The productivity of labour is an important ingredient of the rate of real GDP growth. What happens to productivity (output per worker or output per worker per hour) is important for mature capitalist economies because real GDP growth can be considered as made up of two components: productivity growth and employment growth. The first shows the change in new value per worker employed and second shows the number of extra workers employed.

In mature economies, employment growth has been slowing for decades. So faster productivity growth is necessary to compensate. In Marxist terms, that means slowing growth in absolute value (and surplus value) must be replaced by faster growth in relative new value (or surplus value). See my post,

https://thenextrecession.wordpress.com/2014/01/20/productivity-deflation-and-depression/.

In the first quarter of 2015, US productivity fell at a 3.1% annual rate. For all of 2014, productivity grew by a modest 0.7%, even less than the 0.9% productivity gain in 2013. From 1995 to 2000, US productivity rose at average annual rates of 2.8%, reflecting in part the boost the economy received from the internet boom. But since 2000, productivity has slowed to annual rates of 2.1%.

The productivity slowdown is being replicated in all the major economies. The US Conference Board, which follows productivity growth closely, found that global labour productivity growth, measured as the average change in output (GDP) per person employed, remained stuck at 2.1% in 2014, while showing no sign of strengthening to its pre-crisis average of 2.6% (1999-2006).

The Conference Board reckons that the lack of improvement in global productivity growth in 2014 is due to several factors, including a dramatic weakening of productivity growth in the US and Japan, a longer-term productivity slowdown in China, an almost total collapse in productivity in Latin America, and substantive weakening in Russia.

Labour productivity in the mature capitalist economies grew by only 0.6% in 2014, slightly down from 2013 when it was 0.8%. Productivity growth in the US declined from 1.2% in 2013 to 0.7% quoted above in 2014, whereas Japan’s fell even more from a feeble 1% to negative territory of -0.6%. The Euro area saw a very small improvement in productivity —from 0.2% in 2013 to 0.3% in 2014.

For 2015, a further weakening in productivity is projected, down to 2%, continuing a longer-term downward trend which started around 2005. Despite a small improvement in the productivity growth performance in mature economies (up to 0.8% in 2015 from 0.6% in 2014), emerging and developing economies are expected to see a fairly large slowdown in growth from 3.4% in 2014 to 2.9% in 2015. The decline is primarily a reflection of the continuing fall in growth and productivity in China, but also includes the negative growth rate of Brazilian and Russian productivity

In the US, the ECRI, an economic research agency, argues that: “With productivity growth and potential labour force growth both averaging ½% a year, trend real GDP growth is converging to 1% a year.”

The ECRI goes on: “Recoveries have been weakening due to declines in growth in output per hour (i.e., productivity), growth in hours worked, or both. Taken together, they add up to real GDP growth. It’s just simple math….So, unless there’s good reason to believe that productivity growth will revive, trend GDP growth may very well stay stuck in the 1% range for years to come. If so, growth slowdowns could much more easily push growth below zero, leaving very little room for error. Is the Fed ready?”

What the productivity growth figures show is that the ability of capitalism (or at least the advanced capitalist economies) to generate better productivity is waning. Thus capitalists have squeezed the share of new value going to labour and raised the profit share to compensate. But above all, they have cut back on the rate of capital accumulation in the ‘real economy’, increasingly trying to find extra profit in financial and property speculation. Look at the growth in the accumulated stock of capital in the advanced capitalist economies. This is a measure of the level of productive investment – it’s grinding to a halt.

Take the UK. British real economic output is only about 3% higher than at the beginning of 2008. Yet labour input (hours worked adjusted for schooling and experience) is up 11% and the real value of the UK’s net capital stock has grown only 6%. So underlying productivity has plunged in the last seven years.

A recent paper by the National Institute of Economic & Social Research (NIESR) suggests that the UK’s productivity fall may be due to widespread weakness in TFP within firms. And that seems to be because British companies prefer to employ cheap and temporary labour rather than invest in training to raise skills and utilise new technology. This goes back to the ‘hand car wash’ argument, where cheap labour means that firms don’t need to invest in equipment. Instead new and existing firms just find ways of profiting from the ready supply of cheap labour.

Indeed, a recent IMF paper concluded that labour market ‘deregulation’ (part-time, zero hours contracts, temporary, easy hire and fire etc), introduced as part of neo-liberal policies over the last few decades, may have raised profits but has done nothing to improve productivity and might even have made it worse.

An important debate is taking place inside the US Federal Reserve on the reasons for this slowdown. John Fernald, an economist at the Federal Reserve Bank of San Francisco, has argued that the slowdown started before the financial crisis and was associated with the end of the information-technology driven boom of the 1990s. David Wilcox, director of the Federal Reserve Board’s research and statistics division, argued with colleagues in a 2013 paper that the slowdown was associated with the 2007-2009 recession and a drop-off in new business formation and in productivity-enhancing investment by firms.

The Wilcox story is the more hopeful one. If the productivity slowdown is associated with the recession, then presumably its effects will eventually wear off and growth can get back on a faster path without causing inflation. The Fernald story is troubling. If productivity was really in a downtrend before the crisis, then Americans might be stuck with an economy prone to serial growth disappointments for the foreseeable future.

Now it has been countered by some mainstream economists that productivity growth is not being captured properly in the data. Capital investment growth is not really declining in the major economies. Much of the apparent slowdown only reflects lower relative prices of investment goods compared to consumer goods and services.

In the US, over the past two decades, prices of equipment have risen much less than the GDP deflator. When correcting for this price effect, the fall in US non-residential investment to GDP ratios is much less pronounced. The phenomenon is even more noticeable in IT investment. If IT prices had risen at the same rate as overall prices, IT investment would now be nearly 1.2% of GDP higher than recorded, putting US total investment closer to 20% of GDP, levels last achieved back in the 1990s.

So the argument goes; you only have to look around to see that technological advance is making lives easier and quicker; and within companies, productivity-enhancing innovatory technology is taking place at an accelerating pace. The age of artificial intelligence is fast coming. And it’s just this sort of investment that is low in cost and requires a low threshold to deliver increased productivity.

Over the last 20 years, capex has been increasingly going into hi-tech, R&D and cost-saving equipment and less so into ‘structures’, long-term investment in plant and offices. In 1995, R&D was 23% of US business investment and structures were 21%. Now the R&D share is 31% and structures are unchanged.

Neoclassical economics likes to use a measure of productivity called total factor productivity (TFP). This supposedly measures the productivity achieved from innovations. Actually, it is just a residual from the gap between real GDP growth and the productivity of labour and ‘capital’ inputs. So it is really a rather bogus figure. But the argument goes; maybe capex (investment) may have been growing slower, but ‘capital productivity’ has been rising because that enigmatic component, total factor productivity, has been rising, even if the data on investment growth show a slowdown.

The trouble with this argument is that the data on TFP do not show any sort of pick-up that would be expected from the great new IT revolution that is under way. The latest Conference Board data show that the growth rate of global TFP continues to hover around zero for the third year in a row, compared to an average rate of more than 1% from 1999-2006 and 0.5% from 2007-2012. Indeed, most mature economies show near zero or even negative TFP growth. In China, TFP growth has turned negative and in India it is just above zero, while in Brazil and Mexico TFP growth continues to be negative.

So it is more likely that productivity growth has really slowed because the impact of innovations is still not enough to compensate for the failure of capitalists in most economies to step up investment. Indeed, it is not the pure technology of the Internet and ICT by itself which increases productivity and economic growth. Nobel Economics Prize winner Robert Solow already noted in a famous phrase in 1987, six years after the beginning of the mass introduction of personal computers into the economy, that computer technology was not speeding up US productivity growth: ‘You see the computer age everywhere but in the productivity statistics.’

This has not changed. In 1980, the year before introduction of the modern personal computer, US annual TFP growth was 1.2% (5yr rolling average). By 2014, US TFP was still only 1.2%. Therefore 34 years of revolutionary technological developments in the Internet and ICT had led to no increase in US productivity! The data therefore clearly shows that technological advance in the internet and ICT sector alone do not lead to productivity increases.

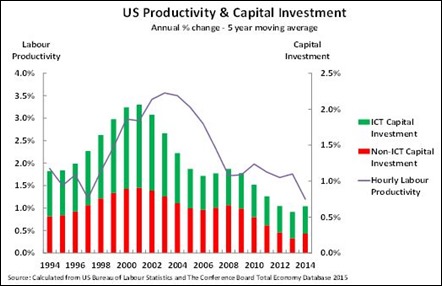

There was one phase during the 34 years of the internet and ICT revolution when US economic efficiency sharply increased. In the period leading to 2003, US annual productivity growth reached its highest level in half a century – 3.6%. This was explained by a huge surge in ICT-focused fixed investment. US investment rose from 19.8% of GDP in 1991 to 23.1% of GDP in 2000, fell slightly after the ‘dot com’ bubble’s collapse and then reached 22.9% in 2005. The majority of this investment was in ICT. After this, US investment fell, leading to the sharp productivity slowdown.

The way in which US labour productivity followed this surge in capital investment is clear from the chart. The correlation between the growth in investment and the increase in labour productivity three years later was 0.86, and after four years 0.89 – extraordinarily high. When capital investment fell, this was followed by a decline in labour productivity – showing clearly it was not ideas or pure technology that had caused the productivity increase.

In other words, productivity growth still depends on capital investment being large enough. And that depends on the profitability of investment. As argued ad nauseam in this blog: there is still relatively low profitability and a continued overhang of debt, particularly corporate debt, in not just the major economies, but also in the emerging capitalist economies (see

https://thenextrecession.wordpress.com/2014/09/30/debt-deleveraging-and-depression/; https://thenextrecession.wordpress.com/2013/12/04/cash-hoarding-profitability-and-debt/).

Under capitalism, until profitability is restored sufficiently and debt reduced (and both work together), the productivity benefits of the new ‘disruptive technologies’ (as the jargon goes) of robots, AI, ‘big data’ 3D printing etc will not deliver a sustained revival in productivity growth and thus real GDP.

Reblogged this on Ghostishynting.

Who will help in this discussion: http://socialdemocracy21stcentury.blogspot.com/2015/08/two-instances-where-marxs-theory-of.html

Tom we’ve been through this before, LK doesn’t know his Karl Marx from his Groucho Marx.

Back to the topic at hand, thank you Michael for yet again proving this is not the Summer of Love for capitalism.

So ICT investment did produce an accelerated AARG in productivity, Solow to the contrary notwithstanding.

Productivity growth should translate into shorter work time and no cut in pay, but it doesn’t because workers are not organised as a class, thus do not have the political power to demand it. The only shorter work time wage-slaves of the world get is unemployment or part-time jobs.

Productivity growth makes for less socially necessary labour time being embodied in finished commodities for sale, thus they contain less exchange-value. Less exchange-value can and usually does lead to lower prices. Lower prices mean less of a rate of profit per commodity sold, except when those lower prices are the price of labour power. Commodities must be sold for capitalists to obtain a profit from hiring wage-slaves to produce them. If real wages don’t increase, because labour is politically weak and divided as a class, the market dries up and capitalists don’t invest in new technology which will lead to greater productivity of the working class. Why hire workers to produce more commodities, if said commodities can’t be marketed? Instead of investing in more fixed capital e.g. machinery etc, the capitalists put their profits in bonds, real estate and tax sheltering bank accounts in the Cayman Islands etc.

Meanwhile, the political acceptance of lower real wages by the working class is helped along by their own increasing productivity and its effect on the prices of goods and services being marketed. Thus, the working class shops at Wall Mart where commodities are cheaper because they’ve been manufactured in the so-called “Peoples’ Republic of China” where employers make the latest in fixed capital ready at hand for workers to use in their places of employment to produce commodities during their labour time for their employers to sell in the markets of the world. Very productive workers they are too! As an extra added bonus for capitalists, the price of their skills is kept very low by the coercive power of the so-called “Communist State”. Workers are made very productive by the machines they themselves have produced, machines which become the property of their employers, of course, because wage-labour creates Capital.

Hi, thanks for the excellent summary. Do you have a link to the IMF paper on labor market regs and productivity mentioned?

http://touchstoneblog.org.uk/2015/04/labour-market-deregulation-when-the-facts-change/

and

Box 3.5 in http://www.imf.org/external/pubs/ft/weo/2015/01/pdf/c3.pdf

Michael,

The productivity slow down is again a typical sign of the turn from the Spring to Summer phase of the long wave cycle, as I predicted a couple of years ago. It is precisely what you would expect to see, as accumulation becomes more extensive than intensive. It means that labour supplies begin to get used up, a factor you have pointed to in your very good article about the continued high rate of economic growth in China, in last week’s Weekly Worker, and which acts to push up wages, which in turn leads to a profits squeeze and more frequent crises of overproduction, and also leads eventually to capital engaging in a new period of innovation to create labour-saving technologies, which then leads to a rising organic composition of capital, as productivity rises, which leads to a tendency for the rate of profit to fall, and for existing capital to be depreciated, which creates the conditions for the new boom.

What is interesting, however, in relation to the discussion over productivity and GDP growth, is the fascination with the actual GDP figure rather than, as you say, its composition. Firstly, the GDP figure is flawed for many reasons. So, too is the productivity figure, which is partly why Charlie Bean is being commissioned to look at the statistics and their collation.

But, as Marx points out, in his critique of Smith’s Trinity Formula, this GDP figure, is actually only a figure for society’s consumption fund, that is only of the new value created by labour during the year. As Marx puts it, it is only v = s, not c + v + s. As Marx explains at length, c actually comprises by far the largest component of output value, and its value is created in previous years, is passed on into the current value of output, but never comprises any component of National Income, because it never creates a revenue for anyone, as it is never a component of social exchange, being taken straight back out to replace the constant capital consumed in the production of constant capital, in the same way that a coal producer uses a portion of their own coal output to fuel the steam engines used to pump water from the mine.

Because orthodox economists base their theory on the Smithian rather than Marxist conception of value, and believe that the value of output is resolvable into revenues (wages, profits, interest and rent) they always end up with a figure for output that is wrong, because wages, profits, interest and rent are only resolvable into v + s, whilst the value of output is c + v +s. The inclusion of adjustments for fixed capital depreciation do not really change this, because the biggest component of c, is not wear and tear of fixed capital, but the consumption of raw materials and other circulating constant capital in the production of means of production.

The only c including in the GDP figure, is actually the value of c used in the production of the consumption fund itself, i.e. the production of intermediate goods. But, as Marx sets out in Capital II, Chapter 20, as well as in Capital III, and at even more painstaking length in Theories of Surplus Value, the value of this constant capital comprising the intermediate goods used in final production is only equal to the new value created by labour in Department. That is in a situation of simple reproduction I (v + s) = II (c), so that as he demonstrates, it is not an inclusion of the circulating constant capital at all, but only an inclusion of the new value created by labour in the production of means of production. That is not changed by assuming extended reproduction, as he sets out, particularly in Capital III, discussing the social reproduction process.

But, there is also another important issue, which he discusses in Theories of Surplus Value, in this respect, which is also the Smithian concern with the actual value of gross output. Marx quotes Ricardo, who points out that it is better to have an economy where 200 workers produce an output of £300, or sufficient to support 300 people, than to have 300 workers who produce an output of £400, or sufficient to support 400 people, even though the GDP, in the latter case is higher.

What Marx and Ricardo point out is that it is not the absolute level of the GDP that is important, but the size of the net product, or surplus value relative to the labour required to produce it. So, it might actually be a healthy sign, if the absolute level of GDP is lower, or even does not rise so much, if within that, the size of the net product gets relatively larger.

Marx gives the comparison of the situation in ancient Germany, where people worked for a period of time on the land producing food, and for a period fighting wars. The more productive the labour on the land, the larger the proportion of the population or the amount of time available to be fighting wars. Yet, as Marx sets out, the labour of soldiers fighting wars creates no value, rather it is a deduction from the produced value, even though it may be necessary labour.

An economy may be in rude health, therefore, even if its GDP does not rise so fast, simply because with rising productivity, it uses a larger part of the net product/surplus value to engage in unproductive labour, which adds nothing to output value. Again, however, this is a problem with the way capitalist economies put together their GDP figure, because even activities that actually create no additional value, are recorded as though they have done so, where they generate a revenue for someone.

Whilst, the unproductive labour may be utilised in some necessary function, which may facilitate indirectly the production of additional value, or may facilitate the realisation of already produced value – for example, as Marx describes it may support an extension of scientific investigation – it may on the contrary simply support an extension of wasteful expenditure in non-productive consumption. The example here, given by Marx is that the huge rise in productivity brought about by machines and other technological development during part of the 19th century, led to a massive expansion by the bourgeoisie in its employment of domestic servants, so that a huge rise in the rate of profit, brought about by the rise in productivity, instead of going into productive consumption went into non-productive consumption, and no addition to the production of value.

Michael,

I’d also be interested in what data you have in relation to productivity growth in different industries. A discussion I heard briefly on US CNBC last week suggested that productivity growth in some industries is actually quite high, and the national figure is being dragged down, by low levels in certain industries, the amount of labour employed in non-productive sectors and so on.

I don’t know if that’s right, but it would be interesting to crunch the numbers on it. There seems little doubt that in some areas able to utilise the latest computer technology – for example DNA sequencing – there has been a huge rise in productivity.

Reblogged this on Alejandro Valle Baeza.

I think we need to be very careful about drawing conclusions based on measures of productivity, especially since the Conference Board numbers don’t seem to agree with those of the the US Bureau of Labor Statistics– see for example BLS’ summary of changes for 2014 at http://www.bls.gov/news.release/pdf/prin.pdf.

In addition, consider the US petroleum industry– in 2015, prices per barrel have declined about $50/barrel from 2014. Employment has declined, but certainly not by 50 percent; rig count has decline but NOT new wells, as efficiencies in use have allowed drillers to drill more wells with a single rig. Output has decreased only some 200,000 barrels per day from peak of 9.7 million barrels per day.

What does that tell us about changes in productivity? Has productivity declined because the value of the output per hour has declined? Has productivity declined because so many fewer rigs are required?

And it is certainly not a decline in productivity that afflicts capitalism, but rather the accumulated increase in the productivity of labor; the overproduction, first and foremost, of the means of production as capital; i.e. as values that can only “exist” to the extent that the value is transformed, transferred into greater commodity values.

There is no “wage push” going on in US industry, with increases in real unit labor costs being below 2% per annum and labor force participation rates still at the historically low end at the spectrum– and the EU with unemployment rates well above the norm since 1990? “Wage push” is, like “rational capitalism” conspicuous only in its absence.

Agreed about being careful – the key contradiction is between productivity and profitability under capitalism.

Not a word on Marx’s insight that “productivity” is useless, as long as what is needed is profitability? Needed by capital, of course. I find here a deconnection with your deep theoretical analysis on the matter.

In fact, that “productivity” is necessary to appropriate (surplus) value, but value is created by labour at a fix rate of 1. Isn’t it?

In a certain capital, i.e. a firm, an industry, or even “developed capitalism”, productivity is the way to beat competitors or, at least, to not be beaten by them. But “capital in general” has in productivity a problem, not an ally.

Besides that, those measures of productivity based on GDP are contaminated by unproductive labour, which undermines value created, but appears as GDP growth.

Am i missing something?

Help, please

Agreed on many of your points. Profitability is key not productivity under capitalism and a rise in the latter will ceterus paribus squeeze the former. Such is the contradiction of capitalism. The point of my post is that productivity growth is necessary to achieve economic growth (even ‘unproductive growth’ like government services) and per capita economic growth and it ain’t happening much because investment is weak. But ye, if investment accelerated to raise productivity growth, eventually that would lower profitability of capital and lead to a slump. Harmonious and sustained growth cannot be achieved.

thanks a lot