What will happen to the world economy in 2018? The global capitalist economy rises and falls in cycles, ie a slump in production, investment and employment comes along every 8-10 years. In my view, these cycles are fundamentally driven by changes in the rate of profit on the accumulated capital invested in the major advanced capitalist economies. The cycle of profitability is longer than the 8-10 year ‘business cycle’. There is an upwave in profitability that can last for about 16-18 years and this is followed by a downwave of a similar length. At least this is the case for the US capitalist economy – the length of the profitability cycle will vary from country to country.

Alongside this profitability cycle, there is a shorter cycle of about 4-6 years called the Kitchin cycle. And there also appears to be a longer cycle (commonly called the Kondratiev cycle) based on clusters of innovation and global commodity prices. This cycle can be as long as 54-72 years. The business cycle is affected by the direction of the profit cycle, the Kitchin cycle and and K-cycle and by specific national factors.

The drivers behind these different cycles are explained in my book, The Long Depression. There I argued that when the downwaves of all these cycles coincide, world capitalism experiences a deep depression that it finds difficult to get out of. In such a depression, it may require several slumps and even wars to end it. There have been three such depressions since capitalism became the dominant mode of production globally (1873-97; 1929-1946; and 2008 to now). The bottom of the current depression ought to be around 2018. That should be the time of yet another slump necessary in order to restore profitability globally. That has been my forecast or prediction etc for some time. Anwar Shaikh in his book, Capitalism, takes a similar view.

This time last year, in my forecast for 2017, I said that “2017 will not deliver faster growth, contrary to the expectations of the optimists. Indeed, by the second half of next year, we can probably expect a sharp downturn in the major economies …far from a new boom for capitalism, the risk of a new slump will increase in 2017.”

Well, as we come to the end of 2017 and go into 2018, that prediction about global growth proved to be wrong. Global real GDP growth picked up in 2017 – indeed, for the first time since the end of the Great Recession in 2009, virtually all the major economies increased their real GDP. The IMF in its last economic outlook put it like this: “2017 is ending on a high note, with GDP continuing to accelerate over much of the world in the broadest cyclical upswing since the start of the decade.”

The OECD’s economists also reckon that “The global economy is now growing at its fastest pace since 2010, with the upturn becoming increasingly synchronised across countries. This long-awaited lift to global growth, supported by policy stimulus, is being accompanied by solid employment gains, a moderate upturn in investment and a pick-up in trade growth.”

Alongside the (still modest) recovery in global growth, investment and employment in the major economies in 2017, financial asset markets have had a great year.

The IMF again: “Equity valuations have continued their ascent and are near record highs, as central banks have maintained accommodative monetary policy settings amid weak inflation. This is part of a broader trend across global financial markets, where low interest rates, an improved economic outlook, and increased risk appetite boosted asset prices and suppressed volatility.”

So all looks set great for the world economy in 2018, confounding my forecast of a slump.

But it is sometimes the case that when all looks rosy, a storm cloud can appear very quickly – as in 2007. First, it is worth remembering that, while world economic growth is accelerating a bit, the OECD reckons that “on a per capita basis, growth will fall short of pre-crisis norms in the majority of OECD and non-OECD economies.” So the world economy is still not yet out of the Long Depression that started in 2009.

Indeed, as the OECD economists put it: “Whilst the near-term cyclical improvement is welcome, it remains modest compared with the standards of past recoveries. Moreover, the prospects for continuing the global growth up-tick through 2019 and securing the foundations for higher potential output and more resilient and inclusive growth do not yet appear to be in place. The lingering effects of prolonged sub-par growth after the financial crisis are still present in investment, trade, productivity and wage developments. Some improvement is projected in 2018 and 2019, with firms making new investments to upgrade their capital stock, but this will not suffice to fully offset past shortfalls, and thus productivity gains will remain limited.”

The IMF’s economists make the same point. The latest IMF projection for world economic growth is for 3.7% global GDP growth over the 2017-18 period, an acceleration of 0.4 percentage points from the anaemic 3.3% pace of the past two years. But this is still less than the post-1965 trend of 3.8% growth and the expected gains over 2017-2018 follow an exceptionally weak recovery in the aftermath of the Great Recession.

The OECD also thinks that much of the recent pick-up is fictitious, being centred on financial assets and property. “Financial risks are also rising in advanced economies, with the extended period of low interest rates encouraging greater risk-taking and further increases in asset valuations, including in housing markets. Productive investments that would generate the wherewithal to repay the associated financial obligations (as well as make good on other commitments to citizens) appear insufficient.” Indeed, on average, investment spending in 2018-19 is projected to be around 15% below the level required to ensure the productive net capital stock rises at the same average annual pace as over 1990-2007.

The OECD concludes that, while global economic growth will be faster in the coming year, this will be the peak rate for growth. After that, world economic growth will fade and stay well below the pre-Great Recession average. That’s because global productivity growth (output per person employed) remains low and the growth in employment is set to peak.

Former chief economist of Morgan Stanley, the American investment bank, Stephen Roach remains sceptical that the low growth environment since the end of the Great Recession is now over and the capitalist economy is set for fair winds. Such growth as the major economies have seen has been based on very low interest rates for borrowing and rising debt in the corporate and household sectors. “Real economies have been artificially propped up by these distorted asset prices, and glacial normalization will only prolong this dependency. Yet when central banks’ balance sheets finally start to shrink, asset-dependent economies will once again be in peril. And the risks are likely to be far more serious today than a decade ago, owing not only to the overhang of swollen central bank balance sheets, but also to the overvaluation of assets.”

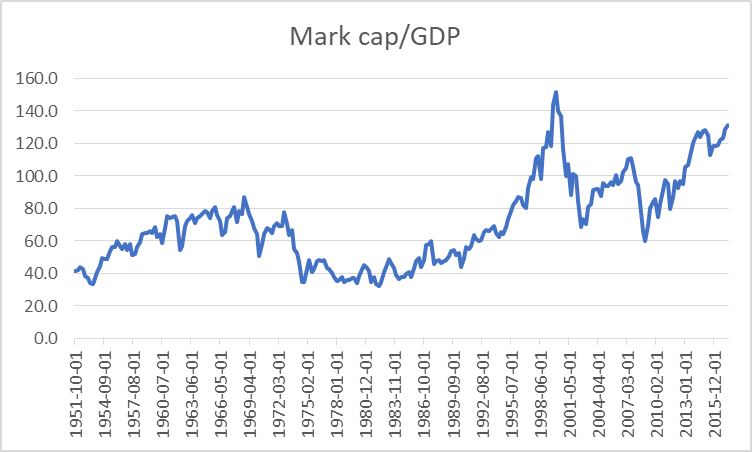

Stock markets are hugely ‘overvalued’, at least according to history. The cyclically adjusted price-earnings (CAPE) ratio of 31.3 is currently about 15% higher than it was in mid-2007, on the brink of the subprime crisis. In fact, the CAPE ratio has been higher than it is today only twice in its 135-plus year history – in 1929 and in 2000. “Those are not comforting precedents” (Roach). One measure of the price of financial assets compared to real assets is the stock market capitalisation compared to GDP (in the US). It has only been higher just before the dot.com bust of 2000.

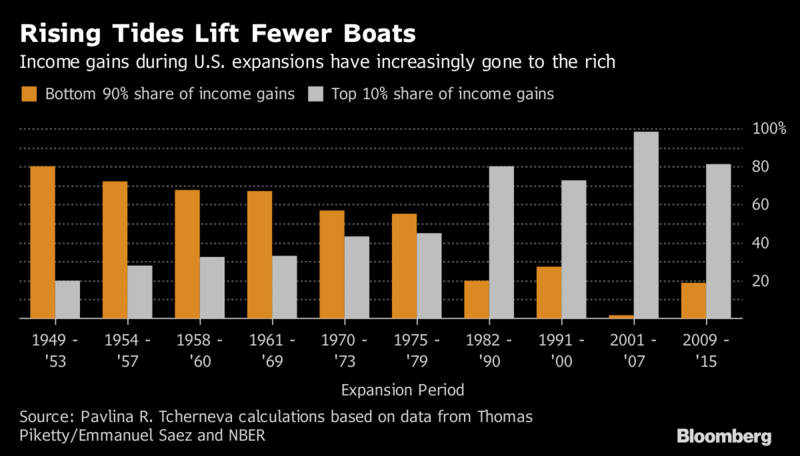

And I don’t need to tell readers of this blog that any economic recovery for world capitalism since 2009 has not been shared ‘fairly’. There has been a host of data to show that the bulk of increase in incomes and wealth has gone to top 1% of income and wealth holders, while real wages from work for the vast majority in the advanced capitalist economies have stagnated or even fallen.

The main reason for this growing inequality has been that the top 1% own nearly all the financial assets (stocks, bonds and property) and the price of these assets have rocketed. Corporations, particularly in the US, have used any rise in profits mainly to buy back their own shares (boosting their price) or pay out increased dividends to shareholders. And these are mainly the top 1%.

Companies in the S&P 500 Index bought $3.5 trillion of their own stock between 2010 and 2016, almost 50% more than in the previous expansion.

There are two things that put a question mark on the delivery of faster growth for most capitalist economies in 2018 and raise the possibility of the opposite. The first is profitability and profits – for me, the key indicators of the ‘health’ of the capitalist economy, based as it is on investing and producing for profit not need.

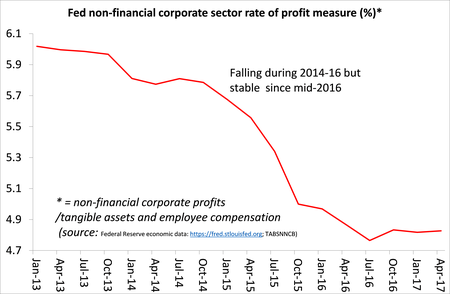

In this context, let’s start with the US economy, which is still the largest capitalist economy both in total value, investment and financial flows – and so is still the talisman for the world economy. As I showed in 2017, the overall profitability of US capital fell in 2016, making two successive years from a post-Great Recession in 2014. Indeed, profitability is still below the pre-crisis peaks (depending on how you measure it) of 1997 and 2006.

As far as I can tell, in 2017, profitability flattened out at best – and still well down from 2014.

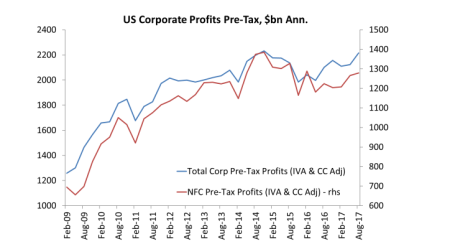

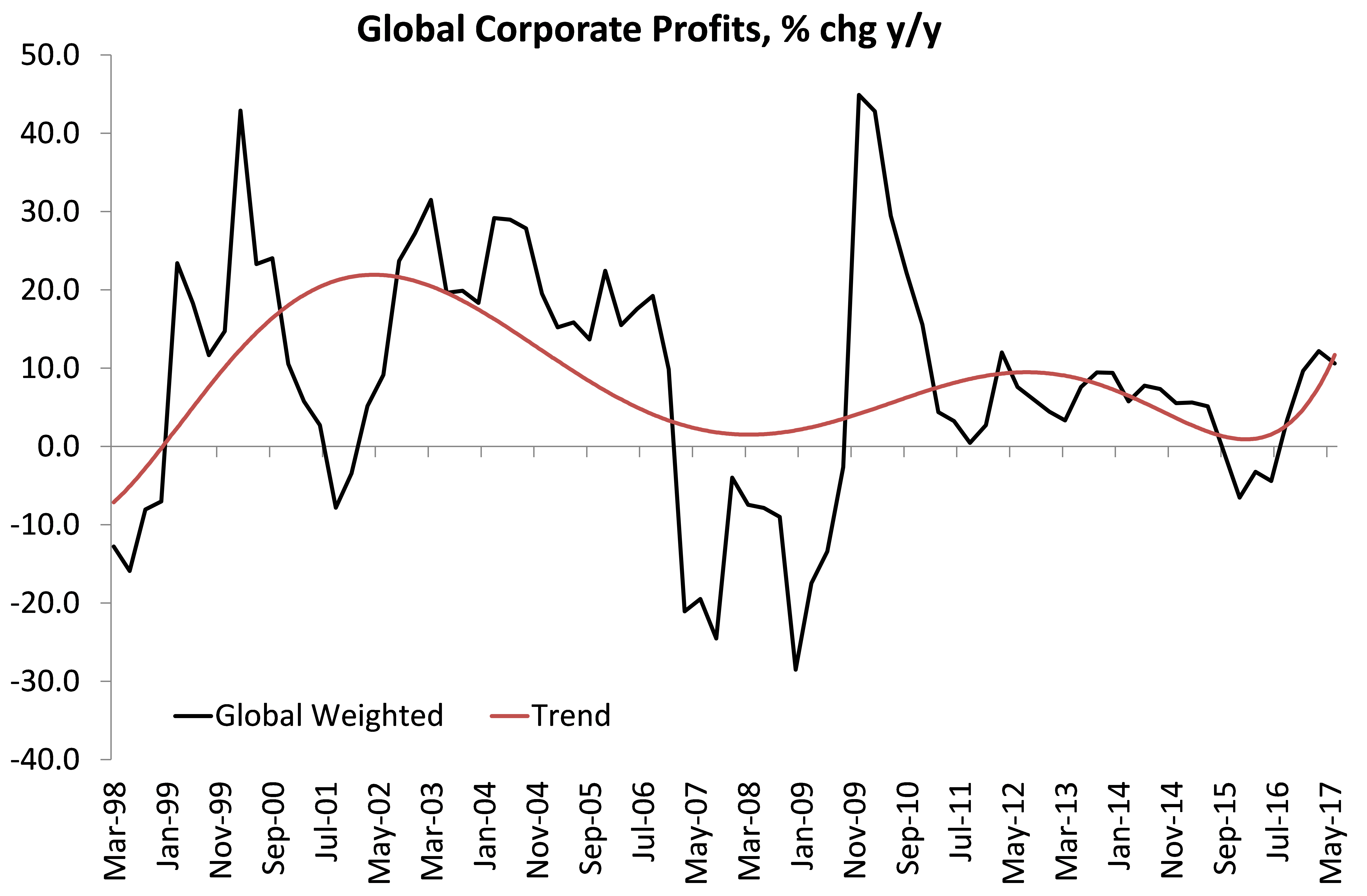

The total or mass of profits in the US corporate sector (that’s not profitability, which is measured as profits divided by the stock of capital invested) has recovered from the depths of the Great Recession in 2009. But the mass of profit slipped back sharply in 2015 (along with profitability, as we have seen above). This fall stopped in mid-2016. The fall seemed to coincide with the collapse in oil prices and the profits of the energy companies in particular. But the oil price stabilised in mid-2016 and so did profits (although profitability continued to fall). Profits rose again in 2017, but, after stripping out the mainly fictitious profits of the financial sector, the mass of profit is still well below the peak of end-2014 (red line below).

As I have shown in other places when profits fall back, so will investment within a year or so. On the basis of the data for the US, 2017 produced flat profitability and a very small recovery in profits. That suggests that, at best, investment in productive capacity will grow very little in 2018, especially as much of these profits are going into unproductive assets, property and financial.

What about the rest of the world? Well, it is clear that the European capitalist economies (with the exception of post-Brexit Britain) have recovered in 2017. Real GDP growth has picked up, led by Germany and northern Europe, although it is still below the growth rate in the US. Japan too has recorded a modest recovery.

When we look at profitability, however, in core Europe it rose only slightly and fell in Japan in 2015 and 2016, as in the US. Indeed, only Japan has a higher rate of profit compared to 2006.

When we look at the mass of global corporate profits (using my own measure), there has been a modest recovery in 2017 after the fall in 2015-6. But remember my measure includes China, where profits in the state enterprises rose dramatically in 2016-7.

On balance, if profits and profitability are good indicators of what is to come in 2018, they suggest much the same as 2017 at best – but probably not provoking a slump in investment.

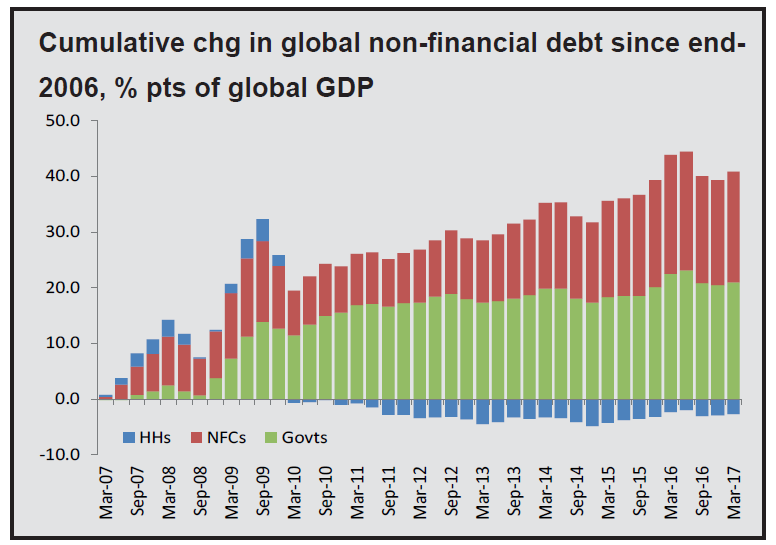

The other question mark against the overwhelming optimism that 2018 is going to be a great year for global capitalism is debt. As many agencies have recorded and I have shown in this blog during 2017, global debt, particularly private sector (corporate and household) debt has continued to rise to new records.

The IMF comments “Private sector debt service burdens have increased in several major economies as leverage has risen, despite declining borrowing costs. Debt servicing pressure could mount further if leverage continues to grow and could lead to greater credit risk in the financial system.”

Among G20 economies, total nonfinancial sector debt (borrowing by governments, nonfinancial companies, and households from both banks and bond markets) has risen to more than $135 trillion, or about 235% of aggregate GDP. In the G20 advanced economies, the debt-to-GDP ratio has grown steadily over the past decade and now amounts to more than 260% of GDP.

The IMF sums up the risk. “A continuing build-up in debt loads and overstretched asset valuations could have global economic repercussions. … a repricing of risks could lead to a rise in credit spreads and a fall in capital market and housing prices, derailing the economic recovery and undermining financial stability.”

The IMF economists do not see this risk of a new debt bust happening until 2020. They may be right. But the policy of low interest rates and huge injections of credit by the main central banks is now over. The US Federal Reserve is now hiking its policy interest rate and has stopped buying bonds. The European Central Bank will end its buying in this coming year; the Bank of England has already stopped. Only the Bank of Japan plans more bond purchases through 2018. The cost of borrowing is set to rise while the availability of credit will fall. If profitability continues to fall in 2018, this is a recipe for investment collapse, not expansion. This would especially hit the corporate sector of the so-called emerging economies.

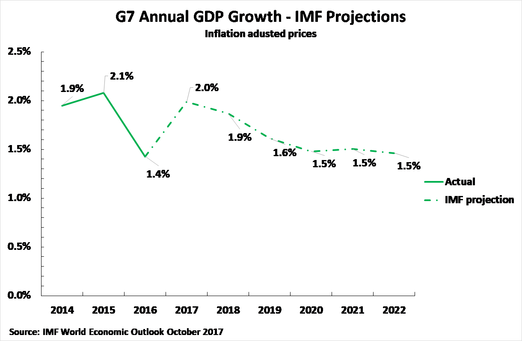

Even if the major capitalist economies avoid a slump in 2018, nothing else has much changed. Economic growth in the major economies remains low compared to before the Great Recession, even if it picks up in 2018. And the prospect for the medium term is poor indeed. Productivity (output per person working) growth is very low everywhere and employment growth from here will be muted. So the potential long-term growth rate of the major economies will slow from any peak achieved in 2018. After very low growth in 2016 of only 1.4%, the IMF predicts G7 growth in 2018 of 1.9% – a moderate but real upturn. However, G7 growth is then predicted to fall to 1.6% in 2019 and to a poor 1.5% in 2020-2022.

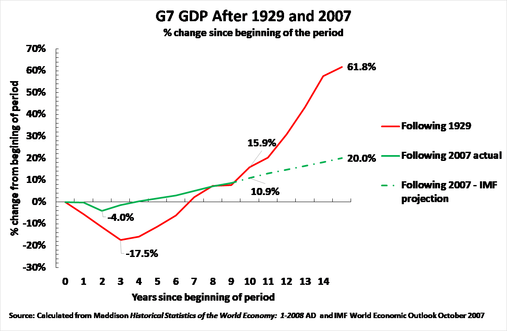

Thus the upturn in 2017-2018 seems cyclical and will not be consolidated into a new longer sustained ‘boom’. That’s because, if there is no slump to devalue capital (productive and fictitious) and thus revive profitability, then investment and productivity growth will stay stuck in depression. Overall growth in the G7 economies since the Great Recession has been slower than during the ‘Great Depression’ of the 1930s. Indeed, based on IMF projections, by 2022, that is 15 years after 2007, total GDP growth in the G7 economies will only be 20% compared to 62% in the 15 years after 1929. And that assumes no major economic slump in the next five years.

Nevertheless, despite weak profitability and high debt, the modest recovery in profits in 2017 suggests that the major capitalist economies will avoid a new slump in production and investment in 2018, confounding my prediction.

Now when you are proved wrong (even if only in timing), it is necessary to go back and reconsider your arguments and evidence and revise them as necessary. Now I don’t think I need to revise my fundamentals, based as they are on Marx’s laws of profitability as the underlying cause of crises. Profits in the major economies have risen in the last two years and so investment has improved accordingly (to Marx’s law). Only when profitability starts falling consistently and takes profits down with it, will investment also fall. Until that happens, the impact on the capitalist sector of the rising costs of servicing very high debt levels can be managed, for most.

What seems to have happened is that there has been a short-term cyclical recovery from mid-2016, after a near global recession from the end of 2014-mid 2016. If the trough of this Kitchin cycle was in mid-2016, the peak should be in 2018, with a swing down again after that. We shall see.

“The OECD’s economists also reckon that “The global economy is now growing at its fastest pace since 2010, with the upturn becoming increasingly synchronised across countries. This long-awaited lift to global growth, supported by policy stimulus, is being accompanied by solid employment gains, a moderate upturn in investment and a pick-up in trade growth.””

Exactly what policy stimulus ar they talking about?! There was definitely stimulus in 2008/9, that led to a fast “V” shaped recover in the US, UK and Eurozone, and yet even before that recovery could get back to pre-2008 levels it was cut off at the knees by the imposition of austerity in the UK, and EU, with Republicans in the US trying to undermine Obama’s fiscal stimulus, and imposing several political crises over the Debt Ceiling and so on.

In the UK, in the last quarter that Labour could take credit for, growth stood at 1%, or about 4% annualised. The Liberal-Tories turned that into a recession within months of coming into office by imposing a nonsensical austerity, that hit first at existing and planned capital spending projects. In the Eurozone, a similar crazy policy of austerity – at a time of 300 year low interest rates – decimated the economies of Greece, Spain, Portugal and Ireland, and looked set to do the same thing to Italy, and possibly France.

The only stimulus that has been provided is a monetary stimulus whose avowed purpose was to reflate the massively inflated prices of financial assets and property, whose ownership now represents the main form of wealth of the capitalist class. The imposition not of policy stimulus, but of policy contraction, via fiscal austerity was intended for the same purpose, i.e. not to stimulate the real economy, whose result would have been to cause interest rates to rise, but was to hold back growth in the real economy, so as to prevent that rise in interest rates, as had happened in 2007, and whose effect would be to decimate the capitalised prices of those financial assets and property.

Had we not had those policies of monetary stimulus alongside fiscal austerity in the period after 2010, the real economy throughout the globe would have continued its upward trajectory it was on prior to 2008, as part of the long wave upturn that started in 1999. It would have led to much higher market rates of interest, and a consequent cratering of the astronomical prices of financial assets and property, as started to happen in 2008.

The actions of states and central banks since 2010 have not prevented that collapse of those asset prices, they have only delayed it, and made the conditions even more intensified, whilst using up all of their available ammo to be able to reflate those prices when they crash this time in even more dramatic fashion. And all of their austerity measures all of their attempts to drain resources away from the real economy by encouraging financial and property speculation, have failed to stop the real economy growing during that period, because of the underlying strength of the long wave upturn that is underway.

That is why I have never bought into the idea of a long depression, secular stagnation, or great recession, or other such buzz words, and resisted the annual predictions of “the next recession” being only months away, or this time next year. It is why year after year I have been proved right in rejecting such predictions, and its why the period ahead continues to be one in which the general trend will be higher and stronger, not downward and weaker.

Well, you can deny that capitalism suffers from periodic crises if you want (you’re free to have and express your opinion), but empirical investigation shows capitalism does suffer from periodic crises. So your opinion, albeit valid from the point of view of freedom of expression, is scientifically wrong.

Except I have never anywhere even come close to saying or even suggesting that capitalism does not suffer from periodic crises! I have written at length about the causes of such crises of overproduction, I have written at length about the nature of the long wave cycle in creating the conditions that lead to such crises of overproduction in its upward phase, as large rises in the rate of profit stimulates increased production, and sharp rises in input prices, as Marx describes in Capital III, Chapter 6 of Capital, which might not be recoverable in end prices. I have written about the role of the long wave cycle in creating the conditions for crises of overproduction in the Autumn or Crisis phase of the cycle, when those tendencies become acute, and where extensive accumulation of capital as opposed to intensive accumulation, leads to labour supplies being used up, as Marx describes in Capital III, Chapter 15, which causes the rate of surplus value to fall squeezing profits, and which leads to high levels of consumption, which make the potential to realise profits more difficult, because to increase demand for the additional production of existing ranges of commodities, prices have to be reduced by larger proportions. And, I have written about the role of the long wave in the Winter or stagnation phase, whereby the crises of overproduction are addressed by a shift from extensive to intensive accumulation, as a new innovation cycle begins, and new labour-intensive equipment is introduced, which creates a relative surplus population, reducing the pressure on labour supplies, reducing wages, and driving up the rate of surplus value, and bringing about a moral depreciation of existing fixed capital, and reducing the value of raw materials.

Marx’s initial analysis of these long wave cycles – though of course he did not call it that – is given in TOSV II, where he examines the movement of agricultural prices in the 18th and 19th century. Marx shows that a dominant factor is the role of large scale capital investment. If we take 2 pieces of land A and B, the natural fertility of B might be greater than that of A, but Marx points out, if A has been cultivated for decades, the capital invested in it will have become incorporated in the fertility of the land. It might, therefore, require several decades of investment of capital in B, before it reaches the same level of fertility as A, even though its own natural fertility is higher. Indeed, its not just the investment directly in the land, as Marx demonstrates, but the investment in all of that necessary infrastructure that enables capital invested in any sphere to be productive.

The consequence, Marx shows is that in those periods where large scale investment in agriculture/primary production is taking place the resultant output does not act to reduce market values. However, once all of this investment, be it fixed capital investment on the land, in new mines/quarries etc., or investment in new infrastructure is in place, which on the basis of Marx’s historical analysis here could take several decades, the increase in productivity brings about a consequent rise in productivity and fall in market values, with a consequent effect on prices, profits and rents.

It is the consequences of the long wave cycle in its different phases that explains the basis of crises of overproduction, not the law of the tendency of the rate of profit to fall – indeed Marx demonstrates that Ricardo was wrong in believing that it is a higher rate of profit that generates additional investment, or causes investment to fall – and Marx also demonstrates that investment can and often does increase when the rate of profit is falling, so long as competition drives capitals to invest in order not to lose market share, when demand in the economy is rising. That indeed can be a trigger for a crisis of overproduction, as each expands production so as not to lose market share, and then find that they cannot sell the output at prices that reproduce the consumed capital.

Far from coming anywhere close to even suggesting that capitalism does not suffer periodic crises, I wrote a book on Marx and Engels theory of the causes of such crises! – Marx and Engels Theories of Crisis.

That much– that Boffy has never denied that capitalism suffers from periodic crises– is true. Of course, Boffy tends to ignore the actual causes of crisis, preferring to identify almost every crisis, from 1847 to 2008 as a financial or credit crisis.

What Boffy has argued is that 2008 was simple a liquidity crisis, a “credit crunch,” made so much worse by wrong-headed austerity policies. Except…..except Boffy confuses, conveniently enough, monetary policy which might have a lot to do with a credit crisis, with FISCAL policy which would have absolutely no effect, one way or the other. Monetary policy has as its focus masses and velocity of currency, and the rates of interest. Fiscal policy refers to government policy re spending on entitlements, subsidies, grants etc.

That 2008/9-20?? was not a credit crunch is verified by the fact that credit was not restricted prior to the crisis, or during the crisis, although it took the massive intervention of central banks, orchestrated by the US Federal Reserve and it implementation of open-ended currency swap lines to keep the system of credit from seizing up due to the lack of solvency.

Of course, anyone paying attention might have noticed that the auto industry in the US was already in recession by 2006, and the contraction was made more intense by the blowout in oil prices in 2007.

In fact, the reason Ford Motor (as opposed to its credit arm which did seek a bailout) did not “need” a bailout is that in 2006 it had begun reducing its hourly work force BY HALF.

Anyone paying attention might have noticed that this was not a liquidity crisis, but rather a solvency crisis. And that profits were being flushed into the hands of the oil majors. If I recall correctly, by 2007, 35% of the profits of the non-financial sector of the US economy were accounted for by oil and gas companies.

What Boffy does deny is what Marx called the “most important law of political economy”– that the very productivity of labor, a productivity that capital has to continuously drive forward to aggrandize profit, undermines profitability.

But hey, I wouldn’t want what Marx really said to interfere with someone who just loves to post walls of cherry-picked Marx quotations.

My apologies if this violates anyone’s rules of decorum.

Just kidding.

Happy New Year to all. Even Boffy.

Here’s what you wrote:

“That is why I have never bought into the idea of a long depression, secular stagnation, or great recession, or other such buzz words, and resisted the annual predictions of “the next recession” being only months away, or this time next year. It is why year after year I have been proved right in rejecting such predictions, and its why the period ahead continues to be one in which the general trend will be higher and stronger, not downward and weaker.”

If you reject the concepts of depression, stagnation and recession, you’re rejecting the possibility of systemic crises in capitalism.

“If you reject the concepts of depression, stagnation and recession, you’re rejecting the possibility of systemic crises in capitalism.”

Except I have nowhere rejected the CONCEPT of depression, stagnation, or recession, and I have written extensively on those concepts, and the basis of their periodicity as determined by the laws of the long wave cycle!

The only thing I have not bought into, and what is stated in the quote you have given is that the current period is one characterised by being “a long depression, secular stagnation, or great recession, or other such buzz words”. The fact that the current period does not fit into any of those categories does not at all mean that the category itself does not exist, or that some future period may indeed be so characterised.

Austerity is not just a reduction in what the state has to do, combine this with a well documented transfer of tax being paid by corporations and the rich to being paid for by the working classes and it is clear that austerity is not only an ideological project but also one of cost reduction! What a stimulus that is!

I think the biggest story since 2008 has been the inequality one. Ok inequality is a fact of life under capitalism but the crisis was used to further consolidate the neo liberal order. I.e. discipline the working classes. Austerity not only achieves a transfer of wealth to the ruling classes it also allows the ruling class to punish the poorest and follow the narrative of lazy and undeserved poor, which in turn brings large parts of the working class into ideological agreement with the ruling class. This dynamic ultimately led to Brexit and Trump. It is this narrative of austerity that allows the ruling class to further consolidate its neo liberal agenda, from market liberalisation, reduction of progressive state schemes through to an attack on workers’ rights. Austerity forces people to take sides in this attack, you can side with the lazy people who given half a chance would drive us into poverty like in Venezuela or you can side with what Gordon Brown and Tony Blair called the wealth creators, thos special people among us who get out of bed in the morning, who climb mountains just for the heck of it, or cycle round the world overcoming every obstacle. Follow these great and motivated people and you can’t go wrong.

Boffy has predicted the collapse of house prices for a decade, yet like a neo liberal he blames the state for this wrong prediction, he predicted that the massive stimulus would be paid for by inflation and he decidedly claimed that austerity would be undermined and not achieved and that governments were deliberately back loading austerity in order to abandon it! What balderdash!

Just how long has to pass before we conclude the basis of Boffy’s argument is seriously flawed?

Obviously being a contradictory system many of these policies will possibly come to bite capitalists back on the arse eventually. But I don’t think that is written in stone or anything.

My prediction for 2018, the rich will continue to live the high life, companies like Apple and Volkswagen will put their profits before the fate of the planet and every living thing on it and the poor will be vilified over and over again. In other words, same shit, different year.

Hmm, the last time I heard those particular hobby horses trotted out was by someone at that time calling themselves Chris, which was just the latest pseudonym used by someone who has the time to trawl through my posts going back 10 years.

But, its Christmas, and I’m feeling in generous mood.

So, now let’s see.

“Boffy has predicted the collapse of house prices for a decade”

And, in 2008/9 house prices in the US, Ireland, Spain fell by around 50-60%. In the UK they dropped 20%.

In actual fact, I have never said when such a collapse was going to happen, only that such a collapse is inevitable sooner or later. And, in fact, as the BBC showed recently, in the UK, in the majority of the country, house prices are down by around 25% since 2007.

The only time I have made an actual prediction that a financial crisis was about to erupt, was in 2008, and that was within a few weeks of that crisis actually erupting! On every other occasion, I have made a point of saying that it is generally impossible to predict when such a financial crash is going to happen, because financial markets work by different laws than economies. In terms of predicting the actual course of the global economy, I have been pretty consistently correct, in spite of all the pressure from the multitude of pundits who have year after year predicted recession or depression.

“he predicted that the massive stimulus would be paid for by inflation”,

and if you look at what I wrote back then when I said that, it was that the inflation would be the result of money printing, i.e. QE, and it has. The state has printed money, and used it to buy up government paper. It massively inflated the prices of government bonds, so as to keep those asset prices up, and at the same time, reduced the interest it paid on its debt! In fact, in the UK, the Bank of England even waived the interest it was due from the government on the debt it had bought up, via QE!

“and he decidedly claimed that austerity would be undermined and not achieved and that governments were deliberately back loading austerity in order to abandon it!”

What was being talked about was what was happening in the UK. And, the fact is that the government did have to reverse a lot of the cuts in capital spending it introduced, and that was one reason they were able to get some growth in 2014, and they did back load much of the revenue cuts, shown by the fact that the majority of welfare cuts, in things like Tax Credits etc. were only introduced in the last few years, and even some of them they had to abandon in recent Budgets, having hoped they would never have to implement them if by that time, the budget deficit had been erased.

But, given that I’m now pretty sure who SIOB actually is, that’s the extent of my Christmas goodwill, so expect no further response.

Christmas is a time when the rich kids get what they want and the poor are left without. A thoroughly capitalist time of the year! Still I did like my new tablet!

2008 cannot be thought of as a financial crisis I don’t think because it was a problem of the real economy that manifested itself in the banking system.

So not only can’t you predict a financial crisis, which is fair enough, but you can’t even get a good handle on a crisis even a decade after it happened! Incidentally you don’t seem to have a coherent theory of a financial crisis, other than it is something you can’t predict. Is it tied to the long wave, the short cycles, the business cycles, does it have its own cycles? What characterises their peaks and troughs? What immediately precedes them?

You predicted house prices would collapse by as much as 80%, but actually after a dodgy few years they have started to rise again and recover. This is shown everywhere, in places like Spain they are still below pre crisis levels but the reason for that was the oversupply. At the time of the crash Spain was building lots of new apartments as they anticipated a market for those developments but the crash stalled that project.

You were incorrect about inflation as a way to reduce debt and you were wrong that austerity was some kind of false promise.

You don’t know who I am, I don’t know who you are, other than the pro imperialist Marxist who loves capitalism. Put it this way I reckon you would be the last person I would want to share a drink with in a pub on New Years eve!

Given difficulty of predictions this would be a good time to review underlying theory. Staring at charts to guess at conjunctions of different cycles is what astrologers do.

Business cycles driven by profitability is not a theory. More like a definition.

Maksakovsky explained Marx’s theory. Why not study and develop it now? Is it really more urgent to just keep following the charts?

What was that line the Shirelles sang in “This Is Dedicated to the One I Love”? “The darkest hour is just before dawn”? Well for our capitalists, the brightest hour is just before the darkness. Let’s just see exactly how bright capital’s sun gets before it collapses into another white dwarf…

A useful commentary despite the contradictory first paragraph corrected at the end of the article, with reference to the dip in profits/investment at the end of 2015. What we all tend to forget is that the biggest prop for the global economy, is not monetary policy, but the passivity of the working class which is only partially addressed under the heading “rising inequality”. As to where we are and will be in 2018 depends on whether we are in a new business cycle beginning in 2016, after the mini recession at the end of 2015, or at the end of the business cycle which began in 2009. Whatever the case, the fictitious boiler is really fired up with no safety valve in place, so matters remain delicately poised.

Forgot to share this interesting link comparing today to 1937 https://seekingalpha.com/article/4134445-beginning-look-lot-like-1937?ifp=0

My angle on that.

https://thenextrecession.wordpress.com/2014/08/01/the-risk-of-another-1937/

Ultimately, the objective material conditions for a very precise prediction of crisis under capitalism still don’t exist. There’re simply no unified international data or trustworthy national data to establish an average profit rate (you could get very close if you had access to the books of the biggest multinationals and financial institutions — including tax havens –, but those are confidential). The best we can do is what mr. Roberts is already doing: taking data from the USA and extrapolating it: the USA is the headquarters of capitalism, home of the universal fiat currency and its imperium. If the USA falls, capitalism falls.

Mr. Roberts will try, and will get as close as possible as his own time and objective material conditions will allow him. But, ultimately, he will fail. Capitalism’s objective conditions of demise will only be determined in its autopsy — indeed, that’s the theoretical problem with the Mechanicists of the early 20th Century: they stated capitalism would automatically develop into socialism, because there would be a time when the productive forces would develop to a stage where it would transmute into socialism. The question they forgot to ask themselves was: when can we know the productive forces are mature enough? Engels solved this charade the past Century, when, in a letter, he stated that we can only know if we actively, consciously, try.

Reblogged this on Reconstruction communiste Québec and commented:

Nevertheless, despite weak profitability and high debt, the modest recovery in profits in 2017 suggests that the major capitalist economies will avoid a new slump in production and investment in 2018, confounding my prediction.

Now when you are proved wrong (even if only in timing), it is necessary to go back and reconsider your arguments and evidence and revise them as necessary. Now I don’t think I need to revise my fundamentals, based as they are on Marx’s laws of profitability as the underlying cause of crises. Profits in the major economies have risen in the last two years and so investment has improved accordingly (to Marx’s law). Only when profitability starts falling consistently and takes profits down with it, will investment also fall. Until that happens, the impact on the capitalist sector of the rising costs of servicing very high debt levels can be managed, for most.

What seems to have happened is that there has been a short-term cyclical recovery from mid-2016, after a near global recession from the end of 2014-mid 2016. If the trough of this Kitchin cycle was in mid-2016, the peak should be in 2018, with a swing down again after that. We shall see.

Very interesting, finding this as I am in mid 2019.