Marx’s model of capitalism assumes a world economy, and starts with ‘capital in general’. It was at that level of abstraction that Marx developed his model of the laws of motion of capitalism and, in particular, what he considered was the most important law of motion in the capitalist process of production, the law of the tendency of the rate of profit to fall.

The rate of profit is the best indicator of the ‘health’ of a capitalist economy. It provides significant predictive value on future investment and the likelihood of recession or slump. So the level and direction of a world rate of profit can be an important guide to the future development of the world capitalist economy.

However, in the real world, there are many capitals; and not just one world capitalist state, but many national capitalist states. So there are barriers to the establishment of a world economy and a world rate of profit from labour, trade and capital restrictions designed to preserve and protect national and regional markets from the flow of global capital. Even so, the capitalist mode of production has now spread to every corner of the globe and the ‘globalisation’ of trade and capital flows makes the concept of measure of a world rate of profit more realistic and discernible.

My first attempt to measure a world rate of profit was in a paper in 2012. A proper measure of the world rate of profit would have to add up all the constant and variable capital in the world and estimate the total surplus value appropriated by this global capital. At the time, this seemed an impossible task. So a weighted average of national profit rates was the only feasible way of getting a figure.

I attempted to develop a world rate of profit that included all the G7 economies plus the four economies of the BRIC acronym. This covered 11 top economies and constituted a significant major share of global GDP. Then I used the Extended Penn World Tables as constructed by Professor Adalmir Marquetti from Brazil. I weighted the national rates for the size of GDP, although the crude mean average rate did not seem to diverge significantly from the weighted average.

I found that 1) there was a fall in the world rate of profit from the starting point of that data in 1963 and the world rate never recovered to the 1963 level up to 2013; 2) the rate of profit reached a low in 1975 and then rose to a peak in the mid-1990s; 3) after that, the world rate of profit was static or slightly falling.

Then in 2015, I revisited the measurement of a world rate of profit . In the intervening period, Esteban Maito had done some ground-breaking work using a similar method of measurement (national rates weighted by GDP) for 14 countries, but using national statistics, not the Extended Penn World Tables, and going back to 1870 for some countries. Maito confirmed my more limited study of a clear downward trend in the world rate of profit, although there were periods of partial recovery in both core and peripheral countries. Maito revised and updated his work for a chapter in World in Crisis: a global analysis of Marx’s law of profitability – essential reading.

The graph below is my adaptation of Maito’s work.

Maito showed that the behaviour of the profit rate on capital stock confirms the predictions made by Marx about the historical trend of the mode of production. There is a secular tendency for the rate of profit to fall under capitalism and Marx’s law operates. Maito also found that there was a stabilisation and even a rise in the world rate of profit from the early or mid-1980s up to the end of the 1990s, the so-called neoliberal period of the destruction of trade unions, a reduction in the welfare state and corporate taxes, privatisation, globalisation, hi-tech innovation and the fall of the Soviet Union. Again, Maito showed that this recovery peaked about 1997.

The measurement of the world rate of profit my 2015 paper (Revisiting a world rate of profit June 2015 ); this time used the more up to date Penn World Tables 8.0 for data based on the G20 top economies. These results exhibited a similar secular decline as did the Maito data. There was a significant fall from the first simultaneous international economic slump in 1974-5 to the early 1980s, then a modest recovery before another fall coinciding with the world 1991-2 economic recession. There was a mild recovery in the 1990s until the early 2000s. After that, the G20 rate of profit slumped, both before the 2008-9 Great Recession and after, with only a tiny recovery up to 2011.

I backed up these results with data from the Eurostat AMECO database, which are even more up to date. The issue with AMECO data is that its measure for net capital stock is highly dubious, especially in the early years from 1963. However, from the early 1980s, the AMECO profit rate follows that of the Penn Tables measure.

Now I have taken a third look at the world rate of profit using the latest Penn World Tables 9.1 data. This latest database has an important innovation. It has a new series called the internal rate of return on capital stock (IRR), a very good proxy for the Marxian rate of profit. Because the data are compiled on the same categories and concepts, the IRR series offers a valuable comparison between national rates of profit and it is also extended to 2017. So we now have a series for the rate of profit for nearly all countries in the world, starting in many cases from 1950 up to 2017. (Internal rate of return)

In future posts on this, I shall consider any measurement problems with IRR and other categories; explain my methodology; and provide sources and workings. Also, I shall look at decomposing the rate of profit into its key factors, namely the organic composition of capital and the rate of surplus value. This decomposition is important. It is one thing to show a falling rate of profit over time; it is another to show that this is caused by Marx’s law of the tendency for the rate of profit to fall. It could have other reasons.

If Marx’s law is correct, then it follows that when the rate of profit falls, the organic composition of capital (C/v) should be rising faster than the rate of exploitation (s/v). Under Marx’s law, a rising organic composition of capital is the tendential determining factor for the fall in the rate of profit and the rate of exploitation is the (main) counteracting factor to that. If the latter rises faster than the former, then the rate of profit rises – and there have been periods when that has happened. But over the secular long term, the rate of profit falls and that is because the organic composition of capital rises more than the rate of exploitation.

I shall not discuss these issues in this post, but just consider the main results of measuring the world rate of profit using the IRR series in the Penn World Tables. I have weighted the IRR series for the size of capital stock (not by GDP as in previous papers) to obtain a better measure for the G20 economies (19 countries excluding the EU), and also for the top G7 imperialist economies; and for selected emerging or developing economies.

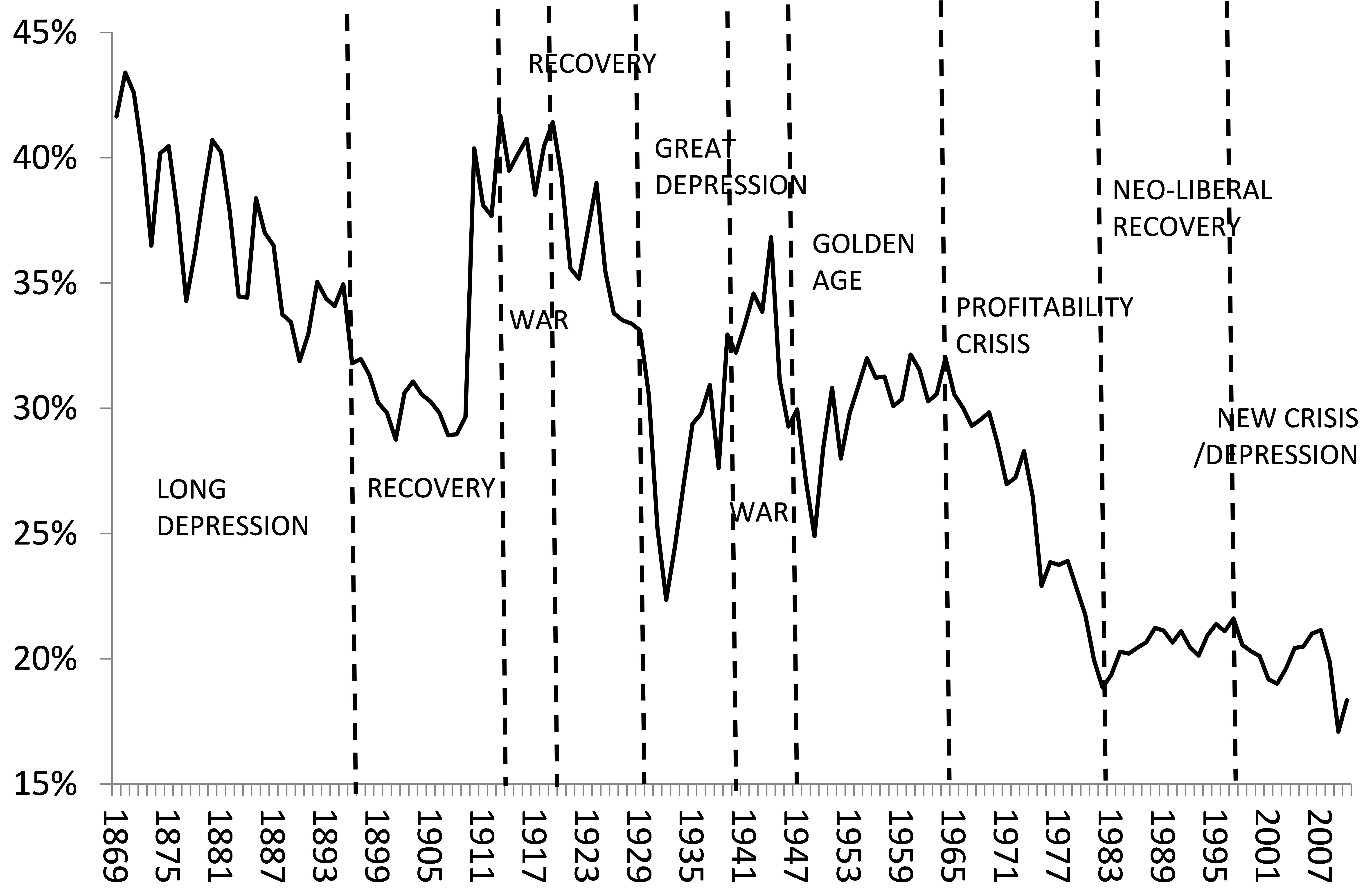

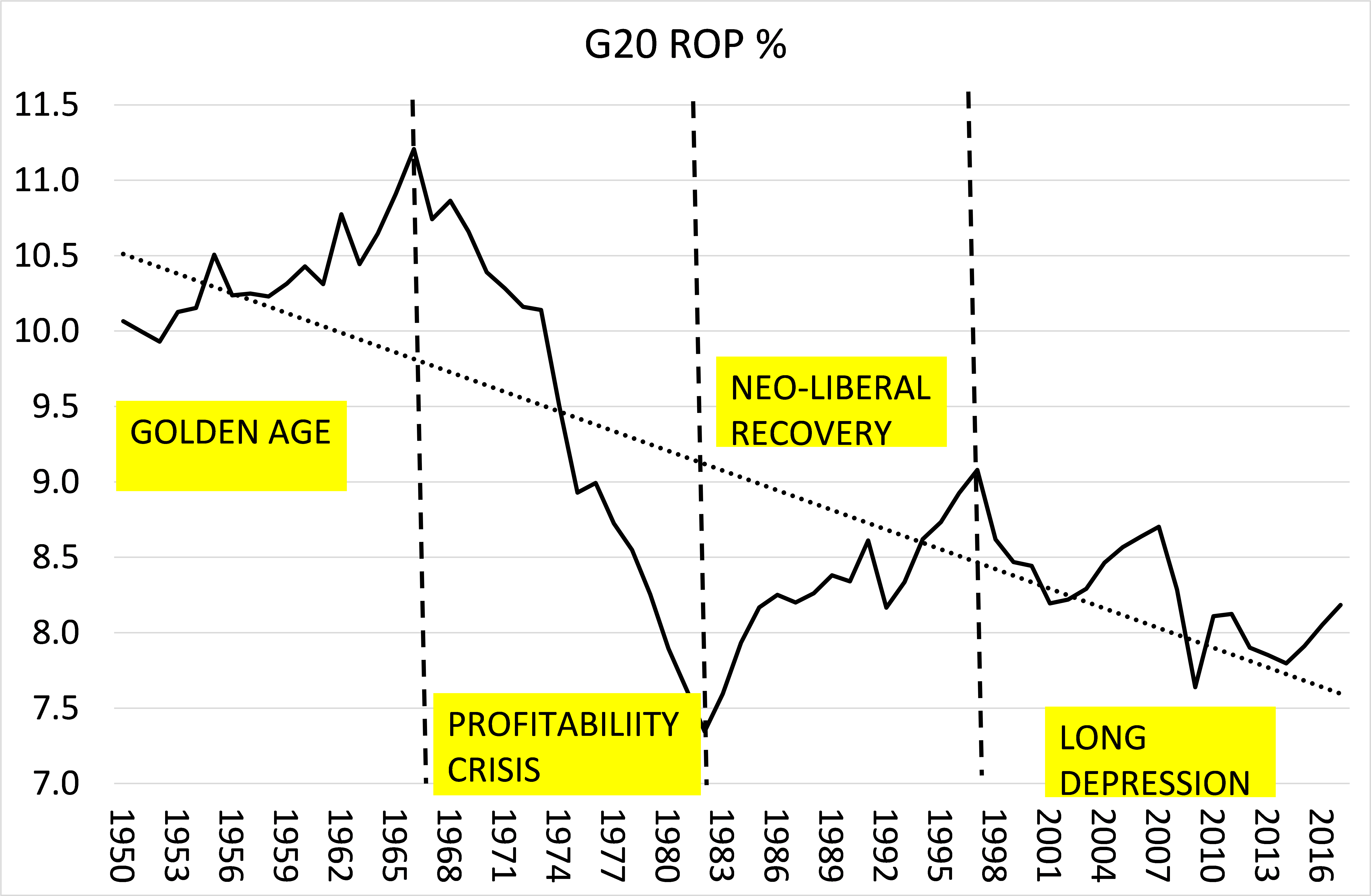

The G7 results confirm the results from my previous two measures in 2012 and 2015; that the rate of profit in the major imperialist economies has been in long-term decline. The rate has not been a straight line down, but can be divided into four periods: 1) the ‘golden age’ of high and even rising profitability from 1950-1966; then the huge profitability collapse from 1966 to 1982; then the (relatively weak neo-liberal recovery); and since a peak in 1997, a general depression in the rate of profit up to 2017 (when the data end).

Now with the IRR series we can measure better the G20 rate of profit, probably the closest we can get to a ‘world rate’. This measure should be better than Maito’s or any previous measure because it includes more countries; although Maito’s ground-breaking work measures rates of profit back into the 19th century, not just to 1950.

The G20 rate of profit matches that of the G7 rate of profit in its trajectory.

But note that the level of the rate of profit is generally higher than the G7 rate. This should be expected under Marx’s law because the organic composition of capital will be higher in the imperialist countries than in the developing countries that are still trying to ‘catch up’ in technology. We shall return to this point in a future post.

Indeed, let’s look at the rate of profit in some selected developing economies, in particular those G20 members, such as Argentina, Brazil, Mexico South Africa, China, India, Indonesia and Turkey. Again, we find that the rate of profit falls over the long term, but with the four sub-periods similar to the G7 and G20 series.

But again, note the much higher level of the rate of profit, up around 24% in the Golden Age compared to just 10% in the G7 economies and falling to 10% in last sub-period compared to 6.5% in the G7. Also, the turning point into the neo-liberal period is later; in 1989 compared to 1982 for the G7. And for these developing economies, any profitability recovery is short-lived, crashing back in the emerging market crisis of 1998. The long depression in profitability in developing economies has ensued since.

Thus we can sum up these initial results from the Penn World Tables 9.1 IRR series as confirming the long-term decline in the world rate of profit (ie for most of the major and larger economies), with various subperiods, just as was discerned in the previous two measures of 2012 and 2015.

In future posts, I shall expand on these results. I shall look at the decomposition of the world rate of profit and the factors driving it. I shall consider the rate of profit in specific key economies (US, Germany, Japan, China) to see what we can learn. I shall try to relate the change in the rate of profit to the regularity and intensity of crises in the capitalist mode of production. And I shall consider the question posed and answered in Maito’s work: if the world rate of profit is set to decline, will it go to zero and how is that possible?; and if so, how long will it take? And what does that tell us about capitalism itself?

Shouldnt the fall of soviet union effect the rate of profit?

I have the impression that it opened new markets.

The cheapening of capital goods can slow down or stop a rising organic composition of capital.

Yes. I shall take up this point in a future post.

Michael surely you recognise that something is wrong with this crude approximation of the rate of profit. The rate of return peaks in 1996 just as globalisation accelerates. So the whole period of globalisation, associated with China’s phenomenal industrialisation, with a vast growth (+1 billion) in productive workers, yes you get it, is associated with a falling rate of profit as measured by return. Hmmm. Economy wide figures even world scale economy wide figures are meaningless because of duplications.

And in case you riposte with the crude composition of capital based not on surplus value but on annual compensation, I would like to remind you I have provided ample empirical evidence to show that in many advanced capitalist economies, the ratio of fixed to circulating capital has not advanced since 2008.

The only thing that matters from an investment point of view is the enterprise rate of profit, nothing else. That is pre-tax profits over fixed and circulating capital. When that is done, Eureka, we have a rate of profit which corresponds to the movement of globalisation and whose collapse after 2013-14, corresponds to the exhaustion of this phase of globalisation. The Penn figures make a mockery of the actual movement in the rate of profit. If the rate of profit guides investment as it does, then overlaying the Penn data on the actual movement of the world economy from the mid-1990s makes no sense.

I think it is time to abandon this approach because you are putting at risk the dynamic connection between profitability and the shape of the world economy.

Dear Michael

as ever a stimulating piece. However I take issue with your initial claim that Marx theoretically formulated a world rate of profit. Not so.

Marx establishes the general (average) rate of profit that through the transformation of commodity simple exchange values to their prices of production in part 2 of ‘Capital’ Volume 3. He is quite explicitly that this is a national rate of profit, but does not see a problem in principle in moving from a national rate of profit to an international one, except he didn’t do it; and there is a problem.

To state the obvious, part 2 comes after part 1 and before part 3. In part 1 Marx sets up the conversion of surplus value as being dependent on the compound of the rate of surplus value, the rate of turnover or variable capital, and the organic composition of capital. His part 2 solution to the formation of prices of production and the rate of profit only considers one of the three variables set out in the premise of the problem.

Engels did some work to bring in turnover from Volume 2, but his editorship did not extend to commentary on the missing dimension of variations in the rate of surplus value, that is the indicator of degree of labour exploitation. That is, neither Marx before his death, nor his executor Engels picked up this thread.

The terms of the problem include therefore the possibility of variations in the rate of surplus value, and not only variations in the average or modal organic composition of capital by sector. Variations in the rate of surplus value would require a different intermediate aggregate category other than industrial sector, such as region, or country, or oppressed social group.

In part 3 Marx draws attention to the role of colonially oppressed labour in particular as a counter-acting factor to the tendency of the rate of profit to fall, but he also rejects, or rather delays consideration, of the more general issue of ‘wages below the value of labour power’ as belonging to the realms of competition. But as we can see this is a theoretical mistake, against the terms of a problem that included the rate of surplus value.

A fuller theoretical solution requires further modification beyond the text of ‘Capital’ Volume 3 which only gives us (national) price of production and (national) rate of profit. This is the real unfinished aspect. We have to complete Marx’s theoretical elaboration, The theory then unfolds into explaining international transfers of value by more than sector differences of organic composition writ large, since the departure of price of production (costs +profit) from the commodity’s simple exchange-value is all the greater once the further modifications are taken into account.

Notwithstanding his broader internationalism, it is import that we recognise Marx’s incomplete definition of the rate of profit in ‘Capital’ Volume 3 is methodologically based on capitalism in one country. Thankfully Marx also gives us a strong clue as to how to get beyond this limitation. Changes in the rate of surplus value affect the value composition of capital, but for a different reason than different sector organic compositions, essentially more oppressive social conditions of exploitation. The interplay and tension between ‘cheap labour intensive’ super-exploitation and ‘capital intensive’ strategies is a contradiction, generated within the system considered as a whole that has been hierarchically structured and internally split by colonialism. Our concept of capital in general needs to include this dimension of systemic contradiction and competition, otherwise we miss the deeply inherent dynamic to imperialism of the capitalist mode of production.

Without doing this, empirical findings on national profit rates need careful consideration as to their derivation, especially concerning the source.profits realised in countries like the US and UK, which to a significant degree can represent higher rates of surplus value in the global South.

These latter issues are well evidenced in John Smith’s ‘Imperialism in the 21st century’ and many other works, especially Marini’s breakthrough conceptualisation of labour super-exploitation. What I am indicating here that there is a critical route from ‘Capital’ to explain what is increasingly undeniable, that inequalities of exploitation are structurally essential to the system and, coming back to the point, consequential to the formation of the rate of profit.

A critic.-

‘’ It is one thing to show a falling rate of profit over time; it is another to show that this is caused by Marx’s law of the tendency for the rate of profit to fall. It could have other reasons ’’.

I am staying here for the moment. What other reasons for decreasing profit? The competition, simply. Which makes it happen: a) Decreasing Profit Rate for all companies, b) TGD for 90% of companies (small and medium) and c) But a GROWING TG for private monopolistic companies (Dow Jones, Ftse-100, Cac-40, Ibex35, etc. ..) and for the 1st company, the State. There are several reasons for this. One would be that if this TGD is heeded due to the decreasing operating capital, it will happen that in socialism, or in current cooperatives, there will be no profit, there will be no profitability. Socialism will eliminate (otherwise it will not be socialism) the exploitation surplus and if it is true as the authors of the TGD affirm that the only current surplus value of capitalism and in general comes only from the exploitation surplus, if socialism eliminates the Operating surplus will then remove the surplus, the profit, the total return. Well, that non-profit in socialism is a theoretical and practical impossibility basically because profit is a universal necessity for every living being if it wants to survive (replacing used assets) and grow (new investments) and I won’t say anything else. And in my opinion, and for the same reason, it is an impossible economic fact in capitalism and in any other mode of production.

A compliment.-

The search for a World Profit Rate that is exposed once again in this article is another enormous intellectual boast to which M. R. has become accustomed to his followers. MR is not scared intellectually (just like other even Marxist authors who are. And MR is not scared simply because he knows much and more than others what he talks about) in his research work and if he has to look for a Universal Gain Rate what does. He has demonstrated his ability in a multitude of research papers, that’s all. I recommend reading his work The Long Depression, and especially his chapter on Business Cycles. Cycles that are my little study specialty. If they want to know everything that is known about cycles today, they will do so by reading this fantastic and informative chapter. And if you want to know how capitalism is moving and where it is going (almost with an exact expiration date discovered) delve into one of the cycles of the Chapter: the kondratiev cycles. Kondrativev cycles, on the other hand, that are not caused by price movements or technology diffusion, but that is another criticism.

Regards,

I don’t have the mathematical wherewithal but I was wondering if it possible to plot rate of profit against social factors like unemployments, homelessness, poverty etc. You might think that as rate of exploitation went up to compensate for loss of profits this would result in Dickensian times.

I Would also expect a correlation with energy use/energy prices – again not able to plot it. Less profit, less energy, compensated with drill baby drill to get the profits going again.

Could be interesting research

I agree with you: “The rate of profit is the best indicator of the ‘health’ of a capitalist economy.”

But I would like to add one or the other “caveat”.

Marx assumed that there were several profit rates at the same time:

1) The younger and more productive capital with a higher profit rate knocks out old capital with a lower profit rate. The individual rate of profit, which is higher than the average, explains the extra profit that capital makes. “The extra profit consists in the excess of the individual profit over the average profit. K. Marx, Capital III, MEW 25, 656. ”

2) Marx did not rule out that large parts of an economy (joint stock companies) operate with a lower profit rate than the social average. “Before we go any further, there is an economically important point to note: Since the profit here (in the large stock corporations, in which management and capital owners are separate) only takes the form of interest, such undertakings are still possible if they only yield interest, and it is one of the reasons that the general rate of profit is held back by the fact that these undertakings, where the constant capital is so enormously proportionate to the variable, do not necessarily go into the adjustment of the general rate of profit. “K. Marx, Capital III, MEW 25, 453.

3) Marx also assumed that different economies operate with different profit rates. “To the extent that capitalist production is developed in a country, the national intensity and productivity of work rise above the international level to the same extent. The different quantities of goods of the same type, which are produced in different countries in the same working hours, therefore have unequal international values, which are expressed in different prices, … “K. Marx, Kapital I, MEW 23, 584.

“But the value law is modified even more in its international application by the fact that the more productive national work also counts as more intensive on the world market, as often as the more productive nation is not forced by the competition to lower the sales price of their goods to their value.” K Marx, Kapital I, MEW 23, 584.

A global average profit rate can therefore only act gradually and only as a trend.

A global rate of profit becomes effective in international companies that exploit labor in several countries. For companies that only operate in one country, a “world profit rate” is more or less irrelevant.

(Sorry for the automated translation)

Wal Buchenberg, Hannover

Wal I agree with your last para and that is why a world rate of profit has become more realistic to discern than say 50 years ago

Is there an organic, theoretical and historical relationship between the law of the tendency of the rate of profit to fall to the appearance of the proletariat as a revolutionary force? When you look back to different historical moments, you can see the proletariat fighting against the conditions imposed by democracy, for example from 1869 to 1893 the world economy entered a depression period, and we saw the constitution of the proletariat as a revolutionary class (the First International) and the Paris Commune of 1871. Then the “recovery” was below 35% so imperialist war broke up in 1914 so did the revolutionary tentative of the proletariat in 1917 and its constitution as a Party: The Third International. In 2008 another accumulation crisis broke up ant the proletariat from Greece called the rest of the class to regroup as a revolutionary force….and here we are….

John I think there is. See my book The Long Depression

Some problems nagging me for a long time:

The amount of value assigned to labor is hard to determine as a (large) part of the necessary labor time for reproduction of the workforce falls outside the labor spent in capitalist service, is spent in service of the state.

In itself it is a question which part of the state is to be assigned to the reproduction of labor. It follows the other part is part of surplus value or are costs of production. For instance: how are costs of infrastructure assigned? What about state owned productive activities? Are they properly represented in statistics?

A similar problem is associated with problem(2) Buchenberg above signals. How is the part of surplus value management appropriates calculated?

I think the authors should exclude China from the calculation, because it is not a capitalist country.

You could do a with-China and a sans-China scenario. That way we can see better the trends of world capitalism.

I don’t know if Vietnam is included in the G20. If that’s the case, it should also be excluded, since it also is a socialist country.

Of course, the same logic would apply to Cuba and North Korea, but those two countries are not usually included anyway, so I’m not mentioning them.

Yes, it is worth doing that. Vietnam is not in the g20

@vk: It is debatable if China is a capitalist country. At least, capitalist companies operate in China, and operate to make profi, and this includes state owned companies. Private companies, Joint-ventures of Chinese companies (mostly state owned) with capitalist companies from all over the world, and lately pure foreign direct investment (Elon Musk’s Tesla car company does not have a Chinese JV partner). There are stock exchanges in Shanghai and in Shenzen, and CGTN, the Chinese Global Television Network, reports the indexes of those stock exchanges. When you look at China via CGTN, one sees a capitalist country,

Then there is the fact that China does not have a real freedom of movement, or rather the right to abode, because of the Hukou system which makes a difference between City dweller and country boy.

John Quiggin posted recently https://crookedtimber.org/2020/07/26/the-end-of-interest/#comments

“Amid all the strange, alarming and exciting things that have happened lately, the fact that real long-term (30-year) interest rates have fallen below zero has been largely overlooked. Yet this is the end of capitalism, at least as it has traditionally been understood. Interest is the pure form of return to capital, excluding any return to monopoly power, corporate control, managerial skills or compensation for risk.

If there is no real return to capital, then then there is no capitalism. In case it isn’t obvious, I’ll make the point in subsequent posts that there is no reason to expect the system that replaces capitalism (I’ll call it plutocracy for the moment) to be an improvement….

To complete the picture of returns to capital, we need to look at stock markets and corporate profits. That’ll be the subject of another post…

It’s tempting to link all of this to the long-term historical decline in interest rates that led 19th century economists, most notably Marx, to talk about the declining rate of profit. But that decline came to an end in late C19. Real interest rates bounced about in the 20th century with no obvious trend. Much of the earlier decline may be have been due to a reduction in default risk as capitalism became established, but that’s just speculation on my part.”

Did Marx and others mean a declining in long-term real interest rates?

Also…What can Quiggin be talking about here? Crisis or collapse? Collapse as failure of expanded reproduction or simple reproduction or what? And, if long term interest rates accurately track pure return on capital, then why would stock markets and corporate profits be different?

John, negative interest rates work in a world that is losing population. They may foreshadow an impending population crash.

Quiggin is searching for a theory, method and answer that Marx has already provided

A question and comment..

The Question:Well this is very interesting. A kind of empirical evidence in support of Mar’x thesis on the falling rate of profit. But empirical evidence aside, why must the organic composition of capital necessarily grow faster than rate of exploitation?.

The comment:

Marx’s thesis of the fall of rate of profit is proposed after he he has already elaborated the average rate of profit. The fall of the rate of profit is the fall of the average rate of profit. As the free movement of capital and to a lesser extent labor(Marx, Capital Vol. 3, chapter 1) is a precondition for the formation of the average profit Marx’s law on the falling rate of profit must necessarily work in a national context.

I believe we cannot speak of the formation of a global average rate profit, especially today. Neither capital nor labor can move freely. The prime obstacle to free movement is state. Marx average rate of profit was not just a mathematical ratio but a means of communism of capital. It funneled the surplus-values produced by different individual capitals the constitute the total national-social capital into one basket and then redistribute the total national surplus-value among the individual capitals with an equal rate according the size of each capital. I do believe that such mechanism does not work on a global scale. While we can legitimately speak of national total social capital, a global total social capital and consequently a global rate of profit can be calculated but do not make sense dialecticaliy.

Another issue is that the rate of profit in imperialist countries such as US cannot be only measured on the basis of operation of capital within their borders. This rate is certainly influenced by the surplus value that the US in the form of knowledge rent, technological rent and monopoly profits extracts from other countries. Doesn’t this imply that in spite of growth of the organic composition of capital in these countries they rate of profit may not fall?

On your first point, I argue that a world rate of profit is becoming more realistic. On the second point, as you say, the US rate of profit is national and may included surplus value from imperialism, but using many national rates helps to capture all surplus value globally

i meant chapter 10.

For the world as a whole: One can use the incremental capital output ratio as a proxy for the world organic composition of capital or, the reciprocal value of it, as a proxy for the rate of profit. https://en.wikipedia.org/wiki/Incremental_capital-output_ratio

Excellent update and refinement of the ROP timeseries. Have been waiting for this.

Question: Are these rates pre or post-taxation?

I suspect, in the Marxian approach, they ought to be pre-tax. If so, it would be interesting to juxtapose these lines with average real corporate tax rates and even calculate a post-tax version of the charts to see to what extent the TRPF has been driving the trend of lowering tax rates in the USA and Europe.

These rates are ‘whole economy’ and include unproductive sectors and are pre-tax. I shall deal with the issue of productive and unproductive sectors and taxation in future posts. But see my book, The Long Depression, appendix on measuring the rate of profit.

I understand you are writing a book about Engels. Did you read the biographie by Michael Krätke? Rob

Rob – yes I have read it. It’s good.

I am going to prepare a short piece on why economy wide rates of profit provide false estimates because of the changed structure of the economy since 1980. I hope to post it by the weekend on the planningmotive.com

Thanks for the reply and two questions.

First in elaborating the average rate of profit Marx validly assumed that there was an equal national rate of interest, and an equal rate of exploitation with regard to all individual capitals of a national economy.

Can we speak of an equal international rate of interest or exploitation for all countries?

If not, what are the implications .for the formation of an international rate of profit?

Second, Marx validly abstracted from state in dealing with competition between individual capitals within total social national capital.

Can we abstract from the state in theorizing the competition between national capitals?I believe no. It was for this reason that Marx in his initial plan would analyse the state prior to international trade. This means that for him the state belonged to a higher level of abstraction than the international trade. Tariffs play a major role in international trade. The fact the states play a major role in fixing the rate of interests also play a role in the the international movements of capital. Central banks even when nominally independent of governments are part of the national sates. For Marx categories of higher level of abstractions are determinations of those of lower lever abstraction. For example value is a determination of price, surplus-value of profit, and money of capital. With the same token state is a determination of international trade without which a global market is impossible. A global market is a condition for the formation a global rate of profit, Now, we have no global state. States always have antagonistic interests, though more powerful states dominate weaker ones. Therefore, although we have a global market this market is radically different from a national market which crucible of the formation of an average rate of profit which really regulates the distribution of capital and labor between different branches. Global market is ultimately fractured along the state borders. I propose these ideas provocatively. Otherwise I consider them as open questions.

How do you consider the role of national state in your theory on the formation of an international rate of profit>?

Professor Michael Roberts has made a compilation of very interesting comparisons. I remain pending the fulfillment of your promises to expand the results of the long-term profit rate, in new deliveries for which we read your interesting work. Thank you