The latest data for net fixed assets in the US have been released, enabling me to update the calculations for the US rate of profit a la Marx up to 2016.

Last year, I did the calculations with the help of Anders Axelsson from Sweden, who not only replicated the results to ensure their accuracy (and found mistakes!), but also produced a manual for carrying out the calculations that anybody could use.

As I did last year and in previous years, I have also updated the rate of profit using the method of calculation by Andrew Kliman (AK) that he first carried out in his book, The failure of capitalist production. AK measures the US rate of profit based on corporate sector profits only and using the BEA’s historic cost of net fixed assets as the denominator.

I also calculate the US rate of profit with a slight variation from AK’s approach, in that I depreciate gross profits by current depreciation rather than historic depreciation as AK does, but I still use historic costs for net fixed assets. The theoretical and methodological reasons for doing this can be found here and in the appendix in my book, The Long Depression, on measuring the rate of profit.

The results of the AK calculation and my revised version are obviously much the same as last year – namely that AK’s measure of the rate of profit falls persistently from the late 1970s to a trough in 2001 and then recovers during the credit-fuelled, ‘fictitious capital period’ up to 2006. The 2006 peak in the rate is higher than the 1997 one. My revised version of AK’s measure shows a stabilisation of the profit rate at the end of the 1980s, after which profitability does not really rise much (although there are various peaks up to 2006). What the new data for 2016 do reveal, however, is that profitability (on both measures) has remained below the peak of 2006 (i.e. for the last ten years) and has fallen for the last two. And, of course, the long-term secular decline in the US rate is confirmed on both measures, some 25-30% below the 1960s.

But readers of my blog and other papers know that I prefer to measure the rate of profit a la Marx by looking at total surplus value in an economy against total productive capital employed; so as close as possible to Marx’s original formula of s/c+v. So I have a ‘whole economy’ measure based on total national income (less depreciation) for surplus value; net fixed assets for constant capital; and employee compensation for variable capital. Most Marxist measures exclude a measure of variable capital on the grounds that it is not a stock of invested capital but circulating capital that cannot be measured from available data. I don’t agree and G Carchedi and I have an unpublished work on this point. Indeed, even inventories (the stock of unfinished and intermediate goods) could be added as circulating capital to the denominator for the rate of profit, but I have not done so here as the results are little different.

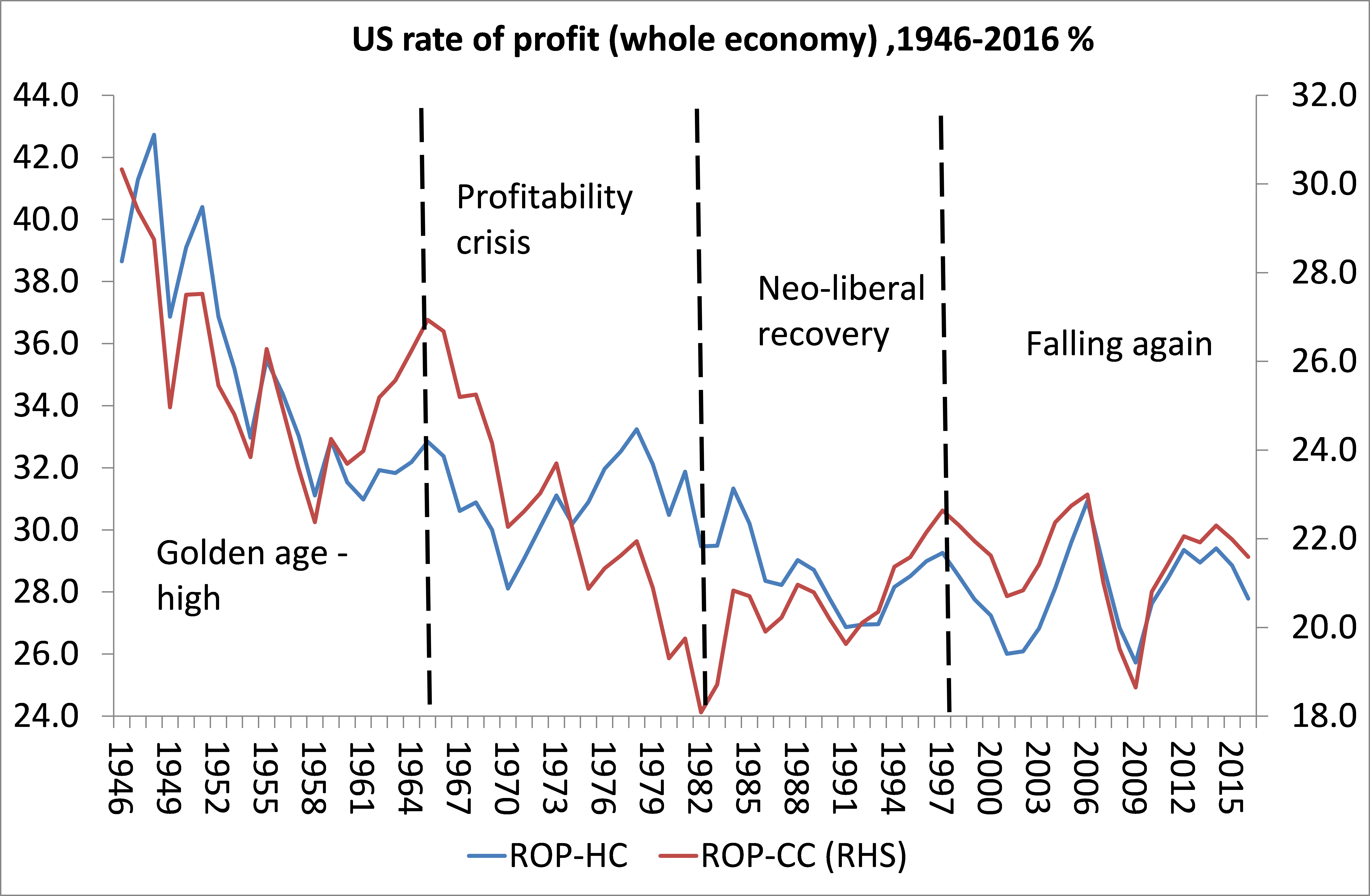

Updating the results from 1946 to 2016 on my ‘whole economy’ measure shows more or less the same result as last year, as you might expect. I measure the rate in both historic and current cost terms. This shows that the overall US rate of profit has four phases: the post-war golden age of high profitability peaking in 1965; then the profitability crisis of the 1970s, troughing in the slump of 1980-2; then the neoliberal period of recovery or at least stabilisation in profitability, peaking more or less in 1997; then the current period of volatility and eventual decline. Actually, the historic cost measure shows no recovery in the rate of profit during the neoliberal period. The current cost measure always shows much greater upward or downward movement. On this measure, the post-war trough was in 1982 while on the historic cost measure, it is 2009 at the bottom of the Great Recession.

What is new about the 2016 update is that the US rate of profit fell in 2016, after a fall in 2015. So the rate of profit has fallen in the last two successive years and is now 6-10% below the peak of 2006.

One of the compelling results of the data is that they show that each economic recession in the US has been preceded by a fall in the rate of profit and then by a recovery in the rate after the slump. This is what you would expect cyclically from Marx’s law of profitability.

In a recent paper, G Carchedi identified three indicators for when crises occur: when the change in profitability; employment; and new value are all negative at the same time. Whenever that happened (12 times since 1946), it coincided with a crisis or slump in production in the US. This is Carchedi’s graph.

My updated measure for the US rate of profit to 2016 confirms the first indicator is operating. The graph above shows that in the last two years there has been a 5%-plus fall. However, new value growth is slowing but not yet negative; and employment growth continues. So on the basis of these three (Carchedi) indicators, a new recession in the US economy is not imminent. Also the mass of profit or surplus value rose (if only slightly) in 2016, and so again does not provide confirmation of an imminent slump.

What the updated data do confirm is my guess last year that 2016 would show a fall in the US rate of profit – and by all the measures mentioned. And, of course, Marx’s law of profitability over the long term is again confirmed. There has been a secular decline in US profitability, down by 28% since 1946 and 15-20% since 1965; and by 6-10% since the peak of 2006. So the recovery of the US economy since 2009 at the end of the Great Recession has not restored profitability to its previous level.

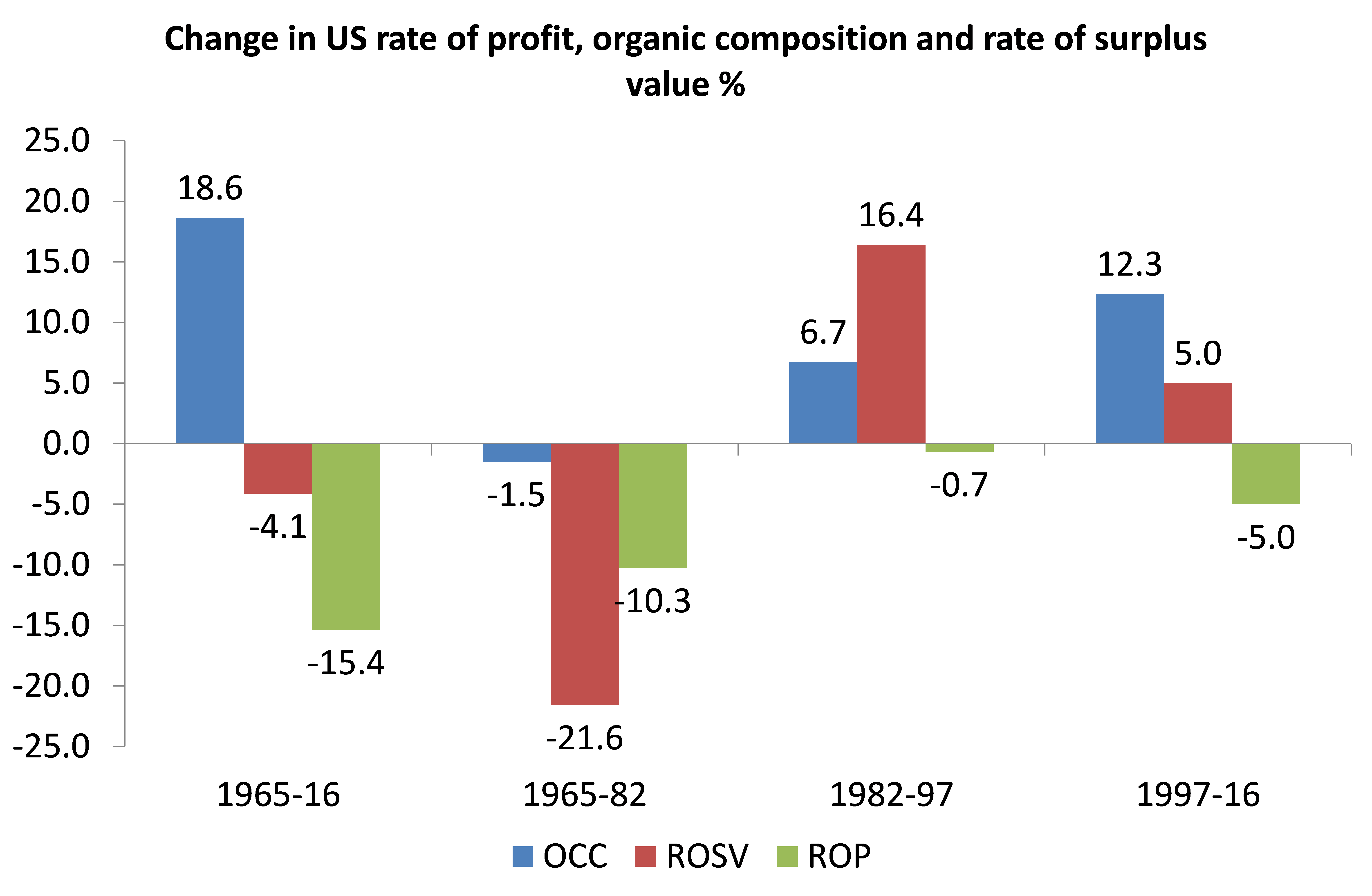

Also, the driver of falling profitability has been the secular rise in the organic composition of capital, which has risen nearly 20% since 1965 while the main ‘counteracting factor’, the rate of surplus value, has fallen 4%. Indeed, even though the rate of surplus value has risen 5% since 1997, the rate of profit has fallen 5% because the organic composition of capital has risen over 12%.

Has the US rate of profit slowed further in 2017? We can use quarterly data from the US Federal Reserve on the non-financial corporate sector to get a rough idea. The Fed data suggest that the rate of profit in the first half of 2017 was flat at best.

So, if the rate of profit is a good indicator of an upcoming slump in capitalism, then the jury is out on the likelihood of slump in 2018. However, the rate of profit is still down from its peaks of 1997 and 2006 and now appears to be flat lining at best.

Hi ! One of your best posts 👍 Thanks for sharing.

Regards Sarabjot Singh

Sent from my iPad

>

Interesting. Michael, in the graph on the OCC, ROSV and ROP, can you break out the 1982-1997 period into 2 distinct “blocks” –say 1982-1989, and then 1990-1997?

Sartesian – on your question. The results are as follows % chg:

1982-9 1990-7

OCC 2.6 6.1

ROSV -7.0 11.8

ROP -2.6 5.4

These are the historic cost measures. On this measure, the US ROP actually fell slightly in the 1980s and then rose in the 1990s. The OCC rose in both periods, but more in the 1990s. The swing factor was the rise in the ROSV in the 1990s.

If I use current cost measures, I get

1982-9 1990-7

OCC -12.0 -4.9

ROSV 6.9 9.5

ROP 14.9 12.2

On this measure there is a large fall in OCC between 1982-89 and a rise in ROSV, leading to a huge rise in the ROP. In the 1990s, this trend in continued.

I think what this shows is that the very large fall in inflation in the 1980s and 1990s is exposed by the current cost measure. Kliman says it is wrong to use current costs and this measure of profitability is meaningless. Interestingly, this divergence in results disappears from 1997-2016. The rate of profit falls about 5% on both measures; the OCC rises about 10-12% on both and the ROSV rises 5% on both. Once the change in inflation ends (and it did in the 2000s, staying about 2% all the time) the divergence on the two measures evaporates.

Thank you. I agree with Kliman here. The historic cost measure accuracy is confirmed in this case by the increased rates of capital expenditure that took place in the 90s

to what extent is the fall of the rate of profit (in any era) due to declining rates of capacity utilization (and realization problems)?

a follow up to Devine’s q: what’s the relation between the argument about the secular decline in the OCC vs the strong cyclical pattern in the post 71 series of debt bubbles that temporarily fix and then reintroduce realization problems? Curious about the way you see the role of credit cycles especially post 71 in the story you’re telling. thanks!

Jim, I think Shaikh brings capacity utilisation into play in his measurement – see his Capitalism book Shaikh, 2016, pp 243-256. I find his results match mine closely. See my article here: http://isj.org.uk/real-capitalism-turbulent/#footnote-10080-23-backlink.

In my view realisation problems arise in the slump itself and then profitability falls further, before reaching a bottom after capital has been devalued sufficiently and the survivors can take advantage of the weak.

“The latest data for net fixed assets in the US have been released, enabling me to update the calculations for the US rate of profit a la Marx up to 2016.”

Except this calculation is not “a la Marx”, because as far as I can see it does not include the current reproduction costs of circulating constant capital, the variation in which are the main factor in Marx’s explanation for the tendency for the rate of profit to fall, nor does it take into consideration the rate of turnover of capital, and changes in that rate, which Marx goes into detail in TOSV to show are a major determinant of the average annual rate of profit, and divergences from it, and it is based upon historic prices, whereas Marx makes clear that the rate of profit must be based upon current reproduction costs, i.e. the need to replace on a like for like basis the constant and variable capital, at its value.

As Marx sets out its impossible on the basis of the National Income data to obtain the required values, because the National Income figure is what it says on the can the total of National Incomes (wages, profits, rents, interest and taxes) the consumption fund of the new new value created by labour during the year (v +s), whereas to calculate the total output value c + v + s ir required, and to calculate the rate of profit it is then required not only to relate s to c + v, which gives only the profit margin, but to determine what proportion of this total laid out capital was actually the advanced capital, so as to calculate the annual average rate of profit.

Without the latter you merely have a figure for the profit margin, which tends to fall as the average annual rate of profit rises, because it simply reflects the rise in social productivity, and greater mass of use values produced by a given amount of capital, which raises the annual average rate of profit, as the rate of turnover rises. By omitting the figure for the circulating constant capital (as Marx demonstrates the figure for “intermediate production” is only the equivalent of Department I (v +s), whereas what is required is the figure for Department I c, what you get is only a figure for the rate of surplus value.

By then relating that figure to the fixed capital, what you get is not even close to a Marxist average annual rate of profit, but a totally bastardised, meaningless figure that can only ever be totally misleading.

I read your paper with Carchedi on turnover which makes every mistake possible. Firstly, it is possible to calculate turnover therefore to deal with aggregated figures. If the same number of workers are employed annually at the same level of productivity and suffering the same rate of exploitation, will turnover influence the mass of surplus value. Of course it will. The faster the turnover the greater the reduction in variable capital benefitting surplus value despite the fact that the total value of the annual net output remains unaltered. Why do the two of you use the silly example of two capitalists in your unpublished paper? Then there is the question of realisation. If at the twilight phase of the business cycle, turnovers slow because the fall in investment has led to a fall in demand so that a production/distribution cycle of 100 days is now extended to 120 days, then not only will the realisation of surplus value fall, so too will the realisation of the annual net value added or output. I have provided proof of these phenomena in my articles so why raise a dubious and unnecessary theoretical example.

Finally of course it is possible to obtain circulating capital. Step one, deduct the surplus from the annual gross output to arrive at the cost of gross output. Step two, divide the cost of annual gross output by turnover to yield working or circulating capital (by using the turnover formula). Step three add this circulating capital to fixed capital to obtain total capital over which to divide the surplus. Arrive at the living concrete rate of profit.

Finally stop substituting annual compensation for variable capital. Outside construction and ship building I do not know of any other industry that needs variable capital to provide a year’s worth of wages.

For those of you interested in a much more modern approach and one which has much more fidelity to Marx and Engel’s method go to the planningmotive.com like hundreds of other readers.

U– can you lay out concretely the differences in the numbers for a rate of profit derived using your method vs. those numbers, and maybe even more importantly, the TREND you calculate compared to the numbers and the trend Michael’s method provides?

Ucan – thanks for your incisive comments. I shall review your points and also attempt your method. If I and Carchedi are wrong in our critique of the role of capital turnover and circulating capital, does it make a difference to the trends in the ROP. Well, if we refer to Esteban Maito’s work, Maito compares profitability for the cases where turnover of circulating capital is computed and where not. Maito estimates capital turnover by dividing the total costs of the economy (intermediate consumption, wages and consumption of fixed capital) by total stock of inventories, according to Fichtenbaum (1988). The fundamental idea of this procedure is that the number of annual turnovers emerges from the number of times the total stock of inventories is expressed in the flow of total costs of the economy.

He concludes “Naturally, it´s lower in the latter” but … does not affect the sense of the trend…, although it softens its slope”. On Maito’s adjusted rate of profit, the US overall rate of profit peaks in 1965, falls to a trough in 1982 and peaks again in 1997, with a new trough in 2009 – trends very similar to the ‘unadjusted’ ROP.

Esteban Maito, “Income distribution, turnover speed and profit rate in Chile, Japan, Netherlands and United States”,

Click to access MPRA_paper_59283.pdf

UCAN,

I agree with a lot of what you have said here, but you say,

“Finally of course it is possible to obtain circulating capital. Step one, deduct the surplus from the annual gross output to arrive at the cost of gross output. Step two, divide the cost of annual gross output by turnover to yield working or circulating capital (by using the turnover formula). Step three add this circulating capital to fixed capital to obtain total capital over which to divide the surplus. Arrive at the living concrete rate of profit.”

However, the problem is to know what the actual gross output value is in the first place. GDP figures are simply, as Marx says, a figure for the consumption fund, or final output. They are the equivalent of National Income, and thereby represent what Marx calls the continuation of the absurd dogma of Adam Smith that economists have adopted ever since, and that is taught to every student of economics that the value of commodities, and thereby of national output resolves into factor incomes – wages, profits, rent and interest plus taxes.

But, as Marx demonstrates in Capital II, Chapter 20, and at laborious length in TOSV I, that absurd dogma of Smith’s is totally wrong, and clearly impossible, because the value of commodities and of GDP cannot possibly resolve into revenues, because it also comprises the value of constant capital, it is c + v + s. not just v +s, and c here, is the value of the circulating constant capital, plus the wear and tear of fixed capital that is consumed by Department, and physically replaced on a “like for like basis”, as marx says in Capital III, Chapter 49, and which thereby creates a revenue for no one.

In fact, if you wanted to calculate a Marxian rate of profit, of the type that Marx discusses in relation to the law of the tendency for the rate of profit to fall, i.e. the profit margin, then you would not include the value of fixed capital at all, because it does not enter the value of production. Only the wear and tear of that fixed capital enters the cost of production, and is thereby relevant to the calculation of that rate of profit. The total value of the advanced fixed capital is only relevant in calculating the annual rate of profit,a nd thereby the annual average rate of profit, but in that case, the wear and tear of that fixed capital should not be included. And, as you say, if it is the annual average rate of profit that is being calculated, it is not the value of the laid out capital that should be used, i.e. the total expenditure on wages, and materials in the year, but only the amount advanced for wages, and materials for one turnover period.

Given that Engels’ estimate of the rate of turnover of capital in the mid 19th century, given in Capital III, Chapter 4, was 8.5, and given the rise in social productivity since then, I estimate that the current rate of turnover of capital is no less than 30, so that to obtain a figure for the advanced capital, it is necessary to divide the figure for the total laid out in wages and materials by 30 to obtain a figure for the advanced variable and circulating constant capital. Using that figure suggests that the average annual rate of profit continues to rise.

But, the problem is that the figure for the circulating constant capital is impossible to obtain directly from the GDP data, because as I have set out previously the figure for intermediate production, which is often cited as being the figure for the circulating constant capital, is in fact, only the figure for the value of the circulating constant capital consumed in final production, and is (on the basis of Marx’s model of simple reproduction),as Marx says, only the value of constant capital created by labour in the current year, i.e. (Department I v +s). It excludes the value the circulating constant consumed by Department I, in current production, and replaced by Department I directly from production on a like for like basis.

In other words, using Marx’s model,

Department I

c 4000 + v 1000 + s 1000 = 6000

Department II

c 2000 + v 500 + s 500 = 3000

The equivalent for GDP here is the 3000 of output value of Department II. It represents the value of final production, and is societies consumption fund. It is equal to total factor incomes i.e. wages and profits of £2,000 in Department I, and wages and profits of £1,000 in Department II, which would likewise appear in the data for National Income.

In examining the data for national output, the 2,000 of constant capital in Department II, is classified as “intermediate production”, because it is only equal to the new value created by labour in Department I during that year, i.e. the £2,000 of new value created by Department I labour, which is divided into £1,000 of Department I wages, and £1,000 of Department I profits.

But, as Marx points out, at length in TOSV, this value of £2,000 of “intermediate production” considered forensically contains not one gram of value of constant capital. It contains only the new value created by labour during the current year.

But, the total value of output, taking out this “intermediate production”, which would be double counted if we added to the output figure of final output (i.e. added it to the £3,000 of value of Department II, in which it is already included) is then £7,000, because it also includes the value of £4,000 of Department I circulating constant capital, i.e. the value of raw materials, semi finished products used in the production of Department I output, and the value of wear and tear of fixed capital in Department, which is physically replaced “on a like for like basis” out of current production of Department I, and thereby creates a revenue for no one.

Indeed, as Marx describes in Capital III, Chapter 49, and at greater length in TOSV, its precisely because the use values that comprise this circulating constant capital have to be replaced on a like for like basis (and the same applies to the physical use values that comprise the variable-capital, which must be physically replaced on a like for like basis if the consumed labour-power is to be reproduced) that the rate of profit must be calculated on the basis of the current reproduction costs, i.e. value of that capital, thereby taking into consideration the changes in social productivity, and consequently value of that capital, in calculating the rate of profit.

To use Marx’s example, a farmer who produces grain might have 1000 kg of grain used as 200kg as seed, and 800 kg paid as wages to workers during the year, after consuming the surplus product himself from the previous year.

This year the output is 1200 kg’s, and out of this he must replace on a like for like basis the 200kg used as seed. This 200kg, thereby amounts to a revenue for no one, it is consumed by capital not revenue. A further 800 kg is withdrawn from this output to set aside as variable capital to be paid as wages so as to reproduce the consumed labour-power. That leaves 200 kg left over as surplus product, which is consumed by the farmer.

The total output is 1200 kg, but only 1000 kg forms the consumption of this society, consumed by workers (800 kg as wages), and the capitalist farmer (200kg as profit). Calculated on the final output that represents the consumption fund (GDP), the rate of profit would be seen as 200/800, but in reality this is only the rate of surplus value. The actual rate of profit here is 200/1000.

The importance of Marx’s insistence on calculating the rate of profit on the current reproduction costs rather than historic prices can then be seen, because given that any rise in productivity reduces the value of the circulating constant capital that must be physically replaced “on a like for like basis”, any rise in social productivity reduces the labour-time required for such physical reproduction, and thereby reduces the value of that capital, and so raises the rate of profit. Given that capitalism raises the level of social productivity constant (indeed that is the basis of the law of the tendency for the rate of profit (profit margin) to fall, as the mass of output rises, and the proportion of the value of each unit of output comprised of material rises, whilst the proportion comprised of wear and tear of fixed capital, and of labour declines) this indicates why the annual average rate of profit, tends to continually rise, as the value of the consumed material, per unit, falls, whilst the value of fixed capital stock continually falls, so that less current labour-time is required to replace this constant capital on a like for like basis, and the same process reduces the value of wage goods, reducing the value of labour-power, as less current labour-time is required to reproduce it on a like for like basis, so that the rate of surplus value rises.

The propositions as set out by marx in the later chapters of Capital, and in TOSV are fairly clear.

* Social productivity continually rises, and this means that the labour-time required to physically reproduce the fixed capital, and circulating capital “on a like for like basis” continually falls, and this means that the rate of profit rises, even if the mass of surplus value were to remain constant.

* The same rise in social productivity means that the wage goods that comprise variable capital can be replaced “on a like for like basis” with less social labour-time, so that the value of these goods falls, the value of labour-power falls, and so the rate of surplus value rises, which means the mass of surplus value rises, which also thereby causes the rate of profit to rise.

* However, the same rise in social productivity means that the technical composition of capital is changed, and this leads to a change in the organic composition of capital. A rise in social productivity means by definition that a given quantity of labour processes a greater mass of raw material, so the technical composition of capital is changed accordingly. If previously 10 hours of labour processed 100 kilos of material, it might now process 200 kilos of material so the technical composition changes from 1:10 to 1:20. Even if the above rises in social productivity have reduced the unit value of the material, say from £1 per unit to £0.75 per unit, the organic composition rises because the consumed material value is now £150, so that the organic composition will have risen from 1:10, to 1:15.

* This same change in social productivity will have reduced the value of machines themselves, and caused a moral deprecation of the existing fixed capital stock, because less current social labour-time is required to reproduce it “on a like for like basis”. That means, as Marx sets out in Capital III, Chapter 6, that along with the fall in the proportion of labour in each unit of output, the value of wear and tear of fixed capital in each unit of output also falls, and the fact that the replacement machines are themselves more efficient and productive, so that each machine produces many more units of output in a given time means that it falls even further.

* By contrast, the proportion of the value of each unit of output accounted for by material will have risen, even as the fall in the unit value of material itself falls, because in each unit of output a diminishing quantity of labour and wear and tear of fixed capital is embodied. This is Marx’s explanation of the law of the tendency for the rate of profit (profit margin) to fall, because rising productivity means that a continually diminishing portion of the value of each unit of output is accounted for by labour, and consequently surplus labour.

* The same rise in social productivity as well as causing the countervailing tendencies for the fall in the profit margin as described by Marx in Capital III, Chapter 14, causes the rate of turnover of capital to rise, and that causes the annual average rate of profit to rise, even as the profit margin falls. These are just reverse expressions of the same phenomenon of rising social productivity, as Marx describes. It means that less capital must be advanced to produce the same level of output, and surplus value, which facilitates therefore, the release of capital, which can then be used to increase output, and speed up economic growth, and thereby also produces a greater mass of surplus value, though this surplus value is spread across a much greater volume of output, so that the profit margin/rate of profit falls.

* Marx’s explanation of the law of the tendency for the rate of profit to fall is premised on this rise in social productivity, and consequent rise in the mass of profit and capital, as opposed to the explanations for the falling rate put forward by Smith, Ricardo, malthus and others, which essentially come down to a squeeze on profits caused by rising costs – wages, rents, etc It assumes that capitalism continues to be based upon the production of material commodities, in which this rise in productivity leads to this continually increasing technical composition, and consequently organic composition of capital, as the proportion of material value in each unit of output rises.

However, in modern economies where the production of physical commodities now represents only around 20% of value and surplus production, and where 80% of value creation is accounted for by service industry, where no such increase in the quantity of processed material occurs, it is clearly of no relevance.

I think it might be helpful to recall how succinctly Marx describes the issue with the rate of profit, and why it is so important to his analysis of capital:

“Therefore, since the aggregate mass of living labour operating the means of production decreases in relation to the value of

these means of production, it follows that the unpaid labour and the portion of value in which it is expressed must decline as compared to the value of the advanced total capital. Or: An ever smaller aliquot part of invested total capital is converted into living labour, and this total capital, therefore, absorbs in proportion to its magnitude less and less surplus-labour, although the unpaid part of the labour

applied may at the same time grow in relation to the paid part. The relative decrease of the variable and increase of the constant capital, however much both parts may grow in absolute magnitude, is, as we

have said, but another expression for greater productivity of labour.”

Now I suspect, given the mechanisms of capital in distributing profits according to size of capitals; in equalizing rates of profit; that turnover rates are subsumed in that general process, and that the rates of profit as derived by ucanbepolitical’s methodology will closely parallel those derived by Kliman, and Michael.

As for Boffy’s assertions, which are, as I understand them, basically that it’s impossible to know the rate of profit, and that even if known, the rate of profit has no determining relation to either the accumulation of capital, “macro” developments in the capitalist economy like recession, expansion; and no relation to actions the bourgeoisie take to offset the unknowable decline…….well I think there’s at least 100 years of capitalist history that argues precisely against those assertions.

Boffy can’t accept the evidence, he thinks we are 18 years in to an Expansionary Long Wave. We have to be because Long Waves work like clockwork for him, even over a period of centuries.

The trends lie in the same direction, the volatility is however greater. Please remember I use current cost fixed assets not historic cost. Theoretically I should adjust for median age of fixed assets but have not done so except in an article on the site which tests the validity of the valuation placed on fixed assets or produced assets. For comparison purposes here are two links

http://theplanningmotive.com/2017/09/26/a-new-and-more-c…e-rate-of-profit/

which covers the same period (you should also read auditing the rate of profit) and

http://theplanningmotive.com/2017/11/12/cracking-the-rat…-profit-in-china/

In the latter article the turnover formula is proven by the data from the National Bureau of Statistics of China itself. The formula yields 6.04 turnovers p.a. and so does adding the days for inventory turnover to the days between sale and payment. Together they also add up to 6 with inventory contributing 46 days of the 61 day turnover and the credit period the rest. The Chinese Bureaux has a greater concern for turnover than does the BEA.

We cannot be selective with the SNA. We cannot on the one hand say we can determine the rate of profit with a degree of accuracy but not use the SNA for determining turnover times or the annual rate of turnover. Both suffer from the effects of duplication, omissions and imputations. But this is the salient point, a rate of profit which incorporates the rate of turnover, for all its faults, will be more accurate than a rate of profit which omits it.

I understand your emphasis, but if the trends are the same, then one of the critical questions is what is the actual deviation over the time periods and for each of the categories that Michael presents in his elaboration.

My latest comment seems to have disappeared so I am repeating it.

The rate of profit derived which incorporates turnovers, in terms of direction is similar to that derived by yourself. However it is more volatile and peaks and troughs differ. To examine the differences please follow the following links. The first is for the US rate of profit in manufacturing the second is for the rate of profit in China for manufacturing 2015. Please note I do not use historic cost of produced assets as does Michael but current cost of produced assets. On my site I have tested the value of the produced assets but do not adjust for median age in the postings listed below because in some countries median ages cannot be arrived at. Nor do I adjust for the chaos caused by the capitalisation of Research and Development together with in-house software (which form the bulk of I.P.

http://theplanningmotive.com/2017/09/26/a-new-and-more-c…e-rate-of-profit/

http://theplanningmotive.com/2017/11/12/cracking-the-rat…-profit-in-china/

The article on China has a singular importance. The Chinese Statistical Bureaux is more interested in turnover than is the BEA. It has a series on the aggregate days outstanding between sale and payment. The formula in 2015 for Chinese manufacturing yields a turnover of 6.04 and this is confirmed by adding the days inventory circulates to the days of payment. When done this too yields a rate of 6 annual turnovers from M….M.

I have read Malto’s article previously. Yes the inventory cycle will mimic the turnover cycle during the mid-part of the cycle so can be used as a proxy, but it is not the same as the turnover of circulating capital where credit plays such a key role.

Finally it is wrong to say we can use the same system of national accounts to derive a rate of profit but not to derive a rate of turnover. Both rates are confounded by the same duplications, omissions and imputations. However a rate of profit that incorporates turnover is more accurate that a rate that does not.

Do you include fictitious capital and profits on Wall Street in these calculations? The ‘organic composition of capital’ has less to do with that, though the banks certainly are always upgrading their software and hardware. I.E. is financial capital included in the definition of ‘productive capital?’ It would not seem to be… but I don’t know.

In all these measures profits made by the finance sector are included – much of which is fictitious. Financial capital is not productive capital as it does not reproduce new value, even if there is some investment in hardware etc. Financial profits and investment is on the back of productive capital. Finance/credit is necessary under capitalism but not productive in itself. We could just measure profitability of productive capital and indeed that would reveal the underlying health of capital. Some measures do just that – ie Carchedi’s paper.

But you included finance capital then. Certainly, a division between these two might show that ‘productive’ capital is actually even less profitable. Thanks.

There is a general misconception in the discussion, as I have set out in response to Citizencoke above, which is that the aim of production is the maximisation of value. Quite the contrary. The aim, as marx describes in his explanation of the Law of Value in his letter to Kugelmann, is the minimisation of value, and maximisation of use value. That is also the basic contradiction within the commodity itself that Marx describes in TOSV, Chapter 17, which creates the potential for crises of overproduction.

The reason I buy a washing machine is that the value I expend, in the form of money to obtain the washing machine is less than the labour I must expend directly washing clothes, to obtain the use value of clean laundry. The same applies to the purchase of vacuum cleaners, dishwashers and so on, so as to be able to enjoy these use values, whilst minimising the value of them, i.e. minimising the expenditure of labour required to produce that use value.

It is in fact, the same when rather than buying a machine to perform this task, I enjoy the benefits of the division of labour to buy the labour service of a jobbing tailor, or a cook etc. When I buy any of these things I engage in a free exchange of value, of a buyer and seller of commodities at their value.

“When I have a coat made for me at home by a jobbing tailor, for me to wear, that no more makes me my own entrepreneur (in the sense of an economic category) than it makes the entrepreneur tailor an entrepreneur when he himself wears and consumes a coat made by his workmen. In one case the purchaser of tailoring labour and the jobbing tailor confront each other as mere buyers and sellers. One pays money and the other supplies the commodity into whose use-value my money is transformed. In this transaction there is no difference at all from my buying the coat in a shop. Buyer and seller confront each other simply as such. In the other case, on the contrary, they confront each other as capital and wage-labour. As for the domestic servant, he has the same determinate form as the jobbing tailor No. II, whom I buy for the sake of the use-value of his labour. Both are simply buyers and sellers.”

And, as Marx says, if I have this coat produced for me at home, or in the example he gives, a piano is built at home, if this piano were later to be sold as a commodity, the owner of this piano can make no profit from it, because the piano maker who comes freely into the house to build the piano obtains in exchange for their labour its value, just as does the cook who comes freely into the house to cook the lamb chops for the rich person. And, if the piano or the pair of trousers are then to be sold, all that the owner of the piano or the trousers can obtain for them is the value they have themselves paid out for the labour provided by the piano maker/tailor alongside the value of the materials used in the production of the piano, trousers.

The aim here is not to increase value, expended labour-time but to minimise it, because thereby a greater quantity of use value is obtained for any given amount of expended labour. And as pointed out in response to Citizencoke, the aim of the capitalist producer is also not to maximise value, but to maximise surplus value. As Marx points out, Ricardo was quite right in distinguishing against Smith that the aim of capitalist production is not the maximisation of the Gross product, but the maximisation of the net product.

Each capitalist seeks to maximise their own net product surplus value, by minimising the individual value of their production, whilst maximising the volume of output/quantity of use values produced, and it is essentially this drive which creates the periodic outbreak of crises of overproduction as the production of these use values exceeds the capacity of the market to absorb them at prices that reproduce the consumed capital.

Apologies. I posted this to the wrong thread.

To answer your question Sartesian, I would direct you to Graph 4 found with the following link http://theplanningmotive.com/2017/09/20/468/ This shows the convergence between the rate of surplus value and the mass of profits, but not with the rate of exploitation which excludes turnovers. The other graph (graph 5) can be found http://theplanningmotive.com/2017/09/04/report-on-the-us…1st-quarter-2017/ This graph shows how the mass of profits+interest only rises to new peaks when the rate of surplus value exceeds the rate of exploitation. In other words it is a function of turnover. I continue to define the US economy as being in the phase of rising animation not the phase of prosperity because the mass of profits have not yet exceeded the previous peak of 2014 and is unlikely to do so until the rate of turnover accelerates further pushing the rate of surplus value above that of exploitation. Hence turnovers allows us to analyse the economy in a new and more precise way. I consider this graph to be a more accurate prognostic tool than the triple indicator graph prepared by Carchedi that appears here in Mchael’s post.

I will be writing a report on the US economy in early December when second quarter gross output and value added is published which will allow me to extend the rate of turnover to the 2nd quarter. Preliminary estimates for S&P profits for the third quarter of 6.1% (FactSet) suggests the mass of corporate profits has not increased compared to the previous year’s quarter (most of the S&P increase derives from corporations with the largest foreign sales and oil companies.) This being so the mass of profits still rests about 10% below the 2014 peak.

Dear friends,

I´m not sure if it´s the correct place for my question, but just in case. I understand it´s a very basic question on the decline of profit rate. Marx thought that, from a historical point of view, as a consequence of this decline, capitalism would arrive to an end, because of the lack of incentive for new investments.

Anyway, capitalists make use of profit not only for consumption but, mainly, for new investments and accumulation. So, if profit rate is not enough to keep capitalists investing, wouldn´t it happen the same thing with public investments or -in a self-management system- with the employees of the enterprise?

Resources for accumulation have their origin in profit rate. But resources for accumulation in a worker self-managed system or in a public ownership system, wouldn´t have to come also from surplus created by the enterprise?

So, the decline of the profit rate, in spite of the end of capitalism, wouldn´t have as a consequence the end of the accumulation options, in any kind of means of production ownership system?

Thank you for the clarification.