pay for that expense, even if the Central Bank and the MMT are used. The current government revenue that is neoliberal almost all of the OECD? Tax revenues that are reduced every year from the 80s (10% reduction / GDP in Spain to 37%). Does this theoretical and real end have that state cut? Remember that BEFORE the Russian socialist revolution in 1917, the State and its total economic activity only reached 10% of GDP in the entire World System. As far as I know, that is an economic phenomenon of state reduction is unstoppable … except revolution. Yes, and as far as I know, that reduction of the State is a consequence of a regressive phase of a revolutionary cycle. In its final step.

On the new banking profits that Mr. Draghi has prepared for the bank in his farewell (to which bank does he go on his golden retirement?) With his Q.E. infinite and the double-level interest rate, just to say that this supposedly and falsely capitalist profit, only adds to the list of ‘socialist’ earnings (100% of its profits?): that banks already have today: 1.- carry and trade Central and State, 2.-QE, 3.- Ladying, etc. Only by the variable lady the excellent Mexican economist Alejandro Nadal calculates that the English bank obtains 23,000 million pounds sterling, a 1.2 % of GDP

http://www.sinpermiso.info/print/textos/creacionmonetaria-y-senorajede-los-bancos-privados

Regards

But if the State comes back, then it will have to invest in the “real economy”, with very low to none profit rate, and with serious and very long term planning of the economy — all that at the expense of big business. That would basically mean a complete transition to socialism.

And you got your history wrong: it wasn’t that there was a neoliberal invasion in 1980. Neoliberalism existed since the 1930s. It was the “keynesian consensus” that collapsed over its own contradictions in 1974-5 that opened the field for the “return of the liberals” (i.e. rise of neoliberalism).

1.- No, I have not said that the State is returning, I have said EVERYTHING AGAINST. I have said that they have been reducing it since the 1980s, and that the economic-political phenomenon is unstoppable except for revolution. Any problem with your English translator? Mine gives them.

2.- First you say that neoliberalism does not develop in the 80s according to my idea. Then you say that he was born in 1930 (with which intellectuals and politicians?). Finally, you say that neoliberalism arises after 1974-1975 due to the collapse of the Keynesian consensus. In other words, you end up giving me the reason. All of the above says it in the same paragraph!

Yes: neoliberalism was a loser for 55 years before finding its opportunity to shine in 1979.

As a doctrine/ideology, it was codified, if memory doesn’t fail me, in 1936 (the event that founded the Mont Pelerin Society).

*45 years.

@michael roberts.

Im not an economist but if I understand it right.

ECB has set an artificial limit to 33%.

ECB buying bonds wont save us from a crisis but are there any chances they manage to delay one?

And if they manage to delay one how long can it be delay?

How long can ECB keeps buying bonds before it becomes a problem?

We are close to 33% is 50% a breaking point? 80%?

You say that the Keynesian solution will not work, why? I ask him. Thank you