Last week, the prestigious Brooking Institution held a conference on the efficacy of monetary policy in stimulating and sustaining economic growth. At the conference, Larry Summers, former US Treasury secretary and professor at Harvard University and Lukasz Rachel of the Bank of England, presented a paper that aimed to revive, yet again, the idea that the major capitalist economies are locked into ‘secular stagnation’: “Our findings support the idea that, absent offsetting policies, mature industrial economies are prone to secular stagnation.”

According this thesis, there is a long-term stagnation in the major capitalist economies. Despite central banks pushing interest rates down to zero or even below (so that bankers and capitalists are paid to borrow!); and despite central banks printing huge amounts of money to buy bonds and other financial assets (quantitative easing), real GDP growth and investment remain weak. Although unemployment rates are officially near cycle lows in many countries, inflation is equally low, confounding the traditional Keynesian view that there is a trade-off between employment and inflation (the so-called Phillips curve).

Central bank monetary stimulation has failed, except to promote ‘credit bubbles’ and speculation in financial assets and property. For example, here are the conclusions of a recent study on the impact of the monetary injections of the ECB in Europe: “the efforts of the ECB to hit its inflation target would be more credible if there was convincing empirical evidence that its balance sheet policies are effective at stimulating output and inflation. Our recent research shows that this macroeconomic evidence is still lacking.”

And there is every prospect of another economic slump approaching in which central banks will be powerless to do anything as interest rates are already near zero and the balance sheets of central banks are already at record highs. “Our findings support the idea that, absent offsetting policies, mature industrial economies are prone to secular stagnation. This raises profound questions about stabilization policy going forward.” (Summers and Rachel)

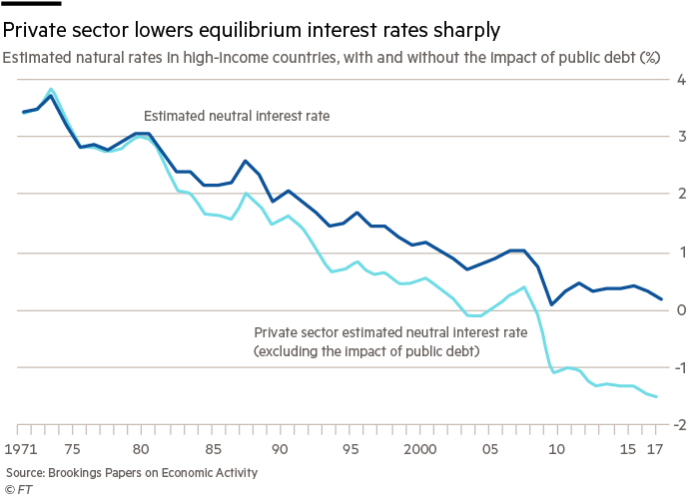

In the FT, Keynesian columnist Martin Wolf echoed the views of Summers and Rachel. Interest rates are near all-time lows and if you follow the Fisher-Wicksell theory of a ‘natural’ rate of interest that enables full employment, then it now seems that the natural ‘private sector’ interest rate needed to achieve jobs for all who want them has be in negative territory.

Of course, this so-called natural rate is a dubious concept at best. But even you accept the theory, as it seems many Keynesians want to do [“That is the root of our problem: the natural nominal rate of interest … today is less than zero, and so the Federal Reserve cannot push the market nominal rate of interest down low enough.” Brad DeLong], it just exposes the problem. Monetary policy has not and will not work in restoring the capitalist economy to a pace of growth that delivers investment and thus sustains jobs at rising real wages.

Indeed, as I have pointed out before, Keynes also realised after the Great Depression continued deep into the 1930s, that his advocacy of low interest rates and even ‘unconventional’ monetary policy (buying government bonds and printing money) was not working: ““I am now somewhat sceptical of the success of a merely monetary policy directed towards influencing the rate of interest… since it seems likely that the fluctuations in the market estimation of the marginal efficiency of different types of capital, calculated on the principles I have described above, will be too great to be offset by any practicable changes in the rate of interest”. In other words, there is no natural rate of interest low enough to persuade capitalists to borrow and invest if they think the return on that investment would be too low. You can take a horse to water, but you cannot make it drink.

This week the Bank of Japan monetary committee met and threw up its hands in despair. After years of central bank ‘unconventional’ monetary easing (buying government bonds to the tune of 100% of GDP!) by printing money, the huge injection of credit into the banks has had no effect in lifting the economy. As Darren Aw, Asia economist with Capital Economics, remarked: “There is a good chance that Japan’s economy will contract again in Q1 2019, for a third time in five quarters”… Given this, the key question for the Bank of Japan is no longer when it might retreat from its ultra-loose policy stance but whether it can do any more to support the economy.” Thus the first of the PM Abe’s three arrows of economic policy (monetary easing, fiscal stimulus and neoliberal de-regulation) has failed.

Now it’s true that per capita GDP growth in Japan since the end of the Great Recession ten years ago is actually faster than in most other major capitalist economies. But that is simply because Japan has a sharply falling population. Real and nominal (before inflation) GDP has been virtually static. National output has remained more or less the same but there are less people that generate and consume it. Japan has the lowest working population as ratio to total population in the top 12 economies of the world.

And yet monetary easing is still pushed by Keynesians, especially the more radical ones from the post-Keynesian school, including those following Modern Monetary Theory (MMT). If the state and/or central bank prints money, it can use that money to stimulate the capitalist economy to get it going. Money is not so much the root of all evil but the genesis of all that is good, it seems. This sentiment reminds me of the earliest exponent of the magic of money – or the ‘money fetish’, namely John Law, who around 300 years ago had a unique opportunity to apply money printing to put an economy on its feet.

Ann Pettifor, the left Keynesian exponent of magic money, has called John Law a “much maligned genius whose 1705 account of the nature of money cannot be bettered”. This proto-Keynesian was the son of a wealthy Scottish goldsmith and banker. Law was born in Edinburgh, proceeding to squander his father’s substantial inheritance on gambling and fast living. Convicted of killing a love rival in a duel in London in 1694, Law bribed his way out of prison and escaped to the Continent. There Law concentrated on developing and publishing his monetary theory cum scheme, which he presented to the Scottish Parliament in 1705, publishing the memorandum the same year in a tract, Money and Trade Considered, with a Proposal for Supplying the Nation with Money (1705).

Law argued for a central bank to issue paper money backed by ‘the land of the nation’. Echoing the MMT (or is it the other way round?), Law proposed to “supply the nation” with a sufficiency of money. This would vivify trade and increase employment and production. Like MMT, Law stressed money is a mere government creation which had no intrinsic value. Its only function is to be a medium of exchange and not any store of value for the future.

Law was sure that any increased money supply and bank credit would not raise prices and expanding bank credit and bank money would push down the rate of interest (MMT again). To Law, as to Keynes after him, the main enemy of his scheme was the menace of “hoarding,” a practice that would defeat the purpose of greater spending. So, like the late 19th-century German money fetisher Silvio Gesell, Law proposed a statute that would prohibit the hoarding of money.

Amazingly Law found a supporter for his theories in the regent of France. The regent, the Duke of Orléans, set up Law as head of the Banque Générale in 1716, a central bank with a grant of the monopoly of the issue of bank notes in France. He was made the head of the new Mississippi Company, as well as director-general of French finances. The Mississippi Company issued bonds that were allegedly “backed” by the vast, undeveloped land that the French government owned in the Louisiana territory in North America.

This scheme eventually led, not to a booming economy, but instead to a speculative financial bubble where bonds, bank credit, prices, and monetary values skyrocketed from 1717 to 1720. Finally, in 1720, the bubble collapsed and Law ended up as a pauper heavily in debt, forced once again to flee the country. Law was not so much a ‘much maligned genius’ but more “a pleasant character mixture of swindler and prophet” Karl Marx (1894: p.441). What the Law debacle showed was that the state just issuing money cannot replace the ‘real economy’ of production and trade. Money alone does not create investment or production.

Of course, modern Keynesians (unless they are of the MMT variety) do not promote unending printing of money for governments and the private sector to spend. That’s because they have been forced to recognise; as John Law found in 1719-20; and as Keynes found in 1933; and as Abe in Japan has found now; and the secular stagnationists also accept, printing money does not work if capitalists and bankers hoard that money or switch it into speculative investments in financial assets.

So what’s the answer? Well, as Martin Wolf puts it: “The credibility of the “secular stagnation” thesis and our unhappy experience with the impact of monetary policy prove that we have come to rely far too heavily on central banks. But they cannot manage secular stagnation successfully. If anything, they make the problem worse, in the long run. We need other instruments. Fiscal policy is the place to start.” Yes, it’s back to fiscal stimulus. But will that work either?

Last year President Trump launched a fiscal stimulus of sorts by cutting taxes for the rich and the big corporations. It boosted after-tax profits in 2017 sharply and real GDP growth ticked up a little towards 3% a year. But that boost has been all too fleeting. US real GDP growth is heading back down to below a 1% rate in this quarter and business investment is also turning down.

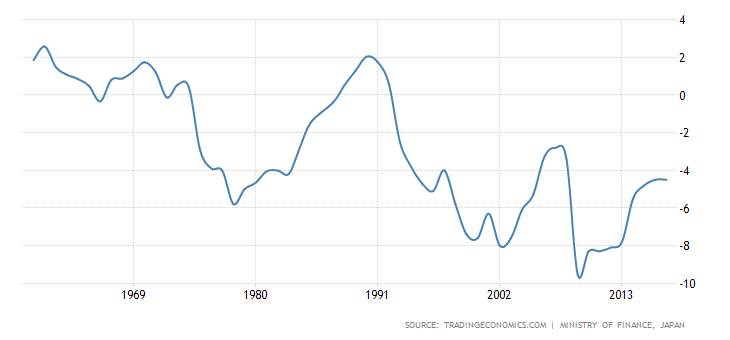

One of the policy arrows of Abenomics in Japan was fiscal stimulus. Indeed, there is no major economy that can match Japan for its government running permanent budget deficits (MMT-style).

Japan: annual budget deficits to GDP (%)

This should be the policy dream of MMT and other post-Keynesians. But it has not worked in Japan. Japan has ‘full employment’, but at low wages and with temporary and part-time contracts for many (particularly women). Real household consumption has risen at only 0.4% a year since 2007, less than half the rate before. So fiscal stimulus has not worked in Japan which remains in ‘secular stagnation’.

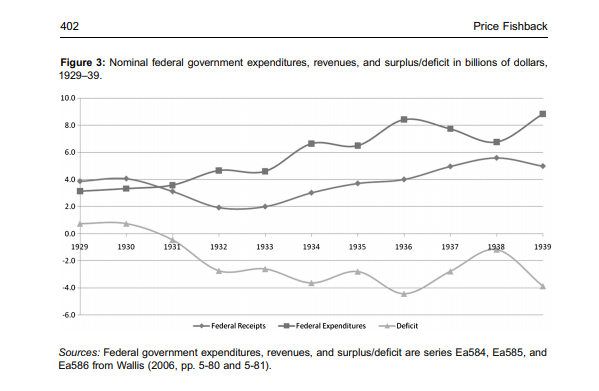

And it did not work in the Great Depression of the 1930s. After dropping monetary easing as the policy answer to the depression, in the Los Angeles Times on 31 December 1933, Keynes wrote: ‘Thus, as the prime mover in the first stage of the technique of recovery, I lay overwhelming emphasis on the increase of national purchasing power resulting from governmental expenditure which is financed by loans and is not merely a transfer through taxation from existing incomes. Nothing else counts in comparison with this.’ Deficit-financing was the answer.

The Roosevelt regime ran consistent budget deficits of around 5% of GDP from 1931 onwards, spending twice as much as tax revenue. And the government took on lots more workers on jobs programmes (MMT-style) – but all to little effect. The New Deal under Roosevelt did not end the Great Depression. Keynes summed it up “It is, it seems, politically impossible for a capitalistic democracy to organize expenditure on the scale necessary to make the grand experiments which would prove my case — except in war conditions,” (from The New Republic (quoted from P. Renshaw, Journal of Contemporary History 1999 vol. 34 (3) p. 377 -364).

Wolf recognises that fiscal policy may also not work. “It is of course essential to ask how best to use those deficits productively. If the private sector does not wish to invest, the government should decide to do so.” So if the ‘private sector’ (ie the capitalist sector) won’t increase investment rates to boost growth despite negative interest rates and despite huge government money injections funded by money printing, the government will have to step in do the job itself, apparently.

Thus, the Keynesian/MMT answer is to act as a backstop to capitalist failure. But the capitalist sector dominates investment decisions and it makes those on the basis of potential profitability, not on the cost of borrowing. Keynes saw it as politically impossible to ensure sufficient investment through government spending – and he was right in a way. Only complete control of the capitalist sector could enable governments to ensure full employment at decent wages. At this point, I’m tempted to repeat the comment of left Keynesian Joan Robinson to MMT/Keynesians: “Any government which had both the power and will to remedy the major defects of the capitalist system would have the will and power to abolish it altogether”.

You write: “If the state and/or central bank prints money, it can use that money to stimulate the capitalist economy to get it going.”

A question: If a non-capitalist state wanted to stimulate non-capitalist economic activity, how would it go about doing that?

Printing money for the government to pay workers to produce goods, services and infrastructure would be fine with me, but it wouldn’t address the fundamental problem of the wage system i.e. the social relation of Capital, nor would it be sustainable because the money commodity represents wealth and to the degree that it doesn’t, its only worth the paper it’s printed on, for wealth has two sources: goods and services produced by wage-slaves doing their socially necessary labour time and natural resources.

Official inflation has not moved up much more than 2% per annum. In my book though, inflation is measured by prices being higher than they should over value. A lot of the prices of assets are inflated, IMO. For example, housing is way over priced in Australia and this is because the supply of housing is kept down in the face of increasing demand. I’d say the same for insurance and other financial services. Speculative ventures into the market place of commodities create the illusion of value. By increasing the price over value what you have in hand is fictitious capital. There was a lot of fictitious capital inflating asset values before the GFC–e.g. Collateralized Debt Obligations and other parts of the finance sector, including insurance and real estate.

Inflation is calculated according to a predetermined “goods basket”. This “basket” is decided by the government, and varies depending on the country.

My knowledge over the fact is scarce, but here in Brazil housing is not part of the IPCA (the Brazilian “goods basket”), so it doesn’t affect official inflation. Brazil has a separate index to measure housing prices and rent (and there are many: they vary according to the region). Usually, they are part of the subsistence use value (essential food, water, electricity etc.).

Some products are not in the calculus directly, but they influence inflation indirectly. E.g. fuel (which tends to affect prices of transport of goods which are in the inflation calculus). So, yes, there is a domino effect of some kind.

You have to go to your country’s government website and see what products are part of your “basket”. My guess is housing/rent is also not part of the Australian inflation index.

–//–

And financial services for sure don’t enter in the inflation calculus. It simply wouldn’t make sense for a capitalist government to do so. I know here in Brazil we have at least separate index to measure credit cost to the “consumer” (i.e. the working class).

Right. Lots of commodities with inflated prices are not included in the official rate of inflation. Still, the prices are inflated over value and that includes real estate, which in Australia, is way inflated, but contributes to what the government measures as the GDP. Thus, the GDP is full of a lot of fictitious capital.

Marx’ comments on John Law are actually quite interesting: “The two characteristics immanent in the credit system are, on the one hand, to develop the incentive of capitalist production, enrichment through exploitation of the labour of others…. on the other hand, to constitute the form of transition to a new mode of production. It is this ambiguous nature, which endows the principal spokesmen of credit from Law to Isaac Péreire with the pleasant character mixture of swindler and prophet.”

The credit system constitutes the transition to a new mode of production. “Prophet” is actually a compliment!

We agree on the problem of fictitious capital, i.e. capitalisation of future income streams. (But this has nothing to do with bubbles!) If the interest rate is lower than the growth rate, assets in limited supply (who provide a positive rental income) can just like states sustain ever growing debt burdens. But this problem is not specifically Marxist. Every bourgeois economist including Smith and Ricardo would agree that rent seeking is bad, a form of private taxation. The best remedy is to tax these rents away.

Our disagreement lies in the following inconsistency in your implicit model. Forget about rent, imagine there is only money capital, real capital and workers. What you can’t explain is, how can capitalists go into a capital strike the moment the profit/interest rate reaches zero, but not use this magic ability to stop the profit rate from falling in the first place???

Marx had a good answer: under a gold standard zero is the limit, why investing, if you can hoard your money capital. But Marxists today can’t answer in this way, cause there is no gold standard. We actually operate under John Law’s paper money! So we could enact negative interest rate (and/or higher inflation). If we would do that, why shouldn’t this allow us to operate without positive profits?

I’m not talking politics here. I’m interested in an economic argument why this can’t work.

Alex, marxist’s don’t analyze capitalism’s problems from within political economy’s idealized (strictly economic) version of the capitalism’s mode of production, but from one (historical materialism) which reflects capital’s social relation and its political manifestations.

I’d be interested in Robert’s response to your question, but I think it is already answered in the quote from Joan Robinson (her ironic advice to capitalist reformers in power) at the end of his post.

I understand that. But it’s nevertheless important to distinguish between economics and politics. If someone -in an economy with no output gap- would advocate making everyone richer by doubling the amount of money everyone holds (including doubling debt and long term nominal contracts…) nothing real would have changed, only prices would double. This is not a political problem. Nothing would change, because nominal values are not real values. In this case printing money is like painting food, the amount of food doesn’t rise by painting pictures of it, a picture of an apple won’t feed anyone.

Things change if you don’t believe Say’s law has it right. If -in a monetary economy in contrast to a barter economy- there is no full employment equilibrium, then money matters.

Think about it: how do Marxists explain that in a crisis conditions of profitability get restored? Either by the outright destruction of physical capital or in a deflationary crisis the price of capital goods crashes, so that money capitalists can buy them up cheap. The rate of return on these capital goods rises if I can get them for a fraction of their former price.

Now, a negative interest rate (or inflation) has the same effect. New real capital can now be produced at much lower prices than in the past. This raises its rate of return. So productive investment can be realized, even if the rate of return is zero or negative, so long the rate of return on money capital is even more negative. Positive profitability is no longer a condition for productive investment.

In a way, negative interest rates are like a crisis, but only a crisis for money capital (but this causes also lower price of real capital). They restore conditions of differential profitability (not positive profitability). Capitalists don’t make positive profits, but they lose less by investing than not investing.

Except that rent is essential to the survival of capitalism, even if, depending on you moral set, it is a “necessary evil”: it keeps land (space) in the commodity form and thus in constant circulation.

Imagine if land could be definitely sold, like if it was a normal good. A person could buy a piece of land and never sell it. But that would be a huge problem to capitalism, because capitalism can’t produce space (it can occupy new space, but not create it in the physical, quantum sense of the word).

Assume a city transits from industry to services due to the complicated process of gentrification. Capital would need to use the space once occupied by factories to build cafés, shopping centers etc etc. But what if the owner of the land doesn’t want to sell it? Capital would be unable to do “creative destruction” because of a mere juridic serendipity. And, since space is always useful, the owner could always simply choose to go back to feudalism, re-cultivating the land — unacceptable to capitalism.

The owner of the land will most probably choose to rent it: he will collect rent (money-capital without the having to invest) in exchange to the promise to the capitalist system (to “society”) that he will always leave his land at the services of capitalist accumulation — he’ll rent to the highest bidder, who will invariably have the highest profit rate. It’s that or capitalism would have frequent civil unrest, for each time it would have to substitute a factory with an ice cream shop.

That’s why every capitalist country in the world — even the USA — has a land tax. The owner of the land must always demonstrate to the State he is capable to give his land to “good use”; in capitalism the sincerest proof of love is money, hence land tax must be paid in the form of a certain quantity of it.

That’s one of the main factor that makes China a socialist country: a private individual can never own land there (except in Hong Kong and Taiwan, which are capitalist; and some land that belonged to some peasants before the revolution in some cities). When you “buy” a estate in China, you’re actually purchasing a 70 year lease. That makes land not inheritable (inheritance is the conditio sine qua non of private property). All land in the socialist part of China is “property” of the State, and, therefore, of all the Chinese proletariat.

I have no problem with a land tax. On the contrary, forcing landowners to use their land in the most productive way is a good thing.

My problem is this: when profits/interest rates go to zero, capital values of every asset which still has a positive income stream and can’t be produced (land is the foremost example, you can’t raise supply and there is always demand, people have to live somewhere) will rise sky high. What is often called asset price inflation or bubble, is just a very rational investment strategy in a low interest environment. This creates the illusion of wealth (fictitious capital) and is clearly inferior to investments which raise productivity (education, technology, infrastructure…). To stop this, the underlying income stream has to be taxed away (and redistributed in form of a workers dividend or through public investment). By doing this the capital value of these assets implodes, making the way free for productive investments.

Rent still has to be paid, but not to the asset owner who therefore can’t capitalize this rent. Buying up land just for speculation wouldn’t fly anymore, because holding land with very high site value would become very costly.

Think of it like a permanent auction with the highest bidder getting the right to occupy the land as long as he can outbid everybody else. All proceeds go to the community.

“Marx had a good answer: under a gold standard zero is the limit, why investing, if you can hoard your money capital. But Marxists today can’t answer in this way, cause there is no gold standard.”

Actually, when the price of gold was under that government set standard, that an ounce was worth $36 an ounce, it was the price of the USD which was out of kilter with its value as a commodity. The USD had been inflated in price over its real value and the ruling classes of OPEC knew it, which is why they demanded to be paid in gold. When Nixon closed the gold window to Fort Knox and declared himself a Keynesian, he allowed the dollar to float in the marketplace of commodities and its price then more or less reflected its value as a commodity. What’s the price of gold now as measured in the money commodity known as the USD?

If supply doesn’t change (unemployed workers can’t be hired to produce oil) and demand doesn’t change either, inflating your currency will only produce price inflation. You can’t get oil cheaper by printing money. I agree.

But from a Marxist (and bourgeoisie) perspective income from the ownership of land, oil, gas… are forms of rent. Ideally rents should be taxed away. There should be no privat ownership of assets which provide rental income. The Alaska permanent fund is a good way to do it.

My difference with Michael Roberts turns on real capital: assets that can be produced by workers.

correction: no apostrophe in “marxist’s”. I used to be English teacher until I got old…

If the aim was to avoid deflation then in this sense they were successful.

I’m tempted to repeat the comment of left Keynesian Joan Robinson to MMT/Keynesians: “Any government which had both the power and will to remedy the major defects of the capitalist system would have the will and power to abolish it altogether”. I see. Is this why you argue that China is run along non capitalist lines?

Don’t you think that emedying the defects of a capitalist system has been the role of the government – expansion overseas, investment for war (non profitable for the losing side), and the permanent war economy of the Cold War.

Hello Michael,

In the MMT writings that I have read, Japan is used an example of how the hysteria about the horrors of elevated public debt makes not sense, not like an example to follow.

I have not read any MMT economist that support monetary policy instead of fiscal policy as you suggest. Do you have any link?

Yes, MMTers do not think monetary easing will work – like Keynes. But they do think fiscal deficits will work – like Keynes. Both policy solutions do not provide any permanent or even significant counteracting influence to regular and recurring slumps in capitalist accumulation and production. MMters, like Keynes, see budget deficits as backstops to capital failure. I reckon both theory and evidence show fiscal stimulua to be inadequate and even counter productive.

Thanks for your answer. I admit I have some problems understanding your position (my fault, I’m not an economist). I would be grateful for some clarification.

I have read in your blog that the great depression only finished with the Second World War big spending. That was a (very big) fiscal stimulus and the government didn’t run out of money, just as MMT propose.

Are you saying that a similar fiscal stimulus would be politicaly impossible in peace times? Or that something fundamental have changed and not even a so big stimulus would do the trick? Or, maybe, something else that I don’t realize?

Good questions. In WW2, the difference was both political and economic. All the resources of the economy were diverted to the war effort and the government took control of all investment decisions. Companies had to invest and produce for the war effort. And workers incomes were controlled and consumption reduced (rationed), so household savings were diverted to arms production. Profitability rocketed. In effect, the capitalist sector no longer operated for its own ends (even though industrial sector made big profits from arms production). This was only politically possible because of the war (as Keynes noted) BUT it was also qualitatively different economically from Keynesian-style fiscal stimulus from budget deficits where the capitalist sector still makes the main investment decisions on the basis of profitability. That did not work in the 1930s or in the period post-2009. A war economy might work but that would not be a capitalist economy but a state-directed and controlled economy.

Thanks again for your answer and your patience. If I understand correctly, you agree with MMT, that the government, as they say, “can always afford to buy anything for sale in its own currency” and, as the WW2 example show us, that could make the economy work.

Your problem with this is that, for this to work, the majority of the investment should be controlled by the government and that would be politically impossible to accomplish because, it represents a change from capitalistic economy to a state-directed economy. I hope I get it right.

More or less. The problem that I have with MMT is that just controlling the currency and printing money will not create value (ie profit for the capitalist sector). As the capitalist sector is dominant, more money printing and permanent budget deficits may just boost financial speculation and/or inflation. MMTers say it wont because the government could stop printing money when full employment is achieved. That’s not so easy to manage as experience has shown. More important, recurring crises of unemployment and underinvestment are not resolved by MMT policy as that depends on the profitability of capital. So MMT acts only as an (inadequate) backstop to capitalist failure (recessions). MMT then is not a complement to socialism but a weak alternative. So it is no different than orthodox Keynesian policies.

Quick question related to historic low interest rates. If the cost of borrowing is extremely low would that at least have some impact on potential profitability of a capital investment?

It may help but on the whole seems to be insufficient in restoring the profitability of investment in most slumps

Simple question: Why do you think Martin Wolf is a Keynesian? I know he is much more skeptical of free markets and globalisation since 2007 (much to his credit I think) but he did not describe himself as a Keynesian in his biographical sketch to his 2004 book (I have not read his later one). Indeed, he was avowedly anti-Keynesian.

Hi Peter, I did not know that Wolf disavowed Keynes in 2004. This is what Wikipedia says “He became one of the more influential drivers of the 2008–2009 Keynesian resurgence, and in late 2008 and early 2009, he used his platform on the Financial Times to advocate a massive fiscal and monetary response to the financial crisis of 2007–2010.”

And from a recent article of his in the FT “Paul Krugman argues, to my mind persuasively, that the basic Keynesian remedies — a strong fiscal and monetary response — remain right.” https://www.ft.com/content/28e2f9ac-2b66-11e8-9b4b-bc4b9f08f381

And this seems pretty conclusive: http://www-personal.umich.edu/~kathrynd/files/PP290/KeynesandtheFinancialCrisis_FT_Dec2308.pdf