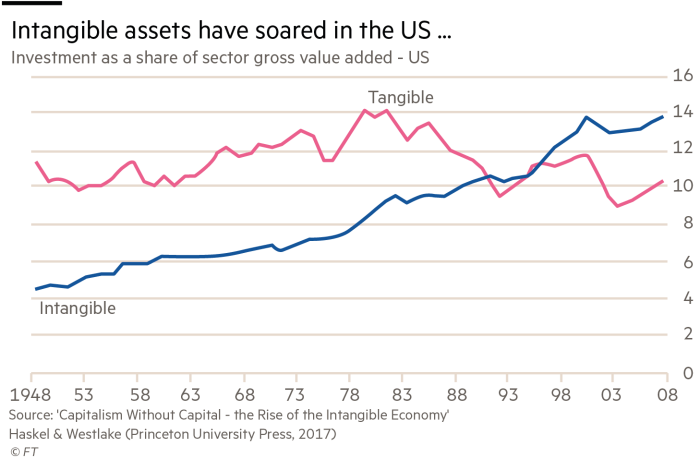

There is a new book out called Capitalism without capital – the rise of the intangible economy. The authors, by Jonathan Haskel of Imperial College and Stian Westlake of Nesta, are out to emphasise a big change in the nature of modern capital accumulation – namely that increasingly investment by large and small companies is not in what are called tangible assets, machines, factories, offices etc but in ‘intangibles’, research and development, software, databases, branding and design. This is where investment is rising fast relative to investment in material items.

The authors call this capitalism without capital. But of course, this is using ‘capital’ in its physicalist sense, not as a mode of production and social relation, as Marxist theory uses the word. For Marxist theory what matters is the exploitive relation between the owners of the means of production (tangible and intangible) and the producers of value, whether they are manual or ‘mental’ workers.

As G Carchedi has explained, there is no fundamental distinction between manual and mental labour in explaining exploitation under capitalism. Capitalism cannot be without capital in that sense.

Knowledge is produced by mental labour but this is not ultimately different from manual labour. Both entail expenditure of human energy. The human brain, we are told, consumes 20% of all the energy we derive from nourishment and the development of knowledge in the brain produces material changes in the nervous system and synaptic changes which can be measured. Once the material nature of knowledge is established, the material nature of mental work follows. Productive labour (whether manual or mental) transforms existing use-values into new use-values (realised in exchange value). Mental labour is labour transforming mental use values into new mental use values. Manual labour consists of objective transformations of the world outside us; mental labour of transformations of our perception and knowledge of that world. But both are material.

The point is that discoveries, generally now made by teams of mental workers, are appropriated by capital and controlled by patents, by intellectual property or similar means. Production of knowledge is directed towards profit. Medical research, for example, is directed towards developing medicines to treat disease, not preventing disease, agricultural research is directed to developing plant types which capital can own and control, rather than relieving starvation.

What Haskell and Westlake find is that investment in intangible assets now exceeds that in tangible assets.

And they reckon this is changing the nature of modern capitalism. Indeed, it could expose the uselessness of the so-called market economy. The argument is that an intangible asset (like a piece of software) can be used over and over again at low cost and allow a business to grow very fast. That’s an exaggeration, of course, because tangible assets like machines can also be used over again, but it’s true that they have ‘wear and tear’ and depreciation. But then software also gets out of date and also becomes ‘tired’ for the continually changing purposes required.

Indeed, the ‘moral depreciation’ of intangibles is probably even greater than tangibles and so increases the contradictions of capitalist accumulation. For an individual capitalist, protecting profit gained from a new piece of research or software, or the branding of a company, becomes much more difficult when software can easily be replicated and brands copied.

Brett Christophers showed in his book, The Great Leveller, capitalism is continually facing a dynamic tension between the underlying forces of competition and monopoly. “Monopoly produces competition, competition produces monopoly” (Marx).

That’s why companies are keen on intellectual property rights (IPR). But IPR is actually inefficient in developing production. ‘Spillover’, as the authors call it, where the benefit of any new discovery is shared in the community, is more productive, but by definition almost, is only possible outside capitalism and private profit – in other words rather than capitalism without capital; it becomes capital without capitalism.

As Martin Wolf of the FT concludes in his analysis of the rise of ‘intangibles’, “intangibles exhibit synergies. This goes against the spillovers. Synergies encourage inter-firm co-operation (or outright mergers), while spillovers are likely to discourage it. Who really wants to give a free lunch to competitors?” So “Taken together, these features explain two other core features of the intangible economy: uncertainty and contestedness. The market economy ceases to function in the familiar ways.”

Under capitalism, the rise of intangible investment is leading to increased inequality between capitalists. The leading companies are controlling the development of ideas, research and design and blocking ‘spillover’ to others. The FANGs are gaining monopoly rents as a result, but at the expense of the profitability of others, reducing them to zombie status (just covering their debts without the ability to expand or invest).

Indeed, the control of intangibles by a small number of mega companies could well be weakening the ability to find new ideas and develop them. Research productivity is declining at a rate of about 6.8 per cent per year in the semiconductor industry. In other words, we’re running out of ideas. That’s the conclusion of economic researchers from Stanford University and the Massachusetts Institute of Technology Innovation. They reckon that in order to maintain Moore’s Law – by which transistor density doubles every two years or so – it now takes 18 times as many scientists as it did in the 1970s. That means each researcher’s output today is 18 times less effective in terms of generating economic value than it was several decades ago.

Thus we have the position where the new leading sectors are increasingly investing in intangibles while investment overall falls along with productivity and profitability. Marx’s law of profitability is not modified but intensified.

The rise of intangibles means the increased concentration and centralisation of capital. Capital without capitalism becomes a socialist imperative.

Also to be noted: concurrent with use of intangibles was tax avoidance. Affecting governments too. The reaction was global (including the US, but not well publicized as party to OECD BEPS). A lot of what is being said about “territorial” taxation was already being well developed, long before the present actor/occupant of presidency took office.

Michael, you might be interested in the following texts, which are confronting similar arguments as advanced by “post-operaismo” theorists (Negri et. al):

Teresa L. Ebert and Mas’ud Zavarzadeh, “The Digital Metaphysics of Cognitive Capitalism: Abandoning Dialectics, the North Atlantic Left Invents a Spontaneous Communism within Capitalism.” http://www.tandfonline.com/doi/full/10.1080/21598282.2014.954310

Rob Wilkie, The Digital Condition. https://www.fordhampress.com/9780823234233/the-digital-condition/

This is surely being overplayed, the so called intangibles are still a marginal part of the story even if they are rising.

Actually I don’t believe in intangibles, i.e. things that can’t be quantified in any way. This would make intangibles magic, belonging to the realm of sorcerers and wizards and not the preserve of science. I strongly disagree with this.

So software can be reproduced at nearly zero cost (not true actually) but if that is the case so can a bouncy ball. Is a bouncy ball intangible?

I saw a report recently about the slave like practices that Amazon, one of the world’s most hi tech companies, subjects its workers to. Right out of Dickens it was. The idea that capitalism is built on intangibles is pure propaganda to paint a rosy picture of modern day capitalism and hide the horrors.

But the big error as far as I am concerned is the belief in intangibles. I say that anyone who believes in intangibles believes in fairies and is therefore telling fairy stories.

The form of a commodity is irrelevant. It can be tangible or intangible, of long duration or fleeting. The problem is the 2013 revision to the SNA which converted R&D and in-house software (including databases) from a cost into capital. To achieve this miraculous conversion the statistical bureaus took something which was not a commodity and turned it into a commodity by imagining up an imputed (non-existing) sale. With swift and deft swipes of the pen R&D and in-house software were transformed into commodity capital. Without this conjuring trick intangible capital would be two-thirds smaller, smaller by far than tangible capital and GDP would be 3% smaller. As aways it is not the form of a use value that matters, it is its social form, whether it has been produced for sale.

You write:

“The authors call this capitalism without capital. But of course, this is using ‘capital’ in its physicalist sense, not as a mode of production and social relation, as Marxist theory uses the word. For Marxist theory what matters is the exploitive relation between the owners of the means of production (tangible and intangible) and the producers of value, whether they are manual or ‘mental’ workers.*

But intangible assets and tangible assets couldn’t be more different.

Intangible assets, unlike physical assets used in production, can play no role in value creation.

They don’t exist, from any perspective.

Tangible capital is politically contestable.

Intangible capital is empirically invalid.

This distinction can’t be elided.

“Intangible assets, unlike physical assets used in production, can play no role in value creation.”

Well that depends on how you define intangible, production and value!

Intangible: something that has no physical characteristics and therefore cannot be seen, touched, tasted, heard or smelt.

Production: the act of making something or creating a service

Value: this is found in a useful thing (ie with physical characteristics) or in a service (intangible) that makes you happier/the world a better place.Only people can create value. Things can’t.

So if I can sum up your position from those rather limited definitions, only people create value. Value can be embodied in physical and intangible things. In order to have physical or intangible things you need a production process of some kind. Only people and physical things can play a role in value creation, and while physical things can play a role in value creation they cannot in themselves create value but people in themselves can. Intangible things can only embody value but can play no role in value creation.

How to pick the bones out of that lot!

Give me a list of 10 intangibles and also do you regard research and development, software and databases as intangible?

“something that has no physical characteristics and therefore cannot be seen, touched, tasted, heard or smelt”

But isn’t the act of lifting an hammer partly intangible (based on your sensory definition), for example you cannot see, smell or taste the brain signal to the hand but if that did not happen the hammer would not get lifted?

“this is found in a useful thing (ie with physical characteristics)”

Why “ie with physical characteristics”? Why can’t something be a useful thing and be ‘intangible’? Why, for example, can’t the genome project be of economic value? Why can’t a teacher employed in the production of brain power be value creating? Also, why is it found in the first place, this value in this useful thing that is?

“Give me a list of 10 intangibles and also do you regard research and development, software and databases as intangible?”

An intangible is by definition something that has no physical/material characteristics. So a computer is tangible. Digital information stored on a hard disc is tangible. Education, healthcare, any form of advice etc is intangible. It has no physical form and only exists in our minds. If it exists outside the human mind, then it must be tangible.

“But isn’t the act of lifting an hammer partly intangible (based on your sensory definition), for example you cannot see, smell or taste the brain signal to the hand but if that did not happen the hammer would not get lifted?”

A hammer is a tangible. The human body is tangible. A physical thing made by a person using a hammer is tangible. But the use value of that work is intangible, since it depends upon the use to which it is put. For example, a flint 10,000 years ago had high use value. Today, it has none apart from as a curiosity.

Same physical thing. Different value in use which depends upon how the flint is subjectively perceived.

Exchange value is, as Marx explicitly stated, intangible.

“Why can’t something be a useful thing and be ‘intangible’?

If it’s intangible, it can’t be a thing. It’s an idea that might be shared but only exists in the mind.

If it’s a thing, then it’s a tangible.

“Why, for example, can’t the genome project be of economic value?”

The genome project has no value unless it’s used by people to support value creation, for example in improving health care. If it’s stored on a computer that no one uses or ever will, it serves no value-creating purpose.

“Why can’t a teacher employed in the production of brain power be value creating?”

Teachers create value but only in interaction with students and others with whom the teacher shares knowledge/brain power. Brain power can’t be separated from the person in whose brain that power is stored.

“Also, why is it found in the first place, this value in this useful thing that is?”

To clarify, logic leads to the conclusion that value is intangible and can only be subjectively defined. It is exclusively created through constructive human interaction. Tangibles support people creating value but cannot create value. Consequently, value can never be embodied in a tangible.

Well education and healthcare are quite broad categories. They are a summary of many processes, systems, relations etc etc. So let’s be more specific. But before we do that, this gets to a problem with the tangible and intangible contrast and a critical one at that as far as I am concerned, the things that are considered intangible are part of a bigger process that includes the physical and not so physical. For example when a finance advice company employs people to deliver financial advice the advisors don’t just speak with ‘intangible’ words, as they speak they might show you a ‘tangible’ graph or open a ‘tangible’ laptop and show you a ‘tangible’ calculation all the while offering ‘intangible’ advice. ‘Intangible’ advice moreover that can have very ‘tangible’ affects! The reverse is true, so called ‘tangible’ things also include a number of ‘intangible’ parts.

Anyway, the specifics:

So the words that come out of the teacher’s mouth are intangible but if those words are stored on disk then this becomes tangible. I am minded to ask, so what!

But we should ask if education passes any of the criteria you specified above, i.e. “Cannot be seen, touched, tasted, heard or smelt”

Well can’t you hear the words of the teacher and therefore isn’t this spoken knowledge by your definition tangible? Can’t this knowledge, held in the teachers mind, become a commodity?

A human body may be tangible but the synapses that connect parts of the brain are not under your definitions, you can’t have it both ways, if knowledge which stirs the brains synapses are not tangible, for example the advice of teachers, neither are the synapses that tell the brain to pick up the hammer.

“It’s an idea that might be shared but only exists in the mind.”

How can it be shared if it only exists in the mind? And moreover so what?

“The genome project has no value unless it’s used by people to support value creation, “

The actual outcome of the project is being sold as we speak, so its commodified before any concrete use has been found, it is being sold based on its potential use.

“Brain power can’t be separated from the person in whose brain that power is stored.”

Of course it can and it happens all the time! We call it exploitation!

“logic leads to the conclusion that value is intangible and can only be subjectively defined. “

Well then the logic is a non sequitur and therefore invalid! Length could be considered intangible, well at least by you, yet it facilitates the objective comparison of the length of things. But of course length is not ‘intangible’. And neither is value!

But moreover tangible or intangible, so what?

“So the words that come out of the teacher’s mouth are intangible but if those words are stored on disk then this becomes tangible. I am minded to ask, so what!”

——-The words are expressing ideas which are without physical characteristics. Electronic digits on a disc are physical and tangible.

“But we should ask if education passes any of the criteria you specified above, i.e. “Cannot be seen, touched, tasted, heard or smelt”

——Ideas can’t be seen, touched, tasted, heard or smelt.

“Well can’t you hear the words of the teacher and therefore isn’t this spoken knowledge by your definition tangible? Can’t this knowledge, held in the teachers mind, become a commodity?”

—–You can hear the words. So can a dog. The ideas the words express are something else.

—–Knowledge in a teachers mind can only become a commodity if the knowledge can be separated from the mind. But it can only be held in one mind or several. Knowledge outside a mind is as useful as cheese on the moon.

“A human body may be tangible but the synapses that connect parts of the brain are not under your definitions, you can’t have it both ways, if knowledge which stirs the brains synapses are not tangible, for example the advice of teachers, neither are the synapses that tell the brain to pick up the hammer.”

——–I’m not an expert on human biology and don’t need to be. Let us deal with one idea: inequality is bad. That’s intangible, although synapses etc support our capacity to understand and interpret it.

“It’s an idea that might be shared but only exists in the mind.”

“How can it be shared if it only exists in the mind? And moreover so what?”

———Sharing means me saying inequality is bad to someone and that person retaining that statement to share with others

“The genome project has no value unless it’s used by people to support value creation, “

“The actual outcome of the project is being sold as we speak, so its commodified before any concrete use has been found, it is being sold based on its potential use.”

———-The price being paid is based on a calculation of the net present value of the income stream it is expected/hoped to generate. That projection is an estimate/guess of what the future will bring and is definitively intangible.

“Brain power can’t be separated from the person in whose brain that power is stored.”

“Of course it can and it happens all the time! We call it exploitation!

——–That exploitation is only possible if an owner of capital can assert ownership over the human mind. This is is precisely what copyright and other forms of IPR do. It happens but is not inevitable. All intellectual property is legalised theft.

“logic leads to the conclusion that value is intangible and can only be subjectively defined. “

“Well then the logic is a non sequitur and therefore invalid! Length could be considered intangible, well at least by you, yet it facilitates the objective comparison of the length of things. But of course length is not ‘intangible’. And neither is value!”

———-Length is a relative concept and an idea that exists in the human mind. It is not a thing, like an apple.

“But moreover tangible or intangible, so what?”

——–The difference between the tangible and the intangible is intuitively, obviously, philosophically and semantically the greatest of all differences.

Lenin existed.

God, the existence of which has no supporting physical evidence, is a figment of human imagination.

Are you telling me there’s no difference between the two and if there is, it is of no consequence to the way the world is viewed?

”Intangible assets, unlike physical assets used in production, can play no role in value creation.”

How about scientific knowledge?

I refer to intangible assets as assets listed on the balance sheets of firms.

Scientific knowledge can only be used to create value when a person cognitively uses that knowledge. It cannot be separated from the person using that knowledge to create value. It is consequently solely an expression of the creativity of a person (in other words, it’s labour).

The only reason why scientific and any other form of knowledge are treated as balance sheet assets is because of laws and accounting codes devised to satisfy the needs of corporations. This is a matter of historic fact. Before copyright laws, which emerged in the West in the 18th century, it was impossible for an owner of capital to enforce a claim over knowledge.

”Scientific knowledge can only be used to create value when a person cognitively uses that knowledge. It cannot be separated from the person using that knowledge to create value.”

I am not convinced. Take two machines in the same factory feeding two assembly lines, but one of which incorporates the latest scientific knowledge. It is not clear to me that the workers on the latter assembly line would be cognitively using such knowledge ( I know I wouldn’t be) , which is the product of the scientific knowledge of the workers who constructed the machine in the first place. The machine might be quite sophisticated but the nature of the labour decidedly routine and mind numbing.

The cost of producing a bouncy ball is almost next to nothing, they can make a mobile phone for less than a $1 (ok they grab that back on calls).

Tangible, intangible! So what

Show me an intangible and I will show you a tangible.

Even goodwill can be measured, they don’t just make up a figure on the spot, the value of goodwill is calculated based on measures.

There are no intangibles! There is nothing beyond the wall!

Goodwill is a term originating in accounting.

It was invented so that a company could buy another company for more money than a book valuation of the acquired company justifies. For example, company A wants to buy company B which has a book value of $100m which can be derived from published balance sheet figures. In order to beat off competitors, company A decides to offer $110m.

You could say A is overpaying, but it normally manages to convince its auditors that the $10m is for value in B that is not recognised by conventional analysis. If that happens, A can list the $10m as goodwill, which is included in its balance sheet separately from the $100m book value of B.

How does A justify paying $10m more than available information shows? Simple: it does a calculation of B’s potential future profit stream based on the actions that A will apply to B after it’s bought. This separate stream of profit is valued using conventional methods and used as the amount above book value that A thinks B is worth.

This projection is based on forecasts, guesses and (often mainly) wishful thinking. It’s an expression of hope. It’s intangible.

The reality is that a growing majority of UK corporations have no or low tangible assets. Goodwill, brand values and IPR are growing. These have no physical characteristics and are obviously intangible.

“The reality is that a growing majority of UK corporations have no or low tangible assets. Goodwill, brand values and IPR are growing. These have no physical characteristics and are obviously intangible.”

Obviously, we must be able to quantify these intangibles otherwise we’d never be able to say that a growing majority of UK corporations have no or low tangible assets. So the challenge Edmund is for you to provide some actual quantities for your claim that a “growing majority of UK corporations have no or low tangible assets.”

So might I suggest you take something like equivalent to the US corporate register and, — by any measure you like– revenues, market valuation, gross property plant and equipment– show over a perioid of time the “growing majority” with no tangible assets. And maybe the growing portion of intangibles making up the general “capital stock” of all corporations.

I suspect you can’t do that. I suspect that any real investigation will show that the significance of intangible assets is greatly exaggerated.

On 31 December 2015, the 25 companies listed on the London Stock Exchange (LSE) with the biggest market capitalisation reported they owned £522bn worth of assets that were physical. Their other assets — types of intangible capital – were worth more than £5.3trn, accounting for 91 per cent of their total balance sheets. These figures are taken from the published balance sheets of the 25 companies.

The pattern of intangible asset ownership varies across FTSE25 companies. The five with the highest proportion of intangible assets (HSBC, Lloyds Bank, Barclays Bank, RBS and Prudential) work in financial services. All of them have more than 98 per cent of their assets held in intangible forms.

Companies with more than 60 per cent of their assets in intangibles comprise four consumer good/drinks manufacturers (Reckitt Beckinser, SabMiller, Diageo, Unilever); two cigarette firms (BAT and Imperial Brands); two telecoms firms (Vodafone and BT); three pharmaceutical/biochemical product firms (Shire, Astrazeneca and GSK) and one events, books and information firm (RELX). Only seven of the 25 had intangible assets worth less than 50 per cent of their balance sheets: BP, ABF, Shell, RTZ, National Grid, BHP and Carnival Corporation.

The aggregate intangible assets of the FTSE25 rose robustly in 2008 but fell by one-quarter in the subsequent seven years.

Despite the decline in the total assets of the FTSE25 after 2008, the proportion accounted for by intangibles in their balance sheets was comparatively stable in 2006-15. After reaching a peak of around 95 per cent in 2008, they drifted down to 91.5 per cent in 2015.

The dominance of intangible capital is due to many factors including:

• The increasing significance of service (intangible) production for all companies in advanced economies. Generally, service industries require fewer physical inputs and less tangible capital.

• Technical factors that have allowed companies to book intangibles as balance sheet assets. This is mainly the result of new approaches to dealing with intangible assets adopted by the accounting profession.

• The higher liquidity of intangible assets. This is attractive to corporations because it allows them to buy and sell intangible assets more quickly than tangible assets.

• A higher rate of return on intangible assets compared with the return attributable to tangible assets.

• Taxation. Corporations have greater capacity to minimise taxation on intangible assets and the income they generate, both of which can be reported in low-tax jurisdictions.

• Mergers and acquisitions. Companies buying other companies can define the amount paid above the fair value of the acquired company as an asset. This is listed as goodwill in corporate balance sheets.

• The creation of definable intangible assets (patents, copyrights etc) through internal research and development (R&D).

There is no reason to conclude that the dominance of intangible capital in the balance sheets of large corporations is not repeated in those of smaller and unlisted UK companies and in other advanced economies.

The word intangible is clearly being misused here! The distention between tangible and intangible is not a terminological step forward but a regression. I guess this is the point to be made.

What you are describing is the age old factitious capital, a capital that now has to ‘serve’ a world market rather than a local one, so of course there has been growth in this sector. But as a % of the ‘industrial’ sector is it that much bigger?

If you are saying that capitalism has fundamentally changed its form then I would say that is a premature and even then the change in form has jack shit to do with intangibles or fictitious capital.

A tangible has physical characteristics. It if doesn’t have physical characteristics, it can’t be tangible,

If it’s not tangible, it’s intangible.

Asset-backed securities, syndicated loans, underwriting, mortgages, puts, calls, options, foreign currency, etc have no physical characteristics unless you are referring to the material used for recording these and other financial promises.

I have a pound note but it’s not a tangible asset unless I was planning to eat it, burn it for heat or perhaps use it for protection or padding.

It’s a promise from the state that has to be exchanged if it is to make any contribution to the value creation process, unlike my trousers in which the fiver is now stored.

Oh Edmund, that just won’t do. Cash and cash type assets are not intangible assets. Open positions in trading markets– i.e. asset-backed securities, syndicated loans, underwriting, mortgages are not intangible assets, puts, calls, options, foreign currency, etc. are not intangible

I’m sorry that I didn’t ask you to define what you are designating as intangible assets, but better late than never.

The issue is conceptual rather than definitional.

Cash is usually legal tender, but it’s still intangible because it’s a promise underwritten by the state, a legal construct.

Financial instruments are not tangible assets. They are promises; ideas and intangible.

Imagine I have a cake ready to eat and you plan to bake an identical cake tomorrow. You want a cake now and I don’t mind having it tomorrow. I give you the cake and you promise to bake a cake tomorrow that you will give to me.

You now have the cake. I have the promise. It doesn’t matter if the promise is verbal, written on a piece of paper, etched in gold or an electronic digit, it’s still a promise: an idea and an intangible.

I can’t eat as I can the cake.

A tangible asset by definition must have a physical characteristic.

Financial instruments don’t unless you are counting the material used to write it down.

Practically all the assets held by banks are non-physical and therefore intangible. They cannot be used directly in the production process. They have to be exchanged first into a tangible asset.

Just like the promise to bake a cake.

As I said clearly a terminological regression.

Forget your trousers by the way, if you pay for financial advice from a company employing finance advisers then the advice now residing in your thoughts has contributed to value creation just as much as your trousers or your novelty sunglasses.

I’m with Edgar on this:

First off, what Edmund classifies– cash and securities– is not at all what Michael is referring to in his analysis. He specifies intangibles as knowledge based– software, r&d, design, branding (patents and trademarks)– items generally known as intellectual property.

Secondly, if cash and securities represent intangible assets, then all of capital is an intangible asset as the point of value, of capital accumulation, is the accumulation of capital AS money. So Edmund tells us the startling news that capital is today just like it was yesterday. Big f—ing deal.

Thirdly, the parable of the cake is nonsense. Asset backed securities, syndicated loans, mortgages– whatever are collateralized. Edmund thinks that’s imaginary? Look at 2008, 2009 and tell me that the bankruptcies, seizures, shutdowns, and government bailouts making bondholders whole were “intangible” and didn’t involve “tangible” items. I hold a lien on the cake. You don’t produce the cake? Guess what? I have the power of the whole state behind me. I seize your oven, your refrigerator, your entire kitchen and liquidate them to retrieve the value of the “intangible” cake. And you’re tangibly out of business.

“First off, what Edmund classifies– cash and securities– is not at all what Michael is referring to in his analysis. He specifies intangibles as knowledge based– software, r&d, design, branding (patents and trademarks)– items generally known as intellectual property.”

That seems to be the case. But intangibles should encompass all assets without physical characteristics. All financial instruments — including “cash” — are intangible because you have to exchange them if you want to a tangible (food, house, electricity, machinery, equipment).

“Secondly, if cash and securities represent intangible assets, then all of capital is an intangible asset as the point of value, of capital accumulation, is the accumulation of capital AS money. So Edmund tells us the startling news that capital is today just like it was yesterday. Big f—ing deal.”

As Michael has stated, capital is not a thing (a tangible) but a social relationship. It’s the way owners assert ownership over the means of production and exploit workers. The point being made is that capital expressed in physical assets and particularly in the means of production is qualitatively different from capital expressed in intangible assets which are promises to pay/enforceable claims with no physical characteristics. A machine making cars has a role in making cars. But how does a document saying the car-making company owes a shareholder money?

“Thirdly, the parable of the cake is nonsense. Asset backed securities, syndicated loans, mortgages– whatever are collateralized.” Edmund thinks that’s imaginary?”

Asset-backed securities, syndicate loans, mortgages are all promises to pay/rights to claim payments. As people with such assets have discovered through history, these are sometimes not worth the paper they are written on or the electronic digits they are expressed in.

Look at 2008, 2009 and tell me that the bankruptcies, seizures, shutdowns, and government bailouts making bondholders whole were “intangible” and didn’t involve “tangible” items. I hold a lien on the cake. You don’t produce the cake? Guess what? I have the power of the whole state behind me. I seize your oven, your refrigerator, your entire kitchen and liquidate them to retrieve the value of the “intangible” cake. And you’re tangibly out of business.

Exactly, capital is a social relation; a social organization of labor. Consequently, tangible or intangible is basically irrelevant. I believe you’re the one claiming there is some fundamental change with the proliferation of “intangible assets” which change you fail to identify, as you fail to properly identify intangible assets.

You confuse “financialization”– in itself a highly suspect conception– with intangibility.

Intangible assets are specifically those linked to intellectual property; not debt and credit instruments.

To explain the difference let us analyse Google. Google does not produce a commodity. In short it does not sell its service like say Netflix. Instead it relies for its revenue on advertising as does Twitter and Facebook. This advertising revenue is a cost to the advertisers and in most cases represents the transfer of value produced by the advertisers say Procter and Gamble to Google as advertising income. As such total value (GDP) is not increased as recorded by the SNA because the output of Google represents the inputs from the advertising companies. (Googles “final sales” = intermediate sales deducted from advertisers.) Now consider what would happen if the labour expended by Google’s workers were actually turned into a commodity. For this to happen, Google has to move from a free to use service to a paid subscription service or pay per click service. As if by magic, the labour of Google’s programmers is now sold, that is turned into exchange value. If advertisers now reduced their advertising by the same amount as Google now received in actual sales revenue, would GDP remain the same. No. It would rise by the same amount as the final sales now attributed to Google, Facebook and Netflix sale of their services. (Remember, advertising is an intermediate sale not a final sale, correctly stated.) It is likely that US GDP would rise by about 2% and one of the issues relating to low productivity would be resolved. Here then is the importance of distinguishing between concrete labour and social labour rather than whether a thing is tangible or intangible. The output of Google’s programmers may be intangible, but more importantly, this labour does not assume the commodity form because it is not produced for sale but used to provide a platform to attract advertising.

Accumulation of capital compels development of our powers of production and redistributes labor. The difference between the industrial era and today in the redistribution of labor is the key.

What’s intangible about a software program that reads data from sensors and can control the application of power to the wheels of a locomotive, maximizing wheel/rail adhesion, improving traction effort, reducing fuel costs, and wheel wear?

What’s intangible about the use of radios to transmit the commands without wires to locomotives distributed throughout the train, thus reducing in-train forces and allowing greater train speeds with less risk of rupturing the couplings between the cars?

I think a big portion of the “intangibles” is actually fixed capital.

I would like to offer a different perspective. At the P2P Foundation, we have argued that more and more value is created outside of purely capitalist circuits. In peer production, globa-local open source communities directly create use value, through shared and open IP, which because of its ‘abundance’ cannot be sold as exchange value. An echo of this are the social media companies, living of our use value media exchanges, search companies, but also Uber/AirBNB models which extract from ‘our’ exchanges. Thus, the new form of netarchical capitalism, expressed by the GAFA companies, only marginally produce commodities and directly exploit human labour through the surplus of the platforms they control. If more and more use value is created outside of capital circuits, and less and less of if can be commodified and realized as surplus value, then clearly this creates a value crisis of capitalism , and of for those needing ‘wages’ and income from capitalism. The statisic above, in my view, corroborates this analysis. See also the Dornbirn Manifesto for a short explanation of this thesis.