In a recent post, Paul Krugman took up the issue of whether movements in the stock market provide a good guide on how the capitalist economy is doing. The question arises because the US stock market prices have hit a new all-time high in the last couple of weeks with apparently slightly better economic news and with the conviction among investors (i.e. big banks, corporation, managed funds and hedge funds) that the US Federal Reserve was not going to raise its policy interest rate this year or even for the foreseeable future.

Krugman reckons that “stock prices generally have a lot less to do with the state of the economy or its future prospects than many people believe. As the economist Paul Samuelson put it, “Wall Street indexes predicted nine out of the last five recessions.” Indeed, Krugman went further in saying that “in some ways the stock market’s gains reflect economic weaknesses, not strengths. And understanding how that works may help us make sense of the troubling state our economy is in.”

Krugman makes three (good) points to explain why stock prices are of little guidance about the state of the US economy: “First, stock prices reflect profits, not overall incomes. Second, they also reflect the availability of other investment opportunities — or the lack thereof. Finally, the relationship between stock prices and real investment that expands the economy’s capacity has gotten very tenuous.”

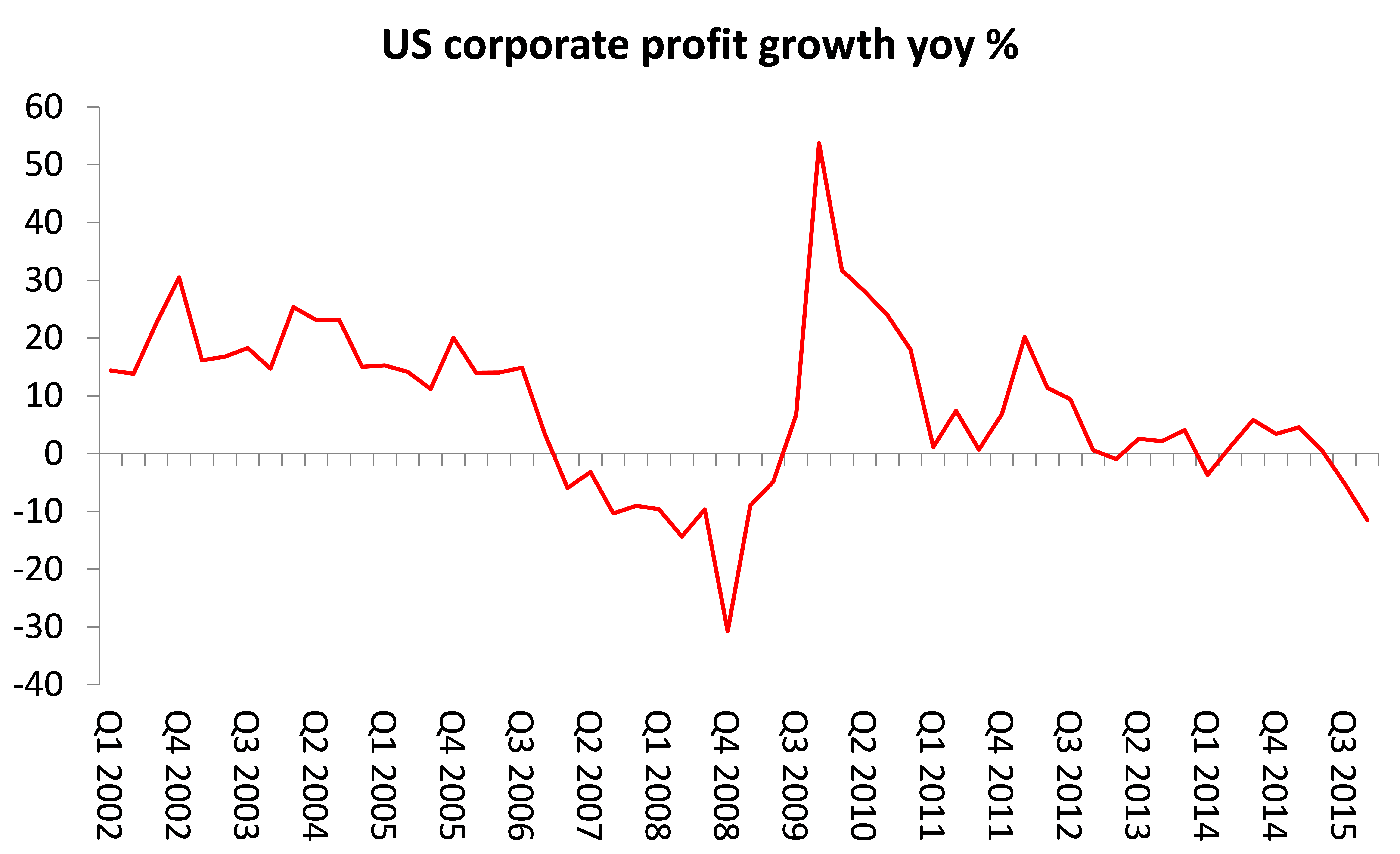

And profits in the US have been falling as a share of total output and even in absolute terms just as the stock market has risen.

And the prospects for investment that will deliver higher growth have diminished. So it would seem that the stock market has got way out of line with the so-called ‘real economy’.

Why? Well, Krugman’s answer is ‘monopoly power’. The very big companies are making big money, and then sitting on the cash and buying back their own shares. As a result, stock prices rise even though investment in the real economy stagnates or falls. There is no doubt that this is part of the explanation. But the other part relates to the very low interest rates that operate across the board in the major economies. Central banks in many economies have driven interest rates into negative territory, so banks are being paid to borrow money and in turn they must offer very low rates to companies and households, particularly the large companies. They can virtually borrow for free and then use the cash to buy shares.

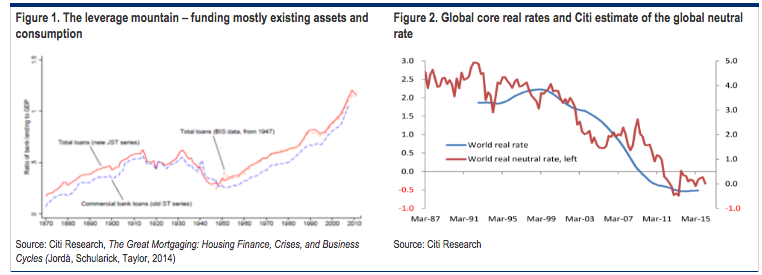

This is a financial credit ‘bubble’ of similar proportions to the housing credit bubble prior to 2007. And it is expressed in the fact that global private sector debt has not fallen at all since the onset of the Great Recession. Instead, debt has been piled up as a cheap way of sustaining capitalist economies. This successfully ‘saved’ the banks, although it has not restored profitable investment and faster growth in the productive sectors of the major economies. This is US corporate debt to GDP below.

This brings me to a recent discussion about the role and relevance of stock markets to the capitalist economy conducted by the two leading mainstream economic exponents of stock market theory from Chicago University: Eugene Fama and Richard Thaler. Both are Nobel prize winners in economics. Fama is famous for his so-called Efficient Markets Hypothesis (EMH) and Thaler is a renowned ‘behavioural economist’. The debate between the two is really about whether the stock market provides a good guide to what is happening in a capitalist economy or whether it is totally volatile and ‘irrational’.

Fama says that EMH explains that capitalist markets, including stock markets, are ‘efficient’ in the sense that the price reflects what buyers and sellers reckon is right given the information before them. Well, that does not sound very profound. And is it true? Fama says “testing the proposition is difficult”! But, he says, it is a good approximation to what is going on. So if stock prices are high and rising, it means that investors think the economy is doing better (given the information they have) and they may well be right.

Thaler, on the other hand, reckons that stock market prices are so volatile that there is no rational explanation of their movements; they can reflect ‘bubbles’ based on what another ‘behavioural’ colleague of Thaler’s, Robert Shiller, called ‘irrational exuberance’. Thaler cites the huge fall in stock prices in the crash of 1987. There was no basis for the crash in the ‘real economy’ which was doing well. Fama’s reply is that people thought there was an economic recession coming on, but they were wrong and then the stock market corrected itself. The crash of 1987, “In hindsight, that was a big mistake; but in hindsight, every price is wrong.” People change their minds.

Thaler argues that there are ‘bubbles’, which he considers are ‘irrational’ movements in prices not related to fundamentals like profits or interest rates. Fama’s reply is that you cannot tell if there is a ‘bubble’ before it happens, only in hindsight and the bubble in prices may merely express a change in view of investors about prospective investment returns, not ‘irrationality’. In this sense, Fama is right and Thaler is wrong.

But that is not very helpful to the rest of us to understand what is happening and what stock markets are doing. Fama is (in)famous for stating after the Great Recession that you cannot predict crashes or slumps and we should not even try (see my The causes of the Great Recession). Just accept that they happen. Thaler is telling us that crashes and slumps are caused by ‘irrationality’ and not by any fundamental developments in the wider economy. Neither mainstream economic theory offers any help, then.

Thaler says the answer is for the monetary authorities to intervene “but very gently” to “lean against the wind a bit. That’s as far as I would go. We both agree that markets, good or bad, are the best thing we’ve got going. Nobody has devised a way of allocating resources that’s better.” In contrast, Fama reckons government or central bank intervention to control market prices (that are broadly ‘efficient’) is “likely to cause more harm than good.”

So, in effect, both Fama and Thaler accept that markets rule and that market prices broadly allocate resources efficiently and ‘rationally’, except that Thaler wants to understand why people act sometimes differently than Fama’s ‘rational’ model. Fama summed up their conclusions in the debate: “In general, it would be useful to know to what extent all economic outcomes are due to rational and irrational interplays. We don’t really know that.” So the great Nobel prize winners don’t know much about why stock prices move up and down, often with no relation to the movement of key economic fundamentals like profits, investment, labour costs etc.

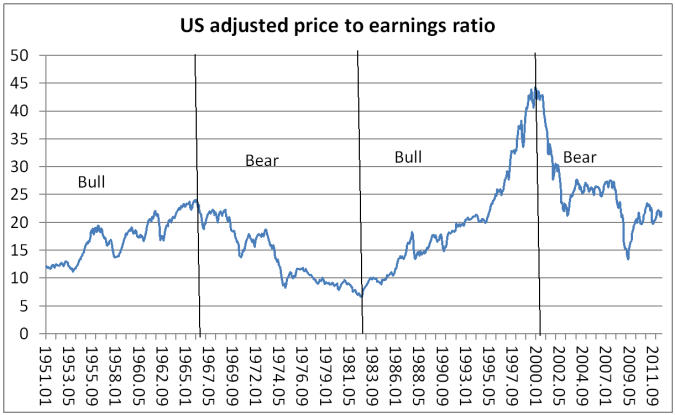

If we consider the movement of stock market prices from the point of view of Marxist analysis, then it is not so mysterious. In previous posts, I have dealt with this issue. As I said in one post: “Whatever the fluctuation in stock prices, eventually the value of a company must be judged by investors for its ability to make profits. A company’s stock price can get way out of line with the accumulated value of its stock of real assets or its earnings, but eventually the price will be dragged back into line. Indeed, if we consider stock price indexes (ie an index of an aggregated group of individual stock prices) over the long term, they exhibit clear cycles, with up phases called bull markets and down phases called bear markets. And these bull and bear markets, at least in the US, match nicely the movement in the rate of profit”.

In Robert Shiller’s own measure of stock market prices relative to profits (below), we can see that stock market prices generally move with profitability, but they can get way out of line for period. Right now they are still higher than they were in the last ‘bear’ market.

Marx made the key observation that what drives stock market prices is the difference between interest rates and the overall rate of profit. What has kept stock market prices rising now has been the very low level of long-term interest rates, deliberately engendered by central banks like the Federal Reserve around the world, with zero short-term rates and quantitative easing (buying financial assets with credit injections). The gap between returns on investing in the stock market and the cost of borrowing to do it is thus maintained.

In his recent opus, Capitalism, Anwar Shaikh looks at the theory of financial prices. (Chapter 10). Of course, every day, investors make ‘irrational’ decisions but, over time and, in the aggregate, investor decisions to buy or to sell stocks or bonds will be based on the return they have received (in interest or dividends) and the prices of bonds and stocks will move accordingly. And those returns ultimately depend on the difference between the profitability of capital invested in the economy and the costs of providing finance.

So this has less to do with ‘monopoly pricing’ as Krugman thinks and much more to do with the expansion of ‘fictitious capital’ relative to the profitability of capital as a whole. And less to do with Keynes’s view, which reckons that stock market prices are driven by subjective ‘animal spirits’ and more to do with the objective level of profitability.

If stock prices get way out of line with the profitability of capital in an economy, then eventually they will fall back. The further out of line they are, the bigger the eventual fall. That is what we can expect now.

Well they’ve given the Nobel Peace Prize to war criminals so why not economic prizes to people who have done nothing but apologize for the system?

It seems quite beside the point to talk about “investors” in a market where the vast majority of trades are carried out by computers for whom the “long run” is measured in seconds. It seems quaint to talk about interest rate/profit ratios in a market rigged by criminal insiders using “buybacks” and accounting fraud to enrich themselves at the expense of the nominal “capitalist owners” so many of whom are pension funds locked into unsalable securities providing no economic return whatsoever no matter how high their quotations get pushed by the manipulators and their central banks.

There’s the adage that goes: Three things children should never see being made……

1. other children

2. sausage

3. money in the stock market

Krugman mentions that the most profitable companies in the US are Apple, Google and Microsoft. These companies have something in common not hard to observe. They are profitable despite the fact that they are not spending (CapEx), i.e. not expanding productive capacities, and sitting on cash (non-taxable because it is parked in tax-havens). This ‘paradox’ for Krugman and others is not such a paradox for some Marxists.

I agree with Michael’s analysis and his criticism of Krugman but I would like to add here John Smith book on imperialism and his notion of an imperialist labor theory of value. Michael covered this book in his blog so I won’t dwell on it.

While stock market prices are reaching historical levels (i.e. fictitious capital is fast and furiously expanding) Marxists should stop discussing the lack of correlation between fictitious and ‘real’ capital because what supports the former is the economic imperialism or the so-called globalization and super-exploitation, i.e. Apple’s profits from selling the iPhone in the US with $500 compared with Apple’s low organic composition necessary to sell and design it (stores and design offices) while production price is less than $200 where Fox Conn bears all the production costs.

The bottom line is that heterodox and even Marxist economists should stop wondering how it is possible to sustain profits without higher productive investments. When production is outsourced (made invisible in the West) and the organic composition of capital is low (or even missing in some sectors where western corporations employ contractors to produce whole goods, even attaching the price labels) combined with super-exploitation (s/v high) profits are immense (see John Smith’s iPhone case study); as such, the need for capex (productive investment) disappears.

Stock buybacks and high dividends remain the main ‘investments’ being possible due to high profits produced with low organic value composition of capital combined with historic low borrowing interest rates.”Marx made the key observation that what drives stock market prices is the difference between interest rates and the overall rate of profit.” This observation is valid but it needs to be added that the ‘overall’ rate of profit can’t be calculated within national economies. This is not trade anymore but global production where buyers control production. When c and v are close to zero or very low for Apple, Google, Microsoft, Nike, Starbucks, etc. then profits skyrocket.

Super-profits are produced in the global South and good profits based on speculation and low interest rates in the global North. The problem will be when ‘capitalism’ hits the fan in the global South and this model of accumulation won’t work anymore. Since 2008 crash many signs of this breakdown appeared.

Why so much fear on Chinese economy slowing down? Why so much talk about China’s exporting deflation or China’s economic policies? Why the military build up around Russia and China? Why energy prices not recovering after two years of slump? It seems that the world capitalist economies are in deep sh.t and energy consumption levels are low with no near future prospects to recover because the economy is sluggish. In Canada’s tar-sands land Alberta the depression is already felt at all levels. Check this post:

http://business.financialpost.com/news/property-post/landlords-scramble-to-fill-near-empty-skyscrapers-dotting-calgary-skyline-were-not-overbuilt-were-under-demolished?__lsa=152a-4bf6

As well as being interesting this is a very topical and well timed piece of research. There is an inflection point taking place in the markets as dividend yields on average are poised to fall below interest rates for the first time in decades. This happened in both 1929 and 1959, the former led to the Great Depression while the latter did not. 2016 is more complex because at no time in history has there been so much idle capital both in relative and absolute terms. Larry Fink of Black Stone should know. As head of the world’s largest asset manager ($4.9trillion) he has a unique perch from which to view the markets. On the 14th July he told CNBC that $55 trillion in cash had piled up on the side-lines of the market. That compares to just $3 trillion involved in the housing market crash of 2008. That $55 trillion in unspent surplus is sufficient to produce 300 million jobs and end the need for migration. Fink is concerned that the profit outlook may undermine this cash pile with unknown consequences for the world economy. Capitalism remains precariously balanced.

While it appears that the US economy improves as far as coffee and pretzels goes, there are more disturbing undertones. US car sales are down 5% on an annualised basis and this was before the US justice department brought criminal actions against Chrysler and BMW for padding their sales figures. Ford could be in the firing line as well given its over large fleet sales. Clearly the oil refiners were duped by the sales figures, for having prepared for a bumper driving season this summer, the US is drowning in petrol which is one of the reasons oil prices have now resumed a downward path. Like the roads, things are not much better up in the air. At Farnborough this year, one of the premier sales events for aircraft manufacturers, orders were down 21% on last year. High end condominiums, the star performer in the housing markets, are becoming more difficult to sell. It is therefore the case that more industries are joining the already fallen, most notably smartphones.

On the 21st of July, the BEA publishes the GO and GV figures for the first quarter 2016, enabling the compilation of the rate of turnover and of surplus value. Shortly after that date I intend to publish a new posting analysing this data on the planningmotive.com In addition, the BEA has finally published GO figures going back to 1947 allowing turnovers, rates of surplus value, composition of capital and an actual rate of profit to be extended backwards by an additional 40 years. I suspect they have done so because of the growing interest in Gross Output and its relation to Gross Value added in academic (Non-Marxist) circles.

Dividend rates falling below interest rates? Negative interest rates are popping up all over the place as the central banks try to limbo beneath their “zero lower bound” policies of the past seven years. But I’ve yet to see a negative dividend rate anywhere in the world.

It is confusing which is why I deliberately used the term on average and referred to the USA where interest rates remain positive while dividend yields are falling. There is much debate currently in the financial press about this inflection point which is useful to follow. In any case, if any website has been writing about the scissors effect between corporate cash flow and investment effecting interest rates it is my site which is why I have always argued that currently debt is not an issue, fictitious capital is. Debt will only become important were interest rates to rise which is unlikely in the near future.