Stock markets rallied in November as inflation rates subsided a little and the US Federal Reserve began to talk of lower interest-rate hikes from hereon. Financial investors are hoping that the Fed is set to ‘pivot’ from tightening monetary policy (i.e. reversing its policy interest rate hikes and stopping selling back its stock of government bonds to reduce liquidity).

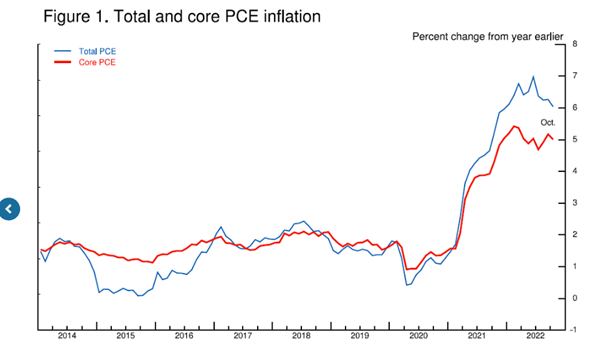

But financial markets are probably getting ahead of themselves. That was made clear by speeches from both the head of the Fed, Jay Powell and the head of the ECB, Christine Lagarde. Both said that they were determined to crush inflation until it returned to their target rates of 2% a year. In a speech last week Powell summed up his policy in the ‘battle against inflation’. He noted that the 12-month personal consumption expenditures (PCE) inflation rate – the inflation measure that the Fed mostly follows – was still at 6%. And stripping out energy and food prices, the core rate was still around 5%, with no indication of any significant fall ahead.

Powell again spelt out the Fed strategy. Ignoring the fact that it was weak supply (blockages in transport, insufficient skilled staff and low productivity) that has been the main cause of the spike in post-pandemic inflation, Powell continued to argue that hiking interest rates would slow aggregate demand and that would bring inflation down as households and businesses reduced spending growth in the face of rising interest costs on borrowing. But this approach could only mean intensifying the hit to the supply side too – in other words, driving the US economy into a slump. As Powell admitted in his speech, “Slowing demand growth should allow supply to catch up with demand and restore the balance that will yield stable prices over time. Restoring that balance is likely to require a sustained period of below-trend growth.” The words “below trend” mean recession and rising unemployment.

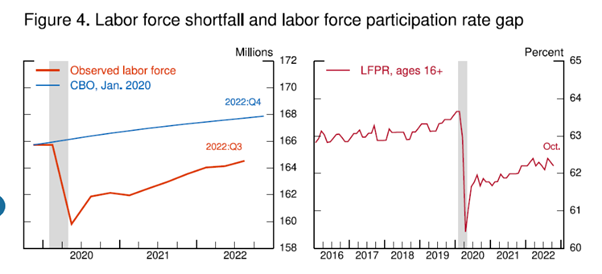

The latest headline employment figures for the US suggested that the labour market, as mainstream economists like to call it, was still pretty tight, as net new jobs in November were much higher than forecast. But rate of monthly jobs gains has been falling since last April. And Powell had to admit in his speech that employment was still millions below its level on the eve of the pandemic. “Looking back, we can see that a significant and persistent labor supply shortfall opened up during the pandemic—a shortfall that appears unlikely to fully close anytime soon.” Comparing the current labour force with the Congressional Budget Office’s pre-pandemic forecast of labour force growth reveals a shortfall of roughly 3.5m Americans.

So it’s not so much a ‘tight’ labour market caused by strong demand for labour, but instead caused by a large number of working age people not returning to the ‘labour market’. Some of the ‘participation gap’ reflects workers who are still out of the labour force because they are sick with COVID-19 or continue to suffer lingering symptoms from previous COVID infections (“long COVID”). But according to Powell, recent research by Fed economists found that the participation gap is now mostly due to excess retirements ie, retirements in excess of what would have been expected from population aging alone. These excess retirements account for more than 2m of the 3.5m shortfall.

But health issues have played a role. Many older workers lost their jobs in the early stages of the pandemic, when layoffs were historically high. The cost of finding new employment may have appeared particularly large for these workers, given pandemic-related disruptions to the work environment and health concerns. The combination of a plunge in net immigration and a surge in deaths during the pandemic probably accounts for about 1.5m missing workers.

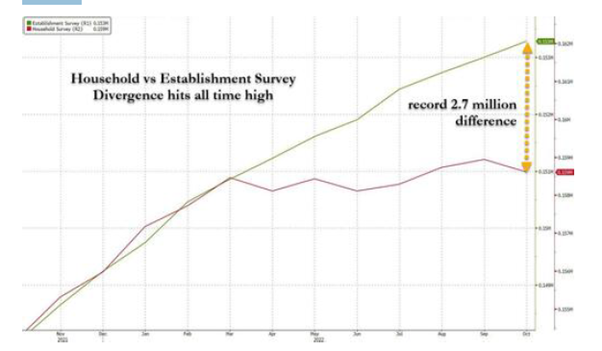

Moreover, there is a weird discrepancy between the jobs increases measured by the so-called establishment survey and the household survey, the latter asking people if they have a job or not. According to the establishment survey, there has been an increase of 2.7m jobs since last March. But according to the household survey, the increase is just 12,000! Something wrong here.

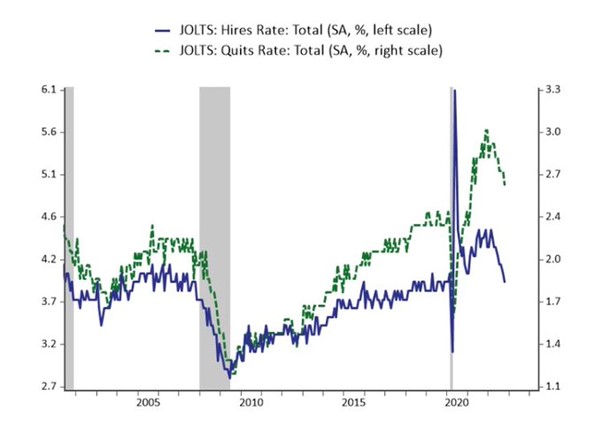

And when we look at other employment surveys, like the so-called ADP measure of private sector employment, we find that there was a fall of 100k jobs in manufacturing and construction in November, while the official establishment survey claims an increase of 35k. Moreover, the new jobs are mostly part-time. Since last March the US has lost 398K full-time employees offset by a modest gain of 190K part-time employees, while a whopping 291k workers were forced to get more than one job over the same period. So there has been no change in the number of people actually employed in the past eight months, but due to the deterioration in the economy, more people are losing their higher-paying, full-time jobs and being forced into much lower-paying work. Another measure of the jobs market is the JOLTS data on hiring and firing. They point to a rapidly cooling labour market too: both job hiring and quitting rates are now falling.

So it’s not wage push in tight labour markets that is driving inflation and it is not ‘excessive demand’ either by households or businesses spending. It remains a supply problem, particularly in energy and food. As a result, the Fed’s policy of determined rate hikes will have little effect on inflation rates. Instead by driving up costs of credit, the economy will topple over and inflation will eventually subside and be replaced by higher unemployment and bankruptcies. Remember what arch-monetarist Paul Volcker said when he was asked whether ‘shock therapy’ hikes in interest rates that he applied as Fed chair in the late 1970s would work. Volcker replied: “yes, through bankruptcies”.

I have shown in previous posts that inflation is primarily a supply-side story ie the failure of capitalist production to respond to the opening-up of economies after the pandemic slump. That is why the monetarist solution of rate hikes and tighter monetary policy and the Keynesian solution of wage restraint will have little effect on inflation – until recession comes.

Let me add some support for this supply-side argument from the horse’s mouth, as it were. Philip Lane of the ECB published a detailed analysis of inflation last week. That analysis shows that it is rising non-labour input costs and higher profit markups that have generated accelerating inflation in food, goods and services sectors over 2021-2022. “It seems clear that both the energy shock and the pandemic cycle (at both domestic and global levels) have exerted upward pressure on input costs and, in some categories, also facilitated an increase in markups.” So it’s raw material costs and profit mark-ups.

And any improvement in inflation rates in the last two months has been due to some subsidence in supply bottle-necks and in energy and food prices. In a new report, some American heterodox economists conclude that inflation rises have been concentrated in some key ‘systemic’ sectors like energy, food and housing. And these sectors are price-inelastic when it comes to interest-rate hikes. “We argue that in times of overlapping emergencies, economic stabilization needs to go beyond monetary policy and requires institutions and policies that can target these systemically significant sectors.”

Meanwhile, real wages in the Eurozone continue to plunge.

In posts during the pandemic slump, I argued that economies may well suffer permanent ‘scarring’ from the collapse in production and investment in a slump even deeper and more widespread than the Great Recession of 2008-9, if lasting less in time. Just like ‘long COVID’ has affected the lives of millions since the end of the pandemic, so has the pandemic slump weakened capitalist accumulation and productivity growth to new lows. As another Fed member, Lisa Cook pointed out, “over the first three quarters of 2022, productivity in the business sector has recorded a disappointing decline of 3¾ percent at an annual rate. Payroll employment in the private sector has continued to increase, yet gross domestic product (GDP) has done little more than move sideways, resulting in an outright decline in labor productivity.”

And another Fed member Brainard is concerned that this low productivity, high inflation scenario will continue despite the monetary efforts of the Fed: “it is the relative inelasticity of supply in key sectors that most clearly distinguishes the pandemic- and war-affected period of the past three years from the preceding 30 years of the Great Moderation…a combination of forces—the deglobalization of supply chains, the higher frequency and severity of climate disruptions, and demographic shifts—could lead to a period of lower supply elasticity and greater inflation volatility.”

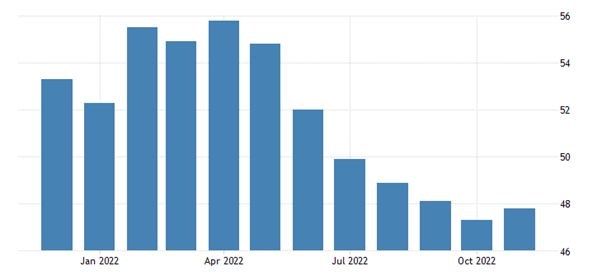

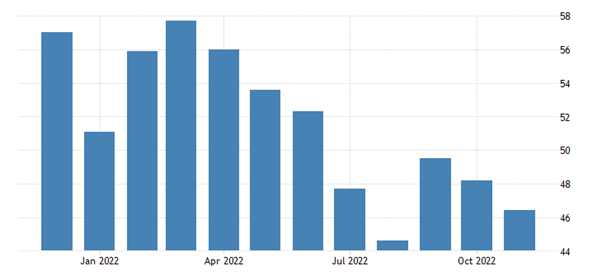

Indeed, the world economy is not only not returning to the pre-pandemic trends in real GDP growth, investment and employment (which were weak enough), but worse, it is heading into a new slump. The business activity indexes (PMIs) in most of the major economies are at ‘contraction’ levels (ie under 50).

Eurozone PMI and US PMI

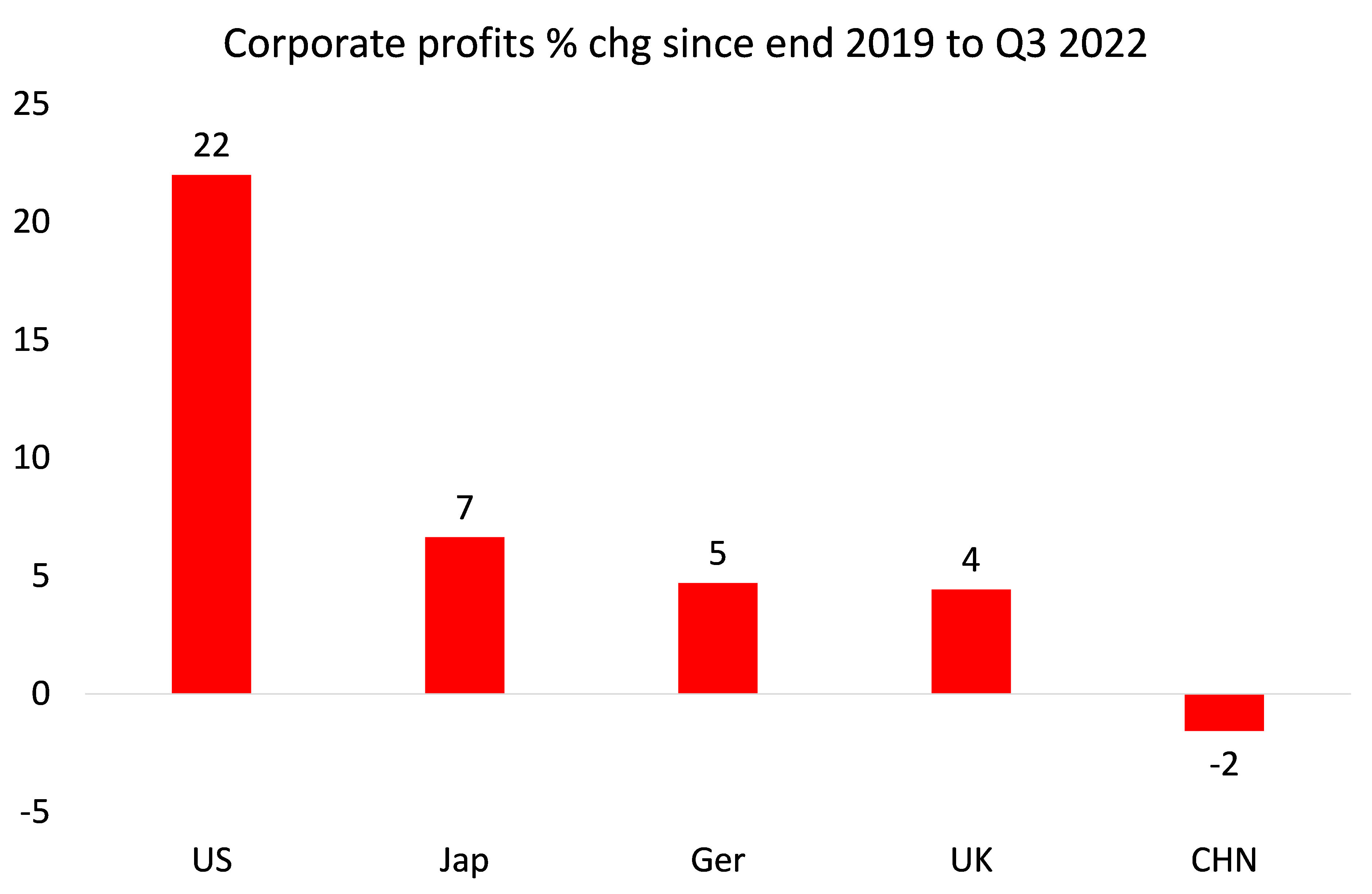

Corporate profits in the major economies are now heading south for the first time since 2016 – in an environment where the cost of borrowing is rising fast (mortgage rates, bond yields, loan charges etc). Global corporate profit growth has slowed to just 4.5% yoy in Q3 2022. US corporate profits have risen by far the most since the start of the pandemic to date (up 22%), but they peaked in the middle of this year and fell absolutely for the first time in the latest quarter. Japan, Germany and the UK corporate profits have risen no more than 4-7% over the same period, while China’s enterprise profits are now lower than at the end of 2019. Indeed, Japanese and German corporate profits are down nearly 15% this year to date, while the UK’s are stagnant.

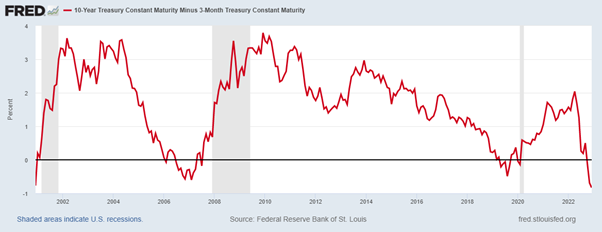

One of the most reliable indicators of an oncoming recession is the so-called inverted bond yield curve. That’s where the rate of interest on long-term bonds (ten-years) falls below the rate of interest on short-term loans (3 months or 2 years). That should not happen if an economy is growing ‘normally’. Then the interest charged on long term bonds would be higher because you get the loan for a longer time. The yield curve inverts only when central banks raise short-term interest rates and investors rush to buy long term bonds because they fear a recession coming.

Well, the US yield curve remains strongly inverted.

again I find the wealth of information you provide extremely useful

E questo professore? Lei é a conoscenza di questo? “La produzione globale di greggio convenzionale ha raggiunto il picco nel 2008 a 69,5 mb/g e da allora è sceso di circa 2,5 mb/g.” Pagina 45 del World Energy Outlook 2018 dell’Agenzia internazionale dell’energia.

Topical post given the collapse of smaller trucking firms in the US, trucker-drivers handing back keys, container ship sailings blanked, trans-pacific freight rates fallen from $20,000 to $2,000 while dozens of new container ships sit on slipways, tens of new chip factories being built which may as well be turned into indoor go-kart tracks, but one thing is still pending, large scale financial ructions. Why? Covid funds and cheap money improved liquidity in these zombie firms. But here is the rub, these firms increased their liquidity but at the expense of adding more debt. They bought time but at the cost of a bigger bust when they go down. That is the key observation.

There may have been a different reason why the stock markets in the West rose:

Chinese stocks, yuan stage powerful rally amid upturn in economic expectations > https://www.globaltimes.cn/page/202212/1281166.shtml

(begins quote) “Chinese assets staged a powerful rally on Monday, with the flagship Shanghai Composite Index regaining the 3,200 level last seen in mid-September, and the yuan strengthening past the psychologically important level of 7 per US dollar.

The strong comeback, buoyed by a supportive monetary policy and a flurry of moves across the country to optimize COVID-19 prevention and control measures, is indicative of an upturn in economic expectations and the rising appeal of yuan assets, market watchers said, predicting a continued revival in investor sentiment.

China still has ample leeway in its monetary policy, they stressed, calling attention to a coordinated macroeconomic push to ready the economy for potential headwinds amid an estimated global recession next year” (ends quote)

This confirms my suspicions that the West was pressuring China to abandon its Zero Covid policy and open up suddenly, accepting the millions of deaths, in order to prop up their own economies.

The West has a conspiracy theory, dominant since the break out of this pandemic, that states that the economy is in a new slump because China is containing is restricting its factories and circulation of goods through its pandemic containment policies (i.e. Zero Covid). If China “lets it rip”, then the global economy will immediately recover, according to them.

If that’s what they’re counting on, they’re setting up themselves for disappointment.

First, because China didn’t abandon Zero Covid: from the very beginning, since the first white paper released (July 2020), the CPC has made it clear Zero Covid was adaptable and would change as the situation changed. It is irrelevant if those last changes were triggered by the protests in Shanghai or not, because Marxism doesn’t separate economy from politics. In fact it was not even the protests by the rich kids from Shanghai that gave the feedback, but the protest from the workers of the Foxconn, who had to sleep on the factory’s floor because of a positive case, which triggered an automatic lockdown protocol.

Second, the West is truly declining, and there’s no coming back. China has already realized that and created the Dual Circulation policy, which will emphasize domestic consumption. To top it off, Russia is set to orient itself permanently to the East, and is already building its Far Asian gas pipeline infrastructure. As France President Emanuel Macron correctly stated, the era of abundance [of the First World] is over.

Please excuse? Though for some reason it is deemed unpleasant (or crackpot?) to talk about political issue in regard to the Fed, it seems to me that this is really unavoidable.

First, everything Powell and others say about inflation is political cover. The plan is to attack wages, inflation is the excuse. It is a very popular excuse as inflation is successfully sold as the worst possible threat to the consumer (the category preferred to “workers” or worse, “bourgeoisie.”) But the goal is to restore profit rates in the long run by lowering labor costs.

Second, the reason this return to Andrew Mellon-style liquidationism is prompted by a deep and fundamental shift in the politics of the haute bourgeoisie. In politics, this is shown by the emergence of Trump. But Trump is as they say a symptom not a cause and there’s more where he came from.

Third, the narrow partisan interest in attacking Biden, who has been universally rejected by the bourgeois media since the defeat in Afghanistan paints Biden personally as responsible for US inflation, even though it is a worldwide problem. Biden is a conservative Democrat who strongly believes in Band-Aids for social problems. The rightward turning bourgeois is deeply offended by this “socialism.” A few billion here for that problem, a few billion there for this problem, and you start talking about some real money, at least as far as they are concerned. Thus, much of Powell’s rigid stance against “inflation” is a partisan move against Biden and the Democrats generally who haven’t quite shaken off completely their supposed commitment to the New Deal. It was meant to foster the Red tsunami.

Fourth, Powell’s “pivot” is prompted by the fact that despite the best efforts of the media and push polls and the whole panoply of bourgeois manipulations, the Red tsunami didn’t materialize. Thus it’s prudent to pretend to moderation while assessing the new political situation. But overall the plan to crush the economy temporarily to hurt the workers is pretty much on track.

Or so I see it. Again, sorry to be offensive.

Hi Michael, I just wanted to really thank you doing public your analysis and interpretations.

Each post it´s an amazing teaching lecture.

Juan Martín

(from Argentina)

Juan Martin Thanks for the support – it’s the purpose of the blog to educate (including myself).

The Fed says that they are raising interest rates to fight off inflation. But in reality they are compelled to raise rates for a different reason that they aren’t aware of, given that they are not educated in Marxist economics. That being the overproduction of non-money commodities relative to the money commodity (gold). During such periods of overproduction, profits of capitalists are threatened. So while dollar profits may soar, golden profits are wiped out. In the final analysis, this is the only thing that counts. Do resolve overproduction within the confines of capitalism, central banks must allow interest to rise to the level that meets the supply and demand for gold, causing a collapse in dollar profits and the further centralization of capital through bankruptcies. It is through the crisis that the credit system gets replaced with a cash system. However, due to cumulative overproduction over the past several industrial cycles caused by the phenomenon of Financialization, a severe crisis would be necessary to fully transform the credit system back to a cash system. It is through this mechanism that the productive forces are brought back in line with the tolerable limits imposed by the capitalist mode of production.

MJ’s greatest pivot is in Beat It where strut became popular. Jackson loves to pivot, same as in Janet. In the end John Travolta is John Travolta and it doesn’t make him different from Kevin Spacey or Rock Hudson. It is wishful thinking to think Will Smith is no different from these backyard experts.