China’s Evergrande Group is the second largest property developer in China and it is teetering on the brink of bankruptcy. Evergrande has hired ‘restructuring advisers’ and warned that its liquidity is under “tremendous pressure” from collapsing sales, facing protests by home buyers and retail investors. Based in Shenzhen in southern China, Evergrande is saddled with almost Rmb2tn of total liabilities or over $300bn.

The share price of the parent, 3333 HK, is down 76% from where it started the year. In August, Xu Jiayin, Evergrande’s founder and one of China’s wealthiest men, stepped down as chairman of the property group. Trading in the company’s bonds has been suspended in Shanghai. Police descended on Evergrande’s office building in Shenzhen when individual investors in the company’s myriad “wealth-management” products gathered to demand repayment.

Evergrande’s demise is a reflection of the dangers of uncontrolled property speculation in the capitalist sector of China’s economy. Evergrande relies heavily on customers paying for flats before the projects are completed. The Evergrande property model is essentially a Ponzi scheme, where the company collects cash from the pre-sale of an ever-growing number of apartments, plus hundreds of thousands of individual investors and uses the cash to fund further sales by accelerating construction in progress and funding down-payments. Like any Ponzi, this works as long as it’s accelerating. But when the market slows, those incoming streams of cash start to fall behind the growing arc of cash demands. Evergrande now has about 800 unfinished projects and there are about 1.2 million people waiting to move in.

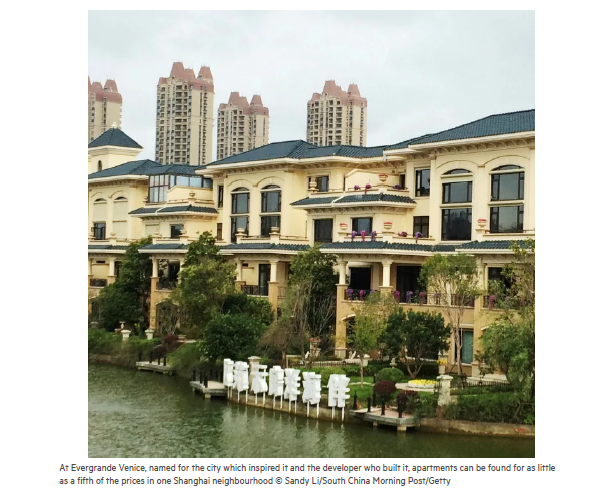

Take one huge Evergrande project. Prices for Evergrande’s Venice properties (situated on the coast 90km from Shanghai) have tripled since sales began in 2012 and 80% of the apartments have been sold in total, though about one-third are unoccupied. But this year sales have slowed. Data from the Qidong municipal housing bureau shows around 60% of the apartments that went on sale have been sold, despite a 15% price discount. Evergrande has now discounted all its apartments by as much as 30% and it has also sought to raise cash through spinning off its stakes in other companies.

What Evergrande reveals is the end game of the huge urbanisation drive that started off to house China’s people. In a transformation of China’s cities, the urbanisation rate surpassed 60% last year compared with 50% in 2011. But because this urbanisation was eventually conducted by the private sector for profit and based on owner-occupation (90% of Chinese own their homes mostly without mortgages), residential property construction has become a financial asset investment, just as it was and is in the major G7 economies. This ‘financialisation’ began in the late 1990s, when the government pursued a policy of making state-owned companies offload their residential assets to their employees – a Thatcher-type selling to council tenants. The idea was that the private sector would look after housing, not the state, from then on.

So instead of housing “being for living in” (Xi), it has become a sector “for speculation” (Xi). Apartments in China have become the investment vehicle of choice for people. Few buyers purchase an Evergrande apartment as their primary residence. And Evergrande has explicitly catered to the better-off Chinese, choosing locations that fall just outside of areas that restrict the number of units a person may buy and advertising the developments as second homes. All over China, even sales clerks and factory workers are sitting on empty Evergrande apartments and dreaming of selling them at a big mark-up to fund their children’s study abroad or their own retirement.

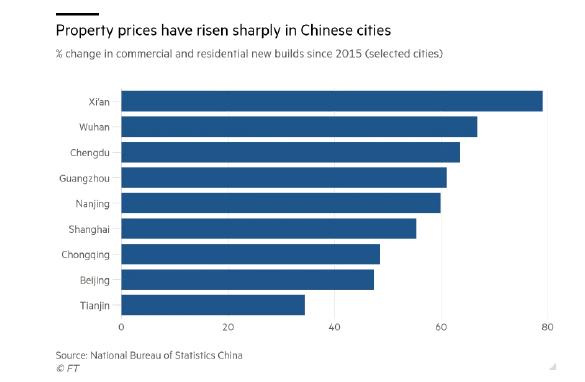

Property prices in coastal cities, where the best work and pay is, have doubled in the last ten years. In Shenzhen, the average apartment price has risen so much that some are finding it cheaper to live in Hong Kong, one of the most expensive property markets in the world. Since 2015, residential property prices have appreciated by more than 50% in China’s largest cities. Over the past decade, average residential land supply per new resident in the top ten cities is only 230 square feet—little more than the size of a typical hotel room—or less than 60% of the average per capita residential space in China.

Speculation has been rife as local governments try to raise funds by selling land to developers which then build estates through borrowing at low rates often from the unregulated shadow non-bank sector. “Property is the single most important source of financial risk and wealth inequality in China,” said Larry Hu, head of China economics at the foreign-owned Macquarie Securities Ltd. And he is right.

Much of the property speculation has been to build ever more commercial developments rather than housing. That’s because the main prerogative for local governments is to accrue revenue. If they can attract more businesses into their jurisdictions and if those businesses become profitable, then the local government can collect more corporate taxes. At the same time, residential land supply is deliberately kept scarce so governments can make money on residential land sales. In effect, residential land sales serve as a cross-subsidy on local governments’ pro-business land policy that sells commercial land cheaply.

The real estate sector now accounts for 13% of the economy from just 5% in 1995 and for about 28% of the nation’s total lending. Given that local governments have $10 trillion in debt, land sales are the most crucial and reliable source of income for debt repayment. So any drastic changes would seriously raise the risk of local government defaults.

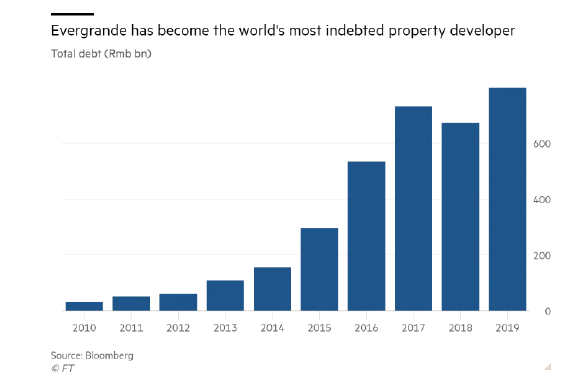

The private property sector’s approach has relied on taking on large quantities of debt to accumulate more and more land — sometimes in speculative areas outside of major cities. In Evergrande’s case, it has enough land to house the entire population of Portugal and more debt than New Zealand. In 2010, it had just Rmb31bn ($4.7bn) in debt and had $190bn of properties under development as of the end of 2020.

The group’s mounting credit woes have coincided with the change in government policy towards the “disorderly expansion of capital”; against big technology groups, the real estate industry and other sectors. The country’s housing ministry announced a three-year inspection campaign to tighten regulation of the property sector. Last year, the government implemented a strict policy aimed at reducing developers’ leverage, which China’s banking regulator has labelled the country’s biggest financial risk. The banks have been told to jack up mortgage rates. Local governments are being directed to accelerate the development of government subsidized rental housing and have been told to increase scrutiny on everything from financing of developers and newly-listed home prices to title transfers.

And in a classic case of ‘financialisation’, Evergrande financed its activities by issuing what are called ‘wealth management products’, in effect mortgage-backed bonds for foreign and Chinese retail investors to buy, paying high interest rates (7-9%). Now the company is declaring its inability to meet these obligations. This uncontrolled expansion of debt by Evergrande and other property companies was ignored by China’s regulatory authorities, just as it was in the US leading up to the property and financial bust in the global financial crash in 2008.

What is going to happen, if and when Evergrande goes bust? Will other property companies crash too?; are we heading for a huge financial crash in China and possibly globally, sparked by the end of China’s property boom? Well, there are four other major Chinese property developers on the brink. The prices of the dollar bonds issued by these companies have collapsed on fears by international investors that those bonds cannot be refinanced when they mature, which would mean a default. So foreign investors in these bonds are taking a big ht. And the ability of these property developers to issue new debt to raise new money to refinance has disappeared.

But in my view, there is not going to be a financial crash in China. The government controls nearly everything, including the central bank, the big four state-owned commercial banks which are the largest banks in the world, the so-called ‘bad banks’, which absorb bad loans, big asset managers, most of the largest companies. The government can order the big four banks to exchange defaulted loans for equity stakes and forget them. It can tell the central bank, the People’s Bank of China, to do whatever it takes. It can tell state-owned asset managers and pension funds to buy shares and bonds to prop up prices and to fund companies. It can tell the state bad banks to buy bad debt from commercial banks. So a financial crisis is ruled out because the state controls the banking system.

But if not a crash, what about the property bust and the high levels of debt incurred? Won’t they reduce China’s ability to grow at the pace previously achieved and targeted for the next five years? Western economists are clear on this: the debt is so large and China’s productive sectors are now so weak that even if China avoids a financial crash, the hit to household incomes and the profits of the capitalist sector are large enough to reduce investment and GDP growth. China is heading for stagnation, if not a slump.

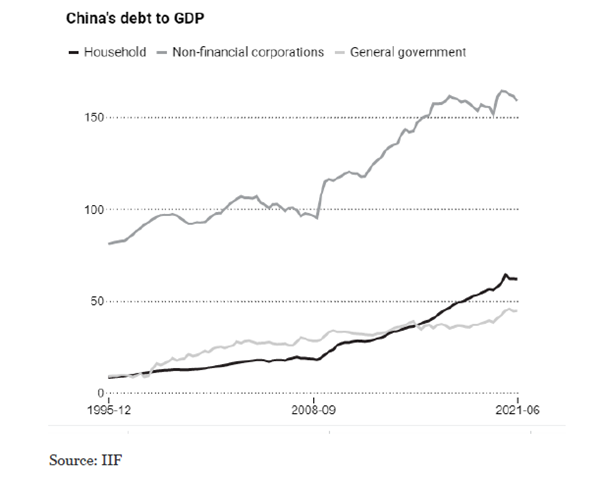

It’s true that China has built up a debt mountain in recent years, of which property debt is a significant part. Total debt hit 317% of GDP in 2020. But most of this debt is in domestic currency and is owed by one state entity to another; from local government to state banks, from state banks to central government. When that is all netted off, the debt owed by households (54% of GDP) and corporations is not so high, while central government debt is low by global standards. Moreover, external dollar debt to GDP is very low (15%) and indeed the rest of the world owes China way more: 6% of global debt. China is a huge creditor to the world and has massive dollar and euro reserves, 50% larger than its dollar debt.

Chinese leaders want to curb the debt level. But as I have explained before, controlling the debt level can come in two ways; either through high growth from productive sector investment to keep the debt ratio under control; and/or by reducing credit binges in unproductive areas like speculative property. The latter would mean a reduction in the profitability of the capitalist sector in China and this would lower the potential for productive investment by that sector. So the loss of profits and household income from property busts would add to downward pressure on growth of output and incomes.

But that forecast is based on the view that the Chinese government should continue to rely ever more on its capitalist sector to deliver. And yet China’s capitalist sector is in trouble in many ways just like in the G7 economies. Profitability in the capitalist sector has been falling and is now at all-time lows; and much of its activities are increasingly in ‘unproductive’ sectors like consumer finance, property or social media.

Again, as I have argued before, the basic contradiction of China’s economy is not between investment and consumption, or between growth and debt; it is between profitability and productivity. The growing size and influence of the capitalist sector in China is weakening the performance of the economy and widening inequalities. In my view, the Chinese economy is now strong enough not to rely on foreign investment or on unproductive capitalist sectors for growth. Increasing the role of planning and state-led investment, the main basis of China’s economic success over the 70 years of the People’s Republic, has never been more compelling.

Read or toss, but I thought you might find this to be interesting.

Sent from my iPhone

>

Topical post with good data. Consequential. You point to the financial insulation of the Chinese economy. True. But on the other hand China is not industrially insulated. Your emphasis is wrong. China is the dominant industrial economy and property/infrastructure one of its key drivers. When China stumbles the world wobbles. We need think no further than copper, iron, coal, industrial equipment and the like. The last time this happened in 2015 and 2019, growth in the world economy came to a standstill. Only this time it is worse. Evergrande is not Lehman Brothers. Lehman Brothers was only a bank. This a building contractor with a spiderweb of suppliers both within and without China.

But it is not only China where the game is up. Given your background you must be privy to communications from US banks. They are flashing red. The advice to their wealthy clients is “get the hell out of Dodge (Wall Street). We always knew that the second half of the year was going to be problematic for capitalism and it is on all fronts. Love it.

Just a tongue in cheek comment. I know you have an inbetweeners view of China. But does not your comment “This uncontrolled expansion of debt by Evergrande and other property companies was ignored by China’s regulatory authorities” suggest that actually the Chinese State looks like a capitalist duck; it acts like a duck, it walks like a duck despite quacking like a parrot.

Maybe it’s a paradox and can talk…but doesn’t speak your language.

Good comments from you and Michael. I’m urging China to go MMT; the sight of all those unfinished housing estates being demolished because private developers have gone bust is very depressing, in a ‘socialist’ nation who can choose to create debt-free public money ‘ex nihilo’, and turn those estates into government-funded housing for low income workers.

In the past in Brazil, cyclically, a large construction company went bankrupt by a Ponzi-type scheme. Despite the country’s disorganization for more than a decade, the problem was solved by individualizing each real estate launch. Accounting is individualized and each real estate release cannot use money from buildings already under construction.

It settles because if a launch goes bankrupt, there is no spread to others, if the construction company goes bankrupt, the good businesses are bought by other developers, the bad ones….

It is easy to regularize the system.

“…the main prerogative for local governments is to… collect more corporate taxes. At the same time, residential land supply is deliberately kept scarce so governments can make money on residential land sales. In effect, residential land sales serve as a cross-subsidy on local governments’ pro-business land policy that sells commercial land cheaply…Given that local governments have $10 trillion in debt, land sales are the most crucial and reliable source of income for debt repayment. So any drastic changes would seriously raise the risk of local government defaults.”

It is one thing for the central government to issue directives to local governments, but it is another thing to exercise effective control. This depends on the central government having the administrative capacity to ensure directives are properly executed. So far as I know planning/supervisory bureaucracies have been heavily pruned. The increasing reluctance even to set goals I think shows that. Also, the resources to do this do depend on the physical resources, not just financial but industrial/commercial. The reduction of the SOEs’ remit, which to me seems like another version of the “cross-subsidy” from state to “private” hands, Do they any longer have the capacity to provide housing for use?Last, I’m not sure that this kind of problem doesn’t obtain in the agricultural sector too, where land has been preferentially reserved to commercial farmers. The problem is, central government interference with local government financing—as local governments would perceive it—seems likely to disorder the commercial agriculture system.

The party personnel in local governments have their local constitutencies. For decades the central government has firmly committed to the proposition that the serious people are the ones who grow the productive forces. (And the inverse, the Maoists who are flighty sectarians who are evil incarnate destroying everything.) China is so vast, that what looks on a map merely like a state or country, is plausibly deemed to be the equivalent of a medium sized country. Control of the whole country has always been a significant task, often failed. The last such period was the warlord period of the twenties in the last century, only partly done away with by the famous Northern Expedition.

“Increasing the role of planning and state-led investment, the main basis of China’s economic success over the 70 years of the People’s Republic, has never been more compelling.” I wholeheartedly agree. From your lips to God’s (Xi’s?) ears.! But the current government in China is deeply committed to the proposition that everything China has achieved began in 1976, when the Dark Ages ended with the fall of the Gang of Four.

Evergrande Gave Workers a Choice: Loan Us Cash or Lose Your Bonus

When the troubled Chinese property giant Evergrande was starved for cash earlier this year, it turned to its own employees with a strong-arm pitch: Those who wanted to keep their bonuses would have to give Evergrande a short-term loan.

Some workers tapped their friends and family for money to lend to the company. Others borrowed from the bank. Then, this month, Evergrande suddenly stopped paying back the loans, which had been packaged as high-interest investments.

–NY Times, September 19, 2021

Mr Roberts, if you conclusion is correct, is China the worst (and only) threat to global capitalism? I mean, the phrase ” In my view, the Chinese economy is now strong enough not to rely on foreign investment or on unproductive capitalist sectors for growth. ” would mean that they have demonstrated a real and functioning alternative to capitalism at large.

No…. capitalism contains the seeds of its own destruction.

Evergrande case examplifies unbridled capitalism that Xi Jinping is trying to regulate. Evergrande examplifies unbridled capitalism destroying the environment of human beings, the animals and the vegetal. The destruction of Amazon forest, the lungs of the earth shows how unbridled capitalism can damage the common good of mankind. Evergrande examplifies unbridled capitalism when feeding and housing fall into the clutches of the private sector whose main objective is profit

“most of this debt is in domestic currency… is owed by one state entity to another; from local government to state banks, from state banks to central government. When that is all netted off,…” The contradictory interests of the different entities, governments, and banks are real. No one of them wants to take the fall. It will not be easy to “net it all off.”

The PBofC (China’s central bank) could “net it all off” by means of a few computer key strokes, because the PBofC is owned by the government.

Inflation not a factor, because the infrastructure/resources already exist.

Word. All of the debt in the US mortgage market was in domestic currency. Didn’t help Bear Stearns, did it? Or Countrywide? Nor did carrying the debt denominated in Euros help Sachsen LB in Germany.

The central bank could have repaid the public debt denominated in the nation’s own currency with a few computer key-strokes, without causing inflation (since the public debt was owed to private sector bond holders)

“the capitalist sector of China’s economy.” The entire economy is capitalist. The state-owned enterprises are run to enrich princelings and high officials, to garner surplus value for specific parts of the government, and to keep the holders of the shares happy. (Yes, most SOEs have issued stock. It is usually a small minority of the total booked equity, but the investors still need to be satisfied.)

“The central bank could have repaid the public debt denominated in the nation’s own currency with a few computer key-strokes, without causing inflation (since the public debt was owed to private sector bond holders)”

The role of the central bank is to protect the “primary lenders”– namely the investment banks that trade in and make the market in government debt. Wiping out the debt without coincident liquidation of the encumbered enterprises is merely kicking the can down the road. What counts is not debt. It’s earnings because earning determine how likely and costly refinancing will be.

It’s not that your asking the leopard to change its spots; you’re asking it to change its diet.

“The role of the central bank is to protect the “primary lenders”– namely the investment banks that trade in and make the market in government debt”

But the main role of a government-owned central bank *should* be to issue debt-free money into the economy, to implement government policy (since the competitive for-profit private sector will never do it) , and consistent with the economy’s productive capacity.

That’s certainly “changing both the leopard’s spots and diet”….no doubt.

You’re going to have to do more than that. You’ll have to change the leopard

The comment about builders being more like speculators in China. The same applies to the US. Here is the latest data from Econoday which may interest your readers. New home sales, 36% bought off plan (before construction) 42% were under construction and only 22% were already built.