Last Thursday the $1.3tn cryptocurrency industry was hit heavily when ‘stablecoin’ Tether — a critical cog in the crypto market — briefly failed to maintain its link with the US dollar. A stablecoin is a crypto currency coin that is tied to an existing fiat currency, namely the US dollar, making it easy to switch (if expensively) between a crypto currency like bitcoin and an official currency like the dollar. Stablecoins are supposed to track real-world currencies and so play a central role in the stability of the broader crypto market by providing traders with a safe place to park their cash between making bets on volatile digital coins.

But last week that one-to-one parity between Tether and the US dollar was broken and Tether’s price in dollar’s fell, if only briefly to 96c.

A fundamental issue for all stablecoins is their resilience to conventional speculative attacks, analogous to attacks on fixed exchange rates. Tether’s accounts show that their cash reserves to back the dollar peg are only 4%, with most of the rest in risky dollar commercial paper. JP Morgan recently reported that the Tether stablecoin has no regulatory supervision or deposit insurance. So if people were unwilling or unable to use Tether tokens, “the most likely result would be a severe liquidity shock to the broader cryptocurrency market,” which could lead to everyone trying to sell at once.

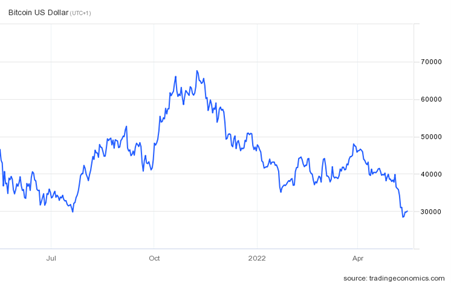

Tether’s wobble happened at the same time that the cryptocurrency market took a huge dive along with other speculative financial assets, like stocks and bonds, in what investors and traders now call a ‘bear market’. This proved, once again, that cryptocurrencies are not money, but just another form of speculative financial asset that will suffer when investment bubbles start to burst.

Tether is the biggest operator in the $180bn stablecoin market. There are 80bn Tether tokens in circulation, meaning it should hold $80bn in assets — a sum that compares with the biggest hedge funds in the world. But details around how those reserves are managed are scant, and not subject to audits under internationally recognised accounting standards. Last year, the US Commodity Futures Trading Commission fined Tether $41mn, claiming the company made “untrue or misleading” statements about its reserves.

The crypto crash was further amplified by another cryptocurrency, TerraUSD. It crashed in price against the dollar by 98%! Terra also calls itself a stablecoin, but it has little in common with Tether besides the goal of being worth $1. Instead of being backed by dollar assets, it is an “algorithmic stablecoin”, where its value against the dollar is determined by ‘decentralised’ decisions made by participants. Its value thus depends not on any dollar-based assets backing the stablecoin, as supposedly with Tether, but purely on the trust taken by the holders of Terra that it is equivalent to a dollar!

This is in effect a ‘Ponzi scheme’ where the value of the assets depends on enough people prepared to keep buying it when others want to sell and not on any underlying value of any commodity backing it. As one observer put it, “this seems like a house of cards because it is. The system relies on an active market, which in turn requires traders to believe they won’t get stuck holding the bag. If everyone sours on TerraUSD at once, the whole thing crumbles.” And it did.

All this proves what I have argued in previous posts. Bitcoin and other cryptocurrencies are no nearer universal acceptance as money than when they first came on the scene. They remain part of speculative digital finance. They will not replace fiat currencies, where the supply is controlled by central banks and governments as the main means of exchange. They will remain on the micro-periphery of the spectrum of digital moneys, just as Esperanto has done as a universal global language against the might of imperialist English, Spanish and Chinese languages.

In the meantime, the crypto mining industry uses huge amounts of energy in the ‘mining’ of these currencies as computer assemblies needed for crypto mining now consume 0.55% of global energy production – about as much as a small country. All the hype associated with crypto obscures the fact that it is using millions of tons of coal, copper, rare earth metals and plastic. China effectively banned the mining and use of cryptocurrencies in late 2021 because mining was consuming so much energy and because of the speculative risks associated with crypto.

These big falls in crypto prices have exposed the failure of some emerging countries’ attempts to raise funds by launching national crypto currencies and by issuing crypto-currency government bonds. Take the El Salvador experiment. Three economists — Diana Van Patten of Yale, Fernando Alvarez of the University of Chicago and David Argente of Penn State — have recently published a study of bitcoin adoption in El Salvador. Their findings, based on a representative in-person poll of 1,800 Salvadoreans, suggest that outside of young, educated, tech-savvy men, durable interest in bitcoin has not materialised.

The Salvador government has offered all kinds of incentives to citizens to use crypto ‘chivo’ over the US dollar, which is in short supply: a $30 installation bonus, paid in bitcoin, worth 8 per cent of the monthly minimum wage; a discount at the country’s biggest petrol stations, only for chivo users; a 150mn national fund to subsidise bitcoin-related fees; a rollout of 200 bitcoin ATMs in El Salvador and 50 more in America; legal tender status, so firms are required to accept the crypto currency and taxes can be paid in bitcoin. But none of this has worked. Most Salvadorians continue to use the US dollar. The study found that “the most important reason for [people who knew about Chivo but did not download it] was that users prefer to use cash. This was followed by trust issues — respondents did not trust the system or bitcoin itself.”

Speculation is inherent in capitalism, but it increases, as other financial activities, in times of economic malaise and crises, i.e. when profitability falls in the productive sectors and capital migrates to unproductive and financial sectors where the rate of profit is higher. This is the reason for the emergence and rise of the crypto market. What the fall of this market now shows is what happens when investors start to expect a fall in profits from an impending slowdown and even recession in the ’real’ economy.

Digital currencies — whether they are private like Bitcoin or central bank (state-controlled) — are all expressions of technological change. This is history’s third money revolution: the first was the invention of commodity money about 5,000+ years ago. The second — made possible only with the invention of the printing press — was paper (fiat) money. The second money revolution created the dichotomy in economics between the real (tangible/objective) economy and the money/nominal one. The tension between the real and the paper money economy created inflation and financial asset bubbles.

Digitisation is the third revolution.

The point is that all three revolutions are the product of technical change not in ideas or institutions.

The ideas — monetary theory — and the institutions — banks and central banks — followed the technical change in the money system.

The third revolution allows the promiscuous creation and distribution of digital money, something which has no physical characteristics or relationship with anything tangible. It’s an idea, but one as influential as the written word.

Critically, what it allows is the separation of the idea of money as a medium of exchange from the idea of money as the store of wealth/value.

The connection between money as a medium of exchange and as a store of value was unbreakable when commodity money — gold and silver etc — was used.

But that’s gone.

This means that money can now solely be a medium of exchange used to make and receive payments in an electronic system.

This analysis only has value if it’s used to suggest what should be done.

The socially-optimal conclusion is that a publicly-owned electronic payments system should be created outside the control of banks and central banks which is freely available to all where money is used solely as a medium of exchange. This will be made possible by attaching a negative interest rate to it.

Wealth accumulation will not be permitted in electronic money.

The critical mistake you make is between digital money and crypto currency. Digital money is state money in another form that is all.

I’m referring to money in digital form. Crypto is one of the forms. central bank digital currencies are another (state-owned)

Its not money tho that’s the whole point, and the digital money which is actually money is that which is backed by the state. What would stop many public institutions from popping up and saying “hey use my currency”, etc it would just be a speculative asset again, the only thing in history to and the only thing which logically could be the basis of money in the context of global market is state backed currency. Also I don’t agree that the division is between a “tangible” economy and a “money/nominal” economy but rather from an economy which is actually producing aggregate profits from surplus labor, this of course being a monetary phenomena still! And then you can abstract a part of the economy which is not creating long term profits, not basing it on the production of value.

Until the printing press, money (in Europe, the Middle East and European colonies at least) was gold and silver coinage. So what was used to make and receive payments inextricably had a value and therefore was a store of wealth for those that had it.

Fiat money broke the link between money as a medium of exchange and money as a store of wealth but states used their power to make people treat fiat money as if it were goid and silver.

Digitisation allows for the first time the manufacture of electronic tokens to be used as a medium of exchange but can penalise holders with a charge to discourage them from accumulating those tokens.

This is consequential for both economic theory and for how economies operate.

But it’s essentially a manifestation of technical change, like the invention of the internal combustion engine.

Retaining in digital money the connection between its role as a medium of exchange with its role as a store of wealth would be a bit like insisting that motor cars should still be attached to horses.

” The tension between the real and the paper money economy created inflation and financial asset bubbles.’

Inflation, the devaluation of money, precedes the establishment of fiat currencies, with coin clipping being an art and a crime in 17th century England

I didn’t say that that the tension between the real economy and the paper money economy was the sole source of inflation. Inflation is often the result of shocks to the system, like the theft of South American gold and silver by the Spanish Empire.

Financial asset bubbles, however, are always a internally-generated fiat/paper/fictitious money phenomena.

Your entire comment is built on an assumption that is false: that non-commodity money is possible under the Capitalist mode of production. The commodity is both a use value and a value. And value must always take the form of exchange value. This is true even in simple barter before the emergence of money. Marx demonstrated in the opening chapters of Capital that even in its simple form the value of one commodity must be measured in terms of the use value of another commodity. Marx then demonstrates that the money relationship of production is simply a generalization of this simple form of value. By doing this, Marx had already proved that under any system of commodity production and exchange, including the most highly developed capitalism, non-commodity money is impossible.

Therefore, since non-commodity money is impossible under the Capitalist mode of production, what you refer to as ‘fiat money’ and ‘digital money’ cannot be real money. They are confined by the limits of commodity money that reigns over the capitalist system (Gold today, but used to be both Silver and Gold in Marx’s day). Should the amount of ‘fiat money’ and/or ‘digital money’ created exceed the amount of Gold Bullion produced globally, the value of said “money” measured in terms of actual money will decline in value over the long run (as was the case in the early 1920s with the Mark and the 1970s with the USD). In conclusion, no “technological revolution” will ever allow the creation of excess “money” to escape the contradictions of Capitalism without causing depreciation of said “money”. This is the limits of the Capitalist mode of production.

We agree.

Capital’s chapter one is absolutely clear about commodity money: gold and silver coinage. It’s internally consistent and logically coherent.

The purpose of my comment is to seek to simplify understanding of digital money.

My first point is that money’s different forms: commodity, fiat and now digital are determined by technical change, not abstract theorising (including by economists).

Once money is seen as part of a technical process it’s much easier for those taking a Marxian approach to human development to comprehend what digital money is and isn’t.

So the money economy is shaped by technology just as the real/tangible economy is.

The institutions surrounding it — like the institutions around commodity manufacturing — are a product — not the source — of that process,

You can’t have capitalists as Marx defined them until you have manufacturing.

You can’t have fiat money before the printing press or digital currencies before the computer.

The analytical tools developed by Marx in C1 can then be deployed.

Marx in the first sentence of the first chapter of the first volume of Capital states the priority; what is a commodity? (commodity is in fact a highly unsatisfactory translation of the German word War which appears to have been used because the French translation of Capital — which Marx actually approved – uses the word marchandise).

Marx logically and coherently argues a commodity has two characteristics (or natures).

1 Use value “conditioned” by its bodily shape

2 Exchange value, is an entirely subjective characteristic that emerged from social interaction: people have through iterative trade developed a social understanding that a thing’s exchange value is essentially due to the labour power a commodity embodies).

These two natures are inextricably connected.

No commodity (or manufactured good) can be a commodity unless it has both use value and exchange value.

Both natures come into existence simultaneously in the manufacturing process.

Neither is more important than the other (this depiction is perilously close to the Christian idea of Jesus Christ: both God and Man consubstantially — ie the tangible and the intangible).

Once you’ve got that, you can understand commodity money.

Yes, it has physical characteristics and yes it contains value due to human labour.

In commodity money, these are indivisible.

So it’s obvious that fiat money IS a commodity (a manufactured good) but one that exchanges for much more than its real, labour-determined value

The question then needs to be asked; how can that happen over the long term (as it has)?

It must be due to state power.

A similar approach should be taken to digital money.

It’s manufactured and has a bodily existence (electronic digits) but its real value is a tiny fraction of its exchange value.

How can that possibly be (unless you’re prepared to argue digital money is a special type of commodity that does not conform to Marx’s analysis)?

It can only retain that exchange value for two reasons:

* speculative buying by private investors which must lead to increasing boom and bust OR

* state power, which is now coming in the form of central bank digital currencies.

All this can be comprehended within the terms of Marxist semantics and substance.

The real purpose of my comment, however is not to understand the world but to change it.

The argument — which is consistent with the preceding line of thought — is that technology allows for the first time for the clear detachment of money as a medium of exchange.

In fact, a Marxist economic programme would REQUIRE that electronic money should never act as a store of value/wealth and should ONLY be used to exchange for things that have value: clothes, cars etc.

This approach means that the reality that fiat/digital money has almost no value would be finally recognised both in theory and in practice.

And the role of the state should not be to defend inflated digital money exchange values but to construct a socially accessible way for it to be bought and sold.

Marx observed that free-exchange (in the capitalist limit) entails the existence of money as a commodity. It was discovered NOT invented 5,000+ years ago. Inflation results from eliminating the store of value from medium of exchange. Digital currencies are an attempt to monetize a commodity with so real use only cost, i.e. negative value.

The Sumerian shekel, the first form of coinage, was developed around 5,000 years ago. Coins did not exist in nature.. They had to be made using gold that had been mined and smelted. That’s invention.

The availability of gold was limited by the extent and effectiveness of mining and this restricted its supply according to the amount and quality labour power applied to the gold coinage supply chain: exploration, mining, smelting, minting. This naturally kept the supply of additional gold in line with the deployment of labour and consequently contained the relative price of gold against everything else.

Inflation in commodity gold economies in the form of a persistent rise in prices was most strikingly recorded following the theft and importation into Spain of South American gold following the conquest of the region.

This was because the supply of gold massively exceeded the amount of labour involved in importing it.

Inflation as a structural feature of any economy is wholly the product of a fiat money system which allows corporations and then the state to expand its supply beyond the increase of value created by human labour.

Economists are guilty of massively complicating our capacity to understand the role of money. They almost never refer to the development of commodity money; the rise of fiat money and the emergence of digital money as being essentially technological developments, ie inventions that have been turned into something usable.

This is a very good article. It confirms ideas I have about money and currencies. There are more crackpot ideas about this than almost anything else. Most of them revolve around a paranoia about ‘government’ and a fallacy of reification; trying to make a physical thing out of an abstract idea.

Money is what is issued by a sovereign state to be used as a unit of account. Nothing else is money.

I wrote something on an this topic awhile back which might interest some people here. https://yaxls.wordpress.com/2022/04/19/an-age-of-monetary-cranks/

”Money is what a sovereign state issues to be used as a unit of account. Nothing else is money

‘’Digital money is state money in another form’’

These two comments reflect, in my opinion, the underlying problem and the viability or not of cryptocurrencies. Which problem?. Who are the owners of the money. Two aspects.

1.- Fetishism of merchandise. Users and investors of cryptocurrencies always seem to endow this currency with “almost magical” properties: for them they are not the solution to almost all social ills, but they almost are. The same thing happens today with robotics, AI, and before with computers, the steam engine, the printing press, etc. This is false, of course. Cryptocurrencies as simple objects that they are have no power. Neither good nor bad, beyond the technological advance that they entail. It is their owners (producers) who do have the power. And the problem of the (bad) distribution of ownership of capital and its associated power has only one solution: Socialism.

2.- Owners of the money. The two previous commentators allude to the current owner of the money: the sovereign states. And, of course, the fact that Huawei wants to unseat Apple with a new and revolutionary smartphone is not the same as the fact that some investors and private users of the cryptocurrency want to unseat the States. Forget about the size and power of the current state owners of money without seeking their support – the support of the state of El Salvador is too little and the Chinese state has just completely banned private cryptocurrencies but goes ahead with its state digital yuan – and Believing that they could compete with them is the fatal mistake of private crypto producers.

If you look at economic history in the broad perspective, isn’t the “money commodity” that serves as store of value, land? It’s not fungible and it’s not portable, but it is by the far the only commodity that historically has made those who had it richer over time. The reason I would say is that it has use value in pretty much any kind of production system where the population is increasing.

In the abstract sense of “land” meaning the national realm, fiat money from states is the taxation on said “land.” In the early US, land sales literally were either the largest or second largest source of revenue, a position traded with tariffs…charges on goods entering into the “land” of the state.

But the reactionary ideology that sees inflation as the expropriation of wealth and no taxation with representation as true freedom tends (especially in the US?) tends to focus on hard money. Hard money helped to kill Reconstructioni in the US, especially after the class struggle crisis of 1877. The right-wingers used to pretend they hated the Federal Reserve. But it’s like never impeaching judges or packing courts, that’s all strictly tactical.

Cryptocurrencies are nothing but financial vaporware.

It is incredible that the regulatory authorities allowed this industry to develop given the opportunities for fraud and criminality.

Behind them is only an idea, a feeble one at that.

But ideas can momentarily develop traction but such ideas eventually pass.

Financial history is replete with them.

There will always be the gullible and those willing to profit from them.

If it was such an obvious vaporwqre you wouldn’t see such big players jumping in. Meta pumping billions into it. Crypto is the logical conclusion that looks for salvation in technology and saviours in silicon valley billionaires.

Right, just as they didn’t jump into the asset backed securities boom, the dotcom boom the saving and loans boom, etc etc ad infinitum

Criticalb,

You should read “Extraordinary Popular Delusions and the Madness of Crowds” by Charles Mackay (first published in 1841).

“They will not replace fiat currencies, where the supply is controlled by central banks and governments as the main means of exchange.” This is not strictly correct. The supply of fiat money is a complex matter as commercial banks are also involved in the generating of credit money. What really distinguishes fiat money is that the state, via taxation, has a claim on the value produced by the working class and it is this which underpins fiat money. Provided the state more or less keeps its fiscal house in order this does not disturb the money supply as for example the COVID Relief funds did. As I have explained in Modern Marxist Monetary Theory, the Stock of M2 consists of legacy value or unspent monetized revenue amounting to 92%, the balance being temporary money i.e. bank credit (loans) 3-4%, new permanent money such as QE until it is reversed 2-3%, and the net balance of flows from speculation which amounts to much less than most assume. (I leave out foreign transactions)

Where Michael is correct cryptos are not real money, nor are they backed by any sources of value. They were and remain ticking financial time bombs that has added to global warming, making some rich provided they sold out and a lot poorer. I believe at present 70% of the holders of crypto are underwater, i.e. they are nursing losses. Total losses as of Friday were $1.3 trillion compared to a peak $2.3 trillion. Consequential. Many workers who thought they could avoid work because of their crypto gains have now been forced back into the labour market.

Cryptos are only relevant as a barometer for what is happening in the real economy now that interest rates were forced up. Money is no longer cheap nor plentiful. Remember, interest rates are the enema of capitalist production purging then freeing up the metabolism of capitalism. They tend to flush away elements of fictitious capital such as cryptos leaving no floaters behind.

“Provided the state more or less keeps its fiscal house in order this does not disturb the money supply as for example the COVID Relief funds did.” This reads as a claim the Republicans like DeSantis are correct in blaming Bidenomics for inflation. But this seems to be an absurd claim, because inflation is a worldwide phenomenon. By orthodox economics the Chinese state is even more a fiscal absurdity than Democratic Party socialism (I don’t agree the Democrats are socialists,) yet inflation there is lower than the US. The last I looked the Dutch were fiscal fanatics but their inflation was at least recently worse.

Taxation also includes tariffs, by the way, which asks the question, which working class is being fleeced by the state? (And I’m not sure that taxation is the main form of exploitation, a notion which seems more Republican than Marxist. I think more people are underpaid than overtaxed…unless you compare taxes to services rendered. But the objection is to taxes, not lack of services.)

‘Provided the state more or less keeps its fiscal house in order’ without the discipline of a physical representation, i.e. specie, when has this happened?

”What working class is being fleeced by the state? (And I am not sure that taxes are the main form of exploitation, a notion that seems more republican than Marxist ’’

Good question.

In my point of view, a current Marxist must ask himself that question and others about the State. Knowing that the current State generates between 35% and 50% of the production in all the countries of the world, in addition to the socialist countries. The current State is more dominant and much larger in size (multiplied by 5) than the State of Marx.

More questions:

1º.- In that exploiting State (or at least in a situation of unequal commercial exchange with its citizens because the State has a guaranteed – a monopoly imposed by force – its production, prices and collection – taxes – but the citizens do not have their guaranteed sales) is it just the Government and the parties or should all of its officials be included in the category of exploiters? Some officials who represent from 15% to 25% of the working population. Are they progressive or reactionary employees (labor aristocracy)?

2º.- Is the economic subject called the State in an increasing or decreasing rate of profit?

3º.- Are the States growing in size or are they decreasing? Does the economic law of the concentration of capital affect them or not? If so, when and how do they grow? I clearly observe periods in which they do grow and others in which they decrease. Since the 1980s they have decreased, and before that, since 1917, they have grown. And historically there are similar periods of growth and decline of the States. Regular and systematic increases and decreases. In cyclical movement

“Provided the state more or less keeps its fiscal house in order this does not disturb the money supply as for example the COVID Relief funds did.”

What does that mean. US Tsy, Fed, and FDIC made interventions on a similar scale in 2008-2009. Wasn’t that “keeping the house in order”?

And the expenditures in Iraq and Afghanistan, did that amount to keeping the house in order? Didn’t produce galloping inflation.

Money represents value. Believing that cryptocurrency can represent value reminds me of spring and Tulips. What happens when the cost of generation exceeds the value produced? Is the price infinite?

Money through history has had three functions; medium of exchange, store of value, unit of account.

Only the first two matter in economic theory.

Gold/silver coinage which was the sole money in Europe (until the printing press) was inextricably both a medium of exchange (for example the Austrian-government minted Marie Louise Thaler was accepted and paid throughout Arabia until the 1950s) and a store of wealth (because it had intrinsic material value).

Fiat money (paper money and coins made of alloy that were deemed by the state to have a gold and silver equivalent) destroyed the link between medium of exchange and store of value.

Digital money allows this division to be practically usable: ie you can have an electronic token used for payments that has no store of value (by attaching a charge to anyone who holds it).

That’s the result of technological change but one that has potentially enormous consequences for economic theory and the way economies operate.

Steven analysing money and price behaviour is a science which does not belong in Congress. One of the key challenges facing Marxist was the world wide price stability ending 2019 compared to the equivalent in length period of Bretton Woods and its gold standard. The reason for this is that money when not disturbed serves to exchange legacy value for current value, or to put it another way the exchange extinguishes past revenue by converting current value into current revenue. So it does not matter what form money takes, paper or digital, it is circulating value which is the key event. Now, when M2 comprises 90-92% of this unspent revenue it acts as the ballast keeping prices stable much to the annoyance of the FED. It can go awry as my analysis of the dual impact of a collapse in value production combined with fiscal funds shows http://theplanningmotive.com/2021/12/16/will-inflation-endure-into-the-new-year-transitory-or-not/

It’s easy for me to define a cryptocurrency: What is the value of a bitcoin? Today $100, tomorrow it could be $1000 or $10. Any country that has a relatively stable currency 1 unit of currency can be worth 10 kg of bread, tomorrow if the economy is reasonably stable it will be worth the same 10 kg of bread. If the country is in a very high inflation, maybe it will be worth 9.5 kg of bread, but never 100 kg of bread or 1 kg of bread, which happens with cryptocurrencies. There is no evolution in cryptocurrencies, it is simply a fraud with embedded technology.

Irrelevant but for what it worth’s the communist backed panspoudastiki gets first place since 1987 in student unions.

http://www.idcommunism.com/2022/05/communist-backed-panspoudastiki-triumphs-in-greek-university-student-elections.html

What will you say about ERC-20?