In Q2 2023 the Chinese economy expanded by 6.3% year-on-year, up from 4.5% yoy recorded in Q1. Sounds strong, but quarterly growth was only 0.8%, slowing sharply from 2.2% qoq in the first quarter of 2023.

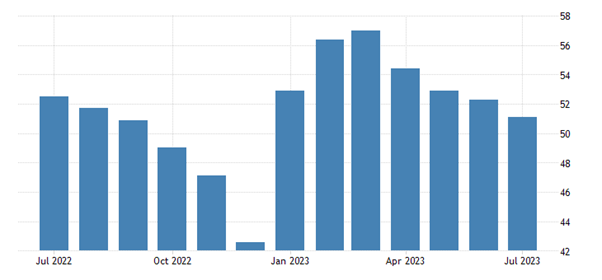

And a reliable measure of economic activity, the purchasing managers survey index for July, was down to 51.1 in July 2023 from 52.3 in the previous month (50 is the threshold between expansion and contraction). This was the lowest figure since December 2022. Factory activity contracted for the fourth month in a row.

The West’s China ‘experts’ have been quick to argue that the Chinese economy is in deep trouble, with slowing growth, falling exports, weak consumption growth and rising debt. The great economic miracle is over.

But how many times have we heard this refrain from the experts over the last 20 years? I could cite article after article, book after book, predicting the collapse of China’s state-led economy, ranging from the claim that is locked into a ‘middle-income trap’ (ie cannot grow fast again); that an ageing population and falling workforce, alongside rising public and private sector debt, is leading to ‘Japanification’ ie a stagnant economy; and finally to forecasts of an imminent collapse in the property and finance sectors.

I have dealt with these arguments in detail in many previous posts. The last one was only in March. Please read that for chapter and verse and the previous posts cited. The data are all there, refuting this ‘expert’ analysis. But of course, it won’t go away because it is in the interests of ‘the West’ to claim that Chinese economic model cannot work and it needs urgently to make a transition, not to socialism, but to outright free market capitalism.

Let us consider the latest round of claims being put by mainstream economists (and parroted by some inside China, ie those who were nicely educated in neoclassical, free market economics in American universities). For example, here is the latest view of the Financial Times. “Government policy is largely to blame for the slowdown. Decades of relying on an investment-driven growth model has slowed China’s transition to a consumer-based economy. Poor oversight of the housing market led to an unsustainable lending boom, while political impediments have hamstrung private enterprises. Heavy-handed Covid restrictions have also left deep scars.”

So first, let’s blame the Chinese government for the slowing economy – presumably for interfering in business and the capitalist sector. But then claim that “decades of relying an investment-driven growth model” is at fault because what is needed is a “transition to a consumer-based economy”. Really? Have the consumer-based economies of the G7 done better than the awful investment-led Chinese economy in the last two or three decades? Take a look at this graph below.

But the FT and other experts might retort, since COVID things have changed in China; now the economy cannot recover. Really? Look at this graph on the growth rate of China and the US since the COVID pandemic started. Indeed, during the COVID pandemic slump year of 2020, every major advanced capitalist economy suffered a recession, but, as in the Great Recession of 2008-9, China did not. And yet China applied the most stringent and draconian series of lockdowns during the pandemic.

And while the US economists are in rapture over 0.6% growth in the US economy in Q2 this year, apparently 0.8% growth for the same quarter in China is to be considered a disaster.

The FT says that “heavy-handed Covid restrictions have also left deep scars.” Well, those ‘heavy-handed’ measures also saved millions of lives in China, when its health system was at breaking point and inadequate to the task. During 2020-21, when the COVID death rate rocketed in the West, China’s stayed at miniscule levels. Eventually, as lockdown exhaustion emerged and protests rose, the government relented and ‘opened up’ the economy, the death rate rose – but only to 85 per million compared to 3300 per million in the US, or to ‘open’ Sweden at 2325 and or even India at 375 (ludicrously underestimated). The ‘deep scars’ were and are still being felt in Europe, the US and Latin America from COVID deaths and long ‘COVID’ on the health of the workforce and economic growth. This year, the IMF forecasts China will grow 5.3%, while the advanced capitalist economies will manage only 1.5%, with the Euro area reaching only 0.9% and Germany and Sweden in outright recession.

The FT goes on that “Poor oversight of the housing market led to an unsustainable lending boom, while political impediments have hamstrung private enterprises.” Much noise has been made about the property crash in China, with several mega-property development companies going bust as the debt borrowing that they built up could no longer be serviced from property sales.

But was this down to poor regulation? We have heard the same cause presented in the property busts in capitalist economies – that it was ‘badly regulated’. But as in those economies, China’s property crisis is not because of bad regulation or ‘unsustainable lending’ but because the housing and property market in China is just that – part of the speculative capitalist market. To quote, Xi himself: ‘housing is for living not speculation’.

And therein lies the rub. Why was a basic human need, housing, handed over to the private sector to meet the needs of millions flooding into the cities over the last few decades? Housing should be done by direct public investment to build houses for all at reasonable rents and so avoid speculation, rocketing house prices and widening inequality. Indeed, the biggest reason for rising inequality in China in the last two decades was not billionaires but the inequality between urban and rural areas and property and non-property owners.

It’s what happened in the West; China should have avoided that too. But in their ‘wisdom’ the Chinese leaders, as advised by their Western-educated bankers and economists, opted for the rentier-capitalist model, which now has come back to bite them.

The government has been forced to act. First, with its “three red lines” policy introduced in 2020, it aimed to limit borrowing by developers and ultimately curtailed their access to financing. Then it started to bail out developers and take over some. But huge debts remain in local government which bore the burden of providing land to these developers and raising funds. Local government debt has spiralled and the oncoming repayment schedule is high.

Local government debt now stands at around 25% of GDP, but if you add in the financing vehicles set up by local governments (LGFVs), then total local government debt is more like 60% of GDP. Worse, faced with tighter credit criteria at home, LGFVs turned to offshore markets and raised a record $39.5 billion in dollar bonds.

I am afraid that the Chinese leaders have not learnt from this. They are now moving to provide easier credit for developers and have dropped Xi’s phrase about ‘homes for living’. The government now talks of helping out the capitalist sector. Senior party and state officials jointly released a 31-point plan earlier to shore up the private economy and improve business sentiment. Various government agencies last week also outlined goals to boost consumer spending on cars and electric appliances, though no direct subsidies for households have been unveiled.

All this is along the lines advocated by the likes of the FT, which reckons that “entrepreneurs and established businesses need stability and regulatory clarity from the government. Further monetary policy loosening by China’s central bank could help. Beijing will also need to restructure its local government debt; one option might be a fire sale of state assets to private companies. The proceeds would help local authorities to avoid a debt crisis.” In other words, the answer is not public ownership of the housing sector and taking over the indebted property companies, but instead a bailout and then a sale of state assets to pay for it ie privatisation not nationalization.

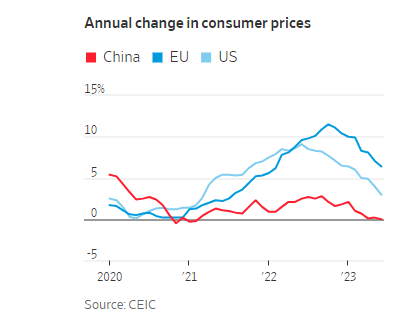

Finally, in its claimed demise of the Chinese economy, the FT returns to the old ‘Western expert’ argument that China must become a consumer-led economy like the G7, if it is to avoid the ‘middle-income’ trap and Japanese style stagnation. But it is the consumer economies of West that are stagnating, not China. Moreover, if ‘stagnation’ means no inflation of prices, then it may have merit. China has the lowest inflation rate of all the major economies in the world, including stagnating Japan which is desperately trying to create inflation!

While households in the West are suffering the biggest fall in living standards since the Great Depression because wages are not keeping up with high inflation, it is the opposite in China.

What is an issue is youth unemployment which is over 20% in China compared to average urban unemployment of around 5%.

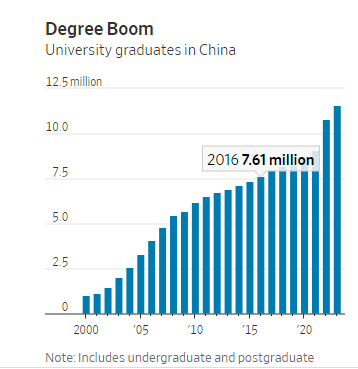

The problem isn’t that jobs don’t exist in China. They do. But the economy isn’t producing enough of the high-skill, high-wage jobs that many college students have come to expect. China is producing more and more university graduates.

But they all expect to get jobs in finance and technology, but not in manufacturing, construction and engineering. It’s a problem that has affected not just China, but also the West. Better-off families want their kids to be working for glamorous tech firms and banks (where they have to work ridiculous hours) rather than in any ‘mundane’ work that often can pay just as much. The government has offered incentives to companies take on students but it does not plan government projects that could provide training in tech and innovation that could meet important social targets.

Then there is external trade. One reason that China’s growth rate has been relatively low in the last year is the collapse of international trade which has turned negative. As a result, China’s exports to the world have dropped.

Yes, that probably means China should concentrate on domestic investment and output, not exports. But that does not mean becoming a ‘consumer-led’ economy. As I have argued before, consumption flows from investment not vice versa – as China’s economy up to now has proved.

The FT and the other experts argue that China is heading for low growth through this decade – see the IMFs latest forecasts.

But as I have argued in previous posts, that does not follow if China uses the potential it still has to invest and grow. Some ‘experts’ are now claiming that India will usurp China over the next decade. But as ex-World Bank and IMF economist Ashoka Mody puts it:

“Since the mid-1980s, Indian and international observers have predicted that the authoritarian Chinese hare would eventually falter and the democratic Indian tortoise would win the race.”

But the World Bank’s 2020 Human Capital Index – which measures countries’ education and health outcomes on a scale of 0 to 1 – gave India a score of 0.49, below Nepal and Kenya, both poorer countries. China scored 0.65, similar to the much richer (in per capita terms) Chile and Slovakia. While China’s female labour-force participation rate has decreased to roughly 62% from around80% in 1990, India’s has fallen over the same period from 32% to around 25%. Especially in urban areas, violence against women has deterred Indian women from entering the workforce.

Assuming that the two economies were equally productive in 1953 (roughly when they embarked on their modernization efforts), China became over 50% more productive by the late 1980s and today, China’s productivity is nearly double that of India. While 45% of Indian workers are still in the highly unproductive agriculture sector, China has graduated even from simple, labour-intensive manufacturing to emerge, for example, as a dominant force in global car markets, especially in electric vehicles.

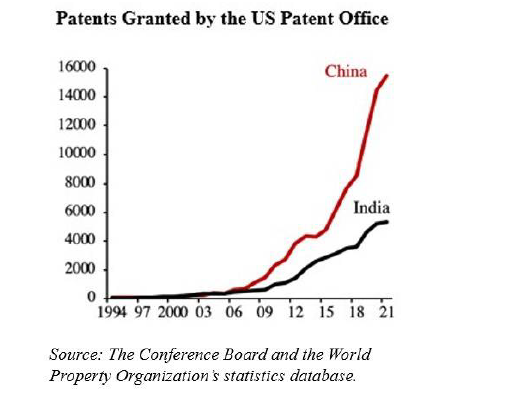

China is also better prepared for future opportunities. Seven Chinese universities are ranked among the world’s top 100, with Tsinghua and Peking among the top 20. Tsinghua is considered the world’s leading university for computer science, while Peking is ranked ninth. Likewise, nine Chinese universities are among the top 50 globally in mathematics. By contrast, no Indian university, including the celebrated Indian Institutes of Technology, is ranked among the world’s top 100.

China still has vast opportunities for infrastructure in its interior provinces. The challenge is turn domestic savings into domestic investment, so capital is allocated to its most productive uses. For me, that means the state must direct the allocation and not leave investment to the capitalist sector to deliver.

Indeed, the capitalist sector in China is failing. The private-sector’s share of China’s 100 largest listed companies by market value dropped from a peak of 55% in mid 2021 to 39% this June, close to its lowest levels in more than three years, according to a forthcoming research report by the Washington, D.C.-based think tank Peterson Institute for International Economics, or PIIE.

Private sector investment shrank by 0.2% in the first half of 2023 from a year earlier, the first contraction since official data collection began in 2005, with the exception of 2020, when the economy was racked by the pandemic. In contrast, investment by state-controlled firms expanded 8.1% in the same period.

The FT makes a point: “China’s central government is one of the least indebted in the world… If China is to sustain its long run of economic success, it is down to Beijing to act.” But the FT’s idea of action is for government to make cash handouts to households and ‘free up’ the private sector. But it’s not a turn to a consumer-led market economy that China needs to get the economy going again, but planned public investment into housing, technology and manufacturing.

Thanks for this informative article. It dawned on me while reading rarely do we see the loss of agricultural land and increased demand for water scrutinised when comparing the economic progress of India and China with the rest of the world. Urbanisation is having a huge impact and we need only look to Japan and the growth of Tokyo-Yokohama to see how the reduction in agricultural land gives rise to food insecurity. Japan is now a net importer of food products when decades ago it was self-sufficient. I was wondering if urbanisation itself might be a constraint on the economic development of both India and China. China and India are huge countries and one wonders where the food is going to come from if these countries can’t feed themselves.

Thank you so much for this, and so many other, brilliant analyses.

Excellent article on Chinese Economy…Very lucid and analytical article…kudos

“And while the US economists are in rapture over 0.6% growth in the US economy in Q2 this year, apparently 0.8% growth for the same quarter in China is to be considered a disaster.”

It’s very easy to understand this logic if one knows how the modern-day vulgar economists think on historical terms.

The present-day dominant conception of historical time is the “End of History”. It claims that History existed up until 1991, when the USSR fell apart. We thus now live in a systemless, timeless, completely undetermistic era, where our only tool for any kind of (always imperfect) prediction of the future is the status quo.

How does this concept of historical time reflects on present-day vulgar economics? There are many individual interpretations, but the most sophisticated and dominant one is the Middle Income Trap, which states that the modern-day First World nation-state is the ultimate form of societal formation. In other words, there is no better world possible than your present-day First World country: a nation can achieve First World status, but can never surpass it.

That’s why a +0.6% growth in a First World country (in this case, the USA) is celebrated effusively, but a 0.8% growth in a Third World country (in this case, China) is not: a First World country is not required to grow because there is nowhere to grow, it is the End of History.

The concept of time of the End of History is Francis Fukuyama’s biggest contribution to Western philosophy. People like to mock or make fun of Fukuyama because they take his infamous book’s title literally, but his thinking is more alive and more dominant than ever. Almost all of the liberal ideologies alive today (including many center-left and leftist ones in the West) are simply a logical variation and area-specific application of his concept of End of History.

–//–

“Much noise has been made about the property crash in China, with several mega-property development companies going bust as the debt borrowing that they built up could no longer be serviced from property sales.”

Do not take my word for it, but I’ve heard some people from China say that the reason there is this property bubble in China is a defect in its central planning system: in China, the Five-Year plan is not as specific as the Soviet one and only determines the growth rate; the provinces can decide on their own how to achieve said growth rate.

And, thanks to how they contabilize this growth (investment in fixed assets is accounted as growth; while in capitalism investment is accounted as a loss), the provincial governments quickly realized they could achieve their province’s growth easily by fuelling their respective real estate markets. This, combined with China’s historically great urbanization process (ten times bigger than the European Second Industrial Revolution, as recognized by ex-PM David Cameron himself), resulted in the Central Government ignoring this problem for a very long time.

However, it is important to highlight that the 28 points are for the entire private sector, not just the real estate sector. At the same day, a 20 measures to boost consumption was also announced, so it is not just an isolated paper to benefit exclusively the private sector.

Michael you and I are of one mind that profit drives economic development by acting on investment. Surely then, the final arbiter on the question whether China is stagnating, has entered a mid-life crisis or is simply facing domestic violence at the hands of the USA, is the rate of profit. Readers of my articles know that I produce a complex rate of return most months for China. Here is the latest http://theplanningmotive.com/2023/06/28/china-complex-rate-of-return-for-the-period-jan-may-2023/ Currently the complex rate of return is running at 4% down from 9% in the period 2010-12 and 6% in 2021 when covid based exports temporarily lifted the rate. In fact the complex rate of return for Chinese industry is at its lowest this century. (Methodological note: I use the term complex to distinguish it from the usual rate of return based only on fixed capital. The complex rate is lower because total assets as defined by the statistical bureau of China includes some financial assets as well as inventory.) Secondly, it is possible to superimpose the fall in the rate of profit over the fall in the rate of invertment in China. Annualized investment is running at less than 5% p.a. this year compared to over 20% when the rate of return was over 9%.

And of course the data is worse for the private sector.

And just as the Chinese Copitalist Party is turning towards the private sector so it will turn against its workers. The fall in the rate of return, a proxy for the rate of profit makes the social contract unaffordable, aka rising standards of living for average urban workers. Thus these economic tensions will no doubt provoke political repercussions. Which is why I have advised you and many others to abandon your position that China is somehow not strictly capitalist. The mid-life crisis is a side show. The real show in town is that the CCP is against the buffers of profitability. The law of value is not some kind of pick and mix stall, it has strict laws, and the CCP is learning that it is a hard taskmaster – either profitability has to be improved or standards of living supported – they can no longer be done together. They have to choose between the economy and their workers, anyone one to bet which side they will choose? (P.s. the granular data I have seen shows wage cuts not wage rises as competition in the labour market intensifies.)

In my view, the rate of profit and the law of value on not in full control in China. So unlike in the West, the profitability of capital is not decisive for investment in China. Otherwise China would have joined the others in slumps in 2008 and 2020. It did not.

Michael the law of value dare not be taken in parts. Its all or nothing. I will address only 2008 as 2020 was not unique. Post 2008 witnessed the greatest investment wave in capitalist history. It transformed the Chinese economy from a contract manufacturer and assembler into a semi-industrialized economy. Total industrial fixed assets increased by 222% between 2008 and 2014 by which time the investment wave was ebbing. In contrast the gross value added by industry increased by only 78% around one third the increase in capital. Thus what was happening was a huge increase in the organic composition of capital. It was this rise and continuing rise in the organic composition of capital that was the gravity dragging down the rate of profit. It was this effect that acted as a headwind to investment. The fact that the rate of investment tracked the rate of profit cannot be dismissed. (All data from the tables found in the Chinese 2022 Yearbook http://www.stats.gov.cn/sj/ndsj/2022/indexeh.htm)

The fall in the rate of return is not only a disincentive to invest, but alas what is all too often forgotten, is that it also provides the means for further investment. So if the rate of return is 5% and net investment is 10%, the balance of 5% can only be achieved through raising debt both nationally and internationally. And given China’s debt levels and the need to deleverage that door is closed even taking into account the appropriation of personal savings through low interest rates for savers. That is why 2008 is unrepeatable.

Instead what we have is a war economy or as the CCP describes it: ‘Military-Civil Fusion (MCF) Development Strategy.’ But that has been forced on China by US imperialism so is a discussion for another time.

Now you know why we need a forum so these vital questions of theory and politics can be thrashed out.

It is now widely reported in the western financial media that SMEE has produced a 28nm DUV lithography machine, something i have pointed out a few months ago. It will be one seventh the cost of the equivalent ASML machine primarily due to the lack of licence payments and advanced chinese manufacturing capacities. This machine will economically etch chips down to 7nm covering 90% of all chip making by value. Good news for China but bad news for the world, because the red line triggering a military attack by the USA on China will be the unequivocal recognition it has failed to arrest China’s technical ascent. Alongside this achievement is the certification of the fighter jet engine ws-15 on par with the best in the West. Time is not on the side of the USA.

“Indeed, the biggest reason for rising inequality in China in the last two decades was not billionaires but the inequality between urban and rural areas and property and non-property owners.” This is a veil. The reason for inequality is exploitation that 1) polarized the country between billionaires and the working class, and 2) stratified the working class, with some 200 million internal-migrant workers earning a pittance in factory sweatshops, precarious delivery assignments, etc. The basic “property” at issue here is the commodity labor power.

There are many references to “the capitalist sector” in the article. The entire economy is capitalist. State firms are run for profit, too. There is no unified allocation of investment (“plan”), only industrial policy tools like Japan, France, and now the U.S. use. Every reference should properly be to “the private capitalist sector.”

Two curiosities about the Chinese real estate sector.

#1: it seems the CPC will backtrack on the “home is for living” statement:

“Chinese real estate stocks soar, propped up by imminent policy easing”

– https://www.globaltimes.cn/page/202307/1295016.shtml –

“The principle that “houses are for living not for speculation” was reiterated in almost every CPC Central Committee meeting since 2019, but this time it did not appear, Huatai Securities said in a note, adding that it is a prompt move to reset the tone of the property industry now when the sector is dragging the heels of the nation’s economic growth.”

So the question is how will they backtrack, not if. This may range from a very astute, Deng Xiaoping-level maneuver to a complete “neoliberal” capitulation to the private sector, a la George W. Bush 2001-2008. The sources of the aforementioned article are also limited – they tell the story from the point of view of the private sector – so we’ll have to wait and see for another one or two decades to observe where it is headed to.

#2: the Chinese stock market has a daily cap on individual paper growth, which is 10%. The aforementioned article states that “Stellar performances among real estate stocks included Gemdale Corp, Jinke Realestate Group and a dozen other developers, with their prices rising by the daily limit of 10 percent, while other developers rose by more than 5 percent.”.

In other words, a Chinese real estate company will never be able to grow more than 10% per day in the stock market.

This daily limit seems to enrage the neoliberals, as this Princeton article demonstrates:

“Daily Price Limits and Destructive Market Behavior”, by CHEN et al.

Click to access PriceLimit.pdf

All the five (!!!) authors seem to be from Hong Kong; all of them are certainly linked to either Princeton, Hong Kong and/or the Shenzhen Stock Exchange. They call this price limit a “destructive market behavior”.

“But how many times have we heard this refrain from the experts over the last 20 years?”

About as many times as we’ve heard that this year is the year of the next recession and if not this year then definitely the next year will be the year of the next recession.

Meaning? Meaning it means nothing absent class struggle and the “resolution” of so-called mistakes, deviations, leanings of a ruling class and/or its elite counterparts by their overthrow.

If that is a dig at me, I think you will find that I have forecast a recession every year. But there will be another one eventually just as China is unlikely to have one.

It’s a dig at those who think “economic determinations”– recession, inflation, public investment vs “private sector” occur apart from and without the content of class struggle. If the shovel fits…….

Probably fits

i find funny that pro China marxists think that Chinese Capitalism is immune to the laws of capitalism and class struggle. Somehow all those billionaires that controls the country care about Socialism(despite treating the chinese workers like disposable garbage) and that some keynesian policies are going to fix all their problems.

Yes, the western news outlets were wrong back then, but now we have evidence that the model China used to grow is not going to last long. The surplus of cheap labor from the country is depleting, strengthening the bargaining power of the workers in urban areas to demand higher wages, hastening the fall of the already rapidly declining profit rate.

To combat this, China is exporting capital and jobs to poorer asian and africans countries, to exploit those countries at the expense of the working class(both chinese and foreign), not unlikely how the West did in the 1980s. This is brewing inter imperialist rivalry between the West and China.

The CCP knows their only chance to keep China’s Capitalism growing and thus holding their control over the country working class is to become a new Imperialist power, emulating the west financialization and desindustrialization(already happening).

It’s not going to happen suddenly, it’s a slow decay and we already seeing the signs of it, but there is much profit to be made yet.

By 2030s the pro China marxists are going to witness that there is nothing special about China, it’s just a semi-peripheral country that managed to accumulate enormous amount of profit thanks to the inhuman exploitation of hundreds of million of people and that it benefited from:

first: The Socialist revolution gains and sovereignty (higher education, infraestructure, life expectancy than others peripheral countries, lots state owned enterprises, land reform, nuclear bomb, transfer of technology deals, control of information flow against western backed color revolutions, centralized state).

Second: from opening up at the right time, when western capitalism, after 30 years of strong welfare state and labor unions, was in crisis, starving for new profits to make, China came to offer hundreds of million of relatively high educated cheap labor for them to exploit, with the CCP relying on some fascistic measures to make sure the workers do not step out of the line.

Your argument is actually two arguments.

1. The first argument is the question of History. Any given new mode of production, when newly installed, will go through a turbulent and very dangerous period of transition. The old mode of production will fight to the end to continue to exist (restoration, counter-revolution), while the new mode of production will fight to continue to be born.

The new mode of production is considered victorious over the old when it becomes irreversible. Irreversibility is the philosophical concept that determines when a new era in History definitely begins, when the new mode of production becomes the “old”. Every mode of production seeks to be irreversible; that’s its fundamental impulse.

So, what happens to China right now is that it represents the new at a historical moment when the old is still very well alive and kicking. China-as-socialism will fight to the very end to continue to be born, while the rest of the world will fight to the very end to continue to exist. This is not a game, there are no rules, all the weapons and tricks are allowed — this is humanity’s fate at stake.

2. The second argument is the actual system that is operating in China right now. The question can be answered very simply and quickly: China’s socialism is not immune to the “laws of capitalism and class struggle” — but it is closer to that than the capitalist world. Therefore, it is more probable that class struggle and capitalist crises deepen and break out in the capitalist world before China.

“By the 2030’s the pro China marxists are going to witness there is nothing special about China….”

But Boi, what is “special” (socialistic?) about a country where, long before 2030 the “billionaires that controls the country….[treated] Chinese workers like disposable garbage…”?

I don’t know what a pro Chinese marxist is, but, if you mean a someone who admires what the Chinese people have accomplished under the direction of the CPC, and who opposes US/NATO terror, threats of war, and imperial sanctions, I’m one of them.

Social democrats who are “Marxists” in their rhetoric but imperialist and anti-communist in their allegiances, always oppose actualy existing “socialist” states.

“I don’t know what a pro Chinese marxist is, but, if you mean a someone who admires what the Chinese people have accomplished under the direction of the CPC”

What the revisionists in the CCP have accomplished:

The restoration of Capitalism in China.

The dismantle of the welfare state and workers rights that existed in China.

Ruined the life of hundreds of million of chinese people who had to live working 16 plus hours every day in sweatshops and factories in the most inhuman condition to enrich foreign capitalists.

Created a new wave of revisionists, who focus entirely on forces of production and not on class struggle or relations of production, and thinks the billionaire infested, boderline fascist current CCP is secretly planning a 180 to Socialism(see the VK response to me)

And finally! saving Capitalism from its biggest crisis in the 1970s, restoring the profit rate for western capital, strengthening western imperialism(was in decline before that), which led to the demise of what left of the former socialist block. In a way, you could say that the opening up of China for western capital not only ended Socialism in China but globally as well. Not to mention that others Global South countries got ravaged by Neoliberalism(which is nothing more than western corporations moving to China, restoring the profit rate and strengthening western imperialism over the Global South and former Socialist block).

So to put it simple, the opening up of China in the 1970s was one the biggest setbacks to Communism, second only to the failed Germany Revolution of 1918–19.

“who opposes US/NATO terror, threats of war, and imperial sanctions, I’m one of them.”

Of course they do!

they want to replace: “US/NATO terror, threats of war, and imperial sanctions”

with: “Chinese/Russian terror, threats of war, and imperial sanctions”

“Social democrats who are “Marxists” in their rhetoric but imperialist and anti-communist in their allegiances, always oppose actualy existing “socialist” states.”

There is only two remaining “socialist” but deep revisionist states: Cuba and DRPK.

I will conclude on this point. One of the problems with corporations reshoring to India from China was that Indian workers enjoyed better labour protections in India than in China. In fact a couple of Indian states revised their labour laws under pressure from Foxconn and Apple so that overtime work was no longer protected in order to satisfy these predators. Ahh, the workers paradise in China.

I believe that China’s social credit system finally clamped down on Foxconn and Apple, which might have been one of the influences (the other being US sanctions) for the “reshoring ” of those sterling corporations to India. .

..”Workers paradise” is a contemptuous Western bourgeois term for really existing “socialist” (“necessarily transitional “state capitalist” ) revolutionary states….

In honesty I must add to the above my gut feeling is that it’s high time the CPC spokespeople dress more casually and shelve their bankers’ monkey suits or they will prematurely find themselves buried in them.

“…Indian workers enjoyed better labour protections in India than in China.”. Nothing could be further from truth than this.

Thanks for your work, but in this case, we should go beyond the dichotomy between investment and consumption. The reason is, in many cases, the two are united, such as in the case of real estate in China: from an investment point of view, since land in China is entirely state-owned, the governments of the various cities need to raise funds quickly by leasing the right to use the land, and then investing them in infrastructures, such as subways, highways and power grids. The infrastructure not only pushes up the price of land but also the cost of the land. These infrastructures not only drive up the price of land but also boost the local economy.

In this process, the government passes on the cost of infrastructure to the price of housing because, as we all know, the government doesn’t produce goods. By selling the right to use the land, the government makes a one-time advance payment on the revenues generated by the infrastructure in the next twenty years. The private real estate capitalists play the intermediary role for a long time and take the profits in the process. You could think of these real estate developers as nothing more than government gloves: a means of raising money from people.

At the same time, the construction of residential buildings requires a lot of labour. It consumes all kinds of building materials and construction machinery, providing a huge amount of jobs in the process. From a consumption point of view, the purchase of a house is also an incentive for the population to spend, which leads to a boom in the household appliances and furniture industries. It can be seen that in China, investment and consumption are actually interconnected, and their link is real estate.

However, after 2016, the situation began to change; firstly, as the proportion of urbanization in China rose to a high level, its speed began to slow down, and secondly, after these real estate capitalists ingesting wealth for more than a decade, they have already become too large that they began to expand their influences in other industries, especially the financial industry, and in this process transferred their wealth abroad, they expecting or dreaming the exchange rate of the RMB after the trade war between China and the United States would collapse like the Thai baht did in the ’97. After that, they could use these transferred funds to return to China and buy-in all kinds of high-quality assets at low prices. In other words, they chose to “short” China. Fortunately, this fantasy didn’t come true, but that doesn’t mean Beijing didn’t notice their behaviour.

And so it is. When these real estate companies were on the verge of collapse due to the collapse of their previous Ponzi schemes, although they were counting on being able to pressure the government on the grounds of being “Too big to fail” like their American counterparts, the government was not interested in providing them with as much relief as the US did for Chrysler in 2008 because They need to pay the price for their own greed. Meanwhile, Beijing needs to emphasize the fact that the government still holds the lion’s share of construction capacity in China because even though the state-owned construction companies have become highly specialized over the past 30 years and more adept at building large, technically difficult and complex national projects, doesn’t mean that they lack the capacity to build large numbers of homes.

The privately owned property companies in China were born in a different age when too many people crowed to the urban; now it is the time to change policy, but the government also has huge pressure on finances, which matters the investment and it needs to keep the unemployment rate at a low level, which matters with the consumption, so it is a painful dilemma.

a) As a fact, economic growth is stopping (‘the great stagnation’ USA) and where is not, in decades will be; undoubtedly in China too. We can argue about how to share the remaining surplus b) population growth continues albeit a slower pace (9 + billions of humans) nonetheless environmental destruction continues at fast pace (consider the Amazonian forests) c)The first steps to mitigate catastrophic these times are a redistribution of wealth, an economy in which production and consumption address only the most basic needs worldwide (a global and radical austere socialism ) plus a rigid control of population. Growth therefore would be less than O. This program is unlikely but is the only chance to avoid the accelerating Malthusian present (wars, famines, floods, diseases, climate change etc.). Quite a sober present and future but, considering the current summer temperatures (land and oceans) and other environmental indicators, without this radical transformation the future is much worse. By the way, the large rivers of Asia begin in the Himalayas and the glaciers are melting.