In the last few years, Robert J. Gordon, a professor of economics at Northwestern University, has persistently argued against the trendy view of the moment that robots, AI and other ‘disruptive technologies’ are about to launch the global economy into a productivity boost never seen before. I have commented before on Gordon’s series of papers developing this proposition.

And very recently, Gordon presented his arguments yet again at ASSA 2016 when he critiqued a paper by David Kotz and Deepankur Basu at an URPE session.

As Gordon says succinctly in that critique: “The evidence accumulates every quarter to support my view that the most important contributions to productivity of the digital revolution are in the past, not in the future. The reason that business firms are spending their money on share buy-backs instead of plant and equipment investment is that the current wave of innovation is not producing novelty sufficiently important to earn the required rate of return.”

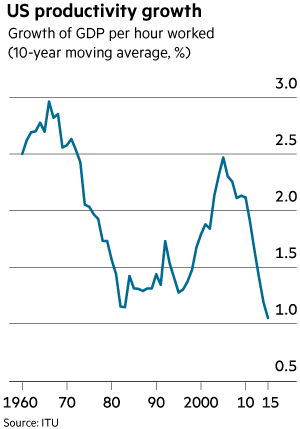

The arrival of the internet and mobile phones has failed to generate a sustained upturn in the growth of productivity. Output per hour worked in the US grew at rate of 3 per cent a year in the 10 years up to 1966, after which the growth rate declined, falling to just 1.2 per cent in the 10 years to the early 1980s. After the launch of the worldwide web, the moving average rose to 2.5 per cent in the 10 years to 2005. But it then fell to just 1 per cent in the decade to 2015. A decomposition of the sources of growth in productive capacity underlines the point. Over the 10 years up to and including 2015, the average growth of “total factor productivity” in the US — a measure of innovation — was only 0.3 per cent a year. Productivity recently has been growing well below the 2.1 percent average gains seen over the past 67 years.

So, according to Gordon, the great new innovatory productivity enhancing paradigm that is supposedly coming from the digital revolution is actually over already and the future robot/AI explosion will not change that. On the contrary, far from faster economic growth and productivity, the world capitalist economy is slowing down as a product of slower population growth and productivity.

Now Gordon has compiled all his ideas and retorts to those who have disagreed into a new book, The Rise and Fall of American Growth. “This book,” Gordon writes in the introduction, “ends by doubting that the standard of living of today’s youths will double that of their parents, unlike the standard of living of each previous generation of Americans back to the late 19th century.” Gordon predicts that innovation will trundle along at the same pace of the last 40 years. Despite the burst of progress of the Internet era from the 1990s, total factor productivity — which captures innovation’s contribution to growth — rose over that period at about one-third the pace of the previous five decades.

Gordon reckons that the American workforce will continue to decline, as aging baby boomers leave the work force and women’s labour supply plateaus. And gains in education, an important driver of productivity that expanded sharply in the 20th century, will contribute little. Moreover, the growing concentration of income means that whatever the growth rate, most of the population will barely share in its fruits. Altogether, Professor Gordon argues, the disposable income of the bottom 99% of the US population, which has expanded about 2% per year since the late 19th century, will expand over the next few decades at a rate little above zero.

Gordon’s argument about productivity growth in the recent past has been confirmed by the evidence, as John Fernald at the San Francisco Fed has shown. And Fernald has argued elsewhere “Growth in educational attainment, developed-economy R&D intensity and population are all likely to be slower in the future than in the past.”

Even Ben Bernanke, the former chairman of the US Federal Reserve, who is now at the Brookings Institution, has sympathy with Professor Gordon’s proposition. “People who invest money in the markets are saying the rate of return on capital investments is lower than it was 15 or 30 years ago,” Mr. Bernanke said. “Gordon’s forecast is not without some market reality.” Other strands of data point in this direction. Business dynamism, measured by the role of new companies in the economy, appears to be waning. The share of employment in companies less than five years old dropped from about 19 percent in 1982 to 11 percent in 2011.

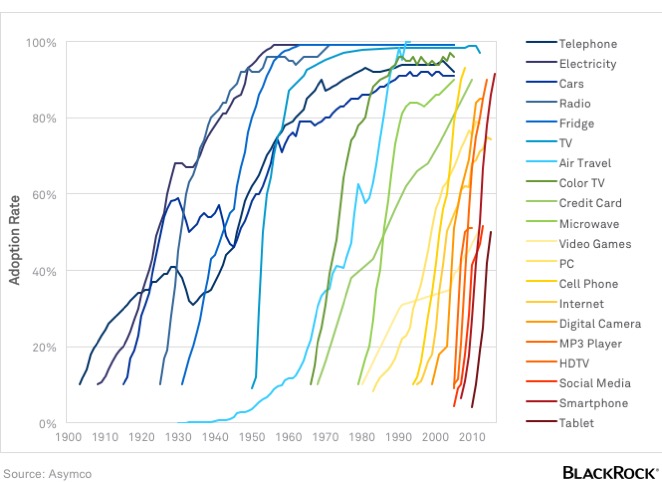

It’s a grim picture that Gordon paints for the future of US capitalism and thus the world. But is it right? The argument against it is that people are adopting new technologies, including tablets and smartphones at the swiftest pace we’ve seen since the advent of the television. While television arguably detracted from US productivity, today’s advances in technology are generally geared toward greater efficiency at lower costs and so will boost the productivity growth of labour (see Blackrock’s diagram below of the adoption rate of current new technologies).

Some argue, against Gordon, that statisticians are failing to measure output correctly, partly by failing to capture free services, such as search, which generate vast unmeasured surplus value. But as Martin Wolf of the FT pointed out recently “it is not at all clear why statisticians should have suddenly lost their ability to measure the impact of new technologies in the early 2000s. Again, most (past) new technologies have also generated vast unmeasured surplus value. Think of the impact of electric light on the ability to study.”

Nevertheless, balanced against Gordon are a myriad of techno-optimists and economists who reckon that the world is on the brink of a productivity explosion driven by robots, artificial intelligence, genetics, and a range of new ‘disruptive technologies’ – disruptive in the sense that traditional jobs and functions are going to disappear and be replaced by robots and algorithms. The optimists argue that, since the time of Thomas Malthus, eras of depressed expectations like our own have inspired predictions of doom and gloom that were proved wrong when economies turned up a few years down the road.

Gordon’s main opposition comes from Professor Joel Mokyr who works with Gordon at Northwestern University. . What Professor Gordon fails to account for, Professor Mokyr argues, is that the information technology revolution and other recent developments have produced mind-blowing tools and techniques, from gene-sequencing machines to computers that analyze mountains of data at blistering speed. This is creating vast new opportunities for innovation, from health care to materials technology and beyond. “The tools available to science have been improving at a dazzling rate,……I’m not sure how, but the world of technology in 30 to 40 years’ time will be vastly different than it is today.”

Every day there is a new story in the media about how people and their skills are or will soon be replaced by machines and computer software that learns for itself. At this year’s World Economic Forum, the annual meeting of the global elite of bankers, politicians, corporate chiefs and military, in Davos Switzerland, the main theme was the ‘Fourth Industrial Revolution’. Advances in robotics and artificial intelligence would have the transformative effect that steam power, electricity and ubiquitous computing achieved in previous centuries.

At Davos, the elite were told by Sebastian Thrun, the inventor of Google’s self-driving cars and an honorary professor at Delft University of Technology, that “almost every established industry is not moving fast enough” to adapt their businesses to this change. He suggested self-driving cars would make millions of taxi drivers redundant and planes running solely on autopilot would remove the need for thousands of human pilots. However, don’t worry, as Thrun was optimistic that redundant roles will quickly be replaced. “With the advent of new technologies, we’ve always created new jobs,” he said.

As one of the most prominent observers of the new ‘industrial revolution, Erik Brynjolfsson, the Massachusetts Institute of Technology professor and co-author of “The Second Machine Age”, put it “We’re moving to a world where there will be vastly more wealth and vastly less work.” But he went on “I think the biggest immediate change will be a move away from … one person [staying] in one profession or one job during their lifetime… That shouldn’t be a bad thing, and shame on us if we turn it into a bad thing.”

Such optimism contrasted with the WEF’s own book launched at Davos, that reckoned increased automation and AI in the workforce will lead to the loss of 7.1m jobs over the next five years in 15 leading economies, while helping create just 2m new jobs over the same period. In the financial sector, a thinking, learning and trading computer may well make even today’s superfast, ultra-complex investment algorithms look archaic — and possibly render human fund managers redundant. You might say we don’t’ care too much about losing hedge fund managers. But AI and robots will destroy the jobs of millions in productive sectors and on much less money. This is the prospect for labour in a robot-led capitalism.

It’s not just the loss of jobs for millions that is the prospect from AI/robots, but some argued that AI threatens to existence of humanity itself. Ray Kurzweil, the American inventor and futurist, has predicted that by 2045 the development of computing technologies will reach a point at which AI outstrips the ability of humans to comprehend and control it. Stephen Hawking has argued that “the development of full artificial intelligence could spell the end of the human race”. And Elon Musk, the founder of SpaceX and Tesla Motors, believes that artificial intelligence is “potentially more dangerous than nukes”. The “biggest existential threat” to humanity, he thinks, is a Terminator-like super machine intelligence that will one day dominate humanity.

Moreover, while computers are quicker, smarter and shorn of human behavioural biases, they come with their own weaknesses. Disaster can strike quickly. For example, Knight Capital, a high-frequency trading firm, imploded in 2012 when its computers ran amok, in practice losing $10m a minute in a devastating 45-minute trading blitz. As Gavekal, an investment brokerage, acerbically noted at the time: “Sometimes all computers do is replace human stupidity with machine stupidity. And, thanks to speed and preprogrammed conviction, machine stupidity can devour markets far faster than any human panic can achieve.” Algos based on artificial intelligence techniques may be the next generation of quantitative finance, but even industry insiders say they can unravel when confronted with the chaotic reality of markets. “This stuff in the hands of the wrong people can be very dangerous,” says Tom Doris, the head of Otas Technologies. For example, self-driving cars suffered twice as many accidents as human-driven ones in 2013, according to a University of Michigan study. Most of them were minor scrapes, and the human drivers were at fault in every case, but this is a vivid illustration of how accidents can happen when man meets machine — whether on the road or in markets.

But can robots really replace humans within 30 years? Many doubt it. Scenarios such as Kurzweil’s are extrapolations from Moore’s law, according to which the number of transistors in computers doubles every two years, delivering greater and greater computational power at ever-lower cost. But Gordon Moore, after whom Moore’s law is named, has himself acknowledged that his generalisation is becoming unreliable because there is a physical limit to how many transistors you can squeeze into an integrated circuit. In any case, Moore’s law is a measure of computational power, not intelligence. A vacuum-cleaning robot, a Roomba, will clean the floor quickly and cheaply and increasingly well, but it will never book a holiday for itself with my credit card.

Luciano Floridi at the University of Oxford agrees that machines can do amazing things, often better than humans. For instance, IBM’s Deep Blue computer played and beat the Grand Master Garry Kasparov at chess in 1997. In 2011, another IBM machine, Watson, won an episode of the TV quiz show Jeopardy, beating two human players, one of whom had enjoyed a 74-show winning streak. But Deep Blue and Watson are versions of the “Turing machine”, a mathematical model devised by Alan Turing which sets the limits of what a computer can do. A Turing machine has no understanding, no consciousness, no intuitions — in short, nothing we would recognise as a mental life. It lacks the intelligence even of a mouse.

Floridi explains that in 1950 Turing proposed the following test. Imagine a human judge who asks written questions to two interlocutors in another room. One is a human being, the other a machine. If, for 70 per cent of the time, the judge is unable to tell the difference between the machine’s output and the human’s, then the machine can be said to have passed the test. Turing thought that computers would have passed the test by the year 2000. He was wrong. Eric Schmidt, the former chief executive of Google, believes that the Turing test will be passed by 2018.. So far there has been no progress. Computer programs still try to fool judges by using tricks developed in the 1960s. For example, in the 2015 edition of the Loebner Prize, an annual Turing test competition, a judge asked: “The car could not fit in the parking space because it was too small. What was too small?” The software that won that year’s consolation prize answered: “I’m not a walking encyclopaedia, you know.”

Where do I stand on this debate: are we entering a new industrial revolution like the early 19th century that will give capitalism a new lease of life in developing the productive forces, even if it means loss of jobs for hundreds of millions and rising inequality of income and wealth? Or are the new ‘disruptive technologies’ just a mirage that will change little in increasing economic growth and productivity, as Gordon argues? I think it is both, depending on the time and the cyclical eruptions that is the capitalist mode of production.

I have great sympathy with the Gordon’s view, but with reservations on timing. I’m not so sure that emerging capitalism cannot provide a new period of capitalist development, if the end of this long depression does not lead to the replacement of the capitalist mode of production by political action from energised working class movements. Also, it is by no means certain that mature capitalism cannot still develop and exploit new technologies, even if it has failed so far, in areas like robotics, artificial intelligence, 3d printing and nanotechnology. Indeed, some argue that US technology in developing shale oil and gas will shift the balance of economic power in energy back towards North America and the mature capitalist economies and away from the Middle East and Asia.

In the third section of Gordon’s book, he looks at why productivity growth did soar at one particularly notable juncture in the 1930s. Gordon reckons that the Great Depression was a period of innovation that “directly contributed to the great leap” in the 1940s. Gordon also points to the “high-pressure learning-by-doing that occurred during the high-pressure economy of World War II.” World War II gave America its first jet aircraft (the Bell P-59), mass-produced penicillin and nuclear power. Perhaps even more important, factories like Henry Kaiser’s shipyards taught managers and workers how to radically speed production. Something similar could happen when this Long Depression ends, as it will.

Also, capitalism could get a further kick forward from exploiting the hundreds of millions coming into the labour forces of Asia, South America and the Middle East. This would be a classic way of compensating for the falling rate of profit in the mature capitalist economies. While the industrial workforce in the mature capitalist economies has shrunk to under 150m, as unproductive labour has risen sharply; in the so-called emerging economies the industrial workforce now stands at 500m, having surpassed the industrial work force in the imperialist countries by the early 1980s. In addition, there is a large reserve army of labour composed of unemployed, underemployed or inactive adults of another 2.3bn people globally that could also be exploited for new value.

So there may be life in capitalism globally yet even if it is in ‘down mode’ right now. Or maybe this potential labour force will not be ‘properly exploited’ by the capitalist mode of production and Gordon is right. The world rate of profit (not just the rate of profit in the mature G7 economies) stopped rising in the late 1990s and has not recovered to the level of the golden age for capitalism in the 1960s, despite the massive potential global labour force. It seems that the countervailing factors of foreign investment in the emerging world, combined with new technology, have not been sufficient to push up the world rate of profit in the last decade or so, so far. The downward phase of the global capitalist cycle is still in play.

Reblogged this on Reconstruction communiste Comité Québec and commented:

I have great sympathy with the Gordon’s view, but with reservations on timing. I’m not so sure that emerging capitalism cannot provide a new period of capitalist development, if the end of this long depression does not lead to the replacement of the capitalist mode of production by political action from energised working class movements. Also, it is by no means certain that mature capitalism cannot still develop and exploit new technologies, even if it has failed so far, in areas like robotics, artificial intelligence, 3d printing and nanotechnology. Indeed, some argue that US technology in developing shale oil and gas will shift the balance of economic power in energy back towards North America and the mature capitalist economies and away from the Middle East and Asia.

In the third section of Gordon’s book, he looks at why productivity growth did soar at one particularly notable juncture in the 1930s. Gordon reckons that the Great Depression was a period of innovation that “directly contributed to the great leap” in the 1940s. Gordon also points to the “high-pressure learning-by-doing that occurred during the high-pressure economy of World War II.” World War II gave America its first jet aircraft (the Bell P-59), mass-produced penicillin and nuclear power. Perhaps even more important, factories like Henry Kaiser’s shipyards taught managers and workers how to radically speed production. Something similar could happen when this Long Depression ends, as it will.

Also, capitalism could get a further kick forward from exploiting the hundreds of millions coming into the labour forces of Asia, South America and the Middle East. This would be a classic way of compensating for the falling rate of profit in the mature capitalist economies. While the industrial workforce in the mature capitalist economies has shrunk to under 150m, as unproductive labour has risen sharply; in the so-called emerging economies the industrial workforce now stands at 500m, having surpassed the industrial work force in the imperialist countries by the early 1980s. In addition, there is a large reserve army of labour composed of unemployed, underemployed or inactive adults of another 2.3bn people globally that could also be exploited for new value.

So there may be life in capitalism globally yet even if it is in ‘down mode’ right now. Or maybe this potential labour force will not be ‘properly exploited’ by the capitalist mode of production and Gordon is right. The world rate of profit (not just the rate of profit in the mature G7 economies) stopped rising in the late 1990s and has not recovered to the level of the golden age for capitalism in the 1960s, despite the massive potential global labour force. It seems that the countervailing factors of foreign investment in the emerging world, combined with new technology, have not been sufficient to push up the world rate of profit in the last decade or so, so far. The downward phase of the global capitalist cycle is still in play.

Karl,

Interesting points. I think you are right to refer to the new industries that arose from the new technologies. What tends to happen is that first these new technologies are used to raise productivity. The reason why capital expands resources on their development after all is because it has faced crises of overproduction, as available labour supplies get used up, wages rise, and profit margins get squeezed.

It faces a limitation on expanding surplus value, because available labour supplies of labour-power have been used up, at existing levels of exploitation/productivity/technology.

“Given the necessary means of production, i.e. , a sufficient accumulation of capital, the creation of surplus-value is only limited by the labouring population if the rate of surplus-value, i.e. , the intensity of exploitation, is given; and no other limit but the intensity of exploitation if the labouring population is given.”

(Capital III, Chapter 15)

So, it searches for and develops new technologies to use in production to replace labour, create a relative surplus population, and thereby reduce wages, whilst also reducing the value of existing constant capital, and thereby ultimately causing the rate of profit to rise, a process seen in these various stages from the early 1980’s onwards.

The application of these new technologies tends first then to be in the development of industries that meet these needs, primarily. A look at Britain and other parts of Europe, in the 1960’s, however, shows that it is then, when once again productivity starts to slow, as that roll out of new technology has become long in the tooth, and as wages begin to rise, that the real expansion of these new technologies into consumer goods production, really starts to take off.

For example, in the early 1960’s, very few people had cars, the majority of TV’s were rented, and so on. A decade later, the situation had been transformed.

I would have to disagree with the impression given by your comment “While the industrial workforce in the mature capitalist economies has shrunk to under 150m….” that it is only workers involved in material production that are productive workers. That was Adam Smith’s second and faulty definition of productive labour, which Marx says represented a slipping back by Smith into Physiocratic conceptions.

Simply because workers are involved in immaterial production, rather than material production, does not at all mean that they are unproductive. As Marx describes, it is whether their labour exchanges with capital rather than revenue, whether they are productive of surplus value, which determines whether they are productive rather than unproductive labourers, and in modern economies the vast majority of production is immaterial rather than material production, and it is this production which is the largest generator of value and surplus value.

Marx describes the way even “unproductive”, i.e. unproductive of surplus value, is productive of value.

“Is not the [total] value of the commodities at any time in the market greater as a result of the “unproductive labour” than it would be without this labour? Are there not at every moment of time in the market, alongside wheat and meat, etc., also prostitutes, lawyers, sermons, concerts, theatres, soldiers, politicians, etc.? These lads or wenches do not get the corn and other necessaries or pleasures for nothing.” (Theories of Surplus Value, p 168)

The actor who gives a performance thereby creates additional value as a consequence of the expenditure of their labour. As a commodity, it has an exchange-value, and thereby exchanges for other commodities of equal value, either directly or via the mediation of money.

“Since here, as in every exchange of commodity for commodity, equal value is given for equal value, the same value is therefore present twice over, once on the buyer’s side and once on the seller’s.” (ibid, p 169)

But, as Marx sets out in contradistinction to Smith’s second definition, the determination of whether this labour of the prostitutes, lawyers, actors and so on is “productive” or not does not at all depend upon the concrete nature of that labour, but as Smith had set out in his first definition, on whether this labour exchanges with capital or revenue.

“A writer is a productive labourer not in so far as he produces ideas, but in so far as he enriches the publisher who publishes his works, or if he is a wage-labourer for a capitalist.

The use-value of the commodity in which the labour of a productive worker is embodied may be of the most futile kind. The material characteristics are in no way linked with its nature which on the contrary is only the expression of a definite social relation of production. It is a definition of labour which is derived not from its content or its result, but from its particular social form.” (ibid, p 158)

“These definitions are therefore not derived from the material characteristics of labour (neither from the nature of its product nor from the particular character of the labour as concrete labour), but from the definite social form, the social relations of production, within which the labour is realised. An actor, for example, or even a clown, according to this definition, is a productive labourer if he works in the service of a capitalist (an entrepreneur) to whom he returns more labour than he receives from him in the form of wages; while a jobbing tailor who comes to the capitalist’s house and patches his trousers for him, producing a mere use-value for him, is an unproductive labourer. The former’s labour is exchanged with capital, the latter’s with revenue. The former’s labour produces a surplus-value; in the latter’s, revenue is consumed.” (ibid p 157)

Let me try to put the new technological changes into a Marxist perspective.

Technological changes:

A) Reduction of Capital Costs due to the sharing of R&D.

Many companies have started working together on R&D. This started when the Free Software/Open source movement started. Software and hardware is now researched in the open with everyone benefiting. This happens because the companies that do the R&D do not profit from the hardware/software but from their use or by providing technical support.

B) New technologies can increase productivity immensely but they destroy the capital of the old investments.

Common examples are:

1) The database market valuation was huge until new free software databases were created. The market shrunk and the new companies managed to take a big share of it.

2) New payment systems like bitcoin/ripple/etc. have the potential to disrupt the current banking system since the cost of banking is becoming almost zero.

C) Massive scale cooperation/coordination can lead to new heights of exploitation.

The internet and mobile phones allow the effortless coordination of many people. This has led many companies to invest to such technologies. The result is that they are able to “employ” a huge number of people with limited cost, allowing them to take over the markets and in the future act as monopolies.

This allows those companies to extract huge amounts of value from an immense number of “employes”.

Main example : Uber is taxi driver company that is now expanding to new markets.

There are 2 main arguments against techno-Utopians.

1) They believe that the immaterial world will become the dominant part of the economy and thus if we share knowledge we will not have need for capital.

The reality is quite different for 3 reasons:

a) The capital spent on factories is still much bigger that the one spent on research. (citation needed)

b) The capital spent on the research laboratories is also very big. We cannot have free access to laboratories.

c) The researchers require to work for many years in projects that might not become fruitful. They need a company to provide them with cash these years.

In other words, we can not get rid of capital and its effect on producing crises, inequality and ecological destruction.

2) Technological advances do not stop the laws of capitalism from functioning.

The problems we face today are not technological, nor can they be fixed by technology. The are systemic problems risen because of the effects of Capital in the Economy.

The effects of a new technological change cannot be determined without the context of Society and Capitalism.

If you want to follow people that are critical of techno-Utopianism you can check Evgeny Morozov and Bret Scott.

I, for one, can hardly wait for Boffy to intervene. Michael has launched a direct challenge to Boffy’s claims about new technologies opening up new profit centers .

I agree that productivity growth is likely to slow. I argued that more than three years ago. But look at the graph above, which shows a similar decline in productivity growth after 1960, and up to 1980, Which is also consistent with the argument I have made previously.

During that period of slowing productivity growth, the consequence was that relatively more labour-power must then be employed for any given accumulation of capital, and increase in output. This relative increase in the demand of labour-power to its supply, then led to periods of full employment in the 1960’s, which caused competition for labour-power, pushing wages and wage share higher, which means that the increased number of workers, with increased levels of wages, demand increased quantities of wage goods, which causes firms to switch production towards the production of these wage goods, and to expand their capitals so as to meet this additional demand for those goods.

As profits get squeezed, but individual capitals need to expand to meet this additional demand, it means that the demand for money-capital rises relative to the supply, which pushes interest rates higher, which causes the capitalised prices of financial assets such as shares, bonds and property to fall.

Its why a look at the big picture shows that during such periods these financial markets tend to decline in real terms, as the real economy expands. The graph of the Dow Jones, adjusted for inflation between 1925 and 2010, given in my post Oil and Equities, demonstrates this point. It shows that on an inflation adjusted basis, the Dow fell by around 60% between the early 1960’s and 1980, when such a period of rising wages causing a profit squeeze, led to rising interest rates.

It makes far more sense to me to say the stock market falls due to a profit squeeze as a result of real wage increases and increases in the wage share, but why on earth is that relevant to the big picture today?

Though from the comments you have made previously I assumed you believed early cycle economic growth was affecting the stock market value, which seems counter intuitive to say the least.

Now I am really confused.

Edgar,

As Marx demonstrates in Capital III, the prices of bonds and shares are determined by capitalising the revenue they produce, just as the price of land is determined by capitalising the rent it produces.

There are two ways that the price of land can rise. One is that rents rise. If the rent on a piece of land is £100 p.a., and the average rate of interest is 10%, the capitalised price of the land is £1,000. If the rent rises to £200 p.a., the capitalised price of the land rises to £2,000.

The second is that the average rate of interest changes. If the rent remains £100 p.a., but the average rate of interest falls to 5%, the capitalised price of the land will again rise from £1,000 to £2,000.

The same applies with bonds and shares. For the price of shares to rise, either profits must rise, so that more can be paid out in dividends, or else, the average rate of interest must fall, so that the capitalised value of these dividends rises.

If a company pays £100 p.a. in dividends, and the average rate of interest is 10%, the capitalised value of the shares is £1,000, which rises to £2,000 if the average rate of interest rises. But, if profits rise, so that more can be paid out in dividends, so that the company now begins to pay out £200 p.a. in dividends, the capitalised value of the shares again rises to £2,000, even if the average rate of interest remains at 10%.

But, the average rate of interest is determined by the demand and supply of money-capital. As Marx sets out in Capital III, a rise in the rate of profit, seen in the early phase of an expansion will facilitate an expansion of dividends, which pushes share prices higher, but the rapid expansion of the mass of realised profits, causes the supply of money-capital to rise faster than the demand for that money-capital, so that the average rate of interest falls, and as it falls this causes the capitalised value of shares to rise further.

That is why rapid rises in the stock market often occur during periods of prolonged economic weakness, or the periods of stagnation as Marx describes them, which he clearly distinguishes from the periods of crises. The period of the 1970’s, was a period of crisis, for example, and the rate of interest was pushed higher, despite slow growth, because companies with squeezed profits from those higher wages, demanded money-capital to make up for the squeezed profits, and often to stay afloat.

In the 1960’s, the mass of profits continued to increase, but profit margins got squeezed as wages rose. The rising rate of interest was more than enough to counteract any rise in dividends to cause the capitalised value of shares to fall. If the current long wave boom started in 1999, then I believe we are at an equivalent position to that seen in the early to mid 1960’s. Something similar happened then with primary product prices to that we are seeing now.

When that overproduction is washed out, we may see a far more rapid rise in commodity price inflation than central banks currently envisage. That also happened, and took them by surprise in 1965.

My understanding is that the higher the dividend payment the greater this is a signal that companies expect weak growth and reduced future profit. And big dividend payouts lower the share price?

The company is expected to make money for the ‘owner’, and the profits are the possession of the owner. So they either get dividend payouts or the money is invested in the company because there is the prospect that the owners will get a greater return later.

Please provide an illustration, post WW2 where: “rapid rises in the stock market occurred during periods of prolonged economic weakness, or the periods of stagnation”

Edgar,

As Marx sets out in Capital III, Chapter 27, the “owners” of joint stock companies are “the associated producers”, i.e. the workers and professional managers of those companies. The joint stock company or corporation is a legal entity in its own right, which itself owns the productive-capital. That was established in English Law nearly a century ago.

“A company is an entity distinct alike from its shareholders and its directors.” (Shaw & Sons (Salford) Ltd v Shaw [1935] 2 KB 113 by Greer LJ.

Shareholders are nothing more than lenders of money-capital to the firm, no different in economic terms to a money-capitalist who lends money to such a company by buying its bonds, or making a bank loan to it. Indeed, in the last period, we have seen many joint stock companies borrowing money in the money market, to buy back the shares that are currently in the hands of shareholders.

Considered economically, the shareholders are entitled to nothing more than the average rate of interest on the money they have lent to the company, with an appropriate adjustment for the risk of holding shares, as opposed to bonds, or via a bank loan.

From a juridical perspective, they should have no more right to appoint their representatives to company boards, as a consequence of lending money to the company by buying its shares, and thereby to exert control over the company’s productive-capital than does a bond holder, or a bank that lends money to the company, or than a bank has a right to tell a homebuyer what colour they should paint their living room, simply because the bank has granted the homebuyer a mortgage.

In fact, in Germany those rights of shareholders are to some extent constrained by the co-determination laws. In the 1970’s, the EU proposed an extension of those laws across Europe via its Fifth Company Law Directive, which would have given workers the right to elect half the Board members of such companies. The Bullock Report of 1975, in the UK proposed similar measures. I have discussed all this in my recent response to Mike McNair.

As Kautsky put it,

“The corporation renders the person of the capitalist wholly superfluous for the conduct of capitalist undertakings. The exclusion of his personality from industrial life ceases to be a question of possibility or of intention. It is purely a question of POWER.”

(The Road To Power)

I don’t know how you get the idea that companies would increase dividend payments because they expect weaker profits growth, because the dividend is merely the form that payment of interest to the money-capitalist takes where the money has been loaned in the legal form of a share.

If companies increase dividends under such conditions it is not a reflection of economic laws, but as Kautsky suggests above, merely a question of political power, a reflection of the fact that these money-capitalists have been able to impose a control over property which does not belong to them, i.e. the productive-capital of the firm.

If we look at that over the recent period, the reason that an increasing proportion of realised profits has been taken up in dividend payments and other capital transfers to money-capitalists (according to Haldane it has risen from around 10% in the 1970’s to around 70% today), it is because the period of falling interest rates that began around 1982, brought with it, the kind of rise in capitalised prices of financial assets, such as bonds, shares, and also of land, described above.

The graph I have referred to above in my blog post on Oil and Equities, illustrates that point.

But, the situation in relation to nominal prices for GDP and stock markets also illustrates the point. Between 1950 and 1980, US GDP grew by 850%, whilst the Dow Jones rose by 300%. In the period between 1980 and 2000, however, US GDP rose by just 260%, whilst the Dow Jones rose by a whopping 1300%, and similar figures can be seen for the performance of the S&P during those periods.

In the latter part, of the later period, and in the period after 2000, the effect of low interest rates on those asset prices has been exacerbated by the direct action of central banks, which have printed money, and used it to buy government bonds, and also thereby provided masses of liquidity to commercial banks to use to lend, to provide liquidity for the speculative purchase of shares to inflate stock market valuations.

The reason they do that is obvious. The bank capital of those banks and financial institutions is based almost entirely on the possession of such financial assets, on the valuation of property that underlies the mortgages they hand out and so on. If the astronomically inflated book values of those paper assets fell significantly – as happened in Japan in the 1990’s for example – then it would become apparent that global banks are insolvent, that their bank capital is actually worthless.

But, it is the much goosed prices of those financial assets, which then means that yields on them get crushed. The actions of money-capitalists over the last period has had very little to do, even more than usual, with financing additional investment in productive capital, and has been largely concerned with simply competing with each other for existing stocks, bonds and property, which pushes the market prices of those assets ever higher.

Even if profits expand at a decent clip, therefore, the potential to finance higher dividends, other interest payments, or rent out of that profit does not rise at the same rate as the huge rise in asset prices, so that even as the absolute amounts of dividends, interest and rent rise, the yield falls. A look at rental yields in places like London demonstrates that. Large rises in rent – which has driven a massive rise in the UK Housing Benefit Bill – but falling rental yields.

In order to compensate for the falling yields, ever more has been drained into the financing of such revenues, and away from capital accumulation, which leads to the process of “capital eating itself”, referred to by Haldane. It is why Haldane, Clinton and others have again raised the issue of a need for a reform of laws on corporate governance. It is why even some of the representatives of money-capital have recognised that such a situation is not sustainable and that the laws of economics will out in the end, requiring a return to investment in productive-capital.

Edgar,

Incidentally, as I also point out in my response to Mike, it demonstrates Marx’s point,

“It would be still more absurd to presume that capital would yield interest on the basis of capitalist production without performing any productive function, i.e., without creating surplus-value, of which interest is just a part; that the capitalist mode of production would run its course without capitalist production. If an untowardly large section of capitalists were to convert their capital into money-capital, the result would be a frightful depreciation of money-capital and a frightful fall in the rate of interest; many would at once face the impossibility of living on their interest, and would hence be compelled to reconvert into industrial capitalists.” (Capital III, p 378)

When the financial pundits claim that QE has not led to inflation, therefore, it is arrant nonsense. It has led to a hyper inflation of these assets prices. As Marx points out above, there has been “a frightful depreciation of money-capital and a frightful fall in the rate of interest”, because every piece of that money-capital now buys less and less in terms of financial assets, capable of bringing it a given amount of return.

A money-capital of £1 million, which previously would have bought 13 million shares, today only buys 1 million of those same shares, and the dividend payment on them is correspondingly reduced. It is why pension funds have developed huge black holes, because to buy the same quantity of shares and bonds, so as to generate the same mass of dividends and interest to cover future pension payments, would have required workers pension contributions to rise massively, and as the provision of pensions is a part of the value of labour-power, it would have required wages to rise, so that workers could make those contributions.

That is just one way in which over the last 30 years real wages have been crushed below the value of labour-power, a situation, which Marx in Capital I, demonstrates is not sustainable forever, and tends to lead to a compensating rise in wages later. The same thing can be seen with the effect of inflating land and property prices, which has massively raised the cost of workers costs of shelter, with a consequent rise in the value of labour-power, which has similarly not been compensated in a rise in wages.

“But, the situation in relation to nominal prices for GDP and stock markets also illustrates the point. Between 1950 and 1980, US GDP grew by 850%, whilst the Dow Jones rose by 300%. In the period between 1980 and 2000, however, US GDP rose by just 260%, whilst the Dow Jones rose by a whopping 1300%, and similar figures can be seen for the performance of the S&P during those periods”

How convenient for Boffy to pick these blocks of time. If you break it down however, you find that between 1980-1990, the DJIA went from about 2700 to about 5000.

From 1990-2000– when the rate of capital investment and the rate of profit all reached post-1970 highs, the DJIA went from 5000 to 16,000.

If we look at trough to peak movement, then from the 1948 low of about 1400 the DJIA peaked at around 7300 in 1965,

Lesson of the story? As they used to say on Wall Street, three things children should never see being made:

1. other children

2. sausage

3. money in the stock market.

Edgar,

Just to give the figures for other market indices they are as follows at ten year intervals.

Dow Jones

1950 200

1960 679

1970 809

1980 824

1990 2810

2000 11723

2010 10618

S & P 500

1950 16.93

1960 59.91

1970 92.06

1980 107.94

1990 353.40

2000 1469.25

2010 1116.56

FTSE 100 ( I only have data from 1984)

1984 1108.10

1990 2442.40

2000 6930.20

2010 5412.90

I’m so gratified Boffy never reads anything I post .

Meanwhile inflation adjusted DJIA:http://www.macrotrends.net/1319/dow-jones-100-year-historical-chart (which I used in the previous post).

unadjusted:https://measuringworth.com/DJA/

unadjusted: the period referred to as “stagflation” in the US– 1970-1980, shows no growth in the DJIA;

rate of growth for the twenty period 1970-1990, less than half the rate of growth of the ten year 1990-2000 period.

Congratulations to Boffy for not making numbers up, just failing to understand them

Edgar,

I should also have given the actual figures for changes in GDP during the periods cited for clarity. The graph of the inflation inflation adjusted performance of the Dow Jones I previously cited above, and is included in my blog post Oil and Equities.

It shows that I think clearly the points I have described above, which you queried in relation to interest rates, and so on. For example, it indicates inflation adjusted rises in the Dow through the 1930’s, a period of stagnation, in Marx’s terminology. During such periods the rate of profit will be rising, as constant capital is depreciated, wages are reduced, and the rate of surplus value is thereby increased, as well as by rises in productivity caused by the introduction of new labour saving technologies.

As I’ve written previously, on my blog in relation to the Long Wave, Ray in his article in the Lloyds Bank Review referred to the work of Mensch, who identified technology peaks which occur at 50 year intervals, and which also appear to regularly arise 40 years before the peak of a long wave boom.

Mensch identified such a technology peak in 1935, and writing in the 1970’s, forecast another such peak to arise in 1985. A peak in 1935 for the technology peak, also coincides with the peak of the boom in 1974-5. A technology peak – this refers to the development of the “base technology”, for example the microprocessor, not to all of the various products that are then subsequently developed on the basis of it – in 1985, which then suggests a peak of the current boom in 2025, also looks about right.

The rise in profits during the 1930’s, on the back of this rising productivity, leads to the supply of money-capital outstripping the demand, which causes interest rates to fall, which causes the capitalised prices of shares and bonds to rise. That same rise during the equivalent period can be seen between the low of 1982 and 2000. I will indicate the relevant changes in GDP that relate to these periods later, both in absolute and inflation adjusted terms.

In Marx’s analysis of the interest rate cycle, and how it relates to the business cycle, he then describes the following period, as the period of prosperity. During this period, as economic activity picks up, this increased economic activity translates the higher rate of profit into higher masses of profit. The higher level of economic activity causes the demand for money-capital to rise, but not by as much as the supply of money-capital rises, as a result of the increase in money-capital resulting from significantly increased realised profits. The consequence is that the supply of money-capital continues to outstrip the demand for money-capital, so the interest rates stay low. The increased profits, which facilitate higher dividend payments push share prices higher, and the low interest rates cause the capitalised revenue to push share prices higher still.

That can be seen in the chart or the periods 1950-65, and would be apparent for the period after 2000, if the chart extended to current levels when the Dow reached its highest level. I have done some work, which is not yet complete, which indicates this even more clearly in relation to changes in global GDP.

Marx then describes the next phase of the cycle as the boom phase, and during this phase the processes I have described previously, and which Marx describes in Chapter 6 and 15 of Capital III, whereby extensive accumulation leads to labour supplies being used up, productivity growth slows, wages are pushed up, and consequently profits begin to get squeezed starts to occur. During this phase, as Marx describes, these processes begin to mean that the demand for money-capital starts to outstrip the supply for both the above reasons, so interest rates start to rise, and this rise in interest rates causes the capitalised prices of financial assets to fall.

That can be seen in the period 1963-74. As I wrote three years ago, I believe we have entered a similar period now. The period after this is characterised by Marx as the crisis phase, when all of these factors become heightened. Labour supplies are used up, productivity growth comes to a stop, profits are squeezed, the demand for money-capital outstrips the supply, as firms fail to produce enough profit to generate the realised money-capital required to fund their accumulation, and many firms demand money-capital not for accumulation, but simply to pay the bills and stay afloat. Its during this period that interest rates rise to their highest level, and the capitalised prices of shares drop sharply.

That was signified by the stock market crash of 1974, an can be seen in the chart where the Dow drops further from 1974 through to 1982.

The corresponding data for GDP for these periods is set out below, first in nominal terms, as that was the basis for the stock market indices given above, and then in 2005 dollar terms, to show the inflation adjusted changes, in accordance with the graph for inflation adjusted stock market prices.

US GDP $ Billions

Year Value % Change

1950 294.00 0.00

1960 526.00 78.91

1970 1,038.00 97.34

1980 2,788.00 168.59

1990 5,800.00 108.03

2000 9,951.00 71.57

2010 14,526.00 45.98

2012 15,094.00 3.91

Here can be seen the much greater rise in nominal GDP from 1950, through to 1980 than in the later period. I have further data, broken down by year, but which is not yet formulated. That would show the position, in relation to the period up to 1974, even more clearly, as well as the period after 1974.

Yet, as the Dow Jones, and S&P data provided above for nominal stock market performance shows, they rose much less during this period between 1960-80, when GDP growth was strong, than in the period 1982-2000, when it was weaker.

The large rise in nominal GDP between 1970 and 1980 is partly due to the higher levels of inflation during that period, so let me then give the inflation adjusted figures.

Year Value % Change

1950 2006 0

1960 2831 41.13

1970 4270 50.83

1980 5839 36.74

1990 8034 37.59

2000 11226 39.73

2010 13088 16.59

2012 13315 1.73

Once again, this shows the same picture as described above. In inflation adjusted terms, the strongest decade of growth is 1960-70. Yet, as the graph for inflation adjusted stock market growth indicates, during that period the markets were falling!

Growth between 1970-80, which covers the last part of the “boom” phase (1962-74) and first part of the “crisis” phase (1974-87), shows the same thing.

The data for the period between 2000 and 2010 is skewed, because of the effect of the 2008 financial crisis on the US economy. The picture up to 2008 gives a different colouration. The real picture will only be clear, perhaps in 20 years time, when the situation over the whole cycle can be seen.

Obviously, I retain all of the criticisms of the GDP data I have set out from a Marxist perspective in the past, which is that it is only an indication of the size and growth of the consumption fund, i.e. of the new value created by Labour, National Income/Expenditure (v = s), and not the value of National Output (c + v + s), as Marx describes at length in criticising such formulations as presented by Adam Smith.

And, as I have set out elsewhere, the picture is also skewed as a result of viewing the trajectory of a relatively declining economy such as the US, as opposed to the situation in respect of the global economy, which is vital from a Marxist perspective.

“whereby extensive accumulation leads to labour supplies being used up, productivity growth slows, wages are pushed up, and consequently profits begin to get squeezed starts to occur. During this phase, as Marx describes, these processes begin to mean that the demand for money-capital starts to outstrip the supply for both the above reasons, so interest rates start to rise, and this rise in interest rates causes the capitalised prices of financial assets to fall.

That can be seen in the period 1963-74. As I wrote three years ago, I believe we have entered a similar period now. ”

So that’s the period we are in now? No longer the “summer” or “late summer” or “early fall” of the long wave upturn?

Labor supplies being used up? That’s why unemployment rates in Europe for young workers are approximately 25%? That’s why labor-force participation rates are at or near their lowest levels in the US?

Demand for money-capital outstrips supply? Where is the demand for money-capital outstripping supply? Banks? Not hardly? Bond markets? No. Activity in the bond markets in January was dramatically less than the previous year. Interest rates rising? Which interest rates? those established by the ECB, the Fed, the Bank of Japan, the People’s Bank of China? Not really. The Fed’s .25% rise has been discounted, literally, as interest rates for US sovereign debt and high quality investment grade corporate debt have remained low, where they have not actually declined.

In secondary markets for emerging market debt? Yes. But is that because demand for money-capital is rising due to “extensive accumulation,” or is it because of a “flight to safety,” because of overproduction, and recession in those markets?

Are we in a “pre-crisis” period, with the period to follow one of “crisis”? When profits fall? But according to Boffy, just recently, the underlying fundamentals of the economy are “strong” and as in 1847 or 1857, will reassert themselves and all problems will be overcome.

And according to others the profit decline is “confined” to the energy sector and the rest of the economy is doing quite well thank you, right?– which of course is nothing but the latest iteration of the view that 2008 was just a “financial crisis,” with no greater meaning for the real economy, where fundamentals are always strong, and healthy. Now it’s a profit crisis confined to the energy sector. Or may energy and mining. Or maybe energy, mining, maritime shipping. Or maybe all of those plus steel? And semiconductors?

What is missing, what is always missing, from Boffy’s fantastic explanations of why everything is always the same and the same is always good is, of course, the role of capital spending itself..

Boffy,

A lot to take in and some of what you say does chime as being true.

Below are the areas of confusion:

“the “owners” of joint stock companies are “the associated producers”, i.e. the workers and professional managers of those companies. “

Maybe the professional managers but the workers? This will come as news to the workers of these organisations who have literally no say in how the surplus is divvied up and are basically instructed to follow orders or face the sack! I suspect a wry smile would pass the face of the directors at this suggestion.

The majority shareholders exert more influence over the company and its decisions than the minority shareholders and workers put together. And from a strategic point of view the majority shareholders have more influence than the professional managers, minority shareholders and workers put together.

A shareholder who holds over 50% of shares, under law, has the power to appoint, and dismiss directors. In other words owning over 50% of shares gives you effective control of the company.

Though things are dependent on the company’s articles of association. These articles can be overridden with 75% of share ownership.

Shareholders are more than lenders of money capital. If Marx said otherwise he must have been an idiot, and he wasn’t!

Workers do not own joint stock companies, if Marx said otherwise he must have been an idiot, and he wasn’t!

The following article discusses the relationship between shareholders and directors. Please note that workers do not form part of the discussion

http://www.companylawclub.co.uk/what-is-the-difference-between-shareholders-and-directors

Regarding the relationship between economic performance and stock price, are we to take it that according to you a fall in the stock market is a sign of a positive economic outlook and furthermore is it your contention that a stock market crash is an indicator of very positive economic outlook?

Edgar,

“Maybe the professional managers but the workers? This will come as news to the workers of these organisations who have literally no say in how the surplus is divvied up and are basically instructed to follow orders or face the sack! I suspect a wry smile would pass the face of the directors at this suggestion.”

The point is made by Marx in Capital III, Chapter 27. The joint stock company/corporation is a legal entity in its own right. It owns the productive-capital, and as Marx points out that firm as an independent entity can be nothing other than those that comprise, i.e. the associated producers, which as he sets out in that chapter include the professional managers, who are merely skilled workers paid a wage, the same as other workers, in fact frequently paid less than other skilled workers.

The professional managers here are those that actually participate in that labour process of organisation and supervision, the people who as I’ve pointed out before were members of unions such as Auew-tass, headed up by CP’er Ken Gill, or ASTMS headed up by left social democrat Clive Jenkins. Like Marx I’m not talking here about the Executives placed above these professional managers, simply to represent the interests of the shareholders, against the interests of the productive-capital.

The fact that the representatives of shareholders exert control over the property of the firm, as Kautsky sets out, and as Marx describes, flows not from the actual economic laws, or even principles jurisprudence, but purely from the political power of those money-capitalists represented by conservative forces.

Its why Marx distinguishes between the situation in the joint stock company and in the worker-owned co-operative. But, its also why I pointed to the fact of the co-determination laws in Germany, and the fact that in the 1970’s, before money-capital began to exert such political control, those proposals for workers democracy, were common place. For example the Bullock Reports terms of reference stated,

“Accepting the need for a radical extension of industrial democracy in the control of companies by means of representation on boards of directors, and accepting the essential role of trade union organisations in this process to consider how such an extension can best be achieved…”

It recommended that trade unions elect half the members of company Boards. Of course, socialists do not for a minute confuse this with any kind of socialism, but it does illustrate the way that the interests of this productive-capital is represented by such social democracy, whereas it is the interest of interest-bearing capital, of fictitious capital that is represented by conservative forces.

Speaking in terms of economics Marx does say that the shareholders are nothing more than the providers of money-capital. Engels says the same thing in his Appendix to Volume III, on the Stock Exchange. Marx describes it succinctly in Chapter 27.

“Transformation of the actually functioning capitalist into a mere manager, administrator of other people’s capital, and of the owner of capital into a mere owner, a mere money-capitalist.”

It is the basis upon which profit is divided into profit of enterprise and interest, with dividends being simply a specific form of interest payment.

“Regarding the relationship between economic performance and stock price, are we to take it that according to you a fall in the stock market is a sign of a positive economic outlook and furthermore is it your contention that a stock market crash is an indicator of very positive economic outlook?”

No, if you look at what I set out, it comprises a number of factors including the amount of profits, which facilitate more or less revenue, as interest to shareholders, and the average rate of interest which determines how that revenue is capitalised into share prices.

So, for example, I set out that in the post-war period of growth (what Marx calls the prosperity phase, and what Long Wave theory describes as the Spring Phase (1949-62), there is rising profits, and low interest rates, which facilitates rising share prices. The same phase would be 1999-2012. In the next phase, which Marx calls the boom phase, and which Long Wave theory describes as the Summer Phase, (1962-74, and I beleive 2012 – around 2025) you start to see the relative surplus population used up. That is more than apparent in China, for example. It can be seen in the UK and US, Germany and other northern European economies. It does not currently mean general labour shortages, because we are only at the start of this phase, as was the case in 1962, for example. But, some specific shortages arise for specific types of skilled labour. That can be seen in the UK in relation to doctors, for example.

In other words, the productivity growth of the previous period which facilitated growth without using up the labour reserves starts to unwind. Wages begin to rise due to a competition for available labour supplies, and that squeezes profit margins as happened in the 1960’s. So, although the mass of profits continues to rise, the demand for money-capital starts to outstrip the supply, pushing interest rates higher, which acts to reduce the capitalised value of dividends, pushing share prices lower, which is what is seen in the inflation adjusted chart for the Dow, after 1962.

At the end of this boom (Summer phase), that process has led to the actual general labour shortages that create the potential for the kind of crisis of overproduction crises that Marx discusses in Capital III, Chapter 15, where he writes that more capital cannot be employed, because so much labour has been employed, and wages have been pushed up squeezing profit margins to such an extent that if more labour is employed, the rate of surplus value will drop to zero, so that no additional surplus value will be produced.

“There would be absolute over-production of capital as soon as additional capital for purposes of capitalist production = 0. The purpose of capitalist production, however, is self-expansion of capital, i.e., appropriation of surplus-labour, production of surplus-value, of profit. As soon as capital would, therefore, have grown in such a ratio to the labouring population that neither the absolute working-time supplied by this population, nor the relative surplus working-time, could be expanded any further (this last would not be feasible at any rate in the case when the demand for labour were so strong that there were a tendency for wages to rise); at a point, therefore, when the increased capital produced just as much, or even less, surplus-value than it did before its increase, there would be absolute over-production of capital; i.e., the increased capital C + ΔC would produce no more, or even less, profit than capital C before its expansion by ΔC. In both cases there would be a steep and sudden fall in the general rate of profit, but this time due to a change in the composition of capital not caused by the development of the productive forces, but rather by a rise in the money-value of the variable capital (because of increased wages) and the corresponding reduction in the proportion of surplus-labour to necessary labour.”

Under those conditions not only have profits been squeezed, reducing the amount that can be paid out as interest/dividends to shareholders, but in order to meet their demands for money-capital, businesses have to resort to the money markets for those funds. Bankers and bourgeois economists believe that the demand for money-capital only ariss for the purpose of investment, but Marx ridicules such views showing that the point that the demand for money-capital oustrips the supply by the greatest amount, is where this money-capital is demanded so that firms can simply stay afloat, and make the necessary payments. Its at this point that interest rates reach their peak.

Its at this point that the capitalised value of shares get slammed, as happened in 1974.

But, that also sets the conditions for the next upswing. During this crisis (autumn phase), capital seeks out labour saving technologies and so on. In the following stagnation (Winter Period) 1987-1999, they start to get introduced, the relative surplus population is built up, wages are reduced the rate of surplus value rises, the rate of profit rises, and interest rates fall, which acts to push the capitalised value of dividends higher, so stock markets rise, which is what is shown in the graph for the period from the early 1930’s, and which is also seen in the period from the early 1980’s.

The point being here that, it is the prospect of economic growth which will act to push up interest rates, as the demand for money-capital rises, and it is that rise in interest rates which will cause the capitalised value of dividends to fall, causing stock markets to drop, as they did in the past, and as they are now.

“The point being here that, it is the prospect of economic growth which will act to push up interest rates, as the demand for money-capital rises, and it is that rise in interest rates which will cause the capitalised value of dividends to fall, causing stock markets to drop, as they did in the past, and as they are now.”

Remember those words. It’s not the slow down in China causing stock markets to drop; It’s not the overproduction of oil. It’s not declining growth rates, and declining absolute growth in Brazil or South Africa or Italy or Canada or Russia.

That’s why global trade has accelerated to levels….wait a minute, never mind.

If memory serves me correct the Bullock report was swiftly discarded and Bullock was sent for re-education!

The idea that professional managers within the firm are the real owners was put forward by JK Galbraith I think. I think the idea is flawed, in that while these managers run day to day operations, bully and discipline staff and can build internal empires etc, in the final analysis the strategic decisions and ultimate oversight are in reality the possession of the majority shareholders and their internal mouthpieces, the board of directors. The professional managers simply do the dirty work. Whether any of these individuals are members of unions seems irrelevant, unless I am missing something.

But in your first comment you said legally the workers were owners of joint stock companies. So, just to be clear on the matter, are you claiming non managerial workers own joint stock companies? And if so can you list those joint stock companies where this worker ownership asserts itself in any meaningful sense? We can then compare your list with the list of joint stock companies where the majority shareholder (s) assert most influence. I think that will best illustrate the truth of matter and blow out of the way any legal technicalities or muddle headed arguments.

“I set out, it comprises a number of factors including the amount of profits, which facilitate more or less revenue, as interest to shareholders, and the average rate of interest which determines how that revenue is capitalised into share prices”

Yes but those factors do not describe the period we are in, are not the big picture to use a phrase you used previously. The fact is that workers share of national income has fallen in the last few decades and the gap between real wages and productivity has widened. If, as you say, share prices fall as a result of a profit squeeze due to high wage share then this must come toward the end of the cycle, not at the early stage of the cycle. I don’t see anything in the unemployment rates in India or China to suggest labour reserves are being used up. I would be more inclined to believe there has been an oversupply of labour. The world you describe as the big picture is decades away.

As an aside I am still not sure whether you think the last 30 years has been a tale of a failure of supply side policies which has resulted in the rich not investing in real production but instead creating asset bubbles etc and living off the proceeds or whether you believe the last 30 years has seen the most staggering investment in real production in human history!

Edgar,

Yes, the Bullock Report was shelved. As were the EU’s Draft Fifth Directive on Company Law. That was the point I made that over the last thirty years it was fictitious capital that became dominant, as the long wave downturn set in after 1974. It was conservative ideology based on its interests that became dominant.

The point was, however, that the Bullock Report had been commissioned, that the EU had drawn up the Fifth Directive, and the Co-Determination Law continued to operate in Germany. And the fact is that today, as people like Andy Haldane have talked about “capital eating itself” as a direct consequence of the interests of fictitious capital, and the need to try to maintain dividend yields, being advanced at the expense of productive investment, so too he, Clinton and others have again begun to talk about the need for reform of corporate governance to deal with that situation.

I think you are confusing appearance and reality. What I am setting out, as Marx does in his analysis in Capital, is the underlying objective reality, not the superficial reflection of that reality in existing legal forms. The objective reality of the economic relations, and property forms is that the age of private capitalist property ended even during Marx’s time let alone, continuing today. Yes, there are lots of small private capitalist firms still today, in fact they make up the large majority of firms by number, but the reality of modern capitalism is that it is dominated by socialised capital, by large corporations, where the firm is a legal entity in its own right, and it is that legal entity not any individual, or group of individuals who own that capital.

As Marx states that legal entity of the corporation can be nothing more than the workers, including the professional managers that comprise it. As he states, in relation to the joint stock company,

“The capital, which in itself rests on a social mode of production and presupposes a social concentration of means of production and labour-power, is here directly endowed with the form of social capital (capital of directly associated individuals) as distinct from private capital, and its undertakings assume the form of social undertakings as distinct from private undertakings. It is the abolition of capital as private property within the framework of capitalist production itself.”

The joint stock company like the co-operative is a transitional form of property between capitalism and socialism.

“The capitalist stock companies, as much as the co-operative factories, should be considered as transitional forms from the capitalist mode of production to the associated one, with the only distinction that the antagonism is resolved negatively in the one and positively in the other.”

And the manifestation of this is,

“In stock companies the function (management) is divorced from capital ownership, hence also labour is entirely divorced from ownership of means of production and surplus-labour. This result of the ultimate development of capitalist production is a necessary transitional phase towards the reconversion of capital into the property of producers, although no longer as the private property of the individual producers, but rather as the property of associated producers, as outright social property. On the other hand, the stock company is a transition toward the conversion of all functions in the reproduction process which still remain linked with capitalist property, into mere functions of associated producers, into social functions.”

As Marx points out those professional managers, the functional capitalists, like all other commercial workers tend to see their wages drop, because of the spread of public education developed by capitalism, a process enhanced much more as capitalism developed the welfare state.

It makes no more sense to describe this transitional phase of property relations standing between capitalism and socialism, as being still the private capitalist property relations of the 19th century, than it would to describe a chrysalis as being a caterpillar, on the basis that it is not yet a butterfly!

The reality is that current property relations stand in this transitional stage, and they are no more heading back in the direction of private capitalist property than a chrysalis will go back to being a caterpillar rather than continuing to metamorphose into a butterfly. The difference here is that it requires human intervention to utilise those objective processes of transformation of property forms and property relations, and to bring the social relations into conformity with them.

The same problem seems to arise with your comments in relation to the current situation. You ask what is the relevance of the comments I made about wages rising and so on to the current situation, but then refer back not to the current situation, but the fact that “workers share of national income has fallen in the last few decades and the gap between real wages and productivity has widened.” In other words not the current situation, but the situation that has existed and developed over the “last few decades”.

The whole point about Marxist analysis is to look at the current situation not as an event frozen in time, but as a process, and to determine within that process the direction of travel – for example, a chrysalis does not morph into a caterpillar rather than a butterfly. It is precisely the fact of the nature of the previous few decades, which led to the current situation, but it is also that which conditions the change in direction, the future direction of travel that determines the other changes that flow from it.

It is not at all the case that this change in direction in the cycle can only be manifest at the end of that cycle, because that is to view things purely in terms of an event rather than a process. Take Marx’s analysis of the period of boom that ran from 1843-1865, for example. It was already the case within the first few years of that boom that wages started to rise. In Value, Price and Profit, he refers to the continual rise in agricultural wags between 1849-59, that eventually led to the introduction of labour-saving equipment in agriculture.

In the UK, in the early 2000’s, labour shortages for skilled workers such as plumbers were one reason for Blair encouraging the immigration of such skilled workers from Poland. The same was true for dentists etc. The UK economy absorbed 2 million additional workers during that period. In 2007, prior to the financial crisis, oil tanker drivers in the UK won a 14% pay rise, and similar wage rises were paid to other workers across Europe. There is currently a shortage of 45,000 lorry drivers in the UK, and that is forecast to rise to a 75,000 shortage in the near future. There is a shortage of train drivers, and so on. In London, a number of construction companies have reported having to not bid for profitable work, because they cannot get the skilled workers required to undertake the construction.

The using up of labour supplies in China has been well documented. It is why China has seen large rises in wages, and why it has begun shifting production to Vietnam, and other developing Asian economies, as well as to developing Sub-Saharan Africa.

I wrote about this back in 2010 – Chinese Workers and the State.

As David Pilling put it in the FT, the authorities are reflecting in their statements a basic reality. He says,

“The years of an endless supply of cheap labour, on which the first three decades of China’s economic lift-off was built, are coming to an end. That is partly demographic. Because of China’s one child policy, the supply of workers under 40 has dwindled by as much as a fifth. Fewer workers means more bargaining power.”

For scales to move in one direction or another it does not require that all the weight be placed on one side in one go, it only requires that weight be added to one side incrementally. For the balance between the demand for labour-power and the supply of labour-power to shift, it does not require that all available labour supplies be used up, it only requires that more labour gets used up than is being added.

The continual and fairly rapid rise in employment in the US, is itself indicative of such a process.

The same thing applies to your query in your final paragraph, which again seems not to understand the concept of process, that what was true at the start of a thirty year process can be metamorphosed into something completely different at the end of that thirty years.