There are two new mainstream papers out that offer some interesting analysis on the reasons behind the Long Depression that the major economies (or at least, the US) have suffered since the end of the Great Recession in 2009 – in the growth of real GDP, productivity, investment and employment.

First, there is a paper by economists at the San Francisco Federal Reserve. The Disappointing Recovery in U.S. Output after 2009 by John Fernald, Robert E. Hall, James H. Stock, and Mark W. Watson. They consider the well-known evidence that US real GDP growth has expanded only slowly since the recession trough in 2009, counter to normal expectations of a rapid cyclical recovery. In the paper, they remove the “cyclical effects” of the Great Recession and find that there was already a sharply slowing trend in underlying growth before the global financial crash in 2008. The Fed economists conclude that the slowing trend reflected two factors: slow growth of innovation and declining labour force participation.

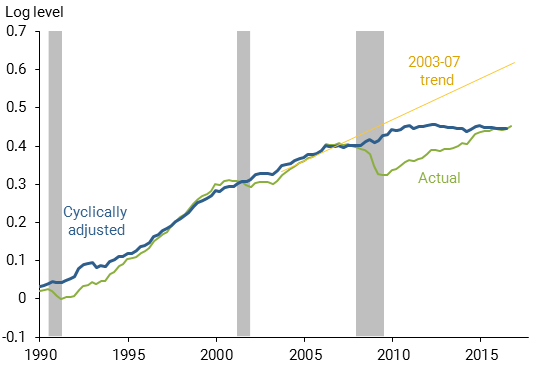

Figure 1 shows business-sector output per person in recent decades. The green line shows that output per person fell sharply during the recession and remains below any reasonable linear trend line extending its pre-recession trajectory. The figure shows one such trend line (yellow line), based on a simple linear extrapolation from 2003 to 2007.

Figure 1

Output per capita: Deep recession plus a sharp slowing trend

The blue line in Figure 1 shows the resulting estimate of trend output per capita after removing the cyclical effects associated with the deep recession. As expected, the cyclical adjustment removes the sharp drop in actual output associated with the recession. But since then, the trajectory of the blue line is nowhere close to a straight line projection from the 2007 peak. Rather, cyclically adjusted output per person rose slowly after 2007 and then plateaued in recent years.

The Fed economists reckon that the slow growth has been due to a slowdown in the productivity of labour, which in turn has been caused by a reduction in investment in innovation and new technology. In mainstream economics, this is measured by the residual of output per person left over after increases in employment (labor input) and means of production (capital input) are accounted for. The residual is called total factor productivity (TFP), to designate the increased productivity per unit of total input. TFP supposedly captures the productivity benefits from formal and informal research and development, improvements in management practices, reallocation of production toward high productivity firms, and other efficiency gains.

The Fed economists, using this factor accounting, find that TFP growth slowed significantly even before the Great Recession. It picked up in the mid-1990s and slowed in the mid-2000s—before the recession—and then was flat or even falling going into the recession.

Figure 2

Pre-recession slowdown in quarterly TFP growth

The economists dismiss the arguments that it was the Great Recession that caused the productivity slowdown or that productivity growth from info tech is being mismeasured: “such mismeasurement has long been present and there’s no evidence it has worsened over time.” They also dismiss the idea common from right-wing neoclassical economists that “increased regulatory burdens have reduced the economy’s dynamism.” They find no link between regulation changes and TFP growth.

The explanation they fall back on is the one presented by Robert J Gordon in many papers and books: that TFP growth is really just back to normal and what was abnormal was the burst in innovation in the 1990s with the hi-tech and dot.com boom. That ended in 2000 and won’t be repeated. “Every story in the late 1990s and early 2000s emphasized the transformative role of IT, often suggesting a sequence of one-off gains—reorganizing retailing, say. Plausibly, businesses plucked the low-hanging fruit; afterward, the exceptional growth rate came to an end.”

The other factor in the slowdown was the decline in employment growth of those of working age. Yes, there is supposed to be near ‘full employment’ now in the US and the UK etc. But participation in employment by working age adults has fallen sharply. That’s because populations are getting older and the ‘baby boomers’ who started worked in the 1960s and 1970s are now retiring and not being replaced.

Figure 3

Sharp declines in labor force participation rate

What the Fed economists want to tell us is that the Long Depression is not just the leftover of the Great Recession but reflects some deep-seated underlying slowdown in the dynamism of the US economy that is not going to correct through the current small economic upturn. The US economy is just growing more slowly over the long term.

What the Fed economists don’t explain is why the US economy has been slowing in productivity growth and innovation since 2000. What is missing from the analysis is what drives the adoption of new techniques and labour-saving equipment. Gordon and others just accept the current slowdown as a ‘return to normal’ from the exceptional 1990s.

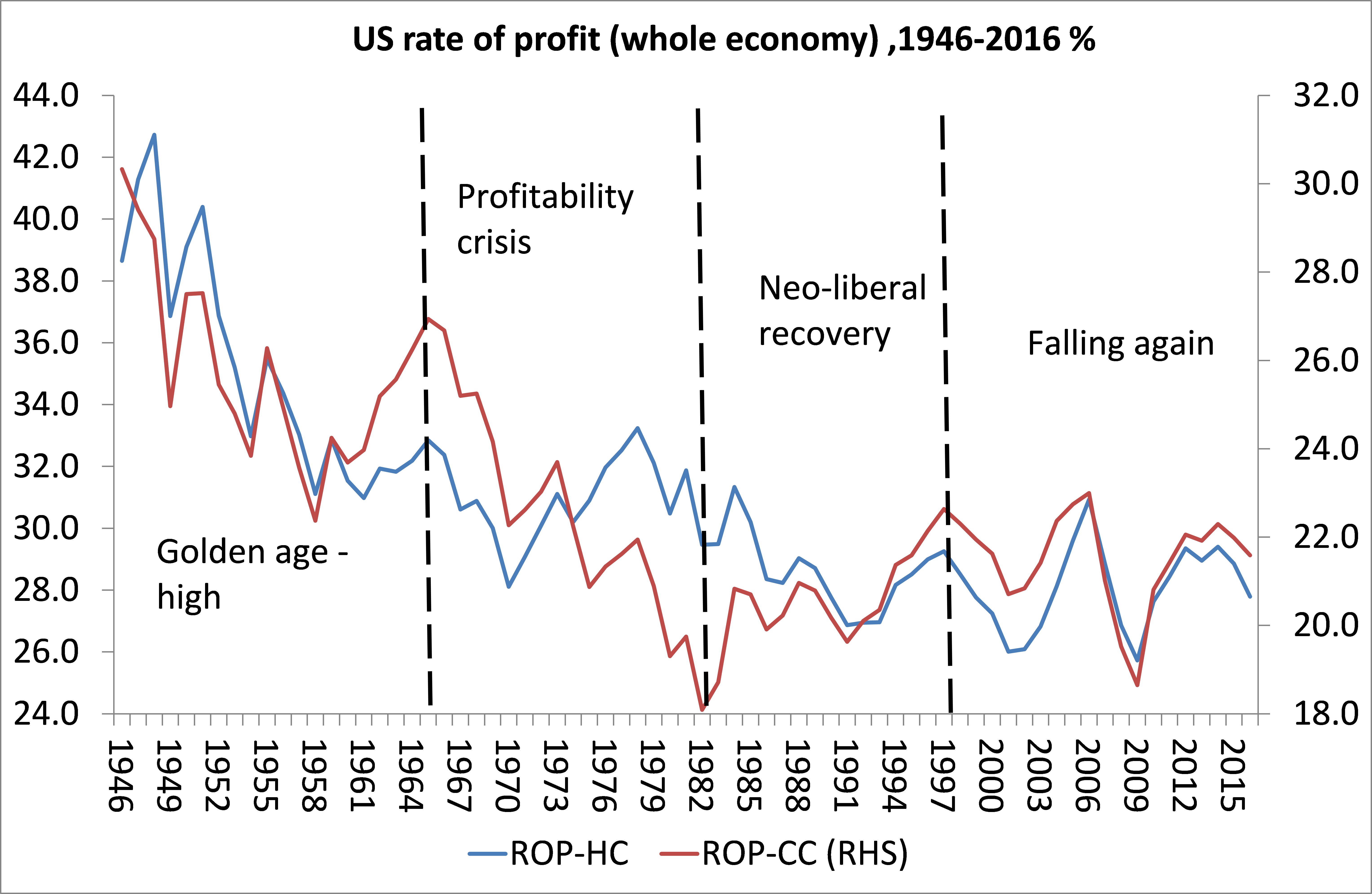

What is missing is the driver of investment under capitalism: profitability. Marxian studies that concentrate on this aspect reveal that the profitability of US capital stock and new investment peaked around 1997 and then turned down. It was this fall in profitability that eventually provoked the collapse in the dot.com bubble in 2000. The subsequent recovery in profitability did not achieve anything better that 1997 and indeed profits growth was mainly confined to the financial sector and increasingly to a small sector of top companies. Average profitability remained flat or even down and the growth in profit was mainly fictitious (‘capital gains’ from real estate, bond and stock markets) and fuelled by easy credit and low interest rates. That house of cards collapsed in the Great Recession.

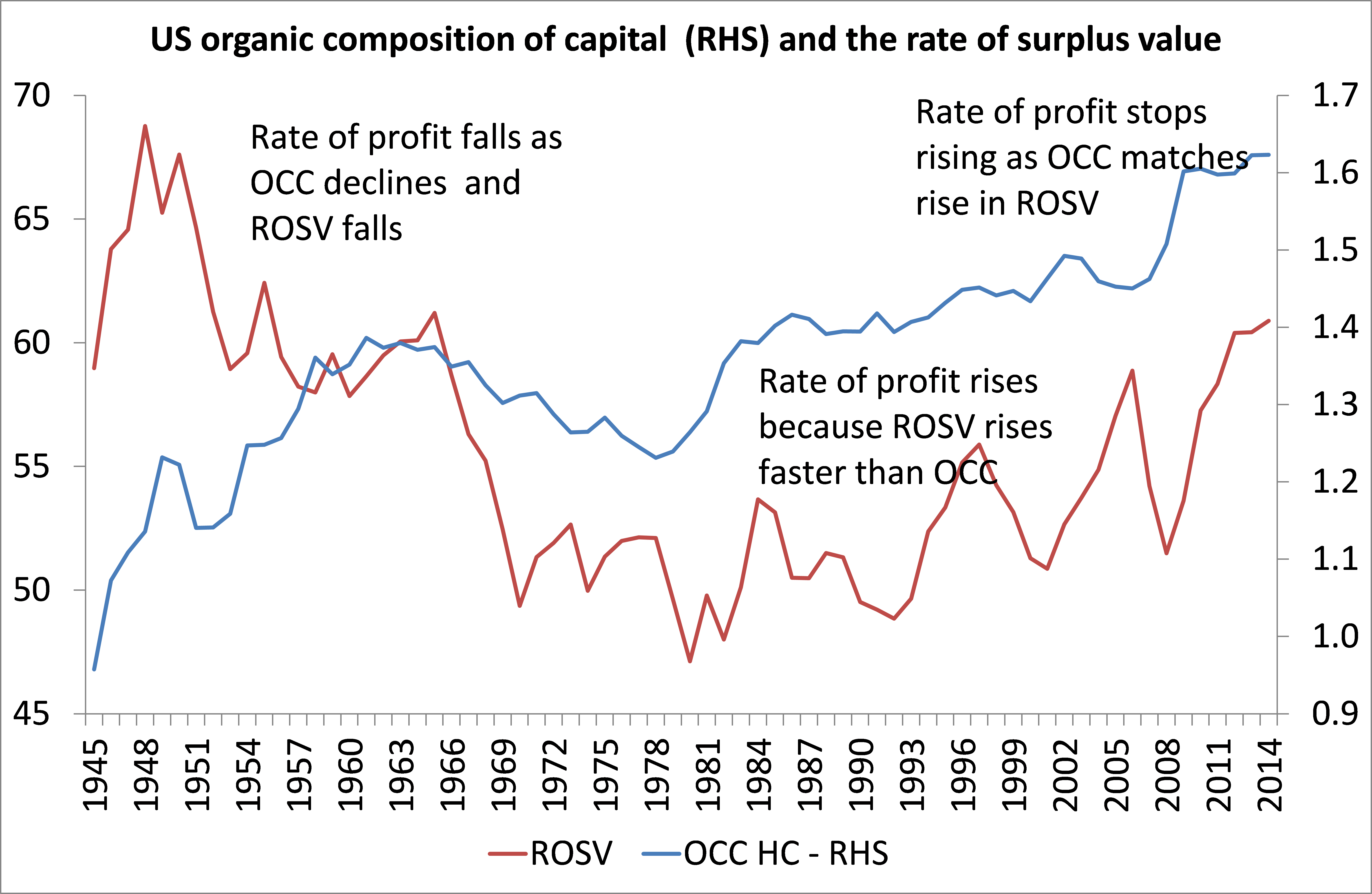

Profitability peaked in the late 1990s in the US (and elsewhere for that matter) because the counteracting factors to Marx’s law of the tendency of the rate of profit to fall (a rising rate of exploitation in the neoliberal period) and increased employment to boost total new value were no longer sufficient to overcome a rising organic composition of capital from the tech boom of the 1990s.

In contrast to this scenario, the Keynesians/post Keynesians have been pushing a different explanation for the fallback in productive investment since 2000 – it’s the growth of ‘monopoly power’. There have been several studies arguing this in recent years. Now a brand new paper by Keynesian economists at Brown University seeks to do the same. Gauti Eggertsson, Ella Getz Wold etc claim that the puzzle of the huge rise in profits for the top US companies alongside slowing investment in productive sectors can be explained by an increase in monopoly power and falling interest rates.

The Brown University economists argue that an increase in firms’ market power leads to an increase in monopoly rents; economic parlance for profits in excess of competitive market conditions-and thus an increase in the market value of stocks (which hold the rights to these rents). This leads to an increase in financial wealth and to what’s known as Tobin’s Q, the ratio of a firm’s financial value (market capitalization) to the value of its assets (book value).

With an increase in market power, the share of income consisting of pure rents increases, while the labour and capital shares both decrease. Finally, the greater monopoly power of firms leads them to restrict output. In restricting their output, firms decrease their investment in productive capital, even in spite of low interest rates.

Now I have dealt previously in detail with this argument that it is increased monopoly power that explains the gap between profits and investment in the US since 2000 or so. It is really a modification of neoclassical theory. Neoclassical theory argues that if there is perfect competition and free movement of capital, then there will be no profit at all; just interest on capital advanced and wages on labour’s productivity. Profit can only be ‘rent’ caused by imperfections in markets. The Brown professors, in effect, accept this theory. They just consider that, currently, ‘monopoly power’ is distorting it. This implies that if there was competition or monopolies were regulated’ all would be well. That solution ignores the Marxist view that profits are not just ‘rents’ or ‘interest’ but surplus value from the exploitation of labour.

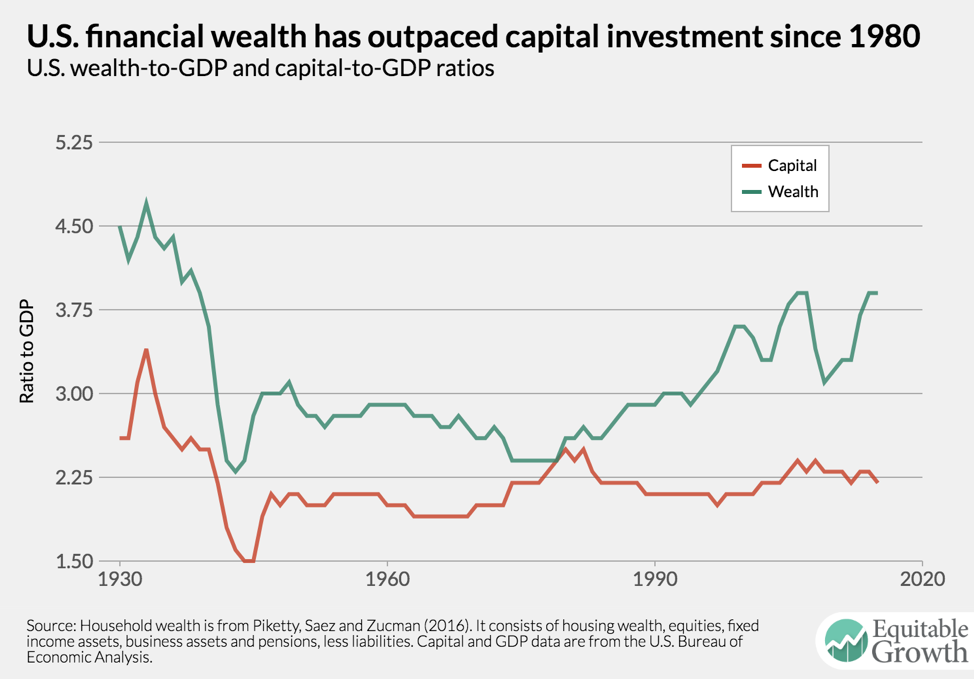

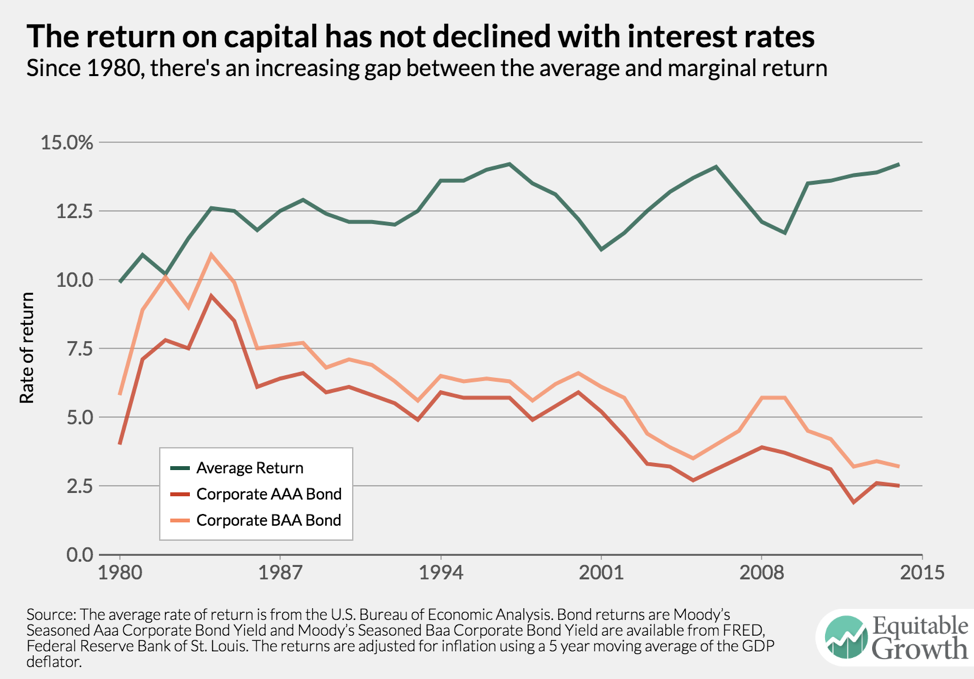

The Brown University professors reckon that average profitability was constant from 1980 onwards, so increased profits must have come from the gap between profitability and the fall in the cost of borrowing (interest rates). But actually, you can see from their graph that average profitability rose from about 10% in 1980 to a peak in the late 1990s of 14% – that’s a 40% rise and is entirely compatible with estimates by me and other Marxist economists. Average profitability was then flat from 200 or so.

Indeed, average profitability fell in the non-financial productive sectors of the economy, which is probably the reason for the gap that developed between overall profitability including financial profits (which rocketed between 2002 and 2007) and net investment in productive sectors. The jump in corporate profits (yes, mainly concentrated in the banks and big tech companies) was increasingly fictitious, based on rising stock and bond market prices and low interest rates. The rise of fictitious capital and profits seems to be the key factor after the end of dot.com boom and bust in 2000.

As I showed in a previous post, these mainstream analyses use Tobin’s Q as the measure of accumulated profit to compare against investment. But Tobin’s Q is the market value of a firm’s assets (typically measured by its equity price) divided by its accounting value or replacement costs. This is really a measure of fictitious profits. Given the credit-fuelled financial explosion of the 2000s, it is no wonder that net investment in productive assets looks lower when compared with Tobin Q profits. This is not the right comparison. Where the financial credit and stock market boom was much less, as in the Eurozone, profits and investment movements match.

It may well be right that, in the neo-liberal era, monopoly power of the new technology megalith companies drove up profit margins or markups. The neo-liberal era saw a driving down of labour’s share through the ending of trade union power, deregulation and privatisation. Also, labour’s share was held down by increased automation (and manufacturing employment plummeted) and by globalisation as industry and jobs shifted to so-called emerging economies with cheap labour. And the rise of new technology companies that could dominate their markets and drive out competitors, increasing concentration of capital, is undoubtedly another factor.

But the recent fall back in profit share and the modest rise in labour share since 2014 also suggests that it is a fall in the overall profitability of US capital that is driving things rather than any change in monopoly ‘market power’. Undoubtedly, much of the mega profits of the likes of Apple, Microsoft, Netflix, Amazon, Facebook are due to their control over patents, financial strength (cheap credit) and buying up potential competitors. But the mainstream explanations go too far. Technological innovations also explain the success of these big companies.

Moreover, by its very nature, capitalism, based on ‘many capitals’ in competition, cannot tolerate indefinitely any ‘eternal’ monopoly; a ‘permanent’ surplus profit deducted from the sum total of profits which is divided among the capitalist class as a whole. The battle to increase profit and the share of the market means monopolies are continually under threat from new rivals, new technologies and international competitors.

The history of capitalism is one where the concentration and centralisation of capital increases, but competition continues to bring about the movement of surplus value between capitals (within a national economy and globally). The substitution of new products for old ones will in the long run reduce or eliminate monopoly advantage. The monopolistic world of GE and the motor manufacturers in post-war US did not last once new technology bred new sectors for capital accumulation. The world of Apple will not last forever.

‘Market power’ may have delivered ‘rental’ profits to some very large companies in the US over the last decade (and just that short period it seems), but Marx’s law of profitability still holds as the best explanation of the accumulation process. Rents to the few are a deduction from the profits of the many. Monopolies redistribute profit to themselves in the form of ‘rent’, but do not create profit.

Profits are not the result of the degree of monopoly or rent seeking, as neo-classical and Keynesian/Kalecki theories argue, but the result of the exploitation of labour. The key to understanding the movement in productive investment remains in its underlying profitability, not the extraction of rents by a few market leaders.

The Long Depression is a product of low investment and low productivity growth, which in turn is a product of lower profitability of investment in productive sectors and a switch to unproductive financial speculation (and yes, partly a product of oligopolistic power boosting the big at the expense of the small).

In 2008 the oilprice was 145 dollars. In the periode 2011-2014 the oilprice was 110 dollars (and 90-100 dollars in the USA). This is much to high for the real economy. A oilprice of 145 dollars indicates a shortage of oil. In the periode 2011-2014 we saw some kind of oil-recovery (huge investments in oil production) ending with introduction of fracking in the US, resulting in low oil price in 2015 which stimulated economical growth and recovery in the US.

“The Long Depression is a product of low investment and low productivity growth, which in turn is a product of lower profitability of investment in productive sectors and a switch to unproductive financial speculation (and yes, partly a product of oligopolistic power boosting the big at the expense of the small).”

An enormous quantity of statistics, all of which are totally illusory because expressed in economically irrational (because the “values” expressed by them are totally incommensurable with the real meanings of those values as scientifically determined in Marxian economics whose metric is “socially necessary labor time” with the concept of social necessity at the root because it is at the root of human existence itself) currency terms and fictitious “real” values derived from them, none of which could conceivably get anywhere close to the real point. The real “cause” (underlying concatenation of circumstances) of the so-called great depression is that global production and productivity “growth” have become NEGATIVE and declining at an increasing rate ever since the ecological crisis stemming from the energy consumption needed for capitalist economic growth became so toxic that the planetary environmental crisis actually became publicly mentionable.

Michael said: “The Long Depression is a product of low investment and low productivity growth, which in turn is a product of lower profitability of investment in productive sectors and a switch to unproductive financial speculation…”

That seems to me comprehensibly. But it seems also to me, this statement is true especially or only in the capitalist center of world economy. The situation in the capitalist periphery is quite different – especially in Asia.

However the great capital operates simultaneously in both spheres. That makes a lot of data difus. For example great japanese companies make little or no profit in Japan, but a lot of profit outside of Japan. The annuals blur such differences.

I think, when we make statements about world economy, we should make clear differences between the (shifting) core of economy and the (also shifting) periphery.

look at this: Regional percentages of the world economy in market prices (1980 – 2020)

http://marx-forum.de/Forum/gallery/index.php?image/920-weltwirtschaft-2020-anteil-der-kernzone-und-der-peripherie/

„This implies that if there was competition or monopolies were regulated’ all exploitedwould be well. That solution ignores the Marxist view that profits are not just ‘rents’ or ‘interest’ but surplus value from the exploitation of labour.“

But labour can only get exploited by being seperated from the means of production. Capitalist relations of production presuppose means of production concentrated in few hands. In that sense capitalism is always monopolistic and profits are always based on the power of property ownership – just like rents.

Gains from wealth/finance have exceeded gains from income/industry over the past 9 years. A capitalist seeks to accumulate capital. If one wants to accumulate more capital, making the value of financial assets grow is easier than selling in the real economy. Since 2009 the net worth of U.S. households has increased at $5.3 trillion a year (total Hh net worth has doubled in value from $48 to $96 trillion — Flow of Funds, FRB, page 2). These assets are two thirds financial paper assets, one third real estate. Gains from corporate income have increased at $1.05 to $1.4 trillion a year since 2010, maybe at a quarter the rate of wealth return. Ninety-four percent of corporate profits have gone into two places, stock buybacks and dividends (see Wm. Lazonick articles at INET.org) That the productivity or profitability of the “real” economy should lag is of no concern to a “capitalist”, his or her real concern is the growth of financial assets (stocks and bonds). His main objective is to feed the growth of this secondary currency — stock values as a secondary currency — and accumulate capital. “Real average weekly income of production and nonsupervisory workers” (80% of the workers, see FRED) is about 4% lower than it was in 1964, 54 years ago, while the “disposable personal income per capita” has increased by 190% (BEA.gov, Personal Income Table 2.1) Total “outstanding debt” of “domestic financial sector” has increased from 21% in 1962 to 116% in 2007. Finance, the tail, is wagging the dog, the productive economy.

Michael, The Nation has just posted a perfect example of the “market power” ideology at work on the left. You may want to take a look here: https://www.thenation.com/article/special-investigation-the-dirty-secret-behind-warren-buffetts-billions/

I don’t yet have a good enough understanding of the conceptual frameworks being used, the meanings attached to the specific aggregates being graphed and discussed, the validity of the statistics for those aggregates or indeed WTF this is all about.

When I look at figure 1 for “Output per capita” I am supposed to see a “cyclically adjusted” slow rise in “TPF” continuing even after the “recession” but flattening more recently. What I actually see is a sharp drop at the time of the GFC followed by a continuation of the previous trend. Whatever “TPF” is supposed to mean, it does not strike me as at all odd that some measure related to productivity might suddenly plummet when the economy as a whole suddenly plummets and might then resume its previous trajectory. Why would one need to either “explain” or “cyclically adjust” this? How could doing so turn an expected symptom of a sudden slowdown in turnover into an explanation?

Turning to US Rate of Profit (immediately following figure 3), I don’t know what the blue and red lines for ROP-HC and ROP-CC represent. But they both seem similar and I assume they are supposed to correspond to some sort of US Rate of Profit.

What I actually see is a decline from 1946 to 1982 (with an anomalous uptick for several years around 1965) followed by a very jerky flattening out from 1982 to now.

What the labels say I am supposed to see is a “Golden age high” till 1964, then a “Profitability Crisis” till 1982, then a “Neo-liberal recovery” then “Falling again” from 1997. I am pretty sure I have heard all those terms before. But they seem to have been stuck onto the graph rather than emerging from it.

Anyway I am trying to pick up a bit by osmosis, following the links. It is very time consuming and I cannot keep up.

This does very strongly reinforce my impression/prejudice that trying to come up with explanations by staring at and talking about this sort of data is paralysing. It is simply the wrong method as explained in the Introduction and Chapter 1 of Maksakovsky on “The Capitalist Cycle”.

Good comparison would be trying to explain perturbations in the orbit of Uranus without an underlying theory that improves on previous views of epicycles within epicycles. We need ellipses, not circles. They need to be around the Sun, not the earth and we need a law of gravity that could be used to calculate the location of some previously unknown planet – as actually happened historically with Neptune.

Closest I have come to understanding this post and related links, is that it relies on “supply side” concepts, which could be compared with heliocentralism. This is explicitly stated in the first link to paper by Stock and Watson.

Something has caused slow GDP growth, investment and “total factor productivity” (whatever that means). We can only look on supply side so “underlying reasons” are slow growth of innovation and declining labor force participation.

We can then go around in circles and get low profits leading to low investment.

But why is attention confined to the supply side?

If there are cyclical disproportions between the two main departments, with relative prices moving above and below values as Marx described, one would expect to find overproduction causing both lower profits slower turnover, resulting in lower investments and lower productivity, and increased unemployment and/or declining labor market participation.

That is simply based on an oversimplification of one phase of a VERY abstract “toy” model of “pure” capitalism as outlined in Chapter 2 of Maksakovsky. Not elaborated to one capable of analysing real data. But surely it is necessary to develop a theory that CAN be elaborated to study concrete data, rather than simply assuming that the causes MUST lie on the supply side and then staring at lots and lots of data and massaging and labelling it according to preconceived notions?

It’s interesting that Marx, in order to critique political economy, decided to begin by abstracting out of his analysis the social organism within which the capitalist mode of production evolved (and which it changes). Maksakovski went even further than Marx, abstracting what he considered non-essential elements (agriculture, finance) from his analysis in order to get at the essential cause(s) of crises under capitalism. Analysis of such complex processes requires such abstraction, but as Marx makes clear, also requires synthesis and reconstruction.

Marx reminds us from the beginning that the mode capitalist production can only be understood in relation to the social order within which it is embedded, one based on the alienation of labor from the means of production (and is seen in the contradictory nature of capitalism’s commodity itself). The labor theory of value can identify the cause(s) of crises as originating within the production process, but the fundamental contradiction underlying crises of overproduction (and underconsumption) is the contradiction between the capitalist accumulation process, and the production and reproduction of the alienated class of laborers–employed and necessarily unemployed–with which it is essentially at war. This war has been global from the beginning, something Marx and Engles recognized as early as the “Manifesto”.

Marx planned to address this fundamental contradiction between capitalism’s mode of production and the reproduction of its own social order, but never completed his project. Maybe Maksakovski, who died young, intended to bridge the gap also. But all human beings, marxists especially, should encourage (rather than reject) the work of those who have taken up this task: feminist social reproduction theorists and those (hardly Keynesians) engaged in applying a labor theory of value and exploitation in solidarity with the actual workers of the world–employed and unemployed, men, women, children, the aged and disabled–rather than abstracting ourselves from all that fundamental, but nonessential, stuff.

Not sure what you are getting at here. Topic is “Underlying reasons for long depression”. Cannot see any relevance of “feminist social reproduction theorists” to that. Maksakovsky’s relevance is in explanation of underlying reasons for the existence of a “business cycle” which has to be the basis for any understanding of particular aspects of business cycles, such as crises and depressions, whether long or short – integrated with understanding of whole cycle including phases of recovery prosperity and boom.

Marx deeply studied to concrete phenomena to isolate fundamental such as value that need to be understood in order to synthesize and construct those concrete phenomena as something comprehended rather than a passing swirl of events (eg the endless graphs in macroeconomic blogging). To prepare for this he developed an extremely abstract “toy model” in the “reproduction schemes” in volume 2 of Capital with just 6 variables – c + v + s in two departments. This not only abstracts from agriculture and from pre-capitalist social phenomena as well as finance (whiile retaining gold based money) but also abstracts from the formation of value but by rises and falls in actual prices above and below values.

Maksakovsky starts from this to the level of extreme abstraction and followed Marx’s method of synthesis and reconstruction by developing the logic inherent in the categories Marx had isolated. He began by introducing the fluctuation of prices above and below values, connecting this with lags induced by waves of fixed capital investment that are themselves induced by previous phases of the cycle thus producing a cyclical phenomena that was implicit in but not expressed by the reproduction schemes at the level of abstraction Marx left them.

In addition Maksakovsky introduced finance (chapter 3) based on Marx’s material in volume 3 of Capital to explain both the amplification of the cycle and the fact that the transition from boom to depression did not take place as a smooth change of direction but a sudden sharp crisis with bankruptcies etc. This also explained why most observers misunderstood the crisis phenomena as primarily financial rather than an expression of the underlying business cycle – this was the most dramatic bit, clearly visible on all their graphs.

In order to achieve this, Maksakovsky did indeed continue to abstract those elements that were not essential to get that far, just as Marx did. But he moved a step towards a more concrete synthesis, not as you seem to be saying a step in “even further” abstraction. This is utterly clear if you read Maksakovsky.

This leaves an awful lot of work to do before we could have a good model of current events. In particular the financial system now is very different from the one Marx and Maksakovsky were describing and the role of the state must be introduced. But it does get to the point of exhibiting a systematic “business cycle” whereas Marx only left the unsystemetized scattered elements needed for that from which alleged “Marxists” have produced every conceivable permutation of speculative “theories” instead of actual systematic development.

”whereas Marx only left the unsystemetized scattered elements needed for that from which alleged “Marxists” have produced every conceivable permutation of speculative “theories” instead of actual systematic development.”

If you know that Marxists have produced only speculative theories instead of actual systematic development, then you must yourself have knowledge of the nature of this systematic development. Why then do you keep such mysteries to yourself instead of systematically explicating them, so that all those ‘alleged’ Marxists might correct the errors of their merely ‘speculative’ endeavours?

”Marx deeply studied to concrete phenomena to isolate fundamental such as value that need to be understood in order to synthesize and construct those concrete phenomena as something comprehended rather than a passing swirl of events”

In explicating such systematic development I wonder if you apply yourself to writing with greater clarity, as I for one find your English, as exemplified by the paragraph immediately quoted above, so incoherent as to border on the incomprehensible.

If English is not your native language, then please accept my apologies in advance.

Arthur, I am no economist and hardly an expert on marxism. Just a retired teacher, a life-long “leftist” student of history and historical materialism. I haven’t read Maksakosvsky, just about him, but am interested enough to read him.

Here’s what Im getting at.

In “Capital” Marx’s critique of Smith et al seems to remain within political economy’s limited terrain of commodity production within an illusory free market. We know, however (from Marx’s method of presentation and from earlier works), that Marx’s primary academic interest was not in economics as such, but in the role of human labor in the production and reproduction of evolving social orders. Political upheaval and communist convictions led him to critically study political economy, the discovery of surplus value, and a new labor theory of value that explained the nature of crises within the capitalist mode of production.

The concept of surplus value, which introduces the use value of labor and its products into political economy’s calculation subverts political economy by bringing in the problematic of the production and reproduction of the working class as a whole, not just those “productively” employed, and not just those employed at the colonial/imperial centers of the global social order. Can a system based on private ownership of the means of production reproduce even its socially necessary laboring classes without theft and mass destruction? The attitude of capitalists then and now was succinctly epitomized in Thatcher’s quip about the non-existence of “society”. These questions, it seems to me, are critical questions to be answered today. If not by marxist economists, then by whom?

I am a native speaker of English writing hurriedly and without spell checking for informal comments in a blog. Do intend to attempt to explicate Maksakovsky’s systematic development in a form more accessible and regret not having been able to focus on doing so. Am participating here partly as preparation for doing so. Also studying other background – eg strongly believe a modern exposition needs to be more mathematical. Understanding what people have difficulty with will be very helpful for that so I welcome any critiques and don’t care how they are expressed.

Was and am not sure what mandm was getting at as the language he used in his first paragraph indicated to me that he had read and understood important concepts expressed at greater length in the Introduction and Chapter 1 of Maksakovsky but later paragraphs suggested mandm had not got to chapter 2 at all since that makes it utterly clear that Maksakovsky was engaged precisely in the synthesis and reconstruction mandm wanted making the extremely abstract model in Marx’s reproduction schemes less abstract whereas mandm thought he was using “even more” abstraction.

The sentence you quoted from paragraph you find incoherent and bordering on incomprehensible was written in that context. It was not an attempt to further clarify what I assumed mandm already did get, but a preliminary to the next sentence emphasizing how extremely abstract were the “reproduction schemes” Maksakovsky started from.

Link to library genesis has free download of Maksakovsky and there is also a link for paperback order at my unopened blog, which will eventually have some “explicating” but is currently even more incoherent than anything I write here.

https://thecapitalistcycle.wordpress.com/

Library genesis is blocked at some locations. The URL suffix is a torrent hash which can be used with any torrent client to get past this:

http://gen.lib.rus.ec/book/index.php?md5=EAC7E58D683A34F76BC03CBC0934E753

The torrent hash part is EAC7E58D683A34F76BC03CBC0934E753 (if unfamiliar lookup “bit torrent” in wikipedia).

A blocked reader here in UK told me that this direct link works:

Click to access %28Historical%20Materialism%20Book%20Series%29%20Pavel%20Maksakovsky-The%20Capitalist%20Cycle_%20An%20Essay%20on%20the%20Marxist%20Theory%20of%20the%20Cycle-Haymarket%20Books%20%282009%29.pdf

Please confirm. (File is over 20MB).

Other recommended reading for Marx’s basic methodology of extracting abstract categories from the unsystematized swirling data of the raw concrete and “ascending from the abstract to the (comprehended) concrete” by synthesis and reconstruction is in section 3 on method in Marx’s “Introduction to the Grundrisse”:

https://www.marxists.org/archive/marx/works/1857/grundrisse/ch01.htm#loc3

(Rest of the introduction also well worthwhile and the whole book is available there as pdf or epub)

https://thenextrecession.wordpress.com/2018/02/14/the-underlying-reasons-for-the-long-depression/#comment-104171

still “awaiting moderation”

I just wrote a response to comment by jlowrie above which is “awaiting moderation” as has more than one link. Please check back to read it when it does appear. Meanwhile I will try just one link. Please let me know if download works for you (20MB file):

Click to access %28Historical%20Materialism%20Book%20Series%29%20Pavel%20Maksakovsky-The%20Capitalist%20Cycle_%20An%20Essay%20on%20the%20Marxist%20Theory%20of%20the%20Cycle-Haymarket%20Books%20%282009%29.pdf

I find the wider context you mention far better discussed in Marx’s “Grundrisse” manuscript than by “marxist economists” today. The translation by Martin Nicolas for Penguin is available in pdf and epub at link in above post. But you can easily just search for “Grundrisse” at marxists.org.

Much shorter fundamental outline of historical materialism is in Engels “Socialism – Utopian and Scientific”. This was close to prescribed reading in the Second International and vastly different from what one could get reading “about” historical materialism from “marxians”. Also try Engels on Feurbach.

”. Please let me know if download works for you (20MB file):”

Here is what you get:”Access to websites listed on this page are blocked pursuant to orders of the High Court” !?!

Most seem to have to do with the movies!

Thanks. Unfortunately that also means the other link I provided in comment still “awaiting moderation” is also blocked by UK censorship.

It is worth taking the trouble to find a way around this. I have created a page explaining details of how and why to do so. Please check it out and post here a link that does work for you in UK so others in this blog can also use it.

https://wordpress.com/post/thecapitalistcycle.wordpress.com/949

I should have given this link:

https://thecapitalistcycle.wordpress.com/2018/02/14/library-genesis-access/

Try this first in case you are lucky. It is the current IP address link listed in summary of the wikipedia page for Library Genesis:

http://93.174.95.27/