Larry Summers is one of the world’s leading Keynesian economists, a former Treasury Secretary under President Clinton, a candidate previously for the Chair of the US Fed, and a regular speaker at the massive ASSA annual conference of the American Economics Association, where he promotes the old neo-Keynesian view that the global economy tends to a form of ‘secular stagnation’.

Summers has in the past attacked (correctly in my view) the decline of Keynesian economics into just doing sterile Dynamic Stochastic General Equilibrium models (DSGE), where it is assumed that the economy is stable and growing, but then is subject to some ‘shock’ like a change in consumer or investor behaviour. The model then supposedly tells us any changes in outcomes. Summers particularly objects to the demand by neoclassical and other Keynesian economists that any DSGE model must start from ‘microeconomic foundations’ ie the initial assumptions must be logical, according to marginalist neoclassical supply and demand theory, and the individual agents must act ‘rationally’ according to those ‘foundations’.

As Summers puts it: “the principle of building macroeconomics on microeconomic foundations, as applied by economists, contributed next to nothing to predicting, explaining or resolving the Great Recession.” Instead, says Summers, we should think in terms of “broad aggregates”, ie empirical evidence of what is happening in the economy, not what the logic of neoclassical economic theory might claim ought to happen.

Not all Keynesians agree with Summers on this. Simon Wren-Lewis, the leading British Keynesian economist claims that the best DSGE models did try to incorporate money and imperfections in an economy: “respected macroeconomists (would) argue that because of these problematic microfoundations, it is best to ignore something like sticky prices (wages) (a key Keynesian argument for an economy stuck in a recession – MR) when doing policy work: an argument that would be laughed out of court in any other science. In no other discipline could you have a debate about whether it was better to model what you can microfound rather than model what you can see. Other economists understand this, but many macroeconomists still think this is all quite normal.” In other words, you cannot just do empirical work without some theory or model to analyse it; or in Marxist terms, you need the connection between the concrete and the abstract.

There is confusion here in mainstream economics – one side want to condemn ‘models’ for being unrealistic and not recognising the power of the aggregate. The other side condemns statistics without a theory of behaviour or laws of motion.

Summers reckons that the reason mainstream economics failed to predict the Great Recession is that it does not want to recognise ‘irrationality’ on the part of consumers and investors. You see, crises are probably the result of ‘irrational’ or bad decisions arising from herd-like behaviour. Markets are first gripped by ‘greed’ and then suddenly ‘animal spirits’ disappear and markets are engulfed by ‘fear’. This is a psychological explanation of crises.

Summers recommends a new book by behavioural economists Andrei Shleifer’s and Nicola Gennaioli, “A Crisis of Beliefs: Investor Psychology and Financial Fragility.” Summers proclaims that “the book puts expectations at the center of thinking about economic fluctuations and financial crises — but these expectations are not rational. In fact, as all the evidence suggests, they are subject to systematic errors of extrapolation. The book suggests that these errors in expectations are best understood as arising out of cognitive biases to which humans are prone.” Using the latest research in psychology and behavioural economics, they present a new theory of belief formation. So it’s all down to irrational behaviour, not even a sudden ‘lack of demand’ (the usual Keynesian reason) or banking excesses. The ‘shocks’ to the general equilibrium models are to be found in wrong decisions, greed and fear by investors.

Behavioural economics always seems to me ‘desperate macroeconomics’. We don’t know why slumps occur in production, investment and employment at regular and recurring intervals. We don’t have a convincing theoretical model that can be tested with empirical evidence; just saying slumps occur because there is a ‘lack of demand’ sounds inadequate. So let’s turn to psychology to save economics.

Actually, the great behavourial economists that Summers refers to also have no idea what causes crises. Robert Thaler reckons that stock market prices are so volatile that there is no rational explanation of their movements. Thaler argues that there are ‘bubbles’, which he considers are ‘irrational’ movements in prices not related to fundamentals like profits or interest rates. Top neoclassical economist Eugene Fama criticised Thaler. Fama argued that a ‘bubble’ in stock market prices may merely express a change in view of investors about prospective investment returns; it’s not ‘irrational’. On this point, Fama is right and Thaler is wrong.

The other behaviourist cited by Summers is Daniel Kahneman. He has developed what he called ‘prospect theory’. Kahneman’s research has shown that people do not behave as mainstream marginal utility theory suggests. Instead Kahneman argues that there is “pervasive optimistic bias” in individuals. They have irrational or unwarranted optimism. This leads people to take on risky projects without considering the ultimate costs – against rational choice assumed by mainstream theory.

Kahneman’s work certainly exposes the unrealistic assumptions of marginal utility theory, the bedrock of mainstream economics. But it offers as an alternative, a theory of chaos, that we can know nothing and predict nothing. You see, the inherent flaw in a modern economy is uncertainty and psychology. It’s not the drive for profit versus social need, but the psychological perceptions of individuals. Thus the US home price collapse and the global financial crash came about because consumers have irrational swings from greed to fear. This leaves mainstream (including Keynesian) economics in a psychological purgatory, with no scientific analysis and predictive power. Also, it leads to a utopian view of how to fix crises. The answer is to change people’s behaviour; in particular, big multinational companies and banks need to have ‘social purpose’ and not be greedy!

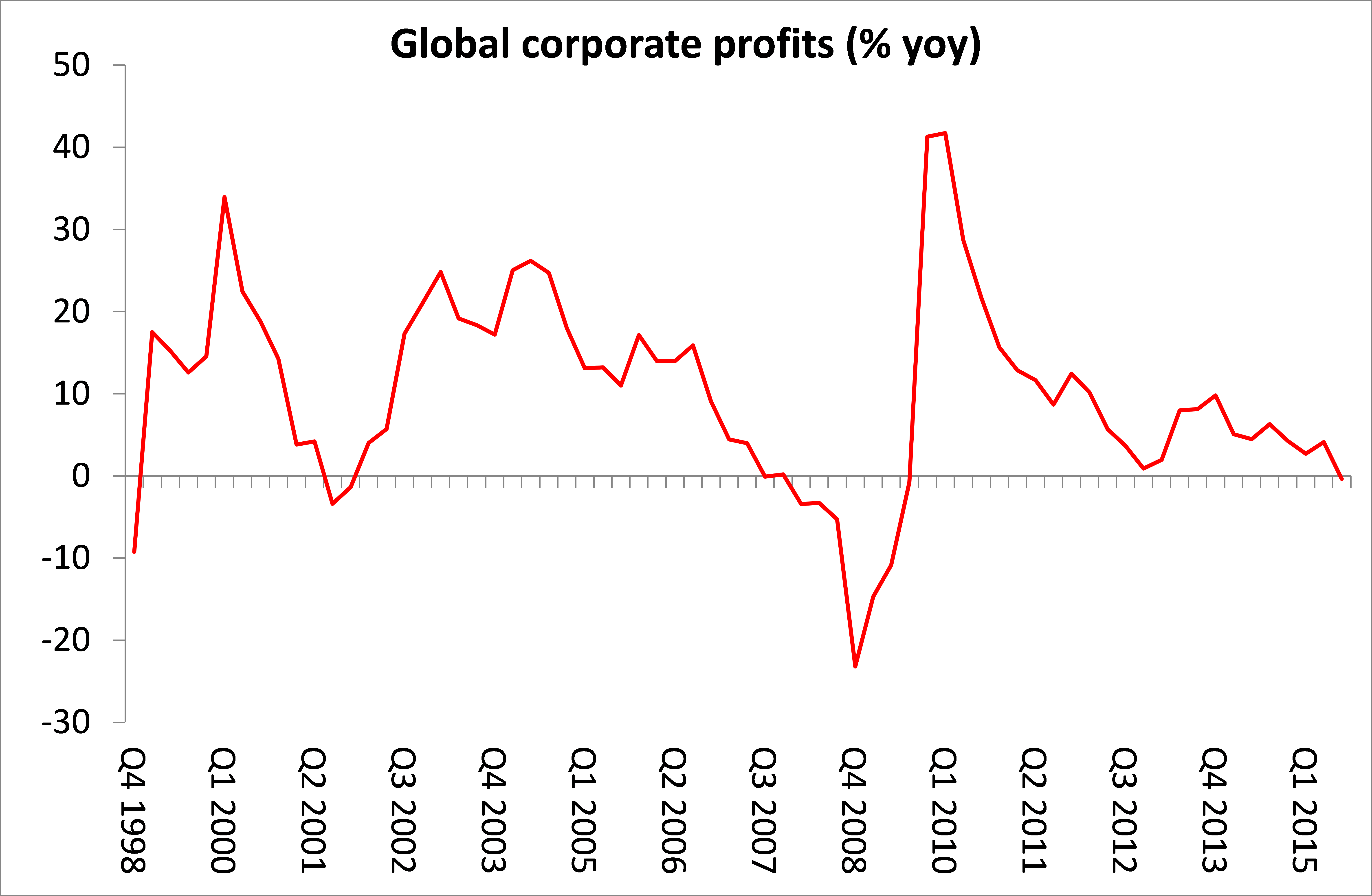

Turning to psychology is not necessary for economics. At the level of aggregate, the macro, we can draw out the patterns of motion in capitalism that can be tested and could deliver predictive power. For example, Marx made the key observation that what drives stock market prices is the difference between interest rates and the overall rate of profit. What has kept stock market prices rising now has been the very low level of long-term interest rates, deliberately engendered by central banks like the Federal Reserve around the world.

Of course, every day, investors make ‘irrational’ decisions but, over time and, in the aggregate, investor decisions to buy or to sell stocks or bonds will be based on the return they have received (in interest or dividends) and the prices of bonds and stocks will move accordingly. And those returns ultimately depend on the difference between the profitability of capital invested in the economy and the costs of providing finance. The change in objective conditions will alter the behaviour of ‘economic agents’.

Right now, interest rates are rising globally while profits are stagnating.

The scissor is closing between the return on capital and the cost of borrowing. When it closes, greed will turn into fear.

Then we have boom to bust. Gresham’s Law- Bad Money (that which is sovereign ‘deemed’) will drive Good Money ( created by gain in GDP) out of circulation. justaluckyfoolJuly 22, 2014 at 2:55 PM

Frederick Soddy predicted the “systemic flaw”: “The Role Of Money”

(Entire book as a free download… http://archive.org/details/roleofmoney032861mbp

Quote Soddy, “It was recognized in Athens and Sparta ten

centuries before the birth of Christ that one of the most vital prerogatives

of the State was the sole right to issue money. How curious that

the unique quality of this prerogative is only now being re-discovered.”

“… It is concerned less with the details of particular schemes

of monetary reform that have been advocated than with the general principles to which, in the author’s opinion, every monetary system must at long last conform,

if it is to fulfil its proper role as the distributive mechanism of society. To allow it to become a source of revenue to private issuers is to create, first, a secret and illicit arm of the government and, last, a rival power strong enough ultimately to overthrow all other forms of government.” **** This is a “Fatal Flaw”.

To regulate this awesome power is really just about impossible since any conditions placed upon restricting the quality or quantity of the bank issuance is impossible because regardless of ‘reserve’ or ‘capital ‘ requirements, these requirements are self-fulfilling after the fact of issuance. The issuance being as “good as the faith and credit of the sovereignty” is unconditionally guaranteed redeemable. THE ISSUANCE WILL DRIVE THE GOOD MONEY OUT OF CIRCULATION. PERIOD.

As for the 2008 crisis there could have been a “systemic failure” because the Private For Profit Banks (PFPB) sold “future cash flow a/k/a interest income”

and were not able to turn that over to the investors. Also after having paid for ‘insurance against loss, it was discovered, the insurers as well lacked ‘the good faith and credit to make good their warranties.

If you can not trust the PFPB and the Insurers guaranteed redemption-the bubble surely would burst.

“…but they can’t get the mortgage notes written down to affordable levels for contractual reasons….”

Quote Sheila Bair (Former FDIC Chairman),”How could things have deteriorated so quickly…? In a word, securitization.

…Working with a Wall Street investment bank, the issuer packages the mortgages together into ‘pools’ and divides the right to the cash flows of these mortgages into securities that are sold to investors…”

(“BULL BY THE HORNS”)

THE KEY WORDS BEING, “…the right to the cash flows of these mortgages into securities that are sold to investors…”

These contracts allowed the investors to take away the rights of the lenders to modify the mortgages: they sold “the cash flows” for cash .

How could they get back the trillions of dollars they already spent so they could repurchase the MBSs ?

The Fed would be able to “fix” the modification problem with a simple strokes on a computer: Allow all to stay at market value, with loans at 3% for 40 years,period. 85% would stay, the other 15% would become welcomed ‘short sales’. END OF CRISES, stabilizing the housing industry, saving millions of jobs and even creating more jobs.

But if they were to reveal the banks made trillions of profit by selling-future interest income. The banks made a fatal error in that they turned over to the investors all control over the performance of the basic asset thereby making it impossible for the PFPB to make good on there “representations”. The only way available to the PFPB was to return the trillions they took since it was discovered that not only were they not of “good faith and credit” but also the insurers they paid were also not of “good faith and credit”. Has anyone asked ,why the Fed purchased almost $1 trillion of MBSs instead of the mortgages ? Would the Fed have exposed-we are in a system that is flawed and may result in catastrophic failure.

WE MUST END: TAXATION OF ISSUANCE OF OUR OWN CURRENCY BY (PFPB) PRIVATE FOR PROFIT BANKS!

“Summers recommends a new book by behavioural economists Andrei Shleifer’s and Nicola Gennaioli”

So, we don’t need those overpaid politicians and economists! Good news!

Jokes aside, only in capitalism humanity gets the blame for the failures of the system.

OMG THEY DON”T KNOW! NOT BERNANKE-GEITHNER-PAULSON-FREENSPAN!https://rwer.wordpress.com/2018/09/12/bernanke-geithner-and-paulson-still-dont-have-a-clue-about-the-housing-bubble/

WHY? Because they do not know “What is Money”. Period.

Quote Cullen Roche,” So you can see that the man running monetary policy in the USA for 18 years was working under a “flawed” framework. If the Fed chief has a flawed understanding of our economic system then who can we really expect to understand all of this? It’s clear to me that no one really does understand it completely and that explains, in large part, why the USA is in the position it is in today.”

“Quote Frederick Soddy, “So elaborately has the real nature of

this ridiculous proceeding been surrounded with

confusion by some of the cleverest and most

skilful advocates the world has ever known, that ( it is not intended to be known.)

SOLUTION____

QUOTE: Soddy, “…indeed it is now a truism was that nothing useful can be done unless and until a scientific money system

takes the place of the one now always breaking down. The corollary, however, is never likely to be popular with our professional politicians…

It was that, if such a thing were done, little else in the way of arbitrary interference with and government control over the essential activities

of men in the pursuit of their livelihood would be required.

Indeed, just as now not one in a thousand understands why the existing money system has such power to hurt him,

so, if it were corrected as here outlined, not one in a thousand would need to know or, indeed, would know,

except by the consequences, either that it had been rectified or how it had been rectified…”

Since, in all monetary civilizations, it is money that alone can effect the exchange of wealth

and the continuous flow of goods and services throughout the nation, money has become the life-blood of the community,

and for each individual a veritable licence to live at all…

A very slight knowledge of our actual existing monetary system makes it abundantly clear that,

without democracy knowing or allowing it, and without the matter ever being before the electorate

even as a secondary or minor political issue, the power of uttering money has been taken out of

national hands and usurped as a perquisite by the moneylender. Practically every genuine

monetary reformer is unanimous that the only hope of safety and peace lies in the nation

instantly resuming its prerogative over the issue of all forms of money…”