Japan’s GDP figure for Q4 2012 was out today. It showed that Japan’s economy unexpectedly shrank last quarter as falling exports and a business investment slump outweighed slightly improved consumption. GDP contracted an annualized 0.4%, following a revised 3.8% fall in the previous quarter. Business investment dropped 2.6% on the quarter, the fourth quarterly contraction in a row. Japan’s depression continues.

That’s why the newly elected right-wing government launched its great experiment in applying all Keynesian remedies at once – monetary and fiscal stimulus along with a very sharp depreciation of the currency against its major trading rivals. The fast devaluation of the yen has provoked objections from other major capitalist countries. The G7 meeting let it be leaked that it was not amused and considered that Japan was taking advantage. And last week, French president Francois Hollande also complained and showed concern about the relative appreciation of the euro hitting French export growth. So the Keynesian experiment in Japan is already causing worries elsewhere. But, more important, will the experiment work?

Noah Smith had a new post last week (http://noahpinionblog.blogspot.co.uk/2013/02/the-koizumi-years-macroeconomic-puzzle.html) in which he asked the question: what caused Japan’s growth speed-up from 2000-07? There is a good reason, at least for Smith, why he wants to know. That’s because the economic performance of Japan is a mystery to him and does not seem to fit any Keynesian explanations. You see, as Smith points out, during that period, Japan remained in a Keynesian ‘liquidity trap’ with interest rates near zero, while prices were deflating. According to Keynesian theory, Japan should have been in another decade of depression. But it was not really.

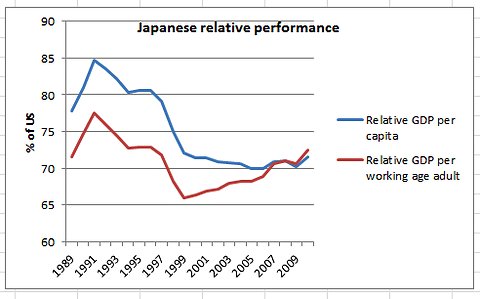

Instead, Japan picked up its growth rate in the 2000s compared to the ‘lost decade’ of the 1990s. Indeed, it partially reversed the decline in GDP per capita relative to the US that it experienced in the 1990s. This improvement has been highlighted also by Paul Krugman in his blog (http://krugman.blogs.nytimes.com/2013/02/09/japanese-relative-performance/). Smith trawled through the possible explanations of this relative recovery which took place during the so-called Koizumi era (‘neo-liberal’ regime of pro-capitalist Japanese PM, Jinichori Koizumi), again hardly fitting in with Keynesian policies.

The improvement was only relative. Real GDP growth averaged 4.6% between 1981-90 in the so-called ‘bubble’ years. The bubble was followed by a crash in the 1990s, and average growth dropped to just 0.7% a year between 1993-99 (I have excluded the slump years of 1991 and 1992). Then after the slump years of 1998 and 1999, annual average growth improved to 1.5% between 2000 and 2007. This was double the rate of the 1990s, if still way below the bubble 1980s years. In the last five years of the Long Depression, Japan’s economy has contracted by an average of 0.2% a year.

Smith notes that Japan continued to be in a Keynesian-style liquidity trap and in deflation throughout the 2000s. Also, the relative recovery cannot be explained by Keynesian-style fiscal stimulus, because government spending fell in both absolute terms and as a percentage of GDP , while budget deficits as a share of GDP also narrowed. As I have shown before, in the 1990s, in contrast, there was considerable extra government spending and rising budget deficits, but these Keynesian prescriptions failed to revive the Japanese economy. Then in the 2000s, there was fiscal austerity under Koizumi and yet economic growth was faster! Of course, part of this paradox is that poor growth in the 1990s meant that the ratio of government spending and deficits to GDP rose, but remember even in absolute terms, government spending and deficits rose – to little effect it seems.

The contribution from net exports did not seem to contribute much either in the 2000s. But Smith did note that bank lending ,which had collapsed in the 1990s when banks were deleveraging their debts from the bubble years, rose in the 2000s. I reckon this is significant and a lesson for the current depression in the major economies. But Smith is at a loss to explain this.

Indeed, he sums up his analysis of Japan in the 2000s as follows: “during the years of 2000-07, Japan grew quite quickly when measured properly (as GDP/working age population), substantially faster than the United States after accounting for demographics. However, during this entire time, it was stuck deep in a liquidity trap, with government spending decreasing and banks and companies deleveraging. Also, Japan did not experience a major improvement in its balance of trade, nor a large currency depreciation, nor an increase in inflation or inflation expectations. Additionally, Japanese services TFP remained flat. And he concludes: “I regularly say things like “Japan confounds macroeconomic analysis.” Now you know what I mean…”

Well, I had a little think about this ‘mystery’ from a Marxist point of view. If growth and investment picked up in the 2000s, then the main reason must be a recovery in profitability. And that’s exactly what the data show, as I portrayed in a recent post (https://thenextrecession.wordpress.com/2012/12/16/japan-election-lowest-turnout-since-records-began/). In that post, I explained how Japan’s rate of profit was held up during the 1980s by a massive credit and property boom. But that could not last. After the great credit bubble burst in 1989, the average rate of profit in the Japanese economy fell nearly 20% during the 1990s. But from 1998 to 2007, it rose nearly 30%. And we can analyse why, using Marxist categories. The organic composition of capital (the value of plant, equipments and raw materials relative to the cost of labour employed) fell for the first time since the second world war, while the rate of exploitation of the labour force rose nearly 25%. In other words, Japaneses devalaued its old assets, reduced the labour force and boosted profits per unit of labour. This was the classic way out for capitalist production – at the expense of labour.

And Japanese capital also devalued and ‘deleveraged’ much of the debt (fictitious capital) that it had built up during the bubble decade of the 1980s, when non-financial corporate debt rose nearly 25% as a share of GDP and household debt (financial and property) jumped by 37%. During the 1990s, the corporate sector deleveraged by 15%, laying the basis for profitability to recover.

We can see in the graph below that Japanese corporations had much higher debt levels (relative to GDP) compared to German, British and American corporations. But they began deleveraging that debt during the 1990s, with the bulk of that done by 2002. The opposite was happening in the other countries.

So I reckon the mystery of Japan’s economic recovery in the 2000s can be explained best in Marxist terms. Average real GDP growth came back (relatively) because Japanese capital had written off old capital enough, both tangible and fictitious, and banks were in better shape to lend again – of course at the expense of a lost decade of income and jobs for its population in the 1990s, culminating in the dire deflationary slump of 1998. The global slump of 2008-9 hit Japan hard, as much of its profitability and growth depend on world markets, as I showed in another post

(https://thenextrecession.wordpress.com/2013/02/06/japan-and-the-race-to-the-bottom/).

Why do we care what the reason was for Japan’s relative improvement in the 2000s? Well, it shows up the weakness of mainstream economics as it does not know why the 2000s were better and, in contrast, it shows the explanatory power of the Marxist analysis. It’s a mystery explained. And it will have lessons for the current ‘experiment’ in Keynesian polices by the right-wing Japanese government.

And that lesson could be learned in this current decade. Japan’s economic growth has been pretty much non-existent since the trough of the Great Recession and the current right-wing government is now throwing the kitchen sink of Keynesian policies at the problem. But the experiment will probably not last beyond the end of this year. Fiscal stimulus is supposed to end in 2014 when the sales tax is planned to increase to 8% and then 10% from October 2015 from the current 5%. By then, yen devaluation will be over and “monetary policy will probably be the only thing left to support the economy next year,” as Masaaki Kanno, chief economist at JPMorgan says. “The moment of truth for the recovery will probably come in fiscal 2014.”

And this time, not only does Japanese capital still have large debts and lower profitability, it also has a declining population. So the ability to generate more value and surplus value from the work force is limited by a contraction in labour supply. That means capital must exploit the workforce even more intensively or invest more in more in costly new technology to try and raise relative surplus value to boost profitability.

Keynesian policies in the 1990s did not work for Japan and they probably won’t work in this decade either. The 2010s will be the next ‘lost decade’.

I’d like to know how much breaking free of the US stranglehold on macro policy especially defence and international relations has to do with the ability of Japanese capital and its political mercenaries to take measures benefiting its profitability.

It really is too bad that Marx never got round to the volumes of Capital dealing with the state, trade, and the world market and crises, even though he was able to include a good deal in the volumes he did finish and indicate his approach in his other work.

The scientific worth of Marxism is fully proven in Capital, but the application and the political realization of Marxism as the core of the Idea of Socialism (to put it in Hegelian terms 😉 are aspects of our method of changing the world that are too often ignored. And the state and trade are prime examples of this. A lot of the conundrums relating to Japan and China would be a lot easier to deal with if these interactive factors were better understood.

“But from 1998 to 2007, it [ROP] rose nearly 30%. And we can analyse why, using Marxist categories. The organic composition of capital (the value of plant, equipments and raw materials relative to the cost of labour employed) fell for the first time since the second world war, while the rate of exploitation of the labour force rose nearly 25%. In other words, Japaneses devalaued its old assets, reduced the labour force and boosted profits per unit of labour.”

Owing to my patchy knowledge of Marxist terminology…if as you say the ‘organic composition of capital’ fell post 98 then doesn’t that mean that labour became a larger component of total expenditures on ‘plant-equipment-buildings and labour’?

Yet at the same time you say exploitation of labour rose by ‘nearly 25%’. Does this mean that falling wages /labour shedding occurred but that investment [plant, machinery etc] fell even faster?

Broadly yes.

Isn’t the reason Japan is faltering again due to insufficient demand in the world economy as a result to Austerity politics?

Also isn’t part of Marxist profit theory a recognition that initially a super profit is made by those with the competitive edge, i.e. more advanced technology before competition brings that back to normal? Could this explain Japan’s recent history? I don’t really see this aspect of Marxian profit theory in your analysis.

Edgar

Yes, clearly Japan as a major trading economy is affected by the weak growth in the rest of the G7. And undoubtedly, Japan’s big rise in the rate of profit after the WW2 was due to the factors that you suggest, but not its recent history.