The US GDP revised data for the third quarter of 2014 came out today. US economic growth was revised up from a 3.5% annual pace to 3.9%. The US economy had expanded at a 4.6% rate in the second quarter. So it has now experienced the two strongest back-to-back quarters of growth since the second half of 2003.

This was the fourth out of the past five quarters that the economy has expanded above a 3.5% pace, although bear in mind that the economy contracted during the first quarter after a ‘bad winter’. So year-on-year growth, a much better guide to the pace of expansion was up only 2.4% in Q3’2014, actually a slight slowdown from Q2 yoy growth of 2.6%.

Nevertheless, 2014 annual real GDP growth looks like reaching at least 2.4%, or slightly higher than the 2.3% recorded in 2013 – if still well below the long-term average of 3.3%, or even the average of 2.7% achieved between 2002 up to 2007, before the Great Recession.

Looking at the underlying data, the main driver of the slight acceleration in real GDP growth in 2014 so far has been business investment and state and local government spending – from a low base. In today’s data, the pace of annual growth in business investment was raised to 7.1% from a 5.5%. That sounds good and year on year growth in business investment reached 8.5% in the third quarter.

However, that may not last. What was also to be found in the revised data were the first figures for corporate profits in Q3. Corporate profit margins, the difference between what businesses charge per unit of production and their costs per unit, reached a record high, at 15.6%

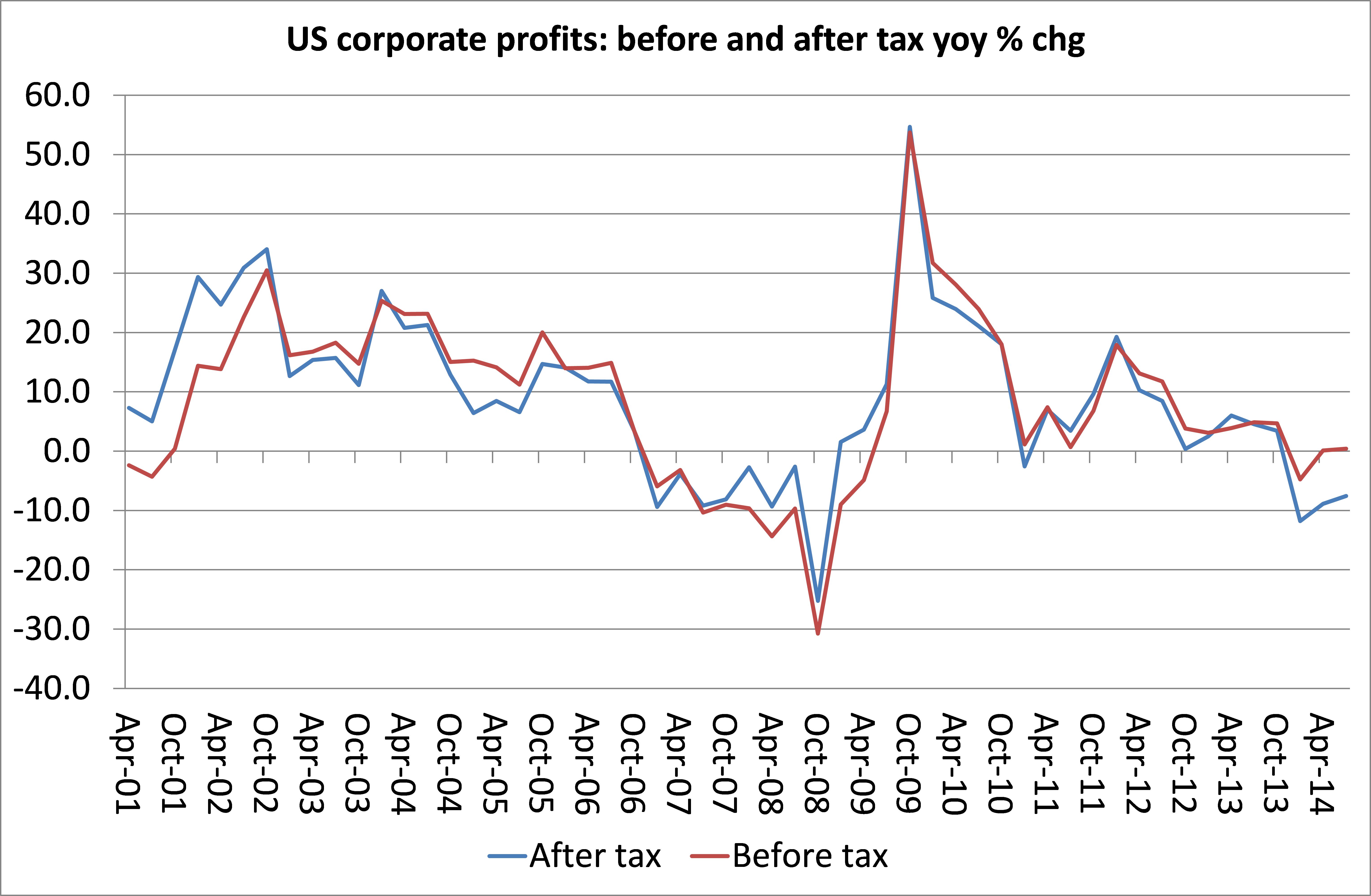

But corporate profits as a whole have virtually stopped rising, up only 0.4% year-on-year in Q3’2014, while after-tax profits are contracting and have been throughout the year.

It is my argument in previous posts and papers that where profits go, business investment will eventually follow and then economic growth and employment. The relatively strong US real GDP growth figures announced today are backward looking. Profits call the tune for the future and they are now stagnant (before tax) and falling (after tax). If we lag the change in business investment (blue line) by a year behind the change in profits (red line), then it looks like this.

The graph suggests that business investment growth is likely to contract and disappear during 2015, if corporate profits stay stagnant or contract further.

GDP growth is definitely a lagging indicator. We should wait and see what happens to corporate profits in the year ahead. Only then we can have an answer.

“This was the fourth out of the past five quarters that the economy has expanded above a 3.5% pace, although bear in mind that the economy contracted during the first quarter after a ‘bad winter’. So year-on-year growth, a much better guide to the pace of expansion was up only 2.4% in Q3’2014, actually a slight slowdown from Q2 yoy growth of 2.6%.”

I don’t think a statistician would agree with that conclusion. Looking at the data, it seems fairly clear that the Q1 data was a rogue number that has had a grossly exaggerated effect on the annual figure. However, even a 2.4% annual figure is considerably ahead of your analysis a few months ago that the US economy was only growing at 1.7%!

Moreover, the latest Philly Fed data show economic activity at level not seen since 1993, and the doubling of the index is pretty much unprecedented. If its correct, and with such a large number there is every possibility it too could be a rogue number, it would imply a 4th quarter growth figure of 6.5%, which would raise the annual figure considerably.

We should bear in mind this growth is in the face of the effects of the sequester, which has taken out a sizeable chunk of planned state spending.

“Looking at the underlying data, the main driver of the slight acceleration in real GDP growth in 2014 so far has been business investment and state and local government spending – from a low base. In today’s data, the pace of annual growth in business investment was raised to 7.1% from a 5.5%. That sounds good and year on year growth in business investment reached 8.5% in the third quarter.”

Which seems to contradict your argument put forward in previous posts that growth has been low because of lack of investment, which was due to low profits. There is undoubtedly a relation between profits and investment, but its not as mechanical as you seem to suggest.

As Marx points out, if there is a big crisis, such as happened in 2008, this causes a sharp drop in profits, and that undoubtedly then impacts investment in the immediate aftermath. Marx talks about this in terms of a lack of confidence by capital in the aftermath of the crisis, and refers to it as a “paralysis”.

Similarly, if profits shoot up extremely sharply, this will cause a rise in investment, as firms expand their production within their existing capabilities, and new firms are encouraged to set up. But, as Marx pointed out in contrast to Ricardo, even where profits are not rising rapidly, or even where they are falling, providing they are not crashing, capital will continue to invest and accumulate because that is its nature.

The extent to which it expands, however, will then depend on the extent to which it considers it can meet the requirements of anticipated demand.

I’m also not sure how you arrive at this conclusion,

“Profits call the tune for the future and they are now stagnant (before tax) and falling (after tax).”

According to MSN Money 81% of S&P 500 companies are beating their profits expectations, and profits are rising at a faster pace than for 4 years.

Confronting this article with the last you wrote about QE failure (https://thenextrecession.wordpress.com/2014/11/02/the-story-of-qe-and-the-recovery/), I try hard to understand why private and business investment can be so high, as you write in this article.

In that regarding the QE you wrote that: “The contribution to the growth figure from private consumption fell from 1.75% pts to 1.22% pts, or from 38% of total growth in Q2 to 35% in Q3. The contribution from business investment fell from 1.45% pts to 0.74% pts, or from 32% of total growth to just 21%.”.

How is it possible this change in a so quick time?

Many thanks in advance for your clarification.

Best regards,

Rumi

I haven’t read the other posts alluded to above. (“It is my argument in previous posts and papers that where profits go, business investment will eventually follow”) So I’m left wondering whether corporate profits and (lagged) business investment aren’t co-variant and a third variable (or more) better explains things. For example, what would be the correlation between these variables and capacity utilization and/or with GDP growth?

On the surface, it seems reasonable to expect increased business investment to follow increased profits, but upon further reflection that’s a dubious notion. If profits are growing because of pricing power while capacity is not strained, there is no need for investment. On the other hand weak profit growth would not prevent a business owner from investing if profits are satisfactory on a marginal investment opportunity.

These are all possibilities. And capacity utilisation is below average in most economies. Profits are up because labour costs have been squeezed. So investment has not been so ‘necessary’ as you say. Still, where profits have risen, as in the US, investment has followed. But pricing power has not been great though and there is a limit to reducing wage costs. And profitability remains relatively poor compared to history. And US corporate profit growth has now slowed. There does seem to be a good correlation between profits and investment, and as a result, quite good one with real GDP growth too. But capacity utilisation is undoubtedly a factor (perhaps in the length of the lagging effect), It’s an issue for more research.

Did you really mean to write “…profitability remains relatively poor compared to history”? Every measure I’ve seen indicates very high profits relative to history. Your margin chart shows it. As a share of GNP, profits are way above the (reliably mean-reverting) series average.

Also, it would be worth specifying whether your business investment figure is gross or net. Gross investment includes investments made to account for depreciation, which runs at roughly 10% of GDP. Net new investment includes only investments above that required to maintain capacity and capability (depreciation effect). Profit growth certainly would not be expected to correlate with the portion of gross investment directed at depreciation. (A sharp decline in the absolute level of profits could negatively impact that, which would result in shrinking capacity.)

Profits are not the same as profitability of capital. Rising profits as a share of GDP do not translate necessarily into a rising rate of profit. A rising and high share of profits in GNP is an indicator of a high rate of surplus value in Marxist terms, and that is clearly the case. But that is not the same as the rate of profit.

According to most (but not all) estimates of the US rate of profit, the US ROP in the 2000s is well below where it was in the 1960s and still below where it was in the late 1990s – although this is debated. See my post https://thenextrecession.wordpress.com/2013/12/19/the-us-rate-of-profit-extending-the-debate/. Indeed, I suggest you read all many posts on measuring the rate of profit so you can make up your own mind on this.

Estimates of the US rate of profit usually use the net fixed assets tables of the BEA which take into account depreciation and the BEA tables for profits can be depreciated accordingly. There is a big debate about whether to use historic or current cost measures of net fixed assets and profits.

Investment is a flow and not the same as the stock of assets. I did a calculation of the correlation between net business investment and corporate profits after depreciation and found a positive .63 correlation – pretty high. Can I also refer you to papers by Andrew Kliman on this issue

Click to access why_financialization_hasnt_depressed_u.s._productive_investment.pdf

and the statistical work by Jose Tapia Granados

Statistical evidence of falling profits as a cause of recession: A short note

Citation: Tapia Granados, J. A., “Statistical Evidence of Falling Profits as Cause of Recession: A Short Note.” Review of Radical Political Economics. Published online 3 February 2012, DOI: 10.1177/0486613411434397