China’s reaction to Donald Trump’s trade war has been to retaliate with its own tariffs on US exports to China, particularly agricultural/food exports like soybeans. Also the government has allowed the Chinese currency, the yuan, to depreciate towards the bottom of its controlled range against the dollar. This makes Chinese exports cheaper in dollar terms and so defeats the purpose of Trump’s tariff increases on Chinese goods coming into the US.

But there is a third move: a considered expansion in government investment in and funding of construction projects to boost domestic output to compensate for any decline in exports. The policy of government investment was hugely successful in helping the Chinese economy avoid the consequences of the Great Recession back in 2008-9. While all the major capitalist economies suffered a contraction in national output and investment, China continued to grow. In 2009, when GDP in the advanced countries fell by 3.4%, Chinese growth was 9.1%. Only one capitalist economy also grew – Australia – an economy increasingly dependent on exports of its raw material resources to its fast-growing Asian giant neighbour.

Simon Wren-Lewis, leading British Keynesian economist and blogger, claims that China’s success in the Great Recession demonstrated two things: 1) that it was austerity that caused the Great Recession and the weak economic recovery afterwards in the major capitalist economies and 2) it was Keynesian policies (ie more government spending and running budget deficits) that enabled China to avoid the slump.

Well, it is no doubt true that after a massive slump in investment and production in the capitalist sector of the major economies in 2008-9, cutting back further on government spending would make the situation worse. In that sense, ‘austerity’ was a wrong-headed policy for governments to adopt. But as I have argued in many previous posts, austerity was not some insanity in economic terms for capitalism, as the Keynesians think. It has a rational base: namely that with profitability in the capitalist sector very low, costs must be reduced and that includes reducing taxation of the capitalist sector. Also the financial sector had to be bailed out. It was much better to pay for that by reducing government spending and investment rather than raising taxes. And the huge increase in public debt that resulted anyway would require controlling down the road.

But what about getting economies out of the slump with more government spending? Wren-Lewis comments “China is a good example of that idea in action. What about all the naysayers who predicted financial disaster if this was done? Well there was a mini-crisis in China half a dozen years later, but it is hard to connect it back to stimulus spending and it had little impact on Chinese growth. What about the huge burden on future generations that such stimulus spending would create? Thanks to that programme, China now has a high speed rail network and is a global leader in railway construction.”

So you see, Keynesian policies work, as China shows, says Wren-Lewis. But were China’s policies really Keynesian? Strictly speaking, Keynesian macro management policies are increased government spending of any type (digging holes and filling them up again) in order ‘stimulate’ the capitalist sector to start investing and households to spend, not save, all through the effect of the ‘multiplier’.

Sure, Keynes talked about going further, with the ‘socialisation of investment’ as the last resort. But no government of Keynesian persuasion has ever adopted that policy (if it meant taking over capitalist investment with state investment). Indeed, the Wren-Lewis’s of this world never advocate or even mention the idea of the nationalisation or socialisation of capitalist sectors. For them, Keynesian policy is government spending to ‘stimulate demand’.

China’s policy in the Great Recession was not just ‘fiscal stimulus’ in the Keynesian sense, but outright government or state investment in the economy. It actually was ‘socialised investment’. Investment is the key here –as I have argued in many posts – not consumption or any form of spending by government. The Great Recession in the US economy was led and driven by a fall in capitalist investment, not in personal consumption or caused by ‘austerity’. In Europe,100% of the decline in GDP was due to a fall in fixed investment.

As John Ross said on his blog at the time, “China is evidently the mirror image of the US …If the Great Recession in the US was caused by a precipitate fall in fixed investment, China’s avoidance of recession, and its rapid economic growth, was driven by the rise in fixed investment. Given this contrast, the reason for the difference in performance between the US and Chinese economies during the financial crisis is evident.”

Wren-Lewis thinks that Keynesian measures would have done the trick and it was “a failure of imagination” by the governments of major economies not to act, but instead impose ‘austerity’.

It’s true that the governments of the major capitalist economies did not follow China’s example partly because they were ideologically opposed to state investment – indeed, their first measure of ‘austerity’ was to cut government investment projects – the quickest way to cut spending.

But the main issue was not ideology or a “lack of imagination”. It is that Keynesian stimulus policies do not work in a predominantly capitalist economy where the profitability of capitalist investment is very low and so investment is falling. With government investment in advanced capitalist economies only around 3% of GDP compared to capitalist sector investment of 15%-plus, it would take a massive switch to the public sector to have an effect. ‘Stimulating’ capitalist investment with low interest rates and welfare spending would not be enough. Capitalist investment would have to be replaced by state ‘socialised’ investment. That only has happened (temporarily) in war economies (as 1940-45). In the last ten years, in the US, Europe and Japan, it has been capitalists who made the decisions on investment and employment and they did so on the basis of profit not economic recovery. Quantitative easing and fiscal stimulus – the two Keynesian policy planks – were ineffective as a result. In contrast, China’s fixed investment increased rapidly because it was driven by a programme of both direct state investment and use of state owned banks to rapidly expand company financing.

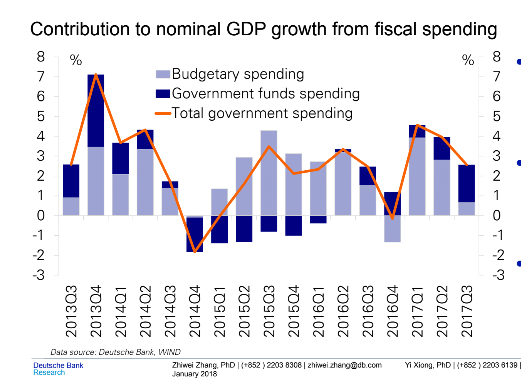

This difference between Keynesian measures in capitalist economies and China’s state-directed investment is about to be tested again. Most mainstream economists are predicting that China will take a hit from any trade war with Trump’s America and economic growth is set to slow – indeed, there is a growing risk of a huge debt-induced slump. But the Chinese authorities are already reacting. Ordinary budget deficits (fiscal ‘stimulus’) are being supplemented with outright state funding of investment projects (dark blue in graph).

Most of this government investment funding is coming from sales of land by local authorities. Through local government funding vehicles (LGFV), they build roads, homes, cities by selling land to developers. But funds also come directly from the national government (80%).

We can expect such funding to rise and investment projects to expand if China’s exports drop back from a trade war with the US. State investment will keep China’s economy motoring, while the major capitalist economies flounder.

Michael, what do you make of this and can you suggest a blog or two of susbstance on this important issue?

https://www.forbes.com/sites/panosmourdoukoutas/2018/08/04/china-is-treating-africa-the-same-way-european-colonists-did/#53711993298b

A question: isn’t enought to use “China’s state-directed investment”? On what basis the word “socialist” in added?

see https://thenextrecession.wordpress.com/2018/06/07/china-workshop-challenging-the-misconceptions/

Simon Wren-Lewis’ error of judgement comes from the failed presupposition that capitalism is an equilibrium-state system (the infamous “Phillips Curve” et al).

He states that, when a crisis happens, there’s a minus that must be compensated by a plus (government spending). But government spending is another minus, so, by rule, there must be a hidden element that compensates this with another plus: enter the “multiplier”.

About China, it’s important to highlight that, when the government “sells” land, it is not selling it in the capitalist sense: it is a 70-year lease. All Chinese land is property of the Chinese government (i.e. people). People only use land, they never own it. And yes, it hasn’t stopped land prices in China to skyrocket in tier 1 cities (Shanghai, Beijing etc.) because, in this 70-year period, you can resell as if it was yours.

Leases are the economic instrument because they alone attract surplus value, not the state freehold. That is why there is a market for these leases. The state held on to the freehold simply to regulate the creation of leases. Without a doubt, long before these leases expire they will be converted into freeholds.

It changes everything because you can’t inherit the land, only the lease. Without inheritance, there’s no private property, therefore there’s no capital, therefore there’s no capitalism.

The lease is with the government, not with the lease-owner. The 70 year period doesn’t reset when the lease-owner resells it.

Of course, no one has a crystal ball: in 70 years, there may be a counter revolution in China in those leases become genuine property. But I’m talking about now, 2018.

If Keynesian theory can include socialized investment as in China’s example, even if capitalists do it only as a “last resort”, why couldn’t a capitalist, or even progressive liberal “socialist”, advocate for and successfully save a foundering capitalist economy (as it sinks because of its depedency on increased profitablity when it historically falls)? Why would someone have to argue for a “Marxist” solution if a capitalist “socialized investment” solution would suffice? Or, are you arguing, as I might, that such socialized investment under capitalism would be an appropriate transitional program to win workers and their allies toward?

I think you have it -if ‘socialised investment’ means that the capitalist mode of production is replaced. Of course, Keynes dd not mean that.

Michael can you explain more this sentence? “Capitalist investment would have to be replaced by state ‘socialised’ investment. That only has happened (temporarily) in war economies (as 1940-45).” In other words, the public investments that took place from the 1940s in capitalist economies (in both developing and developed ones) side by side with privete ones are not the same type of China’s investment strategy nowadays? What is the basic difference? Do you think China is replacing all private investment by public ones?

When public/state investment dominates an economy, the law of value loses its dominance (at least domestically). Only in the war, did that happen in Europe and the US. Before, capitalist investment for profit through the market dominated. And it does now in 2018. I have shown in previous posts, that China has the largest stock of state-owned assets of all major economies and state companies/assets dominate the ‘commanding heights’ of the economy. However, in the last decade or so, private sector investment has overtaken state investment. That will increase the power of the law of value.

https://thenextrecession.wordpress.com/2017/10/25/xi-takes-full-control-of-chinas-future/

Ok, now I see. Thanks for that answer and the link also.

“State investment will keep China’s economy motoring, while the major capitalist economies flounder” is your concluding remark. I cannot agree with this. No capitalist economy can ignore the rate of profit. It alone determines whether more profits will return than the capital invested. If less profits are returned, then instead of capital-accumulation, we have capital-destruction. This always appears as a growing debt problem because to maintain or increase production more capital has to be borrowed to prop up reproduction.

This is always the limiting factor and the flaw in the Keynesian architecture. Of course in the short term government spending can end a realisation crisis due to a fall in investment. But in the longer term if government intervention subsidises unprofitable investments, as in the case of China, it means throwing good money after bad, inflating the problem. That is why investment is unfocused and wasteful in China. I have tried to deal with these problems in a recent posting

Click to access chinas-debt-problems-need-to-be-resolved-pdf.pdf

Finally, in the contest between China and the USA both heavyweights have glass jaws. The only thing keeping them upright is that workers are sitting outside the ring rather than jumping in. But what Trump is unleashing could very well create the conditions both within China and the US where workers will be forced out of their seats.

Your piece on China’s debt problems is very enlightening. I read it with interest. But where is the quarrel? You and Roberts seem to view China similarly.

Maybe the root of your quarrel is dialectical. Michael takes the more positive view in trying to understand the historical dialectic of the Chinese revolution, while remaining dialectical (critical), leaving space for open-ended, historical development; whereas your more strongly negative dialectic is short-circuited by your characterization of the Chinese state as “stalinist”, which pins China in static space like a dead butterfly.

“Stalinist”/”Stalinism” has been used, from a certain teleological perspective, as the pure (ahistorical) negation of revolutionary possibility–as if neither Russia nor China had (or might as well as not have) had revolutions, since they are now only dead-end, distorted, capitalist states.

Marx, unlike Horatio and many marxists, learned something from Hamlet.

I’m replying to my own comment, but it is really directed at jlowry:

The burden of ending “capitalism” is not on its colonial/imperial victims who managed, momentarily, to escape (because they had to) from the law of value, but is and always has been on the working classes at the imperial centers. In this (admittedly dialectically ironical) sense, it is we (western workers and our leaders) who have “betrayed the revolution”–not Bolsheviks, Stalinists, Maoists, etc.

It seems that all the contradictions have now (finally!) come home to roost. What you denounce in China is doubly true for every Nato country–all waging war on their own working classes while fomenting war between and on their traditional colonial/imperial victims.

We must resist all these wars by working to end capitalism at home.

”I’m replying to my own comment, but it is really directed at jlowry:”

It is not clear to me what you take exception to in my posts.

I agree that ‘betrayal of the revolution’ is a conceptual dead end. For me ‘Stalinism’ etc. is a kind of ‘diabolos ex machina’ for those whose revolutions have ended in a theoretical cul-de-sac. The problem with Trotsky’s critique to take one example is that, stripped of his brilliant rhetoric, it is not critical enough by a long way.

What I am condemning is the thesis that juridical status is fundamentally decisive in social analysis. Mao himself gave a good example:”In China women have been given equal status in law with men; so what? Nothing has changed!

This is intended to answer Jlowrie’s question as to what I’m taking exception to in his posts here. It’s the political implications (no doubt not intended) of statements like the one regarding China as being led by “…a government that is hurling towards an ecological apocalypse.”

Why focus on China particularly as heading towards an ecological apocalypse when the destructively productive proclivities of the imperial “West” (led by the military and nuclear hegemonic US) have already pushed the entire planet halfway down the edge of an ecological abyss, and which now substantively threatens China (and the other revolutionary “cul de sac” state, Russia) with nuclear war?

Is China (as a still developing, dictatorial? “capitalist” state) ecologically more dangerous than (the infinitely more aggressive and rich in capital and military assets) “democratic” West? You seem to imply that this is so. This implication lends credence to present imperial war preparations against both Russia and China–just as “cruel dictatorship” implications (particularly by self-styled “socialist” leaders) have lent credence to color revolution quasi-fascist coups in Eastern Europe, and to direct and proxy imperial wars on Afghanistan, Iraq, Libya, and Syria, and now maybe Venezuela.

I agree with you about what needs to be done in China (and what perhaps you believe could have been done in the Soviet Union, what should be done in Venezuela). But nothing substantive can be done to end planetary destruction and bring about socialism anywhere without ending the increasingly aggressive and destructive capitalism in the West.

The scattered/shattered “left” hasn’t even succeeded in being clear about imperialism and resisting our own dictatorial regimes’ war on the Earth and its working populations. Leave China to the Chinese. Whatever the nature of the present Chinese state, it cannot be more ecologically/militarily destructive than the imperial West, which has been about the rapaciously accumulative job much much longer.

”Why focus on China particularly as heading towards an ecological apocalypse?” Well, Michael’s post was focused on China.

If you had read my further comments below, you would readily have ascertained that I, following the analysis of certain eminent scientists, readily see capitalism per se as hurling humankind headlong towards an ecological apocalypse. I do not see on what grounds we should exempt the contribution of the new Chinese capitalist class to the imminent extinction of humanity.

I should refer you to the Chinese Marxist, Minqi Li’s, ”China and the 21st century Crisis,” particularly Ch. 7 ‘The Unsustainability of Chinese Capitalism’.

It may well have been in this book that Minqi argues that in the future China will be able to support a population of only 500 million, and this would require a huge population return to the countryside.

I guess he is something in the way of an optimist!

As for your other comments, I find myself mostly in agreement.

Yes, the Chinese state has the power to keep consumption, both private and social welfare, very low as a percentage of output. But China does not allocate investment according to a unified plan. A huge percentage of it now sits as buildings and half-built structures that serve no economic function and will not for many years. China also expanded output of steel and other commodities that it has been able to dump onto European and other markets. “State investment will keep China’s economy motoring.”

“But China does not allocate investment according to a unified plan.”

Except it does: http://www.china-un.org/eng/zt/China123456/

No form of government is perfect. There will always be setbacks. Yes, many government projects ended up in failures in China, but, overall, it is still the best the Chinese can have now.

“But China does not allocate investment according to a unified plan.”

Does this mean that South Korea has also been a ‘socialist’ state? President Park, formerly known as lieutenant Takagi Masao of the Japanese army, recipient of a gold watch from the genocidal Emperor Hirohito in person for his part in suppressing communists leading the anti-Japanese struggle in Korea, when he seized power introduced a series of five-year plans prepared by an economic Planning Board. The government owned all the banks and some big projects were directly undertaken by state enterprises e.g. the steel maker, Posco. Moreover the illegal export of capital could be punished by death. Can’t see such a laudable policy being introduced in China any time soon, can you?

The Chinese government make no secret of their intention to further the development of capitalist agriculture and the consequent further expropriation of the peasant ( Zhun Xu, ”From Commune to Capitalism” 2018).

Virgens should not confuse juridical status with real economic relations of production i.e. who has the power. Land is becoming a commodity in China. Whatever the legal status of the peasants’ land it will to no more to protect them than it did the copyholders in precapitalist England. It is the intention of the Chinese, as of the Indian, bourgeoisie further to drive the peasants from their land into gigantic metropoles. Now can anyone recall the name of the distinguished American scientist who has affirmed that a sustainable mega-city is an oxymoron?

”No form of government is perfect…. it is still the best the Chinese can have now.” No it is the worst! How about a democratic one i. e. a government of the unpropertied and not of an obscene plutocracy that is hurling China towards an ecological apocalypse!

Further to the above:

By 2050 the percentage of the world’s population living in cities is expected to rise to 75%.

Dr William Rees, who along with Mathis Wackernagel, created the concept of ecological footprint analysis ( and what a great contribution to scientific socialism ), describes modern cities as entropic black holes. Tokyo requires an area twice the size of Japan to sustain it. In fact affirms Rees :sustainable cities is an oxymoron”! They are excellent for population surveillance and urban militarisation though. I have read China is contemplating an urban area of 100 million!

The Deep Adaptation Agenda is discussed in detail starting on page 18 of Bendell’s dissertation, which is readily available at: http://www.lifeworth.com/deepadaptation.pdf.

As for his conclusion: “Disruptive impacts from climate change are now inevitable. Geoengineering is likely to be ineffective or counter-productive. Therefore, the mainstream climate policy community now recognizes the need to work much more on adaptation to the effects of climate change… societies will experience disruptions to their basic functioning within less than ten years due to climate stress. Such disruptions include increased levels of malnutrition, starvation, disease, civil conflict and war – and will not avoid affluent nations.”

For a detailed discussion cf the article by Robert Hunziker in Counterpunch 3/8/18.

Professor Bendell makes it absolutely clear: climate scientists play down the social implications of their scientific discoveries in order not to alarm people. It is already too late. As he says, one day people will wake up to find no water coming out of their taps. In China this day is not distant. But Hey! Let them drink coke!

Sorry, VK, didn’t see a word about unified allocation of investment in the puffery at the link you dropped on us. But you’ll find a brief history of how China abandoned Plans at

http://www.munich-business-school.de/insights/en/2016/five-year-plans-china/

Michael

Great discussion.

For those of us who are trying to develop a deeper understanding of why Keynesian theory and policy is wrong-headed, can you recommend any books or articles?

Mike

I like Paul Mattick

https://www.marxists.org/archive/mattick-paul/1955/keynes.htm

https://www.marxists.org/archive/mattick-paul/1969/marx-keynes/index.htm

Nicholas Wapshott Keynes and Hayek

Geoff Pilling https://www.marxists.org/archive/pilling/works/keynes/index.htm

Geoff Mann https://www.versobooks.com/books/2245-in-the-long-run-we-are-all-dead

Bruce Bartlett https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2838926

Click to access bartlett.pdf

Dear Michael, Why doesn’t Martin Wolffe describe the Chinese policies of the previous ten years as Keynesian?

Foo Wong

On Mon, 6 Aug 2018 at 10:45, Michael Roberts Blog wrote:

> michael roberts posted: “China’s reaction to Donald Trump’s trade war has > been to retaliate with its own tariffs on US exports to China, particularly > agricultural/food exports like soybeans. Also the government has allowed > the Chinese currency, the yuan, to depreciate towards th” >

Marx used “socialism” and “communism” as synonyms for the classless society. “Orthodox” Marxist that I am, I’d never call China “socialist.” (Socialism in one country is utopian anyway — Engels made this clear back in 1847, and for good reason.)

But yes, China is peculiar — a peculiar, statified capitalism (I don’t know what else to call it) but peculiar.

https://www.wsj.com/articles/collapsing-investment-doesnt-mean-collapsing-china-1537157393