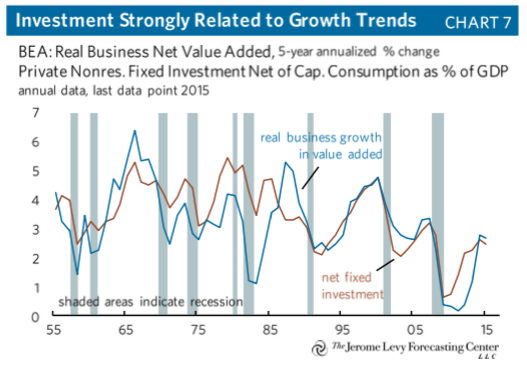

I’m always banging on about the close connection between the movement of investment (expenditure on the means of production) and economic growth. In my view, the evidence is overwhelming (The profits-investment nexus) that it is investment that is the main swing factor in booms and slumps, not personal consumption as many Keynesians focus on. And it is also a key factor in the long-term growth of labour productivity.

A new analysis by the Levy Forecasting Center, an institute that follows closely the views of Keynes, Kalecki and Hyman Minsky, also confirms this view. The report comments that “unsurprisingly, net fixed investment is strongly related to growth.”

The slowdown in real GDP growth since the end of the Great Recession is clearly connected to the slowdown in business investment growth

Business investment in the US has ground to a halt and the age of the existing means of production has risen as ageing equipment and technology is not replaced.

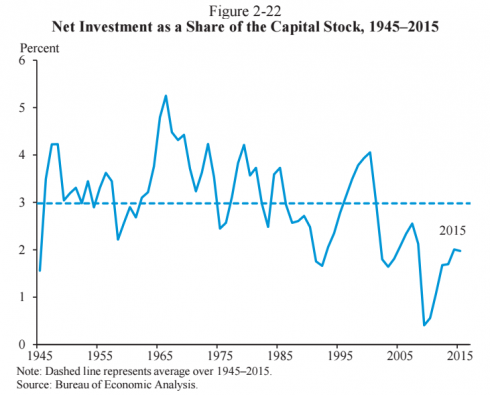

As Levy puts it: “In 2009, net investment as a share of the capital stock fell to its lowest level in the post-World War II era and the nominal capital stock even declined. Although net investment has rebounded somewhat in the recovery, its level as a share of the capital stock remains well below the historical average and it declined slightly in 2015.”

Levy points out that investment growth contributes to labour productivity growth most directly through capital deepening—the increase in capital services per hour worked. “That had added nearly 1 percentage point a year to labor productivity growth in the post-war period to 2010. But since 2010, capital deepening has subtracted from productivity growth and contributed slightly more to the slowdown from 1948-2010 to 2010-15 than did the slowdown in total factor productivity growth.” In other words, it was just the slowdown or cutback in the sheer amount of investment that did the damage, even more than any slowdown in the use of new techniques.

However, the Levy Institute then fails to explain this investment slowdown. It argues that “this broad-based investment slowdown is largely associated with the low rate of output growth both in the United States and globally”. This is a circular argument. The slowdown in economic growth is due to the slowdown in business investment, and that in turn is due to the slowdown in growth!

This is close to the argument of the Keynes-Kalecki thesis (espoused by the Levy Institute) that it is investment that creates profit, not vice versa. This nonsensical view should be countered with the realistic one that is the movement in profitability and profits that moves business investment. And as I and others have shown empirically, this is what happens in a capitalist economy.

For example, Andrew Kliman and Shannon Williams have shown that the fall in US corporations’ rate of profit (rate of return on investment in fixed assets) fully accounts for the fall in their rate of capital accumulation. And they conclude that “Since a long-term slump in profitability, not diversion, is what led to the trend towards dis-accumulation, it is unlikely that the trend can be reversed in the absence of a sustained rebound of profitability”.

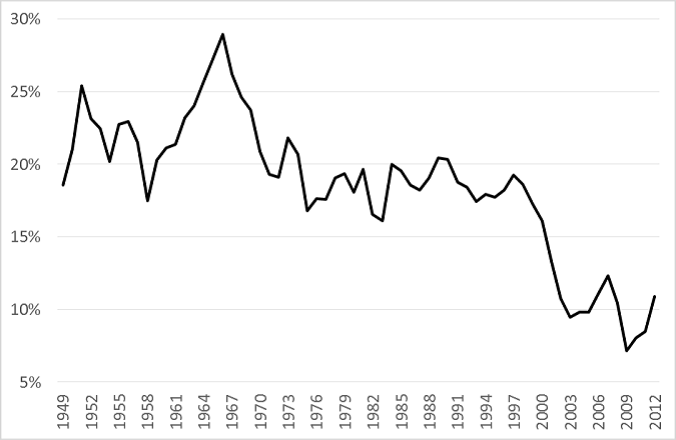

Indeed, if we delineate the rate of profit in the non-financial productive sectors of the economy, we find that profitability has struggled to rise since the 1980s and so along with it, business investment growth has slowed. Anwar Shaikh, in his latest book, Capitalism, adjusts the official data for measuring the US rate of profit and shows that profitability has stagnated at best since the early 1980s, rising to a modest peak in 1997 before slipping back to a post-war low by 2008.

Similarly, Australian Marxist economist Peter Jones has shown that if the ‘fictitious’ components of profitability are removed from the calculation of the US corporate rate of profit, then the ‘underlying’ rate of profit has never been lower (http://gesd.free.fr/jonesp13.pdf). Profitability of productive capital consolidated during the 1990s but then dived to post-war lows just before the Great Recession, with little recovery since.

The US rate of profit (excluding ‘fictitious profits’) %

The Levy analysis also makes the valid argument that high corporate debt is impeding new investment. Non-financial corporate sector debt relative to ‘value-added’ (i.e. sales revenue) is at a historically high level and this is weighing on capital spending.

US business investment in the first quarter of 2017 had a slight uptick after falling for four quarters. That followed a return to positive territory for corporate profits in the second half of 2016 after going negative in early 2016.

Does this mean that investment and economic growth is set to pick up finally? Not according to Levy. Levy interestingly (in opposition to its own Kalecki thesis) note that “looking back, the capex decline in 2015-16 and the subsequent rebound lagged the profits decline and recovery.” But Levy reckons that the “corporate profits recovery is likely to stall by mid-year and capital spending will follow with a lag”. If that happens, the US economy will be heading down, not up, by the end of the year.

“Similarly, Australian Marxist economist Peter Jones has shown that if the ‘fictitious’ components of profitability..”

Here’s what I don’t get– if surplus value is the source for interest, rent, and profits, then other than theft, ponzi schemes, cooking the books etc., how can interest and rent be excluded as “fictitious components”??

If the claim is that capitalism is nothing but a ponzi scheme, well then we can stop wasting time with Capital, vols 1-3, can’t we?

Jones does not exclude rent and interest but profit from the purchase and sale of government bonds.

OK, profit from sales of government bonds. How is that “fictitious capital” or “fictitious profit”? How does that differ from profit from the sales of non-government bonds? Equities? Credit-default-swaps? Leveraged buy outs?

It does not differ. Jones does not account for these in his measure. If he did that might make a further change to his measure. Government bonds are by the far the biggest market though.

What is made or lost on the sale of government bonds, equities etc. is not “profit”. It is a capital gain, or loss. But, as Marx says, apart from inflationary gains, there can be no net capital gains or losses, because what is a capital gain for the seller of an asset is a capital loss for the buyer, and vice versa. As Marx puts it, its just a transfer of wealth from one hand to another.

If there were to be any net capital gain, it could only arise because of a drain from actual profit, i.e. from a drain from produced surplus value, and so for the purposes of calculation of the rate of profit should not be deducted.

I just think we’re better off eschewing all discussion of fictitious capital or fictitious profit as an “explanation” for either, both capital expansion and capital contraction.

Better to restrict the discussion to the ROP in manufacturing, utilities, construction, mining (including oil and gas)– and then analyze the growing importance of the FIRE sector, and the government, as a mechanism for distributing the total surplus value.

I agree that looking at the productive sectors is best. In way, that is what Jones was trying to do. It’s just that the official data require massaging to find that. Jones makes one attempt; Carchedi starts with your approach and I’m working on some more analysis

The first graph is compelling. I would suggest that comparing real business investment to net value added would result in an even tighter fit because of the distortions around depreciation. In any case net investment should be compared to net value added as both are net figures. Valuing produced assets is a real problem as well because of PIM. All efforts to modify the BEA’s valuation I find inadequate and having crunched whole series of numbers, produced assets for all its faults, but excluding I.P., provides a baseline over which to measure the rate of profit.

We tend to concentrate on gross value added not gross output. Yet the amount of circulating capital is amplified by the number of turnovers when we use gross output. In the case of manufacturing where turnover is around five and gross output more than three times that of value added, any movements in the gross output side will be magnified, and any linkages more apparent. I will be looking into this over the next few months. I am of the opinion that the gross output side could shine a clearer light on the reciprocal relationship between profit and investment.

I should have added that circulating capital is more responsive to changes in profitability. Fixed assets often have a gestation period of years. Hence it is in the realm of circulating capital that the answer should lie. In support of Michael’s argument, the fall in turnover times post 2014 results in reduced profits as well as an immediate increase in the amount of circulating capital required to achieve a given output. It is an immediate spur to reduce capital expenditure from the fixed side.

“In support of Michael’s argument, the fall in turnover times post 2014 results in reduced profits as well as an immediate increase in the amount of circulating capital required to achieve a given output. It is an immediate spur to reduce capital expenditure from the fixed side.”

I think you mean results in reduced rates of profit/profit margins. But, reduced turnover time/higher rate of turnover simultaneously and necessarily means a release of capital, and higher annual rate of profit, and consequently higher general annual rate of profit.

And, as Marx sets out, it is the annual rate of profit not the rate of profit/profit margin that is the determinant of accumulation. In other words, if the rate of turnover rises, so that less capital has to be advanced, relative to the capital laid out, then any given amount of profit will represent a larger amount of advanced capital.

For example, if a capital consists of £100,000 and turns over once during the year, so that all of the £100,000 is advanced, and the profit is 10% or £10,000, it will enable an accumulation of 10%. However, if the capital turns over twice during the year, so that only £50,000 of capital is now advanced, the annual profit of £10,000 will enable an accumulation of 20%, or double what it was previously.

There are plenty of reasons to be sceptical about this article. Net investment as a proportion of national income was highest during the recession of the 1980s, i.e. the period of lowest profitability. High wages (as a proportion of national income) then, meant that business replaced workers with machines even though profits were low.

Prior to the that investment as a proportion of national income was low during the 1950s, i.e. the peak years of the post war boom, when profits were high and machinery was cheap.

As for more recent history, there is no downward trend in profitability. The studies cited above have no reasonable estimate of the value of the fixed capital stock, exclude profits hoarded abroad, and have no estimate of turnover etc. They are completely unreliable not to say, misconceived and wrong.

Its perfectly easy to explain why investment as a proportion of national income has fallen recently in the US as a consequence of the growth of services, the movement of manufacturing abroad, and the low price of fixed investment.

“The studies cited above have no reasonable estimate of the value of the fixed capital stock, exclude profits hoarded abroad, and have no estimate of turnover etc. They are completely unreliable not to say, misconceived and wrong.”

Uhh… yeah they do, using BEA valuations of fixed assets as the marker, the index, to the value of fixed capital. What counts is the trend, that’s why you can use markers and develop an index over time. That’s one.

Two: Profits “hoarded” are irrelevant, once they are hoarded. The analysis deals with profits earned, or reported. A hoard comes from past profits (and revenues). Two trillion dollars held offshore the United States is not a current profit and has no relevance to calculations of the rate of profit.

US corporations due report profitability and revenues derived from operations outside the US –“rest of the world”–in the BEA parlance; and the trend over a long time is the growth of those “non-domestic” revenues; a trend “matched” in the short-term by results of the last quarter as reported by BEA where non-domestic contributions to corporate profits increased, and the domestic portions declined.

There are indeed estimates of turnover, however, the mechanisms of capital absorb those variations into the formation of the general or average rate of profit.

“They are completely unreliable not to say, misconceived and wrong”

That’s good to know. However if those reports are unreliable, then there should be away to empirically, practically show and calculate the rate of profit reliably and show the differences between the reliable and unreliable rates, and do the same thing with the misconceived/appropriate, wrong/right rates. But we never get that. In all of Boffy’s talk about turnover rates offsetting the decline in annual rates of profit, I have yet to see any calculation produced by Boffy or any other partisan of the proper, reliable, appropriate analysis of profitability, of a “right” rate of profit.

If the argument is that the rate of profit is irrelevant, that’s swell, or not, because then there is the correlation, coincidence of declining rates of profit (as crudely calculated as they may be) and various stresses and impairments in the accumulation of capital. This really requires some sort of explanation, other than “wrong” or “misconceived,” or “pure chance.”

Besides, I think Bill was busy arguing a couple of years ago that the maritime transport industry was not in the midst of a serious period of bankruptcy, contraction, brought on by overproduction and declining profitability, but actually, according to Bill, in the midst of a boom period. My memory isn’t what it was (influenced I’m sure by the Sessions appearance yesterday), so if I’m confusing Bill with someone else, I apologize. But I think I got that right, and that pretty much sums up the accuracy of Bill’s conception, appropriateness, and correctness in evaluating the bourgeoisie’s economy.

Bill,

I think you are right. Investment was relatively high in the 1980’s, for the reason that Marx describes that its when wages are high, and profits are squeezed that capital has an incentive to develop new labour saving technologies, so as to replace wages, create a relative surplus population, and thereby reduce wages, and raise the rate of surplus value.

“Improvements, inventions, greater economy in the means of production, etc. are introduced not at times when prices rise above their average level, but when they fall below it, i.e., when profit falls below its normal rate.”

(Theories of Surplus Value,II, Chapter 8, p 26 – 7)

Its for this reason, as Marx sets out in Theories of Surplus Value, Chapter 18, as against Ricardo, that the net product/revenue can rise even as the gross product/revenue falls, but may also rise even as the gross product/revenue may also rise.

In other words, the gross revenue may fall, as net revenue rises, as Ricardo correctly says, as against Smith, because the quantity of labour employed falls, wages fall, and profits rise. But, Marx says, that the net revenue can rise even where the gross revenue product rises, because the quantity of labour employed can fall, and wages fall, where that labour is replaced by machines. Revenue is then converted into capital, and in addition the additional profits can also be used to increase luxury consumption by capitalists and landlords.

Its important to note here that the situation that Marx is describing, and what arises during the 1960’s/70’s is a fall in the rate of profit of the type described by Adam Smith, and as Marx describes in Capital III, Chapter 15. In other words, its not a result of the law of the tendency for the rate of profit to fall, but is a result of a squeeze on profits caused by rising wages, and a fall in the rate of surplus value. That is what prompts the drive for the introduction of labour saving technologies. The fall in the rate of surplus value as a cause of a falling rate of profit is the opposite of the conditions that lead to the law of the tendency for the rate of profit to fall, which is premised upon rising productivity, and a rising rate of surplus value.

I think you are also right about the unreliable estimates of profits, and rate of profit. I’m tempted to say that no estimate of the rate of profit is better than a fallacious estimate of the rate of profit. As I’ve described before, even the data for GDP is wrong, as Marx describes in Capital II, III, and in Theories of Surplus Value, because its based on Adam Smith’s “absurd dogma” that the value of commodities is resolvable solely in revenues, and consequently that Gross National Output and Gross National Income are identical.

They clearly are not, as Marx describes, because the value of commodities, and so of National Output also includes the value of constant capital, which forms a revenue for no one. The National Income data is only data for revenues (v +s), i.e. only for the new value created by labour during the year. Consequently calculating a rate of profit on the basis of it is only a rate of surplus value, let alone an annual rate of surplus value, let alone a rate of profit!

Then as you say, particularly in the US, there is the question of the preponderance of multinational corporations, each of which has an incentive to minimise its stated profits in the US, and to hide them away in Ireland or Luxembourg or other countries with low rates of Corporation tax compared to the 35% rate in the US, and also because of the penalties faced by US corporations if they repatriate those profits.

Then there is the question of the failure to take account of the rate of turnover of capital, so that at best all we get is a sort of profit margin figure, which surprise surprise tends to fall over time, as the volume of output expands faster than the growth of variable capital, so that even as the annual rate of profit, and mass of profit rises, the profit margin falls.

Its a bit like saying that Tesco is about to go bust, and is unable to accumulate capital, because it only has a tiny profit margin, whilst the corner shop has a large profit margin, whilst in the process neglecting the fact that Tesco’s small profit margin is spread across billions of items it sells, whereas the corner shops larger profit margin is over only a few thousand.

I should also have said that estimates of the rate of profit based on manufacturing industry is pretty pointless in economies where manufacturing now accounts for only a small proportion of value and surplus value creation, and where it is service industries that account for around 80% of value and surplus value production.

Given the nature of service industries, and their reliance on labour and very little on the processing of circulating constant capital, and given that fixed capital investment in such spheres tends to be chunky, its no wonder that we see large profits but historically low levels of capital investment, in constant capital, at the same as continued accumulation of variable capital, and continued rises in employment.

“I think you are right. Investment was relatively high in the 1980’s”

Sources please. Where was investment relatively high in the 1980s? Not in the US. Investment in non-residential private fixed assets in the US doubled 1960-1969; tripled 1970-1979; increased only 75% 1980-1989; expanded 85% 1990-1999; then expanded only 28% 2001-2007 before turning negative such that the total increase 2001-2009 measures only 9 percent. So….except for the post 2001 period, the 1980s saw the lowest levels of investment.

Should we go through the same inquiry for Britain? or the EU? I’m willing, but maybe Boffy should provide some real data, or real sources. For once.

“Corporation tax compared to the 35% rate in the US, and also because of the penalties faced by US corporations if they repatriate those profits.”

Corporations don’t pay a 35% tax rate in the US. That’s a max rate, unadjusted for deductions, allowances, etc. The actual average rate paid by corporations fluctuates between 12 and 18 percent.

Secondly, corporations face absolutely no penalties if they repatriate profits. There is no penalty for repatriation. The amounts repatriated are subject to the general tax rates applied to other income. That’s all. And the allowances that will reduce that rate also apply.

US corporations pay zero US income tax on profits earned outside the United States, until such time as the profits are returned to US jurisdiction.

Finally Boffy talks a good game about rate of turnover, yet he has never provided a mechanism for evaluating what those rates really are, in the real world, with real corporations engaged in real production and real circulation. Consequently, Boffy has no idea what the actual rates of turnover are and how they might have changed, and how that change has impacted the general rate of profit.

Bill,

The data for the share of investment in GDP is also interesting when examined on a yearly basis, from the perspective set out, because it shows precisely the point of a rise in investment as a percentage of GDP at that point of the long wave cycle where labour supplies have become tight, and wages had risen leading capital to seek out new labour saving technologies.

It rose sharply from around 1968 (the point Mandel argues marks the start of the end of the post war boom), before falling sharply with the onset of the 1974 crisis, and oil price spike. But, it then rises even more strongly through the late 1970’s, for the reasons I set out that capital seeks to introduce this new labour saving technology, so as to create a relative surplus population, and drive down wages/increase the rate of surplus value.

It peaks at 20.5% of GDP in 1979, before falling again as the recession of the early 1980’s struck, before rising again, reaching a peak in 1984 of 20.3%. At the point that the rate of profit starts to rise again then in the late 1980’s, the share of gross investment actually starts to fall again.

this chart from the St Louis Fed, illustrates the point.

“this chart from the St Louis Fed, illustrates the point”

The problem with THAT chart is that it is a chart of gross private domestic investment, and thus includes real estate, rental and leasing– i.e. investment in homes, apartments etc.

Of course it’s just one of the many problems Boffy has with assessing reality.

The reason that the BEAs estimates of the value of the fixed capital stock are unreliable is straightforward, they are based on the revenues earnt by capital in other words they are neo-classical.

Therefore, they vary directly with changes in the mass of profit. As profits rise, so does the estimate of the value of the fixed capital stock, and so the rate of profit does not change.

This is hardly unimportant, and yet it is not considered (as far as I can tell) in the estimates presented above.

In fact the turnover period of the fixed capital stock has significantly fallen during the period of globalisation, due to the proportion of investment in software, which is now around a third of all investment, but is depreciated in just two years, and yet it is claimed the turnover of capital has slowed how?

Furthermore the price of machinery has fallen by around a quarter in real terms over the last two decades.

The rate of profit is estimated only against capital advanced, once the capital is fully depreciated that capital is no longer advanced, even if the ownership of the capital continues to earn its owner a rent. Estimates of the life of capital investments presented by the BEA in their estimates of current cost fixed capital stock, measure this period.

While there is obviously a relationship between the rate of profit and investment this needs to be treated cautiously net investment as a proportion of national income was at its highest during the recession of 1980-82 as is clear from the first chart in this article. The overall level of investment does not only depend on the general level of profits, but the price of capital, structure of production etc.

Profits hoarded abroad are “irrelevant” to the BEA, irrelevant in terms of the estimates of the rate of profit presented here, but hardly irrelevant to the corporations that own them. If annual declared profits are say around $2 trillion, if a further $2 trillion are hoarded abroad, this is obviously enough to obliterate the claimed downward trend in the rate of profit, even without including the other points made above.

The reason that the BEAs estimates of the value of the fixed capital stock are unreliable is straightforward, they are based on the revenues earnt by capital in other words they are neo-classical”

First off, the fluctuations in the valuation of the aggregate non-residential fixed investment as determined by “earning power” is precisely what Marx indicated occurs with capital, and the necessary devaluation of capital when profitability declines, so Bill is arguing that the problem with the BEA assessment is that it reflects what Marx explained….. too faithfully.

That the assessed value of the stock of private fixed investment actually declines during economic contractions is a very real, non neo-classical, occurrence, right in line with Marx’s necessary devaluation of capital that helps “correct” and “restore” capitalism to profitability.

This is the initial reason why we look at the trend of private fixed asset valuations over long periods of time– TRENDS.. i.e. the general pattern of capital accumulation..

Secondly, levels of private fixed asset investment are not determined by earnings.

BEA determines non-residential fixed investment, the “bulk of which consists of capital expenditures by private business” by including investment in structures, investment in equipment, investment in software and research and development.

That’s the second reason that we look at both the valuations and the increments of expansion over longer periods of time, the TREND, and why we can observe the TREND become its opposite at certain critical junctures, as occurred with the bust in the maritime transport shipping industry.

“In fact the turnover period of the fixed capital stock has significantly fallen during the period of globalisation, due to the proportion of investment in software, which is now around a third of all investment, but is depreciated in just two years, and yet it is claimed the turnover of capital has slowed how?

Furthermore the price of machinery has fallen by around a quarter in real terms over the last two decades.”

The proportion of private non-residential fixed assets consisting of intellectual property, R&D, software, etc. was 15.1% in 2008 and 15.8% in 2015. Hardly a momentous shift, nor hardly one that significantly impacts the the turnover of the entire mass of fixed assets necessarily deployed in aggregate for production, but realized only partially in valorization.

And of course we might ask have depreciation rates as a portion of total private non-residential fixed assets (exempting as always, real estate, rental, and leasing) increased?

“Profits hoarded abroad are “irrelevant” to the BEA, irrelevant in terms of the estimates of the rate of profit presented here, but hardly irrelevant to the corporations that own them. If annual declared profits are say around $2 trillion, if a further $2 trillion are hoarded abroad, this is obviously enough to obliterate the claimed downward trend in the rate of profit, even without including the other points made above.”

Profits from past production, hoarded abroad and not deployed in further investment in production are indeed irrelevant. Two trillion held in overseas investment accounts has impact on profits to the degree that any investment has an impact, but the mere existence of 2 trillion has no meaning. Say the 2 trillion is sitting in accounts yield 1% interest; what is the impact on profitability– the 2 trillion or the 20 billion?

“Secondly, levels of private fixed asset investment are not determined by earnings.”

I mean that the levels of PFI are not VALUED by the earnings accruing to physical stock.

Bill,

I gave an indication of the effect of the increase in the rate of turnover on the rate of profit in my book Marx and Engels Theories of Crisis.

I have estimated there, using the rate of productivity growth as a proxy for the annual increase in the rate of turnover that the rate of turnover of capital today is around 3 times what it was in 1950. In other words, if the rate of turnover in 1950 was 20, today it is 60.

The annual rate of profit and so general annual rate of profit is essentially the rate of profit multiplied by the rate of turnover of capital.

Engels in Capital III, comments, that in the mid 1800’s, the rate of turnover was approximately 8. If the rate of profit in the mid 1800’s was then say 20%, the general annual rate of profit would have been 160%. If the rate of profit in 1950 was say 15%, in line with the law of falling profits, the general annual rate of profit would be 300%. Similarly, if say the rate of profit in 2015 had fallen to 10%, the general annual rate of profit would be 600%.

Engels setting out the importance of the rate of turnover on the general annual rate of profit says the following, in relation to the role of communications.

“The chief means of reducing the time of circulation is improved communications. The last fifty years have brought about a revolution in this field, comparable only with the industrial revolution of the latter half of the 18th century. On land the macadamised road has been displaced by the railway, on sea the slow and irregular sailing vessel has been pushed into the background by the rapid and dependable steamboat line, and the entire globe is being girdled by telegraph wires. The Suez Canal has fully opened East Asia and Australia to steamer traffic. The time of circulation of a shipment of commodities to East Asia, at least twelve months in 1847 (cf. Buch II, S. 235 [English edition: Karl Marx, Capital, Vol. II, pp. 251-52. — Ed.]), has now been reduced to almost as many weeks. The two large centres of the crises of 1825-57, America and India, have been brought from 70 to 90 per cent nearer to the European industrial countries by this revolution in transport, and have thereby lost a good deal of their explosive nature. The period of turnover of the total world commerce has been reduced to the same extent, and the efficacy of the capital involved in it has been more than doubled or trebled. It goes without saying that this has not been without effect on the rate of profit.”

As I set out in my book, a similar thing can be seen to have happened in relation to the introduction of containerisation. I also set that out in my series of blog posts on Marx’s Law of the Tendency for the Rate of profit to Fall, and in particular I noted, the World Bank Report using data from the McKinsey Report on containerisation.

“the productivity in 1965 of dock labour (prior to containerisation) was 1.7 tons per hour. Post containerisation, in 1970, that had risen to 30 tons per hour. The average ship size went from 8.4 GRT to 19.4 GRT, insurance costs fell from £0.24 to £0.04, and capital tied up in transit halved from £2 per ton to £1 per ton. Today, 90% of goods are transported by container, in an integrated road, rail and sea system. As the report suggests, the reduction in cost and increase in speed has also had a significant effect in stimulating the circulation of commodity-capital”

But, as I also note in that blog post, the effect of the Internet in speeding up communications, electronic payments and so on, especially in a global economy where service industry is now predominant – think of global downloads of music, video etc – is probably even more significant. I also noted the role of the creation of Customs Unions and single markets like the EU, and the role of the Schengen Agreement in dismantling borders and other such restrictions on the free movement of goods and services.

I’ll give another reference to these in a separate post to avoid it being blocked due to hyperlinks.

I have dealt with this in more detail here. It also includes a hyperlink to another report by McKinsey on the role of the Internet.

In this further post in that series I estimated that the average rate of turnover for capital in car production is around 52. But, for the reasons described even that is rising, and is far from the highest rate of turnover of capital.

Variable capital is being turned over every few minutes in a fast food restaurant, for example. In fact, given that workers are always paid in arrears, the variable-capital advanced to production, is turned over many times before the workers themselves even receive any wages!

One of the problems with Boffy’s account, using “productivity” as a surrogate for turnover time, is that it ignores the most important factor in the increase in productivity and that is increased investment in fixed capital.

It’s all well and good to point out how containterization improved productivity, and how that led to improved circulation and reduced turnover. It’s not well and good to leave out the incredible expansion of fixed capital, bound up in ships, ports, cranes, containers, LNG units, dry bulk carriers in the calculation of turnover rates. That’s the key for Marx, as Marx identifies in the Grundrisse and other portions of the Economic Manuscripts. The turnover of the aggregate capital slows as proportionately less new value is aggrandized.

Example, case in point, SLOW steaming for chrissakes.

For a “counter” example, look at what Boffy quotes from Engels: “The Suez Canal has fully opened East Asia and Australia to steamer traffic. The time of circulation of a shipment of commodities to East Asia, at least twelve months in 1847 (cf. Buch II, S. 235 [English edition: Karl Marx, Capital, Vol. II, pp. 251-52. — Ed.]), has now been reduced to almost as many weeks.”

Is there anything more incomplete, more naive, than arguing, as Boffy does that the turnover time of all the capital deployed has been reduced WITHOUT including the VALUE of the capital embedded in the Suez Canal itself? The value that embedded in the expanding fixed capital of greater number of ships, of a greater size, and greater value? You cannot measure turnover of capital simply by the circulating capital.

Boffy, your figure for 52 is surely based on assembly time. It means that every 6 days, working capital turns over. So clearly, from your perspective, the car companies only pay for parts when they are delivered. In turn 6 days later they are paid for the completed cars which are collected from the end of the production line by dealers who buy them C.O.D. Actually, at the moment, car inventories are about 100 days compared to a usual 73 days which is spread between car manufacturers and dealers. If we take the capitalist formula of current assets/current liabilities we get a figure of about 7.8 turnovers which believe it or not coincides with the figure obtained for the car industry by the turnover formula. This independent figure of 7.8 is provided by Wall Street analysis who crunch individual balance sheets. If you want to look for the link between investment and profits the first place is the most responsive place, circulating capital. Any slowdown in turnover, and I publish the figures quarterly, has the simultaneous effect of increasing the need for capital while reducing the production of profit. Capitalists are not fools. Faced with having to fork out more capital for the same output, in return for less profits, they cut back on production. Superficially this appears as trimming inventories in order to increase the sales to inventory ratio which has fallen. If severe enough this involves fixed capital at a later stage because in order to reduce inventories you have to slow down production making part of the means of production redundant. Hence the link to fixed investment.

You say,

“Superficially this appears as trimming inventories in order to increase the sales to inventory ratio which has fallen. If severe enough this involves fixed capital at a later stage because in order to reduce inventories you have to slow down production making part of the means of production redundant. Hence the link to fixed investment.”

The real link to fixed investment here is to depreciation. If the fixed capital is not being fully utilised, it depreciates. Depreciation, as opposed to wear and tear, of capital represents a capital loss.

In other words, if fixed capital is being used extensively, which would be expected in a period of rapid economic activity, and higher rate of turnover, it will lose a greater proportion of its use value, and value in wear and tear, during any given period of time, because of its more extensive/intensive use, though on average it will theoretically transfer only the same amount of value in wear and tear to each unit of output (only theoretically because in practice the amount of wear and tear will not be proportionally greater).

But, if the fixed capital is under used, not only may this result in inefficient use of capital, causing unit costs to rise, but it will mean that the fixed capital may suffer increased depreciation, which is a function of time not usage. That is particularly the case where machinery etc. is left unused.

The wear and tear of fixed capital is transferred to the value of its output, but the depreciation of fixed capital is not. It is a pure capital loss, as though the machine etc. had been damaged, stolen etc. That is why firms try to ensure that fixed capital is used as extensively and intensively as possible, so as to minimise the capital losses from depreciation.

The other point about the fixed capital here is the effect on raising productivity and thereby raising the rate of turnover. Engels in Chapter 13 sets out the role of rising amounts of fixed capital as capital accumulation proceeds, in raising the level of productivity and thereby raising the annual rate of profit at the same time as the rate of profit/profit margin falls.

He says,

“Let us take three different conditions of an industrial capital.

I. A capital of £8,000 produces and sells annually 5,000 pieces of a commodity at 30s. per piece, thus making an annual turnover of £7,500. It makes a profit of 10s. on each piece, or £2,500 per year. Every piece, then, contains 20s. advanced capital and 10s. profit, so that the rate of profit per piece is 10/20 = 50%. The turned-over sum of £7,500 contains £5,000 advanced capital and £2,500 profit. Rate of profit per turnover, p/k, likewise 50%. But calculated on the total capital the rate of profit p/C = 2,500/8,000 = 31¼%

II. The capital rises to £10,000. Owing to increased productivity of labour it is able to produce annually 10,000 pieces of the commodity at a cost-price of 20s. per piece. Suppose the commodity is sold at a profit of 4s., hence at 24s. per piece. In that case the price of the annual product = £12,000, of which £10,000 is advanced capital and £2,000 is profit. The rate of profit p/k = 4/20 per piece, and 2,000/10,000 for the annual turnover, or in both cases = 20%. And since the total capital is equal to the sum of the cost-prices, namely £10,000, it follows that p/C, the actual rate of profit, is in this case also 20%.

III. Let the capital rise to £15,000 owing to a constant growth of the productiveness of labour, and let it annually produce 30,000 pieces of the commodity at a cost-price of 13s. per piece, each piece being sold at a profit of 2s., or at 15s. The annual turnover therefore = 30,000×15s. = £22,500, of which £19,500 is advanced capital and £3,000 profit. The rate of profit p/k then = 2/13 = 3,000/19,500 = 15 5/13%. But p/C = 3,000/15,000 = 20%.

We see, therefore, that only in case II, where the turned-over capital-value is equal to the total capital, the rate of profit per piece, or per total amount of turnover, is the same as the rate of profit calculated on the total capital. In case I, in which the amount of the turnover is smaller than the total capital, the rate of profit calculated on the cost-price of the commodity is higher; and in case III, in which the total capital is smaller than the amount of the turnover, it is lower than the actual rate calculated on the total capital. This is a general rule.”

Engels sometimes here talks about advanced capital where he actually means laid out capital, but those instances are obvious from the context. In example 1, the level of development is low, and the amount of fixed capital is low, leading to low levels of productivity and a low rate of turnover. The laid out capital in this case is, therefore, less than the total advanced capital, so the annual rate of profit (p/C) is lower than the rate of profit/profit margin (p/k).

In example II, the laid out capital and advanced capital are both £10,000, giving a rate of profit profit margin (p/k) of 20% the same as the annual rate of profit (p/C). That is because here the additional fixed capital causes a rise in productivity, and rise in the rate of turnover.

In example III, the laid out capital exceeds the value of the advanced capital because the fixed capital has increased the level of productivity, so that the circulating capital turns over much faster. Now the annual rate of profit exceeds the rate of profit/profit margin. The more capitalism develops, and the more fixed capital is introduced, which raises the rate of productivity and rate of turnover of capital, particularly as this process also reduces the value the fixed capital stock via moral depreciation, the more the annual rate of profit rises, even as the rate of profit/profit margin declines.

That is why as Engels describes these huge developments that took place in production and communication such as the opening of the Suez Canal, or the development of the Bessemer Process for steel production, bring about these sharp rises in the annual rate of profit, even as the rate of profit falls. This is another aspect of the process that Marx describes whereby this rise in productivity continually diminishes the proportion of fixed capital value in total output, because even though the fixed capital stock grows, not only is it continually devalued by moral depreciation and revolutions in technology and productivity, but the growth of output significantly outpaces the growth of fixed capital.

As marx says in Capital III, Chapter 6

“The value of raw material, therefore, forms an ever-growing component of the value of the commodity-product in proportion to the development of the productivity of labour, not only because it passes wholly into this latter value, but also because in every aliquot part of the aggregate product the portion representing depreciation of machinery and the portion formed by the newly added labour — both continually decrease. Owing to this falling tendency, the other portion of the value representing raw material increases proportionally, unless this increase is counterbalanced by a proportionate decrease in the value of the raw material arising from the growing productivity of the labour employed in its own production.”

It is the fact that the proportion of fixed capital as well as of labour declines within the value of total output that causes the proportion of raw material value to rise as a proportion of output value. It is this continually rising share of material value in total output that Marx says represents the rise in the organic composition of capital that leads to the falling rate of profit/profit margin.

However, as I’ve written previously, if the nature of modern capitalism is dominated not by manufacturing and the processing of materials, but by service production, this tendency of a rising share of material value in total output no longer applies, and so, the basis for the law of the tendency for the rate of profit to fall disappears along with it.

Here’s Boffy, twisting and twisting the night away, trying to thread the eye of his needle with a camel:

“The real link to fixed investment here is to depreciation. If the fixed capital is not being fully utilised, it depreciates. Depreciation, as opposed to wear and tear, of capital represents a capital loss”

In a word: Baloney. The US BEA defines depreciation thusly:

“Depreciation, also known as Consumption of Fixed Capital,/5/ is a charge for the using up of private and government fixed assets located in the United States, which is defined as the decline in the value of the stock of assets due to wear and tear, obsolescence, accidental damage, and aging.”

Depreciation is NOT opposed to wear and tear, depreciation IS wear and tear. Depreciation is calculated over the entire mass of value embedded in the entirety of the fixed asset capital regardless of it being used “fully” or “partially.”

The difference in “use rates” of the fixed capital matters not so much to the depreciation of the assets, but rather how much of that depreciation can be captured, offset, reimbursed by the commodities yielded up in the production process. If Ford Motor has fixed capital of 4X and produces 2 million automobiles of which it sell 1.5 million, is that depreciation in mass or rate significantly different than if it sold all 2 million? Of course not.

And if Ford only produces and sells 1 million, when its fixed assets can support production of 2 million, then it takes longer to recover the capital embodied in the fixed assets– and moreover, if new more efficient machinery is introduced into production by GM, or Toyota, then, while the depreciation of the Ford fixed assets will be accelerated, its ability to circulate the value embedded in those old assets, to recover the depreciation amount will deteriorate, slow down, and the fixed assets will face devaluation– Ford goes into its very own recession.

““The value of raw material, therefore, forms an ever-growing component of the value of the commodity-product in proportion to the development of the productivity of labour, not only because it passes wholly into this latter value, but also because in every aliquot part of the aggregate product the portion representing depreciation of machinery and the portion formed by the newly added labour — both continually decrease. Owing to this falling tendency, the other portion of the value representing raw material increases proportionally, unless this increase is counterbalanced by a proportionate decrease in the value of the raw material arising from the growing productivity of the labour employed in its own production.”

Yes, Marx says that, but he does not say that fixed capital forms an ever decreasing portion of the production process. On the contrary, the very notion of the accumulation of capital means, explicitly for Marx, the accumulation of the means of production as capital– the expulsion, displacement of living labor, by accumulated labor as embodied in the machinery of production, of which fixed capital is, in Marx’s words “the most perfect form” of capital. Marx does say that the value of fixed capital is required in its entirety for the production, but is only recaptured incrementally by the valorization process.

Precisely because the value of fixed capital accumulates “disproportionately” to the value of labor power engaged in production, less new value makes up the value of the circulating capital; precisely because the value of fixed capital accumulates more massively and more efficiently, it gives up less and less of its accumulated value to any individual commodity, to all commodities, in each production period, in all production periods, AND the turnover of the ENTIRE capital slows down. The turnover for the capital necessary to the production process cannot be realized quickly enough in the valorization process. Capital confronts the limitation that is immanent to itself; that IS itself.

The figure of 52 was for both the production time and circulation time. As I wrote in that further blog post,

” In short, on average the capital advanced for car production can turn over on average around 52 times a year, although the Internet is changing this too, as it means increasingly, consumers will be able to order their cars directly from producers, and have them delivered directly to their home. But, even assuming the average turnover period for such industrial capital, is a week, this compares badly with the situation for these new forms of capital.”

You also say,

“So clearly, from your perspective, the car companies only pay for parts when they are delivered. In turn 6 days later they are paid for the completed cars which are collected from the end of the production line by dealers who buy them C.O.D.”

But, the advanced capital has nothing to do with the payment for the elements of that capital as far as the turnover time is concerned. What is measured is the actual capital value, when it is thrown into circulation, and when that capital value returns. Otherwise, as indicated you arrive at ludicrous conclusions.

For example, suppose a firm employ 10 workers who are paid £70 per week in wages, in arrears. The workers produce ice cream each day, which they then sell. If we ignore the constant capital value, and assume a rate of surplus value of 100%, each day £10 of variable capital produces £20 of new value. But, what actually is the rate of surplus value if we take your assumption that the start of the period of turnover is the point that the capitalist actually pays for this labour-power, i.e. pays wages?

At the end of day 1, the capitalist receives £20, but how much capital have they laid out at this point? On your basis 0, and so the rate of surplus value/profit would be infinity! That is why Marx calculates the rate of turnover not on the basis of when the capital is actually paid for – materials obtained from a supplier on the basis of commercial credit would be in the same position – but from the point that the actual capital value is itself advanced to production.

Just in Time production and stock control systems, as I have set out, facilitate this, because the circulating capital, which, as Marx and Engels set out is what the turnover time is based upon, is reduced to a minimum of what is required to be advanced to production at any one time. It is only the circulating capital that is relevant for the turnover time, as marx and Engels set out, because it is only this circulating capital that has to be continually reproduced. The fixed capital value is advanced to production, but as fixed capital does not have to be continually reproduced, only its wear and tear is continually reproduced in the value of the output. That is why the fixed capital value in total is included and relevant to the calculation of the annual rate of profit, but not the rate of profit/profit margin, where only the wear and tear is relevant.

I don’t think the figure for inventories is relevant. It looks at things back to front. Let me give an example. In the 1970’s, I worked in the marketing department of a large ceramic company. From the time a large retailer placed an order, to the time they received the goods, might be say six weeks. But, did this mean that the turnover time for the capital consumed in the production of those goods was six weeks? Absolutely not. The reason it took six weeks was simply down to the fact that the company was working on orders for other companies during most of that time.

In fact, depending on what the order was for, they might get it quicker or slower than that, depending on what was already in stock,

what was work in progress, and what production runs were taking place. The fact was that every single day, clay was coming in one door, being processed, and pushed out of the door at the other end. The main restriction on the turnover time was the physical time required for firing in the kiln. Apart from that, the production process was on such a scale that the working period was in no sense really restricted by the need to produce some minimum quantity prior to shipping.

As I’ve written in another of those blog posts about car production and turnover time, you can now order your car directly online with the car producer, specify the particular requirements you have for it, and watch its progress up to where its delivered to your door. The time it takes to get to you has nothing to do with the turnover time of capital, again because the main factor here is how many other people’s cars the company is in the process of producing before it gets to yours!

The circuit of capital is M.C…P…C*.M*. In other words what concerns Marx is the two sales that constitute the circuit of capital, the first, the purchase which opens it and the second, the sales, which concludes it. Money goes out and new money comes in containing the surplus. You like quoting from Book 3. Engels in editing Marx describes the elements of working capital. Included is credit given and credit taken as well as inventory. The issue of credit deals with your working experience. The BEA is also aware of the confounding effect of credit on sales or more precisely when to document the sale. Fortunately because we are talking about aggregated sales mounting to tens of millions in each quarter for each industry, there is an averaging out of credit given and taken. So the formula remains accurate. Inventory is decisive regardless of what you say. The only time working capital can fall below inventory turnover is when credit is received from suppliers but no credit is given because the goods are sold for cash. That only happens in retail and the turnover formula reveals correctly the turnover of capital is faster than the turnover of inventory. So no surprise there. Your issue of ordering a car on the internet is instructive. If it is fully paid for by the time it is produced, working capital in this case would be zero. A better example would be private education which can be paid at the beginning of term.

You say,

“The circuit of capital is M.C…P…C*.M*. In other words what concerns Marx is the two sales that constitute the circuit of capital, the first, the purchase which opens it and the second, the sales, which concludes it. Money goes out and new money comes in containing the surplus.”

No it isn’t, as Marx sets out in Capital II. The circuit M.C…P…C*.M*, as Marx makes clear is only the circuit of newly invested money-capital. As he also makes clear that is also the case with the newly invested realised profit.

“… it is the form of capital that is newly invested, either as capital recently accumulated in the form of money, or as some old capital which is entirely transformed into money for the purpose of transfer from one branch of industry to another.” (p 61)

But, as he sets out in Capital, and what is central to the analysis of the rate of turnover of capital, is that for all existing capital, the circuit is P.. C’ – M’. M – C … P. The extended form of that is P … C’ (C = c) – M’ (M + m). – M – C… P. Only in the case of the accumulated m is the circuit M – C…P…C’ – M.

“The circuit of productive capital has the general formula P … C’ — M’ — C … P. It signifies the periodical renewal of the functioning of productive capital, hence its reproduction, or its process of production as a process of reproduction aiming at the self-expansion of value; not only production but a periodical reproduction of surplus-value; the function of industrial capital in its productive form, and this function performed not once but periodically repeated, so that the renewal is determined by the starting-point.” (p 65)

The same is true for commercial capital. Its circuit is C’ – C’.

“Consequently if simple reproduction takes place in this form, the C’ at the terminal point is equal in size to the C’ at the starting-point. If a part of the surplus-value enters into the capital circuit, C”, an enlarged C’, appears at the close instead of C’. This is merely a larger C’ than that of the preceding circuit, with a larger accumulated capital-value. Hence it begins its new circuit with a relatively larger, newly created surplus-value. In any event C’ always inaugurates the circuit as a commodity-capital which is equal to capital-value plus surplus-value.” (p 90)

The reason is that what is turned over is the actual productive-capital.“ The money representation (M) is simply that a money equivalent of the capital value, expressed in money, Marx says purely as unit of account, as the only rational way of performing the calculation. What must be replaced is not some amount of money – which is what the proponents of historical pricing suggest – but the physical elements of the productive-capital, and thereby their current capital value. (M) here merely signifies that the current money equivalent of that capital value. As Marx sets out in Capital III.

“This entire portion of constant capital consumed in production must be replaced in kind. Assuming all other circumstances, particularly the productive power of labour, to remain unchanged, this portion requires the same amount of labour for its replacement as before, i.e., it must be replaced by an equivalent value. If not, then reproduction itself cannot take place on the former scale.” (p 835)

In other words, for all existing capital the turnover starts from the productive capital (labour and means of production) in the hands of the capitalist. It is advanced to production, and at the end of the production period, it results in commodities part of which represent the value of the productive-capital used in their production, and the other part representing the surplus product. This starts the circulation period of the capital. It is metamorphosed into Money-Capital, one part representing the money equivalent of the consumed productive capital, the other representing surplus value.

The money capital (M) is then metamorphosed once more into the commodities that represent the productive-capital previously consumed in production, and these now once more engage in production, the turnover of the capital then being completed.

“In so far as reproduction obtains on the same scale, every consumed element of constant capital must be replaced in kind by a new specimen of the same kind, if not in quantity and form, then at least in effectiveness.” (Chapter 49, p 849)

“In the reproduction process of capital, the money-form is but transient – a mere point of transit.” (Capital II)

It is not at all the start and finish point of the circuit.

In 2016 US companies hoarded an estimated $2.5 trillion in profits abroad, a total growing by around $250bn a year.

http://www.cnbc.com/2016/09/20/us-companies-are-hoarding-2-and-a-half-trillion-dollars-in-cash-overseas.html

This materially effects estimates of the rate of profit, as this massive amount of money is not included in the BEAs total for the mass of profit. As profits are around $2 trillion a year, this lowers the total of profit, not by the revenue of the hoard, but by the amount of the hoard not repatriated, i.e. by around 12%.

The BEAs estimates of the fixed capital stock are based on a method developed by Bohm-Bawerk (as they acknowledge). This values the fixed capital stock as a discounted total of its future revenues, so as profits rise so does the estimated value of the fixed capital stock, so the rate of profit does not change. (This is the tautology criticised in the Cambridge Capital Controversy). Capitalists owe their social power to their monopoly of the means of production which means that they can extract a surplus value from the working class, but the rate of profit is not estimated on this but on the actual amount of capital advanced. But under the BEAs chained measures the “value” of the fixed capital stock can even rise above the purchase price as it varies with the change of revenues.

There are different turnovers of capital, but the key one of for the rate of profit, is the turnover of variable capital as after the first turnover the capitalists do not have to advance the capital for wages. Therefore, to use the mass of variable capital overstates the amount that capitalists advance in wages by a factor of between 5 to 8.

BEA table 5.3.5 Private fixed investments by type line 16 intellectual property products divided by non-resident private fixed investments line 2 rises from 1947 7.8% to 1990 22.2% to 2000 27.4% to 2016 32.8%.

Profits from non-domestic operations must be reported. They are exempt from tax if the reporting party declares them “indefinitely invested abroad.” BEA includes profit from non-domestic sources, operations in its calculations of corporate profits, and for example, in 1Q of 2017, those profits from non-domestic sources increased, while profits from domestic operations declined.

“There are different turnovers of capital, but the key one of for the rate of profit, is the turnover of variable capital as after the first turnover the capitalists do not have to advance the capital for wages. Therefore, to use the mass of variable capital overstates the amount that capitalists advance in wages by a factor of between 5 to 8.”

Of course, we could say that not only of the variable capital, but also the constant capital as the successful completion of the circuit recaptures all the capital advanced, but not all the capital invested. So what Bill is telling is not that big revelation. Yes, the wage is recuperated in the circuit, and then that recuperation of the advanced wage is then used to pay subsequent wages. Same for the cost of electricity, and iron ore, so so what? As long as that “accounting” is constant and consistent, we can measure the trend and observe the immanent tendencies of capitalism as they become manifest in the increased or decreased masses of profit, increased or decreased rates of profit, increased or decreased accumulation of fixed assets, increased or decreased rates of capital expenditures.

Re depreciaton. I would recommend everyone take a look at the tables produced by the US Department of Commerce in its Quarterly Financial Report of Mining Manufacturing and Service Industries. Check out table 1.1 which gives the figures for property and equipment, and for accumulated depreciation, depletion and amortization. You can access data back to 1996. I think you’ll find that 1996-2000, accumulated depreciation actually declines as portion of total property and equipment from 53% to 51%. .

For 2003 to 2016 the ratios are pretty consistent, varying between 55% and 57%. Now these may not be precise measures, but again it’s the TREND that matters, and the consistency in the ratio would indicate that the growing level of software, intellectual property, etc. investment and capitalization is not dramatically altering depreciation, particularly since capital spending between 2009 and 2016 has been constrained.

The BEA measures corporate profits from tax return data, at least after initial estimates. For non-domestic profits – if not repatriated to avoid paying US tax – they have to use company reported financial data. This will be subject to accounting rules, but the ‘flexibility’ of them is even greater than under tax rules.

BEA measures corporate profits from BOTH tax return data and corporate financial statements. Profits earned overseas are NOT exempt from being reported to the IRS. They are exempt from taxis, but not the reporting requirement, as long as they are “indefinitely invested abroad.”

Mere technicality, I’m sure.

https://www.forbes.com/sites/danielfisher/2012/10/25/foreign-tax-reserves-are-crack-cocaine-for-earnings-manipulation-study-says/#4877da4641c0

“The Internal Revenue Service code allows companies to shield foreign earnings from U.S. corporate taxes as long as they don’t repatriate them as dividends to the parent. Accounting rules allow companies to avoid reporting a tax liability for these earnings if they plan to leave them overseas indefinitely. Those earnings, called Permanently Reinvested Earnings, or PRE, need only be identified in a footnote on financial statements with the Securities and Exchange Commission. Last year PRE amounted to $1.5 trillion, up 42% from 2009.”

Click to access i1120sm3.pdf

Bit more than a footnote is required. IRS Schedule M3 is supposed to capture the information.

“Capitalists owe their social power to their monopoly of the means of production which means that they can extract a surplus value from the working class, but the rate of profit is not estimated on this but on the actual amount of capital advanced.”

But, as Marx and Engels indicate in Capital III, even by the end of the 19th century, the majority of capital was not private capital, but socialised capital, mainly in the form of Joint Stock Companies, but also in the form of co-operatives – in the UK, the Co-op was the biggest retailer, for example, and was expanding into other areas, becoming the biggest farmer, and so on. Private capitalists, as Engels says in his critique of the Erfurt Programme, and Kautsky extends this in “The Road To Power”, were not the OWNERS of the bulk of means of production, therefore. Private ownership of means of production/capital, by then existed only for the small capitals, which as Marx says, increasingly themselves came into conflict with this large scale socialised capital.

Instead, as Engels sets out in his Supplement to Capital III, the majority of private capital took the form not of means of production/industrial capital, but of fictitious capital – shares, bonds, property, from which they drew interest and rents, and obtained capital gains from speculation. The control that these capitalists exerted came from their continued political power, exerted through parliament and the state, arising from their enormous paper wealth, which allowed them to continue to exercise control over capital they did not own.

For example, their is no more reason that shareholders should be entitled to appoint Boards of Directors and executives to look after their interests and determine company policy than bondholders, or a bank that makes a loan to a company, or an equipment company that loans equipment to a company. All are merely owners of loanable money-capital, which is loaned to the company, and in return for which they are paid interest. In Germany, that right of shareholders is partially restricted by the co-determination laws that enable workers to elect half the members of company supervisory boards, though for the reasons Trotsky described, such arrangements always continue to allow the shareholders to exert majority control.

There is no economic or juridical basis for shareholders exercising control over capital they do not own. As lenders of money-capital to a company they do not own its productive-capital, they only own shares, which are nothing more than paper certificates saying they have loaned that money, and on which they are entitled to the market rate of interest. They exercise control only as Kautsky says, as a consequence of political power. The real capital itself as socialised capital belongs to the company itself as a legal and economic corporate entity in its own right, and as Marx sets out in Capital III, it can only be considered to be the property of the associated producers within that particular firm. It is they not shareholders that should appoint boards, and so on, and exercise control over the capital.

If they did so, then we would not have had the situation seen over the last thirty years or so described by Andy Haldane of the Bank of England, where dividends as a share of realised profit have risen from around 10% to around 70%. Many of those dividends have gone to once more bid up the prices of existing bonds and shares, which leads to a further inflation of asset prices, which squeezes yields, but which in turn induces those same representatives of shareholders to vote through increased levels of dividends.

“There are different turnovers of capital, but the key one of for the rate of profit, is the turnover of variable capital as after the first turnover the capitalists do not have to advance the capital for wages. Therefore, to use the mass of variable capital overstates the amount that capitalists advance in wages by a factor of between 5 to 8.”

The rate of turnover that Marx and Engels describe is the rate of turnover of the circulating capital, circulating constant capital (materials) and variable capital. In effect as Marx and Engels describe, the two are essentially identical, because the materials advanced to production are processed by labour advanced to production, and once combined into a product, they necessarily proceed to be realised as money-capital at the same time. The only difference as Marx sets out in Capital II, and in Theories of Surplus Value Chapter 17, is any difference their might be in metamorphosing the realised money-capital back into labour-power or materials.

Indeed, as he sets out in those discussions this is one cause of crises. The major instance referred to, is that given in Capital III, whereby realised money-capital could not be metamorphosed into replacement materials, because the US Civil War stopped the supply of cotton to lancashire textile factories.

It is only the circulating constant capital that is relevant to the rate of turnover, and not fixed capital, for the reason marx and Engels set out, which is that it is only the circulating capital that has to be constantly reproduced, in order for production to continue on the same scale, i.e. the consumed materials and labour-power have to be physically replaced, which can only happen when their value has been reproduced in the end product, and metamorphosed into money-capital. That is not the case with fixed capital, and in fact, as Marx sets out, the longer its turnover time the better, because it only has to be physically replaced when it is worn out, (unless it is morally depreciated to zero, by some new technology), whilst its value is continually being reproduced and returned to be hoarded in the form of the value transferred to the end product via wear and tear.

In fact, as Marx says, for some very large elements of fixed capital such as canals, the major element is not the accrual of this value in respect of wear and tear, because the capital itself can be thought of as more or less of unlimited life, but is the amount regularly expended for repairs. And as Marx says, the nature of this fixed capital is that at each stage is it gets larger and more technologically sophisticated, not only does it tend to have longer duration, but its cost relative to the output it produces continually falls. Larger more sophisticated machines are not proportionally more expensive than their less productive predecessors, for example. The huge container ships, or oil tankers, for example that now transport the worlds goods around the globe do not cost proportionally more than smaller ships that carry less cargo, and which are slower, thereby carrying less cargo in weight/miles per year. The Internet enables communications at a much faster pace than earlier forms of communication, but its cost is only a fraction of the cost of the previous forms of fixed capital that themselves were only capable of undertaking a fraction of the communication that the Internet now facilitates in a year.

“Therefore, to use the mass of variable capital overstates the amount that capitalists advance in wages by a factor of between 5 to 8.”

Its not what is advanced as wages that is the relevant metric, for the reasons that Marx sets out, or the periodicity of wage payments, for the reasons I set out above. Wages are always paid in arrears, so it is always a case of workers advancing labour to the capitalist, not of the capitalist advancing wages to the worker. The worker has always created the value in advance that is reproduced in the end product, whose value is realised by capital, an then returned to the worker in the form of wages. If the payment of wages, or the periodicity of wages were the determinant then the rate of turnover would be infinity.

The turnover period is rather as marx sets out from the point at which the actual capital itself is advanced to production, i.e. the point when the labour-power is hired, and starts producing. The close of that turnover period comes when that labour-power has produced the required amount of commodities that constitute the minimum for the working period, when those commodities are then put into circulation, sold, and finally the realised money-capital been used to hire and set to work the consumed labour-power.

If we take a worker in a fast food restaurant. The labour is advanced as soon as the worker takes the customer order, the burger is produced, and handed to the customer, and the turnover period ends as soon as the customer has paid for it. All in all, the turnover of this capital, on average amounts to only a matter of minutes. By contrast, a worker in shipbuilding advances labour over a period of maybe two years, before the ship is completed, and sold, before the firm realises the value of the ship, and is able to use it to once more reproduce its circulating capital.

That is why, as Marx sets out in discussing the average rate of profit and prices of production, those capitals that have a longer than average turnover period, have lower annual rates of profit, whilst those with shorter than average turnover times have higher annual rates of profit, and this results in the price of production of the former being higher than the exchange value, whilst the latter’s price of production is lower than its exchange value (discounting the effect of the different organic compositions in both cases). It is why those capitals with longer turnover times have higher rates of profit/profit margins, and those with shorter turnover times have lower rates of profit/profit margins.

But, in fact, the average rate of turnover is much greater than 8. In Capital III, Engels gives a practical example of the turnover time of capital in the mid 1800’s. And he shows that the rate of turnover then was already around 8.5.

“The weekly advance of circulating capital therefore was 358c + 52v = 410. In terms of per cent this was 87.3c + 12.7v. For the entire circulating capital of £2,500 this would be £2,182 constant and £318 variable capital. Since the total expenditure for wages in one year was 52 times £52, or £2,704, it follows that in a year the variable capital of £318 was turned over almost exactly 8½ times. The rate of surplus-value was 80/52 = 153 11/13. We calculate the rate of profit on the basis of these elements by inserting the above values in the formula p’ = s’n (v/C) : s’ = 153 11/13, n = 8½, v = 318, C = 12,500; hence:

p’ = 153 11/13 × 8½ × 318/12,500 = 33.27%.” (Chapter 4)

And, as Engels says the major influence on the rate of turnover is the rise in social productivity, which not only reduces the production time, but also the circulation time. As Engels says,

“The chief means of reducing the time of production is higher labour productivity, which is commonly called industrial progress. If this does not involve a simultaneous considerable increase in the outlay of total capital resulting from the installation of expensive machinery, etc., and thus a reduction of the rate of profit, which is calculated on the total capital, this rate must rise. And this is decidedly true in the case of many of the latest improvements in metallurgy and in the chemical industry. The recently discovered methods of producing iron and steel, such as the processes of Bessemer, Siemens, Gilchrist-Thomas, etc., cut to a minimum at relatively small costs the formerly arduous processes. The making of alizarin, a red dye-stuff extracted from coal-tar, requires but a few weeks, and this by means of already existing coal-tar dye-producing installations, to yield the same results which formerly required years. It took a year for the madder to mature, and it was customary to let the roots grow a few years more before they were processed.

The chief means of reducing the time of circulation is improved communications. The last fifty years have brought about a revolution in this field, comparable only with the industrial revolution of the latter half of the 18th century. On land the macadamised road has been displaced by the railway, on sea the slow and irregular sailing vessel has been pushed into the background by the rapid and dependable steamboat line, and the entire globe is being girdled by telegraph wires. The Suez Canal has fully opened East Asia and Australia to steamer traffic. The time of circulation of a shipment of commodities to East Asia, at least twelve months in 1847 (cf. Buch II, S. 235 [English edition: Karl Marx, Capital, Vol. II, pp. 251-52. — Ed.]), has now been reduced to almost as many weeks. The two large centres of the crises of 1825-57, America and India, have been brought from 70 to 90 per cent nearer to the European industrial countries by this revolution in transport, and have thereby lost a good deal of their explosive nature. The period of turnover of the total world commerce has been reduced to the same extent, and the efficacy of the capital involved in it has been more than doubled or trebled. It goes without saying that this has not been without effect on the rate of profit.”

On the basis of the rapid growth in productivity since the time Engels was publishing Capital III, I think that a conservative estimate of the rate of turnover today is around 60, which, as Engels says, has a correspondingly marked effect on increasing the general annual rate of profit, whilst tending to reduce profit margins/rate of profit.

In relation to the fixed capital, and the wear and tear transferred to the value of the end product, as opposed to the depreciation of fixed capital, I should have made the other obvious caveats, and clarifications. As Marx points out depreciation is not the same thing as wear and tear. This is a distinction between Marx’s analysis and bourgeois accounting practices, which are geared to enabling capitalists to get back their costs via the tax system.