I have argued in many posts that ‘profits call the tune’ in capitalist accumulation. What I mean by that is that any change in business profits (and profitability) will lead to changes in business investment – and not vice versa over time.

Profits are key to capitalist investment, not ‘effective demand’ as Keynesians argue, or changes in interest rates or money supply as Monetarists and the Austrian school argue. I differ strongly from the post-Keynesian view that profits are a ‘residual’ generated by investment; or as Keynesian-Marxist Michal Kalecki put it: ‘capitalists earn what they invest, while workers spend what they earn’.

Yes, workers spend what they earn from wage labour ie (consume and save little); but capitalists do not ‘earn’ profits from their investment in capital (means of production and labour). This theory denies Marx’s law of value that only labour produces value and surplus value (profit) for the capitalist. It turns profit into the ‘gift of capital’; ie there is no profit without capitalists investing. Yet profits can be generated out of the exploitation of labour power and capitalists may not invest. Indeed, that is what we can see now in the expansion of ‘fictitious capital’ at the expense of productive investment.

And it’s not just the theory; the empirical evidence is overwhelming that profits lead investment. In several posts and papers, I have cited empirical work done by Marxist economists like Alan Freeman, Andrew Kliman, Peter Jones, Jose Tapia, Guglielmo Carchedi and others including myself that show this. Moreover, there are also many mainstream economic studies from prestigious sources that deliver the same story.

Recently, in an article for the Financial Times, more evidence that profits call the tune has been presented. Ian Harnett, co-founder and chief investment strategist at Absolute Strategy Research, a macro financial research company, finds that global business investment in the ‘means of production’ tends to follow global profits growth. Harnett’s study is global and not just the US, where most empirical work has been done up to now.

In the graph below, he measures the year-on-year change in global non-financial sector investment after depreciation. In effect, this means new investment over and above that needed to replace worn out equipment and structures. The graph shows that earnings (profits) growth in the non-financial sector from the 1990s leads changes in new non-financial investment: profits call the tune. When earnings growth rises as in the 1990s, investment follows it upwards and then down in the later 1990s. Earnings growth started slowing as early as 2005, leading to a decline in investment, and eventually to the Great Recession.

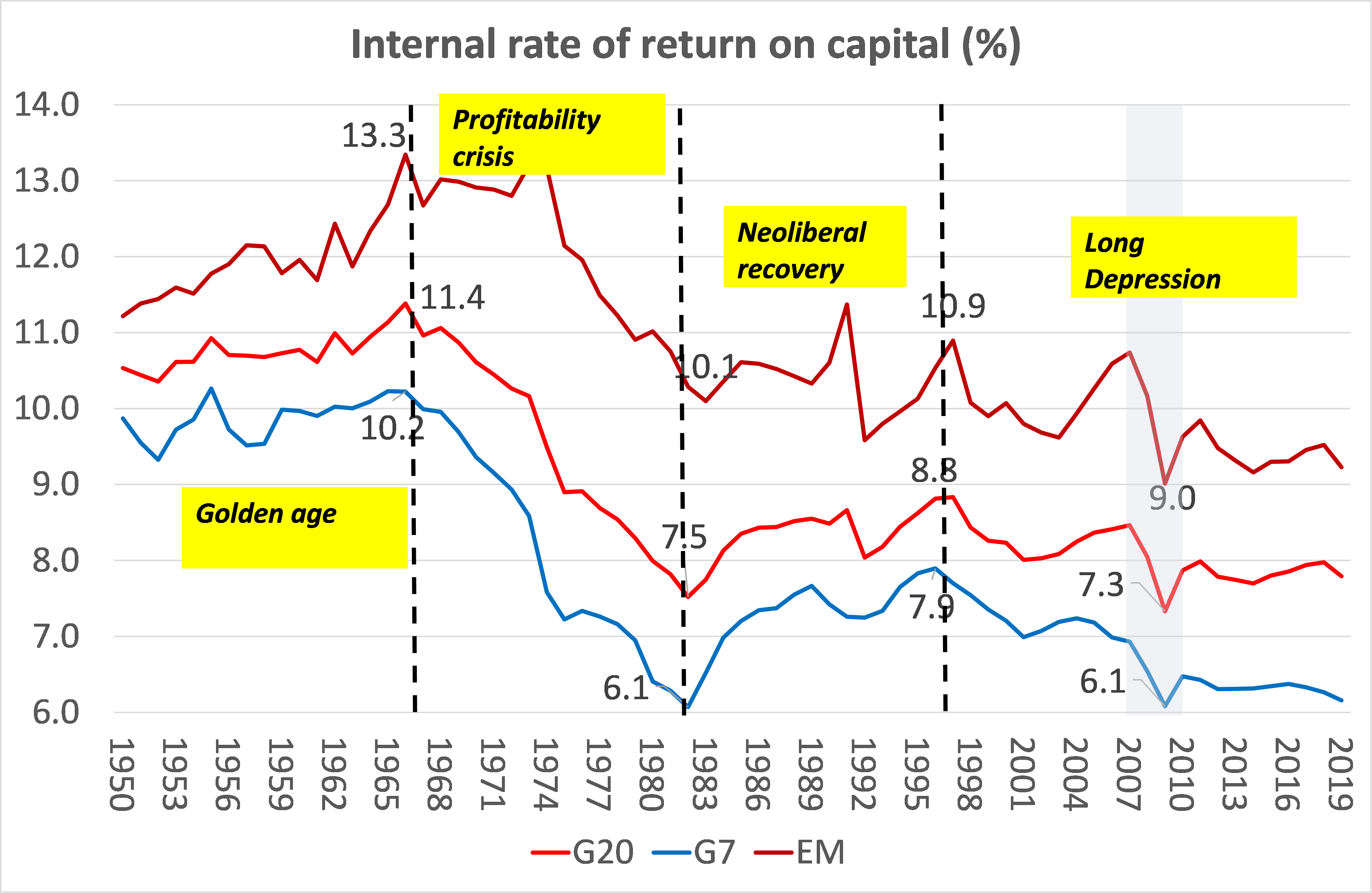

Several studies (including my own) show that the global rate of profit (profitability not profits) has been in secular decline over the last 70 years and in particular since the late 1990s.

Source: Penn World Tables 10.0 IRR series

If the theory is right, then falling profitabilty long term should lead to a secular fall in business investment; and Harnett’s global data confirm that. Harnett’s data show that new investment relative to depreciation has declined globally from a multiple of 2 in the 1990s to less than one now. In other words, annual global investment is now less than that needed to replace worn out fixed assets!

‘Non-financial investment’ includes public sector investment, so it could be that the decline is partly due to fall in public investment as a share of GDP in the last 30 years and not due to a fall in business investment. But while the reduction in public spending in infrastructure etc is a factor, it is clear from the first graph that investment has been falling in line with profitability and not mainly because of ‘austerity’.

If we look at investment rates (as measured by total investment to GDP in an economy), we find that in the last ten years, total investment to GDP in the major economies has been weak; indeed in 2019, total investment (government, housing and business) to GDP is still lower than in 2007. In other words, even the low real GDP growth rate in the major economies in the last ten years has not been matched by total investment growth. And if you strip out housing, business investment has performed even worse.

In his FT piece, Harnett wants to argue that post-COVID things are about to change. There will now be a focus of investing productively by ‘capital-heavy’ businesses through ‘reshoring’; spending on infrastructure especially on environmental targets; and on global protectionist measures to avoid reliance on China’s production etc. Harnett reckons this rise in investment will be driven by a new political will to keep interest rates low and a reversal of neoliberal austerity through extra government spending. But this conclusion runs against his own evidence that investment is driven by profits, not by government spending or ‘effective demand’.

Mr Roberts, I am a Ph.D. Candidate in Ecological Economics, McGill University. I am working on the supply chains of oil sands and try to estimate the relationship (if any) between energetic dimensions and profitability in the production and trade of fossil fuel. Consequently, I am quite interested in the concept of profitability. However, I can think of quite a few ways to define it, in particular if one considers this notion in the long history of political economy. I am wondering if you, or an academic you know, have ever wrote a paper, article, blog post or something on the different definitions of ‘profitability’. I am obviously interested in the Marxist definition, but not only. Thank you very much in advance for your time and consideration.

Hi Charles Measuring profitability depends on many factors. What is the numerator? Is it earnings as reported on company books; is it profits including rents and interest or just profits from producing businesses? Is it net of depreciation or gross? Do we look at just non-financial sector profits? And so on. Then there is the denominator: do we use fixed asset stocks from companies or include inventories; do we include wages in the bottom line as a capital expense as Marx does or not?; do we measure assets in replacement or historic costs; do we use GDP or value added or sales on the bottom line; do we measure in current prices or constant prices? That’s just a start. https://quickbooks.intuit.com/global/resources/expenses/measure-your-business-profitability/ https://thenextrecession.wordpress.com/2011/07/29/measuring-the-rate-of-profit-and-profit-cycles/#:~:text=His%20famous%20formula%20followed%3A%20P,applies%20to%20the%20whole%20economy. https://www.exploring-economics.org/en/discover/on-the-rate-of-profit/

“but capitalists do not ‘earn’ profits from their investment in capital (means of production and labour). This theory denies Marx’s law of value that only labour produces value and surplus value (profit) for the capitalist. “

I don’t see how exactly Kalecki’s (simplifying) statement contradicts Marx’s theory of value. Investment activity ‘earns’ value for the capitalist and this value is the surplus value that is produced in excess of the labor wage. In that sense, the level of activity that capitalists decide to “spend” on investment activity determines their “earning”.

Clearly the data presented in this article are in strong favor of the profits leading investment, my comment is merely on not seeing why Kalecki contradicts Marx on the theory of value here.

Ioannais read this excellent piece by Jose Tapia that deals with your point. https://ideas.repec.org/h/eme/rpeczz/s0161-7230(2013)0000028009.html

“Harnett’s data show that new investment relative to depreciation has declined globally from a multiple of 2 in the 1990s to less than one now. In other words, annual global investment is now less than that needed to replace worn out fixed assets!”

I would scrub that argument. Both you and Harnett are victims of the 2012 international revision to the System of National Accounts in which Intellectual Property elements were converted from costs to capital thus yielding depreciation. I refer in particular to Research and Development as well as in-house software which were capitalized and therefore subject to depreciation. The net effect of these fictitious imputed sales was that I.P. depreciation rose from 10% of total depreciation in the 1950s to 40% now, yes 40%. Thus total depreciation is a nonsense. Strip out the I.P. element and lo and behold depreciation has not outrun investment. In fact, as R&D and software increases in the information age, so does the IP element of depreciation making your above observation increasingly inaccurate. (I am not saying that there has not been a relative decline in investment, and as you know, I have always backed your observation that the cart does not lead the horse, i.e. investment does not lead profits, but profits leads investment.)

I would urge you and your readers to turn your attention to BEA Fixed Assets Table 4.4 on depreciation and divide row 48 into row 51. The System of National Accounts needs to be traversed with knowledge.

Talking about accuracy I would like to point out there are only two accurate Marxian rates of profit. Enterprise Profit divided by constant capital (Fixed + Inventories) and variable capital (annual wages divided by turnover) or enterprise profit divided by fixed and circulating capital which has the added advantage of capturing international outsourcing. Neither you nor the theorists you quote employ either of these formulas.

A hundred years ago, the investment required to add 2000 tons of steelmaking capacity was roughly twice the investment required to add 1000 tons. Economies of scale, although significant, were fractional modifications of this fact. Now, as ucanbepolitical alludes, the investment to double the speed of image processing on one computer can be the almost the same as the investment to double the speed on a million computers: it is the investment in designing and writing new software. What is the impact on the working class? That is the big question, since in the U.S., for example, real median earnings of workers have stagnated and fallen since 1973. The explanation has big implications for capitalism and socialism, that is, for the era of revolution.

Michael,

“Profits are key to capitalist investment, not ‘effective demand’ as Keynesians argue…”

Keynesians might argue this way but Keynes agreed with you.

Read pages 46-47 of the GT.

However, while changes in expectations about profits affect investment, investment constitutes an important component of effective demand.

Dear Mr Roberts,

I’d like to have your thoughts about this.

Even though profits certainly call the tune of capitalist investment, and thus predict slumps in a capitalist economy, have you considered the possibility that earlier in the business cycle, the lack of effective demand may itself lead to the fall of profits ? I explain myself.

First, during the bust, firms over-invest due to the absence of economic planning, which eventually leads to excess production relative to market capacity. At the end of the bust, firms thus have to fight for limited effective demand, and to do so they start to push their prices down, lowering their margins. As a consequence, profits fall and, as you have shown many times, investment shrinks, so the bust begins.

I sometimes feel that because you have to defend Marxist theory so much against its critiques (especially the TPRF, and especially against Keynesians) you do not emphasize ways in which effective demand may fit into Marxist crisis theory as well. One could actually see the lack of effective demand (and competition) at the middle of the business cycle as a catalyst that makes the law of value and the TPRF come into force. Indeed, at the end of the bust, when the firms with the highest organic composition (the most productive) push down their margins to compete for limited effective demand, it brings down market prices closer to the new socially necessary values, which leads to a new lower average profit rate compared with the beginning of the cycle. This rate is too low for total profits to keep rising. So absolute over-production is reached and the crisis begins.

PS : I mean absolute over accumulation

PPS: and I write bust instead of boom a couple of times… good luck

Dear Martin This deserves a proper reply which I dont have the time to do right now. I think that I would pose it this way. In the ‘business’ cycle (or profit-investment cycle) as capitalists increase production and invest, the organic composition of capital will rise and profitability at a certain point will start to fall – even if ‘effective demand’ is still robust. Then profit growth will slow. Competition between capitals will intensify and price competition will follow. This will intensify profit slowdown to the point of absolute overaccumulation and a fall in total profits. Then investment collapses and with it employment and wages and thus effective demand drops. This can cause further price reductions and bankruptcies. Effective demand is a product of capitalist investment and workers consumption and it spirals down in the slump reducing sales and thus profits. But consumer demand only falls after investment demand and not by nearly as much. Interestingly, empirical evidence shows that profits call the tune for investment but also investment calls the tune (at a later stage in the cycle) for profit.