As I have said in a previous post (see https://thenextrecession.wordpress.com/2013/03/16/workers-punks-and-the-euro-crisis/), Slovenia is likely to be the next Eurozone state that will require a bailout after Cyprus. Slovenia’s banks need €1bn for recapitalisation after taking heavy losses on the commercial property development bust and on falling government debt prices (Italy?). And the new centre-left coalition needs about €3bn to cover the budget deficit and debt repayments this year. It does not look like it can find this money from the country’s own taxpayers and banks. So watch this space.

As Cyprus enters a long period of austerity with the banking sector decimated and the economy diving (one forecast is for a 20% fall in real GDP through to 2017), the debate continues. Is it better for small economies like Cyprus, Slovenia and even Greece to leave the Eurozone, institute their own currencies and devalue against the euro and the dollar, so they can grow through cheaper exports in world markets? Or is better to continue with the grinding down of living standards under the ‘heel’ of the dreaded Troika? Does leaving the euro mean that people can avoid a huge loss in jobs, public services and living standards?

My view is that either way, staying in or leaving the euro, will deliver more or less the same result for the majority. That’s because this crisis is not a crisis of the euro as such but a crisis of the capitalist mode of production. The way out for for the Eurozone is for austerity to lower the cost of production in the weaker states to the point where profitability begins to rise and these smaller economies can start to restore economic growth. The problem with this solution is that this could take a decade (it’s taken years already) and so it may never happen before capitalism enters another global slump – indeed, that may happen precisely because profitability cannot be restored.

There is some progress through austerity within the eurozone. A key proxy for competitiveness is an economy’s current account, the broadest measure of trade with the rest of the world. It shows improvement across the periphery EMU nations. The combined account of Greece, Ireland, Italy, Portugal and Spain narrowed to a deficit of 0.6 percent of gross domestic product at the end of last year from 7 percent in 2008 and will be in balance later this year. While a slide in imports accounts for some of the correction, Greece boosted its exports outside the EU by about 30 percent in the fourth quarter of 2012 from the previous year, while Italy’s rose 13 percent in January from a year ago. While austerity weakens consumer demand, it can begin to turn round profitability. For example, Spain has slashed social-security payments from companies, raised the retirement age and made it easier to fire workers. Portugal has weakened collective bargaining, cut redundancy payments and suspended four national holidays. Greece has pared public-sector wages, lowered the minimum wage, and eased redundancy rules; and is selling state assets.

A November study by Berenberg, a Brussels-based research group, found unit labor costs fell 10.5 percent from 2009 to 2012 in Greece, 10.3 percent in Ireland, 6 percent in Spain and 6.1 percent in Portugal. Over the entire euro-area they gained 1.5 percent. Relative labour costs in Spain and Portugal have now dropped below Germany’s for the first time since 2005. This has all helped to raise profitability in 2012 in most ‘austerity’ EMU economies (see graph). But, with the exception of Ireland, all the peripheral EMU economies still have much lower rates of profit than their peaks before the global crisis of capitalism hit. However, with the exception of Italy, profitability did recover in 2012. In the case of Ireland, profitability turned round as early as 2010.

Why has Ireland done relatively better? I think there are two reasons. First reducing unit labour costs in production has a much bigger effect on growth and profits in an economy like Ireland with annual exports equivalent to 100% of GDP compared to 20-40% in the other countries. Second, unit labour costs were cut so much more easily because of emigration. Irish youth, especially skilled workers, just left the country for the UK and elsewhere. Indeed, the turnaround from net immigration (or Irish returning home to a fast-growing ‘Celtic tiger’ before the crisis) to net emigration is truly dramatic.

Now many Keynesians like Paul Krugman or George Stiglitz argue that the euro crisis is a crisis of the failed project of the euro, not a crisis of capitalism. So the answer is for the smaller EMU states to leave the euro. For example, Krugman reckons the answer for the Cypriot people is to leave the euro. “Cyprus should leave the euro. Now. The reason is straightforward: staying in the euro means an incredibly severe depression, which will last for many years while Cyprus tries to build a new export sector. Leaving the euro, and letting the new currency fall sharply, would greatly accelerate that rebuilding… What’s the path forward? Cyprus needs to have a tourist boom, plus a rapid growth of other exports — my guess would be agriculture as a driver, although I don’t know much about it. The obvious way to get there is through a large devaluation” (http://krugman.blogs.nytimes.com/2013/03/26/cyprus-seriously/). Keynesians bemoan the fact that this advice has not been heeded. But there is a good reason for this.

Take the example of Iceland. This tiny island, smaller in population that Cyprus, is not in the eurozone, or even the EU. But it is used as the model by many Keynesians (see Krugman on Iceland: http://krugman.blogs.nytimes.com/2012/07/08/the-times-does-iceland/) for Keynesian-style alternative policies, including devaluation. Krugman argues for “the relevance of the Icelandic sort-of miracle… What it demonstrated was the usefulness of devaluation (and therefore of having your own currency), and the case for temporary capital controls in an emergency. Also the case for letting creditors of private banks gone wild eat the losses. Iceland did not engage in fiscal stimulus; it didn’t have to, given the kick from a huge depreciation of the currency. And more broadly, Iceland is a dramatic demonstration of the wrongness of conventional wisdom in these times. .. Iceland broke all the rules, and things are not too bad.”

But did Iceland ‘break all the rules’ and are ‘things now not too bad’? This is another Icelandic myth according one Icelandic blogger: “people continue to spread the factually dubious statement that Iceland told creditors & IMF to go jump, nationalised banks, arrested the fraudsters, gave debt relief and is now growing very strongly, thanks. No, Iceland did not tell the IMF to go away (https://www.imf.org/external/country/ISL/). Iceland didn’t bail out the collapsed banks, but that wasn’t for the want of trying. If you read through the Report of the Special Investigation Commission you’d find out that the Icelandic government tried everything it could to save the banks, including asking for insane loans to pay off the banks’ debts (http://sic.althingi.is/). The short version is that they tried to save the banks, save the creditors and screwed up completely. Iceland arrested a few bank fraudsters, but just the pawns, small fry, and the lackeys.

Yes, Iceland did nationalise its banks but then privatised them again in record time. Two out of the three collapsed major banks in Iceland are now owned by their creditors, not the state. The third bank, Landsbanki, is still nationalised but that’s solely because of ongoing court cases involving Icesave. Most of the creditors actually sold their stakes onto foreign hedge funds. Some of the bankrupt banks only remained in government control for a few weeks. SPRON, for example, was merged into Arion Bank which in turn was given to its creditors a few weeks later. essentially a free gift to Kaupthing’s foreign creditors.

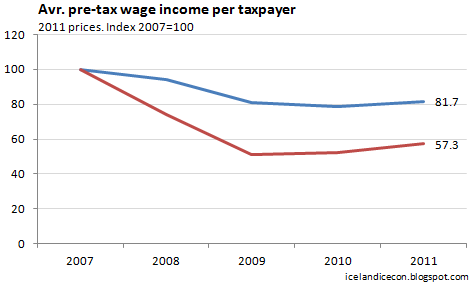

Iceland’s lauded recovery model involving devaluation of its currency coupled with capital controls is now a drag on growth. Iceland is growing at 2 percent, faster than much of Europe. But the IMF had originally forecast annual growth of around 4.5 percent from 2011-2013. It now is under half that. Many Icelanders say they do not ‘feel’ this modest growth. Outside booming fishing and tourism, businesses complain of stagnation. Some 80 percent of households are swamped in housing loan debts indexed to inflation. Investment is under 15 percent of GDP, a record low. State workers like nurses are raising worries about inflation amid increasing demands for better salaries. An hour’s drive from the capital to the town of Keflavik, dozens of Icelanders line up for free food aid. People must present rent or mortgage slips and their salary slips. Real incomes have dropped sharply for Icelandic households and their debt is index-linked to inflation. Pre-tax gross income of the average Icelander has decreased by 18.3% since 2007. Measured in USD however, the fall is 42.7% since 2007.

So both austerity and Keynesian-style devaluation have resulted in a sharp fall in living standards, whether in Greece or Iceland.

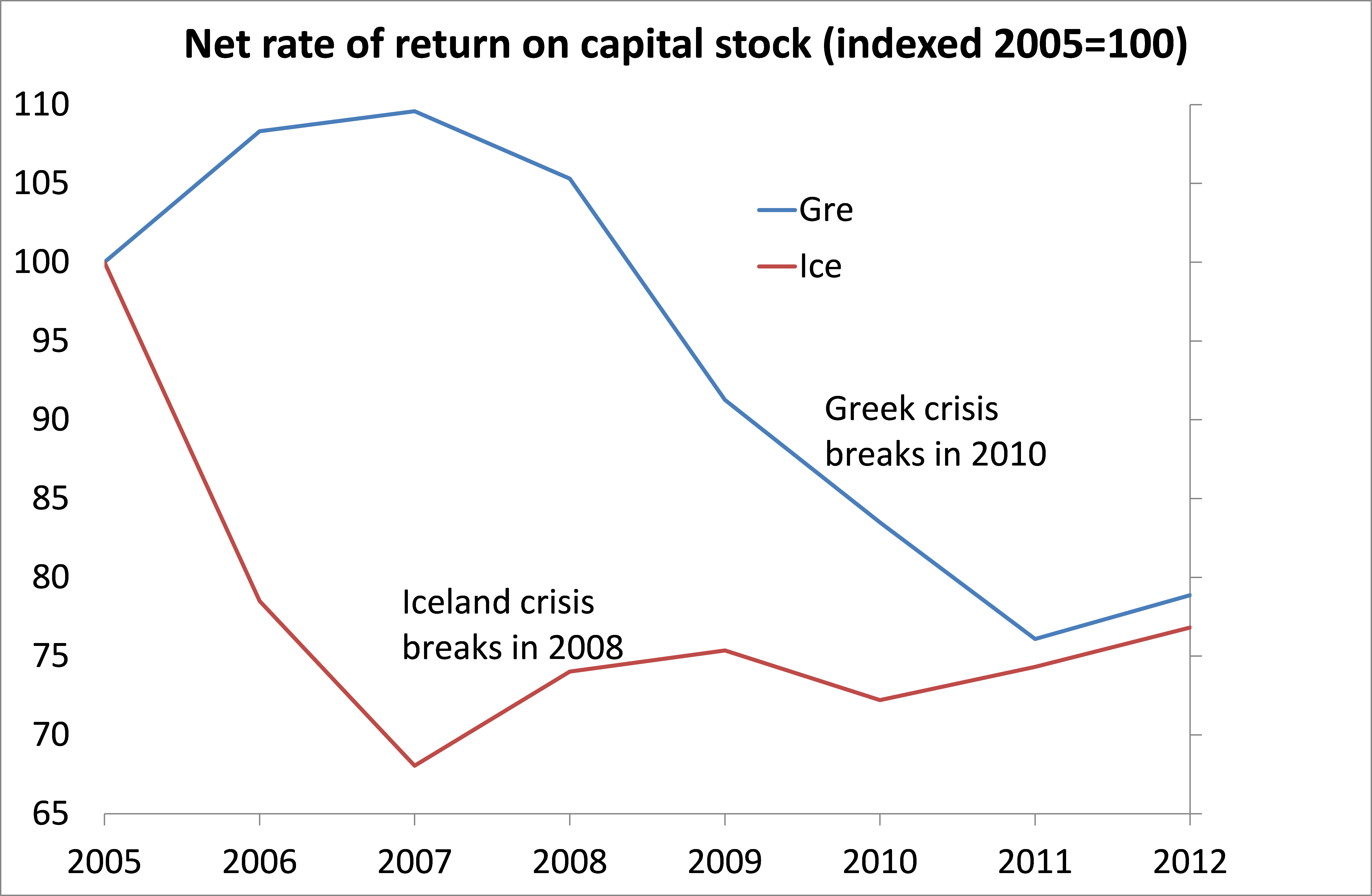

Restoring profitability is key for economic recovery under the capitalist mode of production. So which pro-capitalist policy has done best on this criterion? Let’s compare Greece and Iceland. Iceland’s rate of profit plummeted from 2005 and eventually the island’s property boom burst and along with it the banks collapsed in 2008-9. Devaluation of the currency started in 2008, but profitability in 2012 remains well under the peak level of 2004, although there has been a slow recovery in profitability from 2008 onwards. Greece’s profitability stayed up until the global crisis took hold and then it plummeted and only stopped falling last year. Profitability in ‘austerity’ Greece and ‘devaluing’ Iceland is now about the same relative to 2005 levels. So you could say that either policy has been equally useless.

Perhaps the biggest lesson of this crisis of capitalism is the lasting damage that the Great Recession and the subsequent Long Depression has had on the ability of the capitalist mode of production to deliver on profitability and economic growth. A recent study found that there has been a significant deterioration in long-term real GDP growth (http://www.voxeu.org/article/eurozone-looking-growth). Trend growth for the four main Eurozone countries is forecast to be a little less than 1% and slightly less than 2% after 2014, with trend growth highest in Spain and France; and the lowest for Italy and Germany.

Weak trend growth in a central scenario

Source: BofAML Global Research.

It could be even worse, if investment fails to recover quickly. Trend growth might well remain negative in Spain and Italy and may fail to increase for Germany or France. As the authors conclude, “this exercise shows the damage will indeed be long lasting, permanently impairing growth in a context of an ageing population that needs higher growth capacity than ever before.”

Good piece.

Strange that the home of all the Eurosceptics is the US and Britain. Neither in the single currency.

Britain doesn’t have the € and had a big devaluation.

As Sarah Palin probably wouldn’t say, ‘how’s that currency independence working out for ya?’

I’m curious and admittedly naive. But I don’t understand why Capitalism NOW needs to drive down the value of labor even further than it already has? (I do of course understand the systemic tendency to continually do so). It just seems to me that in the US, wages are at a 40 year low. Social wage (welfare state benefits) have been continually whittled away for years and years. Unemployment is substantial. Unionization is at a historic low. Technology has made substantial sectors of the working class entirely redundant. Corporations sit on huge stores of capital–more then in he past 35 years–yet don’t invest (investment strike.) I guess I’m wondering, from he perspective of Capital,what would make investment more likely? What social conditions would make the prospect of profit more likely, would elicit investment? (I realize this is a US centric question.) I also realize this question sounds like ‘when is enough, enough?” But I AM curious, what do Capitalists really want as a tipping point to new investment?

In the immortal words of New Order– “It’s never enough… until your heart stops beating.”

If capital is, exists only, in and through its self-expansion, as Marx so acutely analyzed, we can see that logically, inherently, its the very structure of capital— the need to expropriate ever greater masses of surplus value– that determines its “dissatisfaction,” its discontents.

@ S. Artesian. Yes I agree with your observation.. I am reminded of that old song by John Fogerty, “Fortunate Son” —Some folks inherit star spangled eyes,

Ooh, they send you down to war, Lord,

And when you ask them, “How much should we give?”

Ooh, they only answer More! more! more!”

This said, I guess the theoretical question (although in this period it may be only an academic one) is what produces the opposite reaction of Capital? That is, in what historic period, under which ideal conditions, does Capital find investment attractive? My question is really about why this is the particular historical juncture for an investment strike,when in fact, Capital has made such huge gains in driving down the condition (and “price’) of the WC over the last 35-40 years? (my periodization may be a little off, and again, U.S Centric, but it think it is still pretty close to correct. Let’s just say post 1973 or 74–the end of Capitalism’s “golden age”) It’s not like they (Capital and Capitalists) are so vehement in their opposition to investment because labor is strong and waging an effective war against the extraction process, so strong that Capital must “resist” and teach workers a lesson. On the contrary, Labor is weak and the conditions for surplus extraction, at least at the point of production (and frankly social reproduction), would seem to me to already be pretty favorable to Capital. If so, if cheap labor is plentiful, if the organization of the working class is weak, if technology allows further displacement of living labor, etc. then why isn’t this a GREAT time to start investing? What is the disincentive? And why now? Maybe I’m seeing the trees and missing the forest? Maybe this crisis of devaluation has other explanations?

This isn’t meant to sound trite but presumably [according to what I read here at least] capitalists will invest when and only when the rate of profit is nearer historic highs. Investment is higher in the US since their ROP is also higher. ergo…

Well, I don’t know that you can call it an “investment strike”– at least in the US. Yes, cash levels are at record highs. However capital spending programs, for US Class 1 railroads, are at historic highs– over $13 billion I think.

In fact, one of the reasons why pressure is kept up and intensified on workers is the fact that not enough accumulated capital has yet been “discounted”– destroyed– and overproduction of capital, of the means of production of capital is continuing, particularly in the transport/circulation sector– maritime shipping is strangling pretty much on the glut of shipping ordered in 2006/2007.

Contrasting the current “recovery” from that of the 2001-2003 recession is that earlier contraction and recovery in the US fixed asset replacement rates actually dropped below “1”– meaning fixed assets were being used up and not being replaced– around 2006 the bourgeoisie had to begin spending again and look where that got them.

Marx, in the Grundrisse I think, remarks that the dilemma of capitalism is that at one and the same time it makes labor– expressed as labor time– the source of its expansion, while at the same time to expropriate that labor as labor time, as surplus value, capital must continuously reduce/expel it from production.

This changes the all important relation between a) necessary labor-time and surplus labor-time and b) the “inanimate mass” of the means of production and the proportion of living labor. In short, the more capital exchanges itself with labor power, the less of itself capital actually exchanges with labor power, and hence the smaller the increment of expansion. Reducing wages, to a very real extent, only makes this “dilemma” more acute for the bourgeoisie.

Too much or too little investment?

@Brad. I think the reason is that there are other points in the cycle of accumulation where there barriers or problems:

* International competition especially in manufacturing is so fierce that is drives down prices and therefore profits (Robert Brenners argument);

* there is a lack in effective demand exactly because wages are so low and because states impose strict austerity. Not much demand, not much opportunity to invest (Keynesian argument):

* and, the underlying “tendency of the rate of profit to fall” (Marx) is at work; technology is so super-efficient that it has driven down the share of variable capital (i.e. labor) and has increased the share of constant capital (machines, building, raw materials) in the organic composition of capital. But because variable capital, or labor, is the only source of surplus value, which is the basis for profits, profits are low and captalists do not invest.

All together this leads to the current situation of overaccumulation where, as you write, there is so much capital looking for profitable investment, but there are just not enough opportunies.

What I always find difficult to understand, or to judge, is what reason is “the most important”. Or can we just say, there are various reasons and crisis dynamics?

To the extent that Robert Brenners argument holds one would assume that if the likes of China, India and Brazil continue to grow [per capita growth] they will ‘enjoy’ a more redistributive policy going forwards [Keynesian demand management] so opening up another round of outsourcing and development in yet to be exploited third world states [are there any suitable ones left?] Another billion or so consumers must surely make a difference?.

Debt write downs/write offs/deleveraging, also gives a further boost to demand in the medium term perhaps…but does it require investment to increase first?

New technologies have been touted as a requirement to facilitate a new round of investment. New methods of energy extraction are having an effect in the US[fracking] Japan [methane extraction from sea bed deposits] but perhaps we are in need of a new technol’ revolution on the scale of computerisation and until we get one or a combination of the above… investment will be disappointing/somewhat anaemic? .

Africa is the next target for expansion. China is already in there.as the potential for a good ROP is enormous.

The comparison between Iceland and Greece is interesting but you forgot to mention that in the case of Greece employment collapsed, unemployment is 27% and is projected to rise to 30% by the end of the year. In the meantime the economy is in depression 5 years in the row (2013 will be the sixth) the gdp has fallen by 20% and the decline will continue indefinitely given the new cuts that the government agreed with the troika. Iceland may well not entered a new period of dynamic capitalist growth but it no way experienced the catastrophe that befell on Greece. Internal devaluation is much more harmful in terms of unemployment and the percentage of gdp fall, than currency devaluation. That makes a lot of difference.

One more correction: the boost of Greek exports is mostly fake as it is the result of a logistic trick in the counting of petroleum products. Moreover, the rise in the Greek exports started from a historically low point, so it’s still negligible.

True, some funny things going on there. Looking at nominal exports from the peak at Oct’20008, after a 40% fall in 2009, exports recovered by Nov 2012 to be 30% above the 2008 peak, but have dropped back to that level. That’s because the rest of the Eurozone is in a depression. Greek capitalism remains appallingly weak and cannot get out of its crisis without Euro fiscal transfers and private foreign investment. In other words, Greek capitalism must remain a Franco-German satellite whether the Greek elite sticks with the euro or tries to go it alone.

Some concerns with the logic and persuasiveness of this post:

1) Roberts is Marxist because he recognizes the European crisis a “crisis of the capitalist mode of production.” Roberts asserts that a Marxist, as opposed to Keynesian, approach demands that we understand the economic decline in Europe as a crisis of capital. Fine. Further, however, he asserts that apprehending a crisis of capital proscribes questioning the necessity and benefit of the Euro to Germany’s periphery, which is what only Keynesians do.

2) To explain why TINA, he readily deploys the total abstraction that is a conservative econ “law”: “The way out for the Eurozone is for austerity to lower the cost of production in the weaker states to the point where profitability begins to rise and these smaller economies can start to restore economic growth.” This absolute abstraction demands you ignore most of the common peripheral conditions such as little to no domestic consumer demand, and at least one already-dominant goods-exporting metropole (eg. Germany), and a forced program of reallocating wealth from working-class people and the public to bankers (AKA austerity), do not automatically incentivize investment, productive expansion, and may prevent it, including dragging down that metropole (assuming that Germany does not have as ready, competitive market access to other peripheries without engaging in expansionary warfare, thereby radically changing the economic order). Recognizing that structural “incentives” operate differently across regional economic stratification would be a Marxist political-economic approach.

3) On the basis of an iffy conservative econ foundation–assuming that a bit of data indicating increase in exports v. imports indicate that the conservative law is applicable (But it may not. The assumption may well remain unfounded.), the fusion theorist then makes a further theoretical extension, “While austerity weakens consumer demand, it can begin to turn round profitability.” He then goes on to talk about how austerity state reform ensures that that profitability is being allocated in an exclusive, concentrated (It’s possible that it’s even extractive.) way, as if that were some sort of evidence for profitability itself, and, by strictly-theoretical extension, the restoration of classical British competitive capital investment, productivity increase, and trickle-down wage increases (not to mention mercantilist (buy-cheap, sell-dear) imperial colonialism in the background, and the role of capitalist confidence and belief in the requirement for a low-end consumer market in permitting regionally-limited wage increases instead of wealth accumulation). This is conservative econ theory. There is no Marxist or for that matter real empirical reason to assume that such an amazing restoration would be the result that would take place with austerity governance in capitalist region peripheries today. For example, from an Instrumentalist Marxist empirical perspective there’s been little elite discussion of anything other than implementing austerity and privatizing public wealth; rather, if anything, the influential Austrian conservative theory that infused economic, legal and political frameworks beginning in the early 20th century, effectively deprioritizes investment incentives, reducing them to little more than a nostalgia-harvesting communications strategy, in favor of accumulation via privatization itself. (The exception is German Ordoliberalism, which did uniquely see economic growth based on rules for the state, liberation for capital (and an exclusively-generous infusion of investment from the US for decades) that promoted a very competitive high-value export niche.) But especially outside of specific historical relations (competitive capital in primary regional metropoles), profitability has no natural, automatic relationship with either productive investment or a country’s economic well being and development.

4) Now that I’m unsure about whether I can use such an analysis in my own work, I want to know How does Michael Roberts measure countries’ rate of profit? Dumenil & Levy-style? Alan Freeman-style? That will require digging.

5) Roberts shows, like Mark Blyth, that the countries that do show some profitability recovery, such as Ireland or Estonia, Latvia, Lithuania, are countries of mass working-age population exodus. So we may surmise from these observations that a successful austerity system requires (individually-costly) mass working-age population migration, a global policy issue unto itself. Blyth’s analysis has the merit of additionally observing, thanks to a dialectical sensitivity, that the profit recovery did not lead to the REBLL countries’ economic recovery, as it was by and large invested in real estate speculation and thereby resulted in *increased* country indebtedness. In other words, the conservative econ assumption—Everyone can cut their way to growth– is invalid in this context. We will see if Ireland, Portugal, Spain & Greece contradict the earlier REBLL experience or not.

6) Roberts, blogging, basis his view, that Iceland cannot be a model for economically-restorative political action, on the view of an Icelandic blogger. I will look over that blogger’s evidence-links later (The blogger provided links to the IMF and Thingi Commission, but didn’t report transparently on the evidence. That will require digging.), but Roberts describes the evidence this way: Icelandic leaders tried to bail out its banks but didn’t. That evidence flatly does not dispute the case that not bailing out the banks can be replicated, or that it isn’t a beneficial idea. Who knows? Maybe Icelandic leaders tried to fake bail out the banks? We know that Icelandic leaders were replaced early on. Maybe the guys with ties to the banks were hoofed and the next leaders “failed” to bail out the banks.

7) Temporary bank nationalization is not a case for not nationalizing the banks. Maybe it’s tactically-beneficial, or economically-beneficial to nationalize the banks temporarily, if global finance won’t permit permanent nationalization.

8) Roberts asserts Iceland is economically indistinguishable today from Greece. Roberts equates Iceland’s current growth to Greece’s because a) the average income in Iceland isn’t as high as it was before the crazy financial bubble burst, and b) “Iceland is growing at 2 percent, faster than much of Europe. But the IMF had originally forecast (higher) annual growth.” Further, by the normal laws of economics that were so valued above in Roberts’ argument, if Icelandic debt is indexed to inflation, isn’t it helpful that incomes have dropped since the bubble days? Roberts has failed to produce any kind of convincing argument against the Icelandic model, the Icelandic capital controls-currency devaluation model. By this dubious sophistry, in which Icelandic stabilization is indistinguishable from German-imposed PIIG austerity, the counterfactual Roberts is de facto asserting in this blog is that if Iceland had taken austerity it would have produced by contrast a preferred outcome, a la his comparatively rosy depiction of Ireland, in which mass labor exodus (and potentially real estate speculation and increased debt) is not disruptive after all, right? Is this a good way to do Marxist political economy?

9) Roberts ends with a completely-obfuscatory comparative chart, given his argument is that capital is competitive, asocial and must be incentivized with a high rate of return on capital. The chart, comparing the drop in rate of return from a 2005 base, is presented to give the impression that Greece’s net rate of return is low, but slightly higher than Iceland’s. Roberts allows magnanimously that they are equivalent. That chart tells us nothing about these countries’ comparative rates of return on capital. Maybe Iceland’s is decent. We don’t know. Why don’t we know? Is this bullshit supposed to distract us from questioning whether rate of profitability itself is a measure of economic thriving in metropoles’ peripheries under conditions of global monopoly capitalism today–whether the current neoliberal arrangement today is the best of all possible capitalist world? I am all in for an argument that we need to fight to socialize the economy (not just the risks and costs). But down this conservative econ-Marxist road lies not anti-social democratic savvy, but confusion and TINA paralysis. You could not expend so much effort distorting empirical reality, just as easily acknowledge that economic growth *slowdown* (v. cross-regional manic-depression) is here to stay, consider thoughtfully how expanding Iceland’s model would create and/or limit political-economic opportunities, and argue that there needs to be mass struggle against global monopoly capitalism as a power *relation* that demands socially-irrational expropriation and exploitation (By the way, better explaining Iceland’s struggles with the IMF and hedgies in righting its ship).

You should mention the name of the icelandic blogger, as you’re using his work!