Back in 2012, I presented a paper to the Association of Heterodox Economists entitled, A world rate of profit (a world rate of profit). Marx’s model of capitalism and its laws of motion are based on ‘an economy’, in other words, a world economy. Of course, there are still many barriers to the establishment of a world economy and a world rate of profit from labour, trade and capital restrictions designed to preserve and protect national and regional markets from the flow of global capital.

But in 2014, capitalism is much closer to be being a global economy than it was in 1914. So I tentatively suggested in that paper that, maybe, we could start to talk about a world rate of profit and start to measure it as an indicator of the underlying health and activity of capitalism globally.

In the paper I set out to try and measure a world rate of profit. I was not the first to do this. Minqi Li et al did some ground breaking work in their paper, Long waves, institutional changes and historical trends: a study of the long-term movement of the profit rate in the capitalist world economy, Long-Term Movement of the Profit Rate in the Capitalist World-Economy. They developed a world rate of profit for a long period going back to 1870. For the 19th century, their study integrated just the UK, US and Japanese rates of profit. For the period after 1963, the authors brought in Germany, France and Italy, to make the G6. Among other things, Minqi Li et al found that their world rate of profit tended to fall between the late 19th century and the early 20th century and again tended to fall between the mid-20th century and the late 20th century. And they confirmed a rise from the mid-1980s to a peak in 1997.

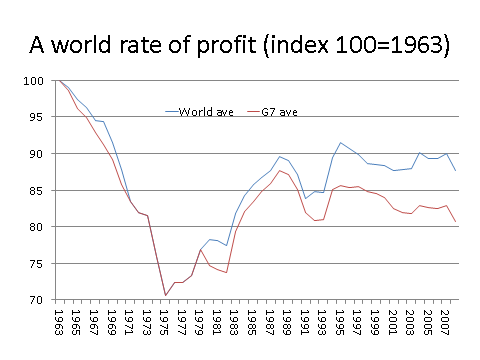

In my own study, I developed a world rate of profit that includes all the G7 economies plus the four economies of the BRIC acronym. So this includes 11 top economies which constitute a significant major share of global GDP. I use the extended World Penn Tables that David Zachariah used in his individual country study (see his paper, Dave Zachariah, Determinants of the average profit rate and the trajectory of capitalist economies, 4 February 2010, zacha10) I weighted the national rates for the size of GDP, although the crude mean average rate does not seem to diverge significantly from the weighted average. A proper measure of the world rate of profit would have to add up all the constant and variable capital in the world and estimated the total surplus value appropriated by global capital. This is really an impossible task. So weighted national profit rates are the only feasible way of getting a figure.

I found that there was a fall in the world rate of profit from the starting point of the data in 1963 and the world rate has never recovered to the 1963 level in the last 50 years. The world rate of profit reached a low in 1975 and then rose to a peak in the mid-1990s. Since then, the world rate of profit has been static or slightly falling and has not returned to its peak of the 1990s. And there was a divergence between the G7 rate of profit and the world rate of profit after the early 1990s. This indicates that non-G7 economies played increasing role in sustaining the world rate of profit. The G7 capitalist economies have been suffering a profitability crisis since the late 1980s and certainly since the mid-1990s.

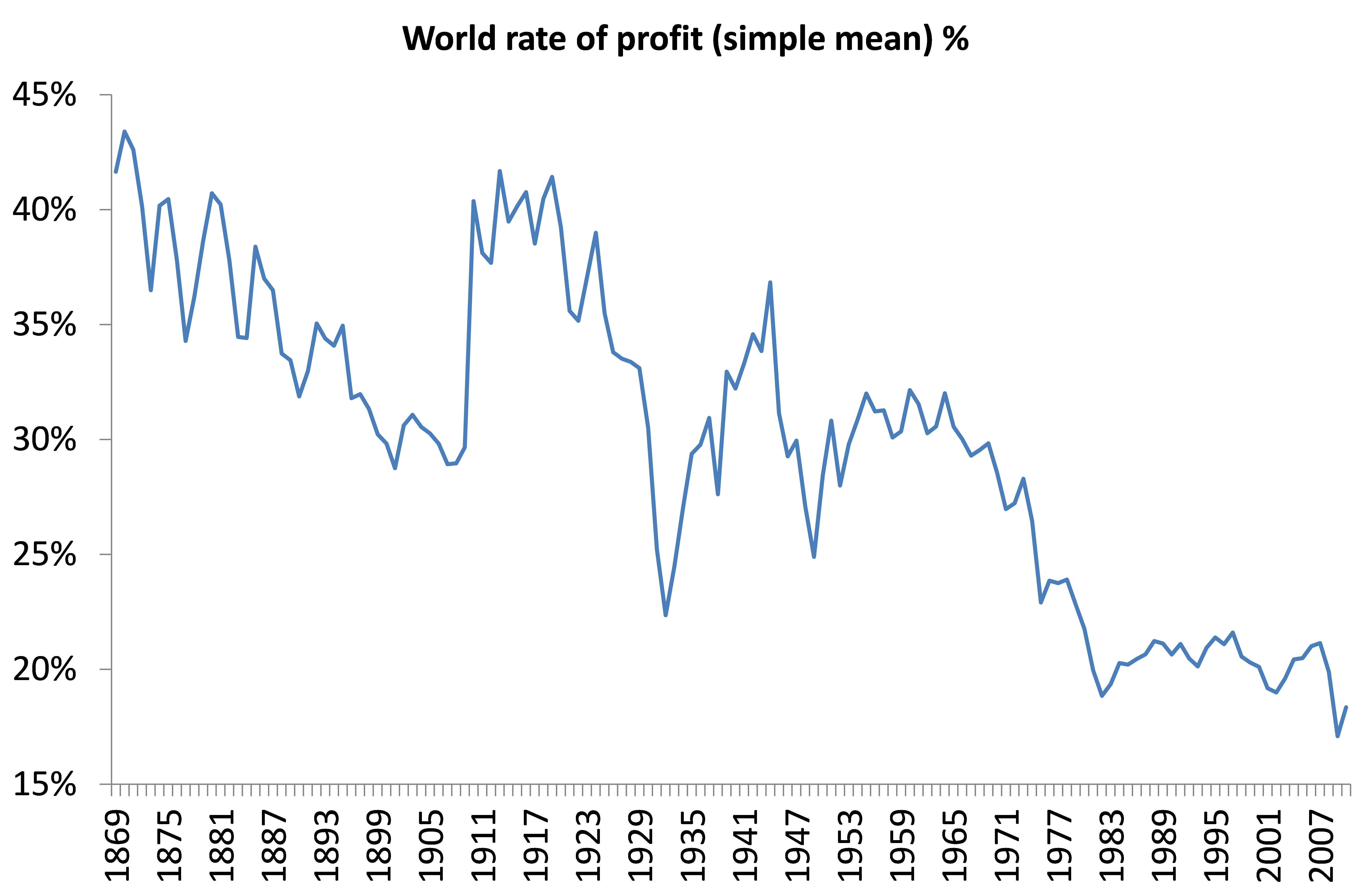

Now I have gone over all this again because there has been a brand new estimate of the world rate of profit in a new paper by Esteban Maito of Argentina (Maito, Esteban – The historical transience of capital. The downward tren in the rate of profit since XIX century). His paper presents estimates of the rate of profit on 14 countries in the long run going back to 1870. And Maito uses national historical data for each country not the Extended Penn Tables that I used. His results show a clear downward trend in the world rate of profit, although there are periods of partial recovery in both core and peripheral countries. So the behaviour of the profit rate confirms the predictions made by Marx about the historical trend of the mode of production. There is a secular tendency for the rate of profit to fall under capitalism and Marx’s law operates. Here is Maito’s world rate of profit back to 1869 (simple mean version).

Maito also finds, as Minqi Li and I do, that there was a stabilisation and even a rise in the world rate of profit from the early or mid-1980s up to the end of the 1990s, the so-called neoliberal period of the destruction of trade unions, a reduction in the welfare state and corporate taxes, privatisation, globalisation, hi-tech innovation and the fall of the Soviet Union. Again this seems to have peaked about 1997 (if China is excluded).

This is where Thomas Piketty comes into the story. In his book, Capital in the 21st century, now acclaimed by all the great and good in mainstream economics (see my posts, https://thenextrecession.wordpress.com/2014/04/15/thomas-piketty-and-the-search-for-r/ and https://thenextrecession.wordpress.com/2014/04/16/piketty-fest-continues-some-directions-for-the-reader/), and by many on the heterodox left, Piketty alludes to his book title as a follow-on from Marx’s Capital.

But he takes time out to insist that Marx’s law of profitability has proved to be fallacious. According to Piketty, “the rate of return on capital is a central concept in many economic theories. In particular, Marxist analysis emphasises the falling rate of profit – a historical prediction that has turned out to be quite wrong”. I won’t go into Piketty’s reasons for claiming why Marx was wrong here (I am saving that for my upcoming review of Piketty’s book in Historical Materialism). But the evidence from Maito, Minqi Li and myself makes a nonsense of Piketty’s conclusion about Marx’s law.

Piketty reckons that the net rate of return on capital (Piketty’s r) has been pretty static over the last 200 years at about 4-5%. This is crucial to his explanation of how capitalism can get into deep trouble. For him, it will be due to a rising share of profit going to capital and causing such extreme inequality that it threatens social instability. In contrast, Piketty does not see any crisis coming from falling profitability in the capitalist mode of production.

Piketty’s calculation that the net rate of return on capital has been steady is dubious even on his own definition of capital. But the real problem is that he defines capital as the same as wealth and thus includes residential property, even though houses are not means of production and do not ‘earn’ an income (unless they are owned by real estate companies and rented out). By including residential property in his calculations and concocting the ‘income’ from people’s homes as ‘rental equivalents’, Piketty ends up with completely distorted results for his r.

Moreover, here is some irony. Maito uses Piketty’s historical data for Germany to get a rate of profit for that economy. But Maito leaves out residential property and correctly categorises capital as the value of the means of production owned and accumulated in the capitalist sector. The result is not some steady r, but a falling rate of profit a la Marx. There a long-term decline, but with a rise from the 1980s to 2007 (which confirms my own estimates for Germany –

see https://thenextrecession.wordpress.com/2013/09/22/german-capitalism-a-success-story/).

Actually, Piketty’s r for Germany also falls from 1950 and then stabilises from the 1980s too. This is because, by 1950, landed property (also used in Piketty’s measure of ‘capital’) has disappeared in value and Germans generally have a much lower ownership of residential property compared to capitalist means of production as capital.

So Marx’s law of the tendency of the rate of profit to fall is again confirmed by this latest evidence on a world rate of profit. In my view, it remains the most important law of motion of capitalism, not Piketty’s r.

Mr. Roberts, I’m a lowly unionized labourer, and not a Marxian economics scholar, so ill make my comment/question brief. If your theory and Marx’s is correct on the world falling rate of profit, does this explain in the political sphere, why US imperialism is in decline while others such as India, China, and Brazil are on the rise? How does this falling rate of profit explain the recent findings in the NY Times and Wall Street Journal, that profits are at an 85 year high while wages are at 65 year low? I understand that rate of profit and accumulation of profit are two different things but at some points don’t they intersect?

Hi Jim,

I don’t consider a unionised labourer as ‘lowly’ nor a Marxian scholar as ‘high’. By the way I am a unionised ‘knowledge’ worker also.

To your conundrum: how can profits be at 85-year high and yet profitability is low? We can answer this question by using Marx’s law of profitability. Marx defined the rate of profit in a capitalist economy as the total amount of surplus value (profit if you like) captured by the capitalists at any one time divided by the total amount of capital accumulated and invested to get that profit. This capital is composed of what is invested in means of production like machinery, plant, technology and raw materials – this Marx called constant capital (c) AND the total amount invested in employing a workforce to use the means of production – this Marx called variable capital (v). So Marx’s rate of profit is total surplus value or profit (s) divided by constant capital (c) and variable capital (v). The simple formula is s/c+v.

Now Marx said over time capitalists invest more in mechanisation and technology relative to using labour. They try to get more profits by replacing labour with machinery to boost the productivity of the workers. So, over time, capitalists invest more in constant capital (c) than variable capital (v). So the ratio c/v, which Marx called the organic composition of capital, rises as capitalists expand production over decades. But more mechanisation and innovative technology will boost productivity and probably increase profits, so it is likely that the amount of profit (s) to the amount of wages paid to workers (v) will rise, depending on how well the unions do against the employers. This ratio s/v, Marx called the rate of surplus value. It is equivalent to a rise in the profit share compared to the wage share in all output – the point that you are making is happening now in the US.

So here is how the law works. If c/v rises faster than s/v then the rate of profit (s/c+v) must fall – it’s simple math. Marx says that in reality that is what does happen in a capitalist economy over the long run, most of the time. This is disputed by critics of Marx’s law.

What has happened in the US in the last 50 years? c/v has risen faster than s/v over that period, so the US rate of profit is lower in 2014 than it was in 1947 or even 1963. However, there have been periods when s/v has risen faster than c/v. This is what happened between 1982 and 1997 in the US, the so-called neo-liberal period when the unions were attacked in America and elsewhere. So in this short period, the rate of profit rose. Since about 2002, the rate of surplus value (s/v) has risen sharply and inequalities of income and wealth have got way worse. So profits have hit new highs. BUT during the last decade, c/v has actually risen faster even than this rising s/v, so the US rate of profit in 2014 is lower than it was in 1997. This explains the conundrum: capitalists have high profits and wages are being squeezed BUT because they still have a huge overhang of old capital (and also debt), so that their c/v is high, their overall rate of profit has not improved since 1997.

In the end, the rate of profit is what matters because capitalists can keep trying to increase their profits, but if the rate of profit keeps falling, eventually profits will too and then there is a crisis and slump. Indeed, the best way for capitalism to get its profitability back up is to have a slump (at our expense) so that unprofitable companies are bankrupted and more profitable ones take their markets, so reducing costs of c; while workers are made unemployed to reduce costs of v. That is the ‘aim’ of the Great Recession, but even that has not done the job yet. So we have high profits (s) and low wages (v), but a lower rate of profit (s/c+v).

But the Penn world tables are a PPP not a value measure. So how can they form part of an estimate of profit rates?

P.S. your table does not confirm the tropf in any respect as it shows profit rates have been rising for decades.

P.P.S. how do you account for the restoration of capitalism in the centrally planned economies? There was obviously no rate of profit before capitalism existed in them?

Its true that in Capital III, Chapter 13, Marx describes the “Rate of Profit”, as

“… the total amount of surplus value (profit if you like) captured by the capitalists at any one time divided by the total amount of capital accumulated and invested to get that profit.”

But, there are a number of points to be borne in mind.

1) This definition of the rate of profit was basically that used by previous bourgeois economists, such as Ricardo.

2) On the back of it they thought the “Falling Rate of profit” was important, because they thought it meant that Capitalism was doomed, because ultimately it would have to collapse under its own weight.

3) Marx thought that was nonsense and said so. His writings on the Falling Rate of Profit are designed to show precisely why their theory about this leading to a collapse of capitalism was wrong.

4) He shows that not only does the process which leads to a tendency towards falling profits also leads to a tendency towards rising profits, and the same process he says MUST cause the mass of profits and of Capital to RISE. As he goes on to say that it is this growth in the mass of profit not changes in the rate of profit that are decisive to accumulation, this puts the theory in its proper historical place.

5) In defining the “Rate of Profit” on the above basis as the bourgeois economists do, he also makes clear that this is based upon a single turnover of the circulating capital during the year. On that basis in Chapter 13, he analyses the “Rate of Profit” in terms of the component parts of the price of an individual commodity unit. In other words, he analyses the proportion of profit to unit price. In fact, he is making clear that on this basis what he is analysing is the undoubted fall in the profit margin on individual commodity units as the level of production is inexorably raised.

6) But, in Capital III having analysed the “Rate of Profit” on this basis he says,

““However, the rate of profit, if calculated merely on the elements of the price of an individual commodity, would be different from what it actually is. And for the following reason:”

and Engels adds,

“[The rate of profit is calculated on the total capital invested, but for a definite time, actually a year. The rate of profit is the ratio of the surplus-value, or profit, produced and realised in a year, to the total capital calculated in per cent. It is, therefore, not necessarily equal to a rate of profit calculated for the period of turnover of the invested capital rather than for a year. It is only if the capital is turned over exactly in one year that the two coincide.]”

And that is because Marx and Engels believed that the “Rate of Profit” as you have described it, and as was purveyed by the bourgeois economists, as well as the capitalists for their own reasons because it makes the rate of profit look much lower than it really is, and makes it look as though they have advanced much more capital than they really have, was a fraud.

That is why in Capital II, and in Capital III, Chapter 4 they define the annual rate of surplus value, and the annual rate of profit, which takes into consideration the rate of turnover of the circulating capital, and thereby shows that as social productivity rises, and raises the organic composition of capital, it brings about a corresponding rise in the rate of turnover of capital, which brings about a release of capital, which means that the annual rate of profit, as an accurate measure of the rate of profit and of the capital actually advanced by the capitalists, RISES not falls.

In Chapter 4, Marx makes this clear.

“To make the formula precise for the annual rate of profit, we must substitute the annual rate of surplus-value for the simple rate of surplus-value, that is, substitute S’ or s’n for s’. In other words, we must multiply the rate of surplus-value s’, or, what amounts to the same thing, the variable capital v contained in C, by n, the number of turnovers of this variable capital in one year. Thus we obtain p’ = s’n (v/C), which is the formula for the annual rate of profit.”

Given the huge rise in productivity over the last 100 years, and particularly over the last 30 years, it is undoubtedly the case that social productivity has risen – the process Marx identifies as raising the organic composition of capital – but that same process, as Marx sets out, MUST raise the rate of turnover of capital proportionately. If you just adjusted the rates of profit shown to take account for the average annual rise in productivity over the time period, as a proxy for the rise in the rate of turnover, the results of your data would be totally different from those you present.

Using an average 2% p.a. rise in productivity since 1950, as a proxy for the average rise in the rate of turnover, you arrive at profit rates today, that have to be trebled to make them comparable with the figures for 1950. That would give current profit rates way in excess of the earlier highest rates.

Thanx for the explanation. It leads to me to ask further questions though. How does this rate affects real value? I mean a million dollars today is work less than a third of what it was forty years ago. Also, the US prints money at its discretion with no underlined value other than what irrational markets determine. The US use to be on a gold standard. How are money supply and value of capital affected if at all by the falling rate of profit? I see how the fall of profits would increase prices regardless of demand and supply, but I still think I’m missing some pieces to the puzzle. Thanx again.

The ‘printing of money’ (or the creation of more credit and funds in banks) through so-called quantitative easing will accelerate inflation of prices if there is no corresponding rise in output to match it. So either the prices of the goods and services we buy will rise faster or the prices of financial assets, stocks and bonds, will rise faster, or both. In the recent period, printing money has just led to a stock market boom and not higher inflation of goods and services, because the extra credit has been used by the financial system to speculate or hoard. Credit-fuelled inflation pushes prices of things out of skew with the underlying value of those things as measured in labour time (or its monetary expression, namely gold). This will be expressed in the falling exchange value of the money used (dollars). But this cannot last indefinitely. The law of value and the law of profitability will exert itself and eventually cause a bust in the stock market or a sharp reduction in inflation when the credit boom turns into a credit crunch and bust. Money supply and the prices of things, including wages and goods, can get out of line with value, but like a yo yo, they will be pulled back with a vengeance later.

I’ve had just about all a human can take of Boffy’s distortion of Marx– where the decline in the rate of profit is always offset by an increase in the mass of profits; where increased investment in fixed assets and in constant capital automatically leads to shorter circulation times and quicker realization of capital; where the only problem capital ever faces is in the creation of new use-values, and never in VALUE production itself, i.e. the organization of labor as a commodity, as wage-labor, as value yielding, as surplus value producing WHICH can only occur if the means of production and subsistence are OPPOSED to the laborers, as CAPITAL; where VALUE is eternal, and the law of value is ahistorical, applying to all societies regardless of the mode of production AS IF the law of value exists, could EVER EXIST, independently of the the specific relations of the specific classes….

I’ve had enough of all of this and I will post as many selections from Marx as necessary to refute Boffy’s nonsense.

First, re circulation somehow offsetting the decline in profitability brought about by the growth of “c”: in the Grundrisse, Marx points out “Circulation therefore does not carry within itself the principle of self-renewal. The moments of the latter are presupposed to it, not posited by it.”

And later in the Grundrisse: “The simple movement of exchange values can never realize capital.”

Make what you want of that. I make that the realization of capital requires the expansion of value production, meaning the exploitation of wage-labor, and when the profitability of that exploitation falls, increased circulation cannot overcome the decline.

Or as Marx makes it clear in the Grundrisse labor exists as a/the use value of/for capital; the mediating activity by which capital realizes itself. It is the means by which it reproduces itself AS EXPANDED VALUE.

If we are to regard Marx’s work as the immanent critique of capital, as the critique contained within capital’s own manifestations, then we have to recognized that the “fault” “limits” “conflicts” “contradictions” of capital are contained exactly in this reproduction of expanded value. We must recognized that VALUE is an historically specific category, not a “universal” one; that VALUE production is the limit to capital. That, at a certain point, the labor process and the value production process which are fused in a specific social form, are in opposition to each other and explode into conflict.

Marx states: “The constantly ongoing devaluation of capital, resulting from the increase in the force of production………”

Stop right there: Get that? Capital is constantly devalued by increasing the force of production. This represents and obstacle, and impediment, and integument to the reproduction of capital. It is necessary to the expansion of capital– just as the prices of production serve to transfer value, to devalue some capitals– but the ongoing devaluation overtakes accumulation when profitability, when the rate of profit declines and the devaluation of “secondary” tertiary, etc. capitals does not siphon enough profit to offset that decline in profitability.

Really interesting post Michael. I am trying to read Maito’s work on the Argentinian rate of profit at the moment, with my limited spanish!

I was wondering what your thoughts are about the capital/output ratio as a proxy for the organic composition of capital? Anwar Shaikh seems to use it as such. Furthermore, why do you think this has fallen since the 1980s? It surely cannot be that capitalist production has been regressing in technological terms… As you can see I am a bit confused about these quantitative concepts and their meaning. Any light you could shed on this would be greatly appreciated.

Certainly capital shares “something” with all previous production– namely that it is “social” production; involving the organization and distribution of the total socially available labor-time over the activities necessary to the reproduction of society.

Yet capital is a specific organization of that social labor-time; where the “need” can only be meet through the organization of labor as a commodity for exchange– as a value for the production of values. This in turn requires a specific set of historical conditions (which Marx claims have been most clearly and perfectly achieved in England)– those conditions being the separation of the laborer from the instruments of labor– the dispossession of the independent, subsistence, and subsistence plus surplus producers. This IS the fundamental condition for the organization of capital; for VALUE PRODUCTION, which after all, is what capital is. And all this depends on LABOR having NO USE VALUE to the laborer SAVE ITS VALUE IN EXCHANGE FOR THE MEANS OF SUBSISTENCE.

This leads to the exchange of commodities at the time socially necessary for their reproduction– a UNIQUE SPECIFIC CONDITION for social production.

Marx puts it like this in the Grundrisse:

“The great historic quality of capital is to create this surplus labour, superfluous labour from the standpoint of mere use value, mere subsistence; and its historic destiny (Bestimmung) is fulfilled as soon as, on one sider, there has been such a development of needs that surplus labour above and beyond necessity has become a general need arising out of individual needs themselves– and, on the other side, when the severe discipline of capital, acting on succeeding generations has developed general industriousness as the general property of the new species, and finally when the development of the productive powers of labour, which capital incessantly whips onward in its unlimited mania for wealth, and the SOLE CONDITIONS IN WHICH THIS MANIA CAN BE REALIZED (caps added-SA), have flourished to the stage where the possession and preservation of general wealth require a lesser labour time of society as a whole, and where the labouring society relates scientifically to the process of its progressive reproduction, its reproduction in constantly greater abundance; hence where labour in which a human being does what A THING COULD DO HAS CEASED (caps added-SA).

So if “value” is eternal, if the law of value is universal, how can any of the above be accurate? How in fact if the “issue” — offspring of capitalism is unique, socialism, and requires such previous development, can the “law”– WHICH IS THE CLASS RELATION necessary to this development– have existed universally, eternally previous to the existence of the classes? It cannot.

Hence, what counts are the specific laws of value production, and the specific conflict within the terms, the conditions of value production– the conflict between labor and the conditions of labor. The condition of labor in capitalism is that in order to aggrandize greater portions of surplus value, capital has to expel proportionately greater amounts of living labor from production, thus undermining the very source of its profitability– the component, the relation, the RATIO of the source of new value, of profit to the production process.

Criticizing Ricardo for assuming that the categories of capitalist production are “natural,” ahistorical, universal, Marx writes:

“With him [Ricardo], however, wage labour and capital are again conceived as a natural, not as a historically specific social form for the the creation of wealth as use value; i.e. there form as such, precisely because it is natural, is irrelevant, and is not conceived in its SPECIFIC relation to the form of wealth, just as wealth, itself in its exchange value form, appears as a merely formal mediation of its material composition; thus the specific character of bourgeois wealth is not grasped– precisely because it appears there as the adequate form of wealth as such….. as if the form of wealth based on exchange value were concerned only with use value, and as if exchange value were merely a ceremonial form….. ”

So much for the universality of value production, its “eternal” quality divorced from the specific class relations of capital. So much for the problems of accumulation being confined, OR contained in the production of use values.

If we calculate the annual rate of profit, which is what Marx and Engels describe as reflecting the real situation, as opposed to the “Rate of profit”, which distorts the real relations. Then as Marx points out, its calculated as p’ = s’n (v/C). In other words, the annual rate of profit is = to the surplus value produced in one turnover period, multiplied by the number of times that the circulating capital is turned over during the year multiplied by the advanced capital for that turnover period.

Put another way, as Marx describes it, if we take the laid out capital for the year, which is what we have as the denominator for the Rate of Profit, and divide it by the number of times the capital turns over during the year, we have the advanced capital. Whatever the rate of profit determined on the basis of the rate of profit, we can equally arrive at the figure for the annual rate of profit, by multiplying that figure by the rate of turnover of capital.

Marx and Engels make clear that the main causal factor in raising the rate of turnover, and thereby raising the annual rate of profit is rises in productivity. As they point out, it reduces the working period, and the circulation period, thereby releasing capital, and increasing the rate of profit. This is set out clearly in Capital II, Chapter 15, and 16.

If e assume a 2% p.a. rise in productivity then as a proxy for the rise in the rate of turnover. We get a rate of turnover today, which is three times that for 1950. If we multiply the current rate of profit by 3, that gives us a comparable figure to 1950. In other words, it would give us a rate of profit today of around 3 x 20 (taking the 2007) peak or about 60%, which compares with a rate of profit of around 27% at the peak in 1953.

Assuming a similar trebling every 60 years, that would mean that to compare with the rate of profit indicated for the 1875 peak of around 50%, it is necessary to multiply the current figure by around 10 times to account for the current rate of turnover of capital being ten times higher than it was in 1875. That would give a current annual rate of profit of around 200% compared to the 50% rate for 1875.

As I said, calculated as an annual rate of profit as Marx and Engels do, the rate of profit today is much higher than in the past.

As for the ramblings of sartesian about the role of circulation, what does that have to do with anything that has been said. He’s clearly just on another of his usual trolling fishing trips, and demonstrating he doesn’t understand the issues in the process..

Boffy claimed that increased output from machinery while lowering the “unit” rate of profit, automatically raised the “turnover”–and thus the annual rate of profit. Marx makes it clear that no such thing occurs; there is no automatic increase in turnover, since turnover is a function of circulation which depends on all producers, not simply the application of new machinery to any individual process.

You will note how Boffy in the past was inclined to argue that now, just because a machine produces 6 (toothbrushes, plates, auto batteries, widgets) in the time it took to produce 1, such increases in production did not automatically mean increases in purchases of toothbrushes etc.

Now Boffy conveniently forgets what he previously argued when he argues that the decline in the “unit” rate of profit is offset by the automatic increase in “turnover.”

You all can make the call on who understands the issues.

Its fairly clear that you don’t understand the issues, because you’ve included a load of comments in all these posts that have absolutely nothing to do with what is being discussed, and your comments in respect of circulation show you don’t understand the function of the rate of turnover, or even what it means.

You have introduced a load of quotes about Value and the Law of Value, when the discussion has had nothing to do with those topics, and you have clearly just introduced all of that jumble of words into your posts, as part of a trolls day out fishing trip, trying to provoke me to take the bait.

As I found out long ago that its pointless wasting time trying to talk to trolls like you, I won’t be bothering taking any of that bait.

But, the comments about Value can quite easily be resolved by listening to what Marx himself had to say on the matter about the role of Value in a socialist economy.

““Secondly, after the abolition of the capitalist mode of production, but still retaining social production, the determination of value continues to prevail in the sense that the regulation of labour-time and the distribution of social labour among the various production groups, ultimately the book-keeping encompassing all this, become more essential than ever.”

Capital III, Chapter 49, p 851

All the quotes I’ve introduced are to refute claims you have made previously, and continue to make about what Marx wrote.

With the abolition of capitalism, value production, as such must disappear as the source of value production is wage-labor.

Value represents a specific social organization of labor; a specific mode of distributing, assigning, the available social labor time to the reproduction of that society. That you don’t understand that is beyond dispute– as are your ridiculous, and misleading comments, about turnover– as if production was immediately and directly turnover, and realization.

Book-keeping remains; value does not. All economy is, as Marx wrote, the economy of time. Not all economies of time are economies of value.

The fact that you don’t have the slightest conception of the historical specificity of the law of value, that it only exists as and due to a relation of classes defines precisely your lack of comprehension of what Marx regarding profit, profitability, fixed capital, turnover times and circulation.

Oh… and the issues are what they always have been:

What in fact does Marx say about the rate of profit, the tendency of the rate to decline, what are the causes of trends, tendencies in the rate of profit, what is the impact of those trends in the rate of profit on further accumulation of capital— AND does what Marx actually says explain the actual actions of classes, of the bourgeoisie, of the “motion of capital.”

But here’s a challenge– let’s pick and industry say petroleum extraction, and let’s look at the historical data as provided say in the US Federal Reporting System of the US Energy Information Agency.

I’ll provide my calculations of the rate of profit; and Boffy can provide his calculations of the rate of profit, say annually since 1965.

We’ll look at the mass of profits also. We’ll look at net property plant and equipment; we’ll look at capital spending; we’ll look at anything Boffy wants to look at, and we’ll see if the rate of profit exhibits steady improvement; if we have steadily increasing revenues; if we have steadily increasing capital expenditures; if we have everything Boffy says we should have– increasing turnover improving the actual profitability such that the rate of profit is always improving the more “c” expands.

Marx:

“But from the fact that capital posits every such limit as a barrier and hence gets IDEALLY beyond it, it does not by any means follow that it has REALLY overcome it, and since every such barrier contradicts its characters, its production moves in contradictions which are constantly overcome but just as constantly posited. Furthermore. The universality towards which it irresistibly strives encounters barriers in its own nature, which will, at a certain stage of its development, allow it to be recognized as being itself the greatest barrier to this tendency, and hence will drive towards its own suspension…”

“…The whole dispute as to whether OVERPRODUCTION is possible and necessary in capitalist production revolves around the point whether the process of the realization of capital WITHIN PRODUCTION [caps added-sa] directly posits its realization in circulation; whether its realization posited in the PRODUCTION process is its REAL REALIZATION…..Ricardo and his entire school never understood the really MODERN CRISES, in which this contradiction of capital discharges itself in great thunderstorms which increasingly threaten it as the foundation of society and production itself.”

–Grundrisse The Chapter on Capital Notebook 4 (Transition from the process of the production of capital into the process of circulation…..)

And there’s always this gem: “The higher the development of capital, the more it appears as a barrier to production– hence also to consumption–”

So we’ve refuted: value production being “natural,” universal; the law of value governing pre-capitalist (and post-capitalist) societies; that the barrier to capitalist accumulation and reproduction is somehow the limit to “use values” or its production of use values; that turnover, circulation, realization, automatically follows increased production of capital, commodities, of values.

Now as opposed to Boffy’s mythology of capital machinery, Marx says this: “Hence, the larger is the part of the capital consisting of the fixed capital–i.e. the more capital acts in the mode of production corresponding to it, with great employment of produced productive force- and the more durable the fixed capital is, i.e. the longer its reproduction time, the more its use value corresponds to its specific economic role- the more often must the part of capital which is determined as circulating REPEAT THE PERIOD OF ITS TURNOVER, AND THE LONGER IS THE TOTAL TIME THE CAPITAL REQUIRES FOR THE ACHIEVEMENT FOR ITS TOTAL CIRCULATION.

— –Grundrisse, The Chapter on Capital, Notebook 7 (Turnover time of capital…..)

Marx continues, as if anticipating the tub-thumpers of fictitious capital:

“This much clear, then, which already follows from the difference introduced by fixed capital into the industrial cycle, namely that IT ENGAGES THE PRODUCTION OF SUBSEQUENT YEARS, and just as it contributes to the creation of a large revenue, it anticipates future labour as a counter-value. The anticipation of future fruits of labour is therefore in now way a consequence of the state debt, etc., in short, not an invention of the credit system, It has ITS ROOTS IN THE SPECIFIC MODE OF REALIZATION, MODE OF TURNOVER, MODE OF REPRODUCTION OF FIXED CAPITAL.

That specific quality introduced with increasing fixed capital is– lengthening of the period of total turnover, of total realization.

Now, if the introduction of the increased component of fixed capital into the increasing component of constant capital, does not reduce the turnover period, but lengthens it; does not offset the decline in the “unit” rate of profit by increasing the annual rate of profit, where are we? We’re where we always are– with the relation between the living and dead components of capital determining profitability; with the contest between accumulation and devaluation; where accumulation produces devaluation. And this is where the decline in the rate of profit is NOT offset, and cannot be offset by an increase in the MASS of profit–

that point is the point where, with a declining rate of profit because of the amassed, stored, accumulated capital in its fixed assets, the ability to EXPAND the production of VALUE at an increment high enough to generate profit is IMPAIRED due to the high THRESHOLD COSTS FOR SUCH EXPANSION represented in the established industries themselves. Thus boutique auto producers can gain a hold, a fraction, in the market, and thus thus markets can be segment or “niched”; thus automakers accustomed to, organized around lower profit margins, as the Japanese automakers are can gain significant market share– with the support of MITI, or similar organizations;but the large auto makers established majors in their “home markets” are not generating profits quickly or massively enough to capture significantly greater shares of the established markets.

Hello. Mike, thanks for the post (check your email with one comment from me)

Henry, in some weeks I will translate my work on Argentina. May be that will help.

I recently update my profile with this paper on world rate of profit in the long term (is on evaluation in Cambridge Journal of Economics) and other paper on turnover speed (on evaluation on Capital & Class).

You can read them with my other jobs here: https://uba.academia.edu/EstebanMaito

ABOUT TURNOVER SPEED. My work that on Capital & Class is the first one with a real advance in the matter, also the first that compare turnover in four countries

Boffy mislead all the problem. The increase in turnover speed DOES NOT increase profitability in an automatic way. Per se of course yes. But the REAL conclusion of the increase in turnover speed has nothing to do with that meaning-less “mathematical excercise” he did, the REAL conclusion of that increase is that FIXED capital become even bigger related to CIRCULATING. Fixed capital that Boffy not even mentioned. Profitability seems about “margins over sales, with turnover adjustment”. Not even close.

In the paper I compare US, Netherlands, Japan and Chile, I estimate simple and annual surplus value rates, and value composition of capital adjusted by turnover. There are many interesting conclusions. Laborforce is cheaper in core countries than in Chile when we take variable capital and not wage bill, due to a higher turnover speed.

If we don´t take turnover speed, Chile seems to have a higher surplusvalue rate and a higher composition but it´s really the inverse.

Functional distribution changes too. Wages share are less in core countries when we take variable capital. I say there is a “turnover effect”, more annual turnovers multiply by a big number a lesser GDP proportion (the VC). In Chile, the opposite. You have a minor wage share but VC is higher because of turnover speed differentials.

At the end of the article you have an annex with all the data.

E.

Esteban,

“Boffy mislead all the problem. The increase in turnover speed DOES NOT increase profitability in an automatic way. Per se of course yes. But the REAL conclusion of the increase in turnover speed has nothing to do with that meaning-less “mathematical excercise” he did, the REAL conclusion of that increase is that FIXED capital become even bigger related to CIRCULATING. Fixed capital that Boffy not even mentioned. Profitability seems about “margins over sales, with turnover adjustment”. Not even close.”

1) But, Marx and Engels set out in Capital II, Chapters 15 and 16, and in Capital III Chapter 4, and in Capital III, Chapter 13, that an increase in the Rate of Turnover, DOES and MUST raise the annual profit, and it DOES result in a release of Capital. As they set out in Capital II, it is precisely the rise in social productivity which is behind the change in the Organic Composition of Capital, which brings about this same rise in the rate of turnover of Capital, and release of Capital.

It does so, because it reduces the working period, and thereby reduces the amount of productive-capital that has to be advanced. If the rate of surplus value even just remains the same, and so the quantity of surplus value produced remains the same, but the value of the advanced capital falls, for example, because productive-capital is advanced for 4 weeks rather than 5 weeks, then the annual rate of Profit MUST rise.

2) Fixed Capital, which I have mentioned plenty of times in discussing its relation to circulating capital, according to Marx FALLS not rises, in relation to the LAID-OUT circulating capital. That is why he discusses at length the reason that the value of wear and tear in the price of each commodity unit continually falls. It falls, because it brings about this same rise in social productivity. One machine replaces several previous machines, and each new machine processes a much greater quantity of circulating constant capital.

As Marx describes in Capital III, Chapter 6, the value of fixed capital tends to fall more rapidly than that of materials, ebcause the former is the product itself of the industrial process and benefits from the rise of productivity, but the latter are more frequently the product of natural processes, there values tend to fall in steps over the longer period, as new techniques are introduced, new lands opened to agriculture, new mines started, and new materials developed etc.

Fixed capital value rises relative to the circulating constant capital in respect of the advanced constant capital, precisely because of, and can only be because of a rise in the rate of turnover of capital. If one machine processes 10 times as much as some older machine, or one machine processes as much as 10 did previously, then the proportion of its value compared to the laid out circulating capital, MUST fall for the reasons Marx describes. Its only because the rise in productivity reduces the value of the advanced circulating constant, because the working period is shortened, that the fixed capital CAN rise in value proportionately to the circulating constant capital.

3) “In the paper I compare US, Netherlands, Japan and Chile, I estimate simple and annual surplus value rates, and value composition of capital adjusted by turnover. There are many interesting conclusions. Laborforce is cheaper in core countries than in Chile when we take variable capital and not wage bill, due to a higher turnover speed.

If we don´t take turnover speed, Chile seems to have a higher surplus value rate and a higher composition but it´s really the inverse.”

That is interesting, because that seems to confirm completely the point I was making!

Correction.

Point 1. line 3-4 should read, “that an increase in the Rate of Turnover, DOES and MUST raise the annual rate of profit”.

Boffy I said that turnover speed PER SE of course that YES, increase profitability, but from one year to another an increase or decrease may be compensated with an increase or decrease of variable capital and fixed capital..

“Fixed capital value rises relative to the circulating constant capital in respect of the advanced constant capital, precisely because of, and can only be because of a rise in the rate of turnover of capital”

WHAT? Don´t you know what PROFITS are? They can, and generally, MUST be used to investment.

Another great mislead. First Fixed, now Profits.

I will express the issue in my work terms and data

Netherlands (mill of Euros)

1973: FIXED.84.000 WAGES 47.000 VARIABLE CAPITAL 6000 TURNOVERS 8

2011: FIXED 1.000.000 WAGES 306.000 VARIABLE CAPITAL 22.000 TURNOVERS 13,5

2011 wages divided by 8 turnovers (1973) = 38.250

2011 wages divided by 13,5 turnovers (2011) = 22.000

Idle of circulating variable capital 1973-2011 = 16.250.

Increase in fixed capital 1973-2011 = 916.000

As I understand 16.250 is not equal to 916.000.

Esteban,

I don’t know what point you are trying to make here by giving the relation between the laid out and advanced fixed capital relative to the variable capital. I agree that the fixed capital rises relative to the variable capital on both measures!

The point above was the same point that Marx makes, which is that the value of Fixed Capital relative to the laid-out circulating CONSTANT capital tends to fall. It does so, for precisely the same reason as lies behind the tendency for the rate of profit to fall, as he makes clear – rising social productivity. It is precisely the contradictions that this process creates, which are the basis of one form of crises, as set out in Chapter 15.

But, even there, Marx describes the way that for prolonged periods, and particularly in certain industries, there is no technological change, and therefore, no basis for a change in the organic composition of capital, and so no basis for a tendency for the rate of profit to fall.

The increase in the proportion of fixed capital to circulating constant capital is driven, as Marx describes by technical innovation. Unless that technical innovation produces machines that are more productive than current machines, and which cost less than the paid portion of labour they replace, there is no reason Marx says for capital to introduce them. As he says no capitalist will introduce a machine that does not increase their profits.

But, the introduction of technically superior, i.e. more productive machines on this basis, devalues the existing capital stock via moral depreciation, which as Marx says is a powerful means itself of reversing the tendency of the rate of profit to fall – at least if you value productive capital as Marx does according to its current replacement cost, rather than its historical cost.

But, the consequence of introducing machines that are more productive in this way MUST be as Marx says, to reduce the value of fixed capital in relation to the value of the circulating constant capital it processes – that as Marx says is how you define the productivity of the machine!

A new machine that costs £1,000 and replaces an existing machine with a value of £1,000 is only more productive if the new machine processes more material than the older one in any given amount of time, i.e. if the new machine processes 2,000 kilos of material in a year, whereas the older one processes only 1,000 kilos, the new machine is twice as productive. But, if the price of the material remains constant, that means the value of the new machine falls in half compared to the laid out circulating constant capital compared to the older one.

That is why as part of this process, as Marx sets out in Chapter 15, the value of wear and tear transferred by fixed capital into the price of each commodity unit must fall. But, the other side of this, is that if this machine processes the same quantity of material in half the time, the working period for the capital is halved, so the rate of turnover for this capital is necessarily increased, as Marx sets out in Capital II, Chapter 15 and 16. If the turnover period was previously comprised of 4 weeks working period, and 2 weeks circulation time, the working period is now reduced to 2 weeks, giving a turnover period of 4, or an increase in the rate of turnover of a third.

The effect of this is two fold as Marx sets out in Capital II, and III. Firstly, advanced capital is released as a consequence of the reduction in the turnover period, which means this capital is available for additional accumulation. This additional capital can be used more or less entirely for investment in more of these new machines. If the turnover time is halved, whatever was laid out as circulating capital for 4 weeks, can now be laid out for two weeks, which means that twice the quantity of productive-capital (material and labour-power) can be bought during that period. Secondly, because more labour-power is now being employed as a result of the increase in the rate of turnover, even with the same rate of surplus value, more surplus value is being produced for a given quantity of advanced capital, so the rate of profit must rise.

That is the case with a single capital, but assuming similar effects on “many capitals”, it can be seen how this affects not just the working period, but also the circulation time in further raising the rate of turnover.

Those who have based their claims for the “Great Recession” on the idea of the tendency of he rate of profit to fall, have done so on the basis that the rate of profit has actually fallen or not rise since the 1980’s. In fact, on almost any metric, its clear that the rate of profit did rise from the mid 1980’s. So, the argument then fell back on the rather spurious idea that it never rose above its previous peaks. Spurious because if its rising its rising whatever its relation to some historical level.

But, taking into consideration the changes in the rate of turnover, its clear that even on this basis the claims don’t stand up. Taking into consideration the rise in the rate of turnover due to the rise in social productivity, its clear that the annual rate of profit is higher today than it was at its previous peak. Even if we assume that the rate of turnover increased not by the equivalent of the average rise of productivity of 2% p.a., I had suggested previously, but only posit a rise a sixth of that, so that instead of the rate of turnover of capital rising 3 fold in the last 60 years, it has only risen by 1/2, that would give a current rate of profit of around 30%, compared with the previous peak of around 27%.

Yet, if we look at the changes effected during that time its clear that the rise in the rate of turnover must be much greater than that. I’d suggest Estoban looks at some of the back issues of Capital and Class from the 1980’s and 1990’s, which detailed some of the changes brought about in production techniques during that time, which increased productivity by 100%! The introduction of robots, of non-linear continuous flow production systems, and forms of flexible specialisation, detailed in C&C of the time, illustrate how revolutions in production were effected that slashed the working period. Even “Just In Time”, affects not just the circulation period, but also the working period, because it reduces the size of the advanced productive-capital held in the form of a productive supply.

Finally, let me give another important way in which in terms of the total social capital, these changes have affected the rate of turnover, and rate of profit. Since the 1980’s there has been a huge shift from manufacturing industry to service industries. Suppose the average working period of manufacturing industry is 4 weeks, compare that with a service industry such as say McDonalds, or Stabucks, or a Cinema.

For a fast food restaurant, the circulating capital can pretty much be advanced daily. In fact, the variable capital for such production is advanced, and turned over, even before any wages are paid out, which rather makes a mockery of trying to calculate a rate of profit based on its historic cost, i.e. the variable capital has been advanced, and produced a profit, which has been returned before any price has even been paid for the labour-power that produced it!

The circulating constant capital in the form of burgers, baps etc. is advanced daily, and gets processed daily by the labour-power. The finished product is sold to consumers daily, and so the circulating capital is returned daily, and as cash can either be stored in petty cash or banked daily. If its payment by card, then due to revolutionised payment systems that have slashed circulation times, the money is in the firm’s bank account almost instantly.

In other words, the circulating capital is turned over here on a daily basis. Whereas the turnover time for manufacturing industry might have been 4 weeks on average (but choose your figure, because obviously a shipbuilder takes perhaps 2 years to turn over their circulating capital), or a rate of turnover of 12 times a year we now have a rate of turnover of 365!

As your own data show, such rises in the rate of turnover unavoidably increase the annual rate of profit, and bring about the release of significant amounts of capital for additional accumulation.

Just to respond to this comment”.

“WHAT? Don´t you know what PROFITS are? They can, and generally, MUST be used to investment.”

The investment of profits cannot explain the rise in the organic composition of capital, for the reason Marx sets out, i.e. for long periods, capital simply reinvests profits on the same technical basis. in the terms of the Regulation School is is a period of extensive rather than intensive accumulation.

If we have c 1000 + v 1000 + s 1000, and the s is wholly reinvested so that we have c 1500 + v1500, this accumulation will involved a proportionate increase in the quantity and value of fixed capital employed, but it will NOT bring about any change in the relation of fixed capita to circulating capital, or any change in the organic composition of capital arising therefrom, or, as Marx points out, therefore, any reason for the rate of profit to rise!

“Growth of capital, hence accumulation of capital, does not imply a fall in the rate of profit, unless it is accompanied by the aforementioned changes in the proportion of the organic constituents of capital. Now it so happens that in spite of the constant daily revolutions in the mode of production, now this and now that larger or smaller portion of the total capital continues to accumulate for certain periods on the basis of a given average proportion of those constituents, so that there is no organic change with its growth, and consequently no cause for a fall in the rate of profit. This constant expansion of capital, hence also an expansion of production, on the basis of the old method of production which goes quietly on while new methods are already being introduced at its side, is another reason, why the rate of profit does not decline as much as the total capital of society grows.”

Capital III, Chapter 15

The whole point about my comment, which you seem to have completely missed is that, as Marx says, the organic composition of capital, which creates the tendency for the rate of profit to fall REQUIRES that the proportion of fixed capital rises to the advanced circulating capital, because its only on that basis that more material gets processed by any given quantity of fixed capital and variable capital. But, that can ONLY occur on the basis that the replacement machine is more productive than the machine it replaces, i.e. there must have been technological advancement, which is the whole point Marx is making in the quote above.

But, if there has been such technological advancement, bringing with it moral depreciation etc., then say the new machine is twice as productive as the machine it replaces. It now produces the material required to meet the requirements of the working period in half the time, which means that the quantity and value of circulating capital advanced in 4 weeks is now advanced in 2 weeks. There is no change in the value of the advanced capital for the working period, but there are now twice as many working periods in a year, twice as much labour-power exploited in a year, and twice as much surplus value produced. So, the annual rate of profit measured against the advanced capital rather than the laid out capital doubles.

Moreover, you are wrong to believe that the replacement fixed capital could only come from a reinvestment of profits. Besides, the issue of credit, primary accumulation from secondary funds etc. which are really just a distraction, the fact is, of course, that each capital hoards money-capital as an equivalent for the value of wear and tear of its fixed capital returned to it via the circulation of its commodity-capital.

If any particular capital, at any one time, as Marx sets out in Capital II, there is going to be a sizeable proportion, is about to use its amortisation fund to replace such fixed capital, it will, of course do so to buy the latest version of machine, rather than simply replace its existing machine on a like for like basis. As the example of computer equipment indicates, not only will such replacement equipment be much more productive than the equipment being replaced, but frequently it will also be a lower value than that of the machine being replaced.

In other words, firms can frequently upgrade their equipment, not by any resort to their profits, but simply by resort to their amortisation fund, depending upon the stage in the replacement cycle, i.e. depending upon already having had the majority of the value of the original machine returned to them via the circulation of its commodity-capital, over several years.

By the way, my work is conservative. Variable capital is considered as an annual amount, but when the year ends capitalists don´t throw that capital as garbage, the SAME capital (few more, few less according to increase in employment) keeps playing that rol the next year. So positions like Boffy´s has a less argument too.

Now we come to Marx’s analysis of the rate of profit in the Grundrisse.

In Notebook 7, Marx says:

“Thus, in the same proportion as capital takes up a larger place as capital in the production process relative to immediate labour, i.e. the more the relative surplus value grows–the value-creating power of capital– the more DOES THE RATE OF PROFIT FALL. ….Hence the rate of profit falls relative to the total value of the capital presupposed to production–and of the part of capital acting as capital in production. The wider the existence already achieved by capital, the narrower the relation of newly created value to presupposed value (reproduced value). PRESUPPOSING EQUAL SURPLUS VALUE, I.E. EQUAL RELATION OF SURPLUS LABOUR AND NECESSARY LABOUR, there can therefore be an unequal profit, and it must be unequal relative to the size of the capitals. The rate of profit can rise although real surplus value falls. Indeed the capital can grow and the rate of profit can grow in the same relation if the relation of the part of the capital presupposed as value and existing in the form of raw material and fixed capital rises at an equal rate relative to the part of the capital exchanged for living labour. But this equality of rates presupposes growth of the capital without growth and development of the productive power of labour. One presupposition suspends the other. This contradicts the law of the development of capital, and especially of the development of fixed capital. Such progression can take place only at stages where the mode of production of capital is not yet adequate to it….”

First let’s keep in mind that all these movements of capital are cyclical, but that within the cycles, that with the repeated cycles, and trend is established, an overall structural movement based on the growing accumulation of capital

The movement of the rate of profit in synch with the growth of the fixed assets and raw materials is possible, but it is an “outlier”– it is a condition counter to the real domination of capital– where the productivity of labor does not grow, which means in fact, that the application of fixed assets to production is impeded in that wage is not reproduced in less time; the necessary labor is not reproduced. “This contradicts the law of the development of capital, and especially the development of fixed capital.”

Marx calls the various iterations of the decline in the rate of profit, or the changes in rates of profit in proportion or disproportion to the size of the capital the “most important law of modern political economy, and the most essential for understanding the most difficult relations. It is the most important law from the historical standpoint. It is a law which, despite its simplicity, has never been grasped and, even less, consciously articulated.”

Marx, of course, is about to consciously articulate the importance of the law: “hence it is evident that the material material productive power already present, already worked out, existing in the form of fixed capital, together with the population etc., in short all conditions of wealth, that the greatest conditions for the reproduction of wealth, i.e the abundant development of the social individual– that the development of the productive forces brought about by the historical development of capital itself, when it reaches a certain point, suspends the self-realization of capital, instead of positing it.”

Wow. Let’s continue:

“Beyond a certain point, the development of the powers of production becomes a barrier for capital”….. [ and let’s not lose sight what capital “means”– it means the expansion of value production, of the production of the means of production and subsistence as values to be exchanged with living labor; it means reproducing the capital relation and “materializing” that relation in greater accumulations]…. ; hence the capital relation a barrier for the development of the productive powers of labour. When it has reached this point, capital; i.e. wage labour enters into the same relations towards the development of social wealth….as the guild system, serfdom, slavery, and is necessarily stripped off as a fetter…. [Marx is just getting warmed up]… “the material and mental conditions of the negation of wage labour and of capital…are themselves results of its production process [see previous comments about the conflict between the labor process and the valuation process; between labor and conditions of labor].

“The growing incompatibility between the productive development of society and its hitherto existing relations of production expresses itself in better contradictions, crises, spasms. The violent destruction of capital not by relations external to it, but rather as a condition of its self-preservation, is the most striking form in which advice is given it to be gone….Since this decline of profit [NOTE: Marx does not distinguish rate from mass of profit here, the decline of one is the decline of the other] signifies the same as the decrease of immediate labour relative to the size of the objectified labour which it reproduces and newly posits, capital will attempt every means of checking the smallness of the relation of living labour to the size of the capital generally, hence also of the surplus value, if expressed as profit, relative to the presupposed capital by REDUCING THE ALLOTMENT MADE TO NECESSARY LABOUR AND BY STILL MORE EXPANDING THE QUANTITY OF SURPLUS LABOUR WITH REGARD TO THE WHOLE LABOUR EMPLOYED.”{caps added}

Well so much for big capital then being more inclined to “cut its capital costs” as Boffy would have us believe, rather than attack wages.

“These contradictions lead to explosions, crises, in which momentary suspension of labour and annihilation of a great portion of capital violently lead it back to the point where it is enable [to go on] fully employing its productive powers without committing suicide.”

So, I’ll pause here… with plenty of more from the Grundrisse still to come– not to mention the other economic manuscripts Marx wrote between 1857 and 1864, and from volume 3 itself.

One can, of course, disagree with Marx, argue that Marx was wrong… but what one cannot do is what Boffy does and pretend Marx is saying something about profit and profitability which he does not say and which he directly refutes.

Continuing with the Grundrisse, Marx writes regarding the transformation of surplus value into profit:

“The two immediate laws which this transformation…yields for us are these: (1) surplus value expressed as profit always appears as a smaller proportion that surplus value in its immediate reality actually amounts to.”

And

(2) “The second great law is that the rate of profit declines to the degree that capital has already appropriated living labour in the form of objectified labour, hence to the degree that labour is already capitalized and hence also acts increasingly in the form of fixed capital in the production process, or to the degree that the productive power of labour grows. The growth of the productive power of labour is identical in meaning with (a) the growth of the relative surplus value or of the relative surplus labour time which the worker gives to capital; (b)the decline of the labour time necessary for the reproduction of labour capacity; (c) the decline of the part of capital which exchanges at all for living labour relative to the parts of it which participate in the production process as objectified labour and as PRESUPPOSED VALUE (my caps). The profit rate is therefore inversely related to the growth of relative surplus value or of relative surplus labour, to the development of the powers of production, and to the magnitude of the capital employed as [constant] capital within production. In other words, the second law is the tendency of the profit rate to decline with the development of capital, both of its productive power and of the extent in which it has already posited itself as objectified value…”

And then Marx writes, regarding the accumulation of fixed capital:

“While it is the tendency of capital, on one side, to increase the total value of the fixed capital, [so], at the same time [is its tendency] to decrease the value of each of its fractional parts.”

Indeed, these are the economies in the purchase, use, and maintenance of fixed capital that every capitalist pursues.

Marx continues: “As soon as fixed capital enters into circulation as value, its use value or the capital realization process ceases, or, it enters into it only as the latter ceases. Hence, the more durable, the less it requires repair, total or partial reproduction, the longer its circulation time, the more does it act as productive power of labour, as capital i.e. as objectified labour, which posits living surplus labour. The durability of fixed capital, which is identical with the circulation time of its value, or with the time required for its reproduction arises from its concept itself as its value-moment…..”

The longer the circulation time… we get not only increases in circulating capital, but a lengthening of the total circulation time, the time necessary to achieve a complete “turnover” of the value fixed in the “sunk” assets.

In Chapter 4, Vol 3 of Capital, Marx writes on the effect of turnover on the rate of profit– turnover time is the fusion, the sum, of production time and circulation time; and since circulation time– the time it takes to transform the m to c to c+ to m+– represents the time from outlay until return– increased circulation time diminishes the mass of surplus value that can be extracted– the feeding back of the expanded value into production.

However in Marx’s discussion he carefully distinguishes and maintains the distinction between production time and circulation time and NOWHERE does he argue that a reduction in the production time due to increased applications of fixed capital, enhancing the extraction of relative surplus value automatically, inevitably, or of necessity MUST reduce the circulation of time. Nowhere does he argue that a reduction in production time IS a reduction in the time of circulation..e

Circulation time and production time are distinct components of turnover, or realization, and everything Marx wrote earlier about the application of greater values of fixed capital increasing the circulating time of that objectified value stands on its own.

Marx writes that “the main means of cutting circulation time has been improved communication”– no doubt about it– canals, railroads, telegraphs, telephones, high-speed trading– are part and parcel of the accumulation of capital. Reductions in circulation time can increase turnover and enhance the rate of profit. Yet there is no automatic improvement in turnover due to the reduction in production time.

In fact, improvements in productivity, reductions in production time, or increased output in the same time, can have exactly the opposite impact on rate of turnover for numerous reasons including if and when the means of circulation are inadequate to the required movement. We can see this going on right now where the increased output of “tight oil” from the Bakken field in North Dakota has led to incidents of rail congestion, “gluts” and trans-shipment points, shortages of locomotives, crews across rail networks impacting the turnover, not only of the shale oil commodity capital, but impairing the transport of grain in both Canada and the US.

The so-called “release of capital” is only a sometimes thing, and only rarely is expressed across the expanse of capitalist production.

Absolutely correct. In fact the decrease in production turnover generates a requirement to increase the rate of consumption, otherwise inventory carrying time and costs increase.

Now regarding Boffy’s interpretation of Marx’s analysis of the rate of profit being accompanied by an increase in the mass of profits…. Marx says in Vol 3 [“The Law Itself”] “Previous economists, not knowing how to explain the falling rate of profit, invoked the rising mass of profit, the growth in its absolute amount, whether for the individual capitalist or for the social capital as a whole, as a kind of consolation, but this was also based on mere commonplaces and imagined possibilities.” It’s almost as if Marx knew somebody like Boffy would be looking for a consolation prize.

[But we should note– Boffy is not just arguing that the decline in the rate of profitability for the social capital has been accompanied by an increase in the mass of profits– he is arguing that rates of profit have increased, and have increased spectacularly over-the-past-only-he-knows how many years. ]

How does Marx explain the increase mass of profits?– By a massive increase in capital deployed against, engaging, increased masses of wage-labor:

“When the percentage composition in the previous example was 60c + 40v, the surplus-value or profit on it was 40 and the rate of profit therefore 40 per cent. Let us assume that at this level of composition the total capital was 1 million. The total surplus-value and total profit would then amount to 400,000. If the composition were later to become 80c + 20v, the surplus- value or profit on each 100 would be 20 with the level of exploitation being the same. But the surplus-value or profit grows in its absolute mass, as we have shown, despite this decline in the rate of profit or the decline in the production of surplus-value by each capital of 100 and this growth might be from 400,000 to 440,000 say. THIS IS POSSIBLE ONLY IF THE TOTAL CAPITAL THAT CORRESPONDS TO THIS NEW COMPOSITION HAS GROWN TO 2,200,000 [my caps]. The mass of the total capital set in motion has risen to 220 percent of its initial value, whereas the rate of profit has fallen by 50 percent. If the capital had simply doubled, then at the rate of profit of 20 percent it could only have produced the same amount of surplus value and profit as the old capital of 1,000,000 did at 40 percent. Had it grown by less than this it would have produced less surplus value or profit than the capital of 1,000,000 did previously, although at its earlier composition this would only have had to grow from 1,000,000 to 1,100, 000 in order for its surplus value to rise from 400,000 to 440,000.”

“Here we can see asserting itself the law we developed earlier [ volume 1, chapter 25, 2] according to which the relative decline in the variable capital, and thus the development of the social productivity of labor, means that an ever greater amount of total capital is required in order to set the same quantity of labour-power in motion and to absorb the same amount of surplus labour…”

“A fall of 50 per cent in the rate of profit is a fall of a half. If the mass of profit is to remain the same therefore, the capital must double.”

And where does this massive increase in capital come from to generate the massive profits? Where can it come from? With the means of production organized as commodities, as values, it can only come from the expansion of value– from the mass of social profits themselves; it can only come from the expanded and/or intensified exploitation of labor-power. Hence the accumulation of capital sooner or later reaches a point where it must attempt to drive the wage below the value of labor-power, below its costs of reproduction. At its apotheosis, capital is nothing but primitive accumulation all over again.

The single most important thing to remember when reviewing Marx’s evaluation that the conditions that determine the tendency of rate of profit to decline are the conditions that accompany the increase in the mass of profits is– simply that in discussing the increase in the mass of profits, Marx is referring to the total social capital; he is analyzing the overall development of capital as a totality.

Consequently, the more capitalist production develops, the more capital accumulates, the more it reproduces itself, the more it engages wage labor, the greater the mass, and the lower the rate of profit. This is cold consolation, and no compensation for the capitalists, since the increment of the expansion of value– the rate of accumulation is the be all and end all of value production. As a consequence, the distribution of the mass becomes ever more critical– which is why Marx asserts that competition does not cause the rate of profit to decline; rather the decline in the rate of profit determines and intensifies competition.

Reblogged this on Econo Marx 21.

The problem with all these measures of the rate of profit is they are distorted by credit money. Prior to 1971 it could be argued that the link to gold placed some limit on the size of the distortions, so that long term trends can still be observed, but ever since fiat money there has been little to hold back the growth in credit money & so fictitious capital distorting recorded rates of profit. That’s not to deny there may well have been an increase in the so-called neo-liberal era, but we need to recognise that at the very least recorded profit rates have been artifically boosted.

Fiat money dates back long before 1971, and so does credit! In the Contribution to a Critique of Political Economy, Marx demonstrates how even gold coins, or silver coins are equally fiat money! he quotes Ben Franklin statement that in Britain silver sixpences whose silver content had been worn away significantly still circulated as though they have a value equal to their face value. They did so because they were a token representing that value, a token backed by the authority of the state that minted them.

Your idea that the link to Gold was somehow significant is the same mistake made by Ricardo, which stood behind the disastrous 1844 Bank Act. As Marx makes clear in Capital III, money is not a thing, it is a form of value, and value is labour. As Marx demonstrates in the “Contribution” provided the money tokens and credit in issue are not in excess of the value/labour-time they represent then such credit and fiat currency can act just as well as any other physical representation of the equivalent form of value.

But, similarly, as Marx describes in Theories of Surplus Value II, those who want to palce the responsibility for crises on credit are wide of the mark, and thereby divert attention away from the real cause, which is the fact that capitalism expands production of use values way in excess of the markets ability to absorb that quantity of those use values at any given time. An excess of those tokens does not change any of the underlying value relations, as Marx demonstrates, because all it does is to multiply each side of the value equation by the same number!

Once again, Boffy argues that somehow the mass of profits compensates the indivdual capitalists for the decline in the rate of profit. In fact, Boffy is arguing that the decline in the rate of profit is necessarily, inherently, compensated by the increase in the mass.