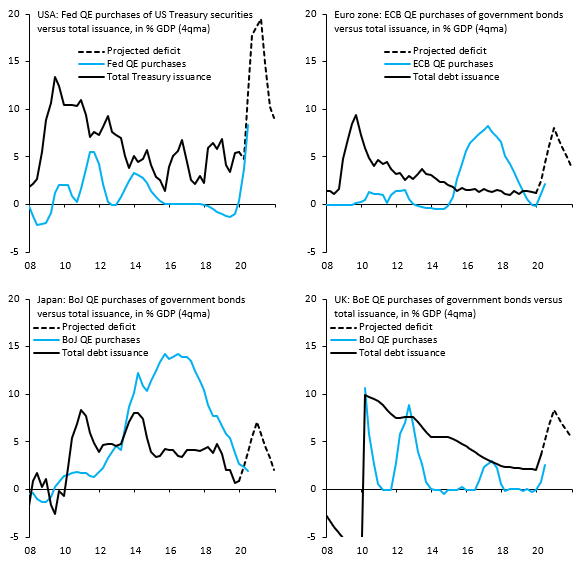

Optimism reigns in global stock markets, particularly in the US. After falling around 30% when the lockdowns to contain COVID-19 virus pandemic were imposed, the US stock market has jumped back 30% in April. Why? Well, for two reasons. The first is that the US Federal Reserve has intervened to inject humungous amounts of credit through buying up bonds and financial instruments of all sorts. The other central banks have also reacted similarly with credit injections, although nothing compares with the Fed’s monetary impulse.

As a result, the US stock market’s valuation against future corporate earnings has rocketed up in line with the Fed injections. If the Fed will buy any bond or financial instrument you hold, how can you go wrong?

The other reason for a stock market rally at the same time as data for the ‘real’ economy reveal a collapse in national output, investment and employment nearly everywhere (with worse to come) is the belief that the lockdowns will soon be over; treatments and vaccines are on their way to stop the virus; and so economies will leap back within three to six months and the pandemic will soon be forgotten.

For example, US Treasury Secretary Mnuchin, reiterated his view expressed at the beginning of the lockdowns that “you’re going to see the economy really bounce back in July, August and September”. And White House economics advisor, Hassett reckoned that by the 4th quarter, the US economy “is going to be really strong and next year is going to be a tremendous year”. Bank of America’s CEO, Moynihan reckoned that consumer spending had already bottomed out and would soon rise nicely again in the 4th quarter, followed by double digit GDP growth in 2021!

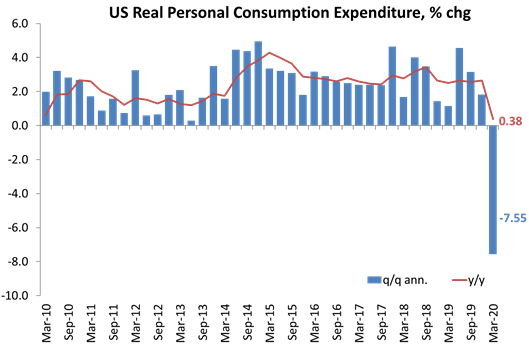

That US personal consumption had bottomed out seems difficult to justify when you look at the Q1 data. Indeed, in March, personal spending in the US dropped 7.5 percent month-over-month, the largest decline in personal spending on record.

But it’s not just the official and banking voices who reckon that the economic damage from the pandemic and lockdowns will be short if not so sweet. Many Keynesian economists in the US are making the same point. In previous posts, I pointed to the claim by Keynesian guru, Larry Summers, former Treasury Secretary under Clinton, that the lockdown slump was just the same as businesses in summer tourist places closing down for the winter. As soon as summer comes along, they all open up and are ready to go just as before. The pandemic is thus just a seasonal thing.

Now the Keynesian guru of them all, Paul Krugman, reckons that this slump, so far way worse on its impact on the global economy than the Great Recession, was not an economic crisis but “a disaster relief situation”. Krugman argues that this is “a natural disaster, like a war, is a temporary event”. So the answer is that “it should be met largely through higher taxes and lower spending in the future rather than right away, which is another way of saying that it should be paid for in large part by a temporary increase in the deficit.” Once this spending worked, the economy would return just as before and the spending deficit will only be ‘temporary’. And Robert Reich, the supposedly leftist former Labour Secretary, again under Clinton, reckoned that the crisis wasn’t economic but a health crisis and as soon as the health problem was contained (presumably this summer) the economy would ‘snap back’.

You would expect the Trump advisors and Wall Street chiefs to proclaim a quick return to normal (even though economists in investment houses mainly take a different view), but you may find it surprising that leading Keynesians agree. I think the reason is that any Keynesian analysis of recessions and slumps cannot deal with this pandemic. Keynesian theory starts with the view that slumps are the result a collapse in ‘effective demand’ that then leads to a fall in output and employment. But as I have explained in previous posts, this slump is not the result of a collapse in ‘demand’, but from a closure of production, both in manufacturing and particularly in services. It is a ‘supply shock’, not a ‘demand shock’. For that matter, the ‘financialisation’ theorists of the Minsky school are also at a loss, because this slump is not the result of a credit crunch or financial crash, although that may yet come.

So the Keynesians think that as soon as people get back to work and start spending, ‘effective demand’ (even ‘pent-up’ demand) will shoot up and the capitalist economy will return to normal. But if you approach the slump from the angle of supply or production, and in particular, the profitability of resuming output and employment, which is the Marxist approach, then both the cause of the slump and the likelihood of a slow and weak recovery become clear.

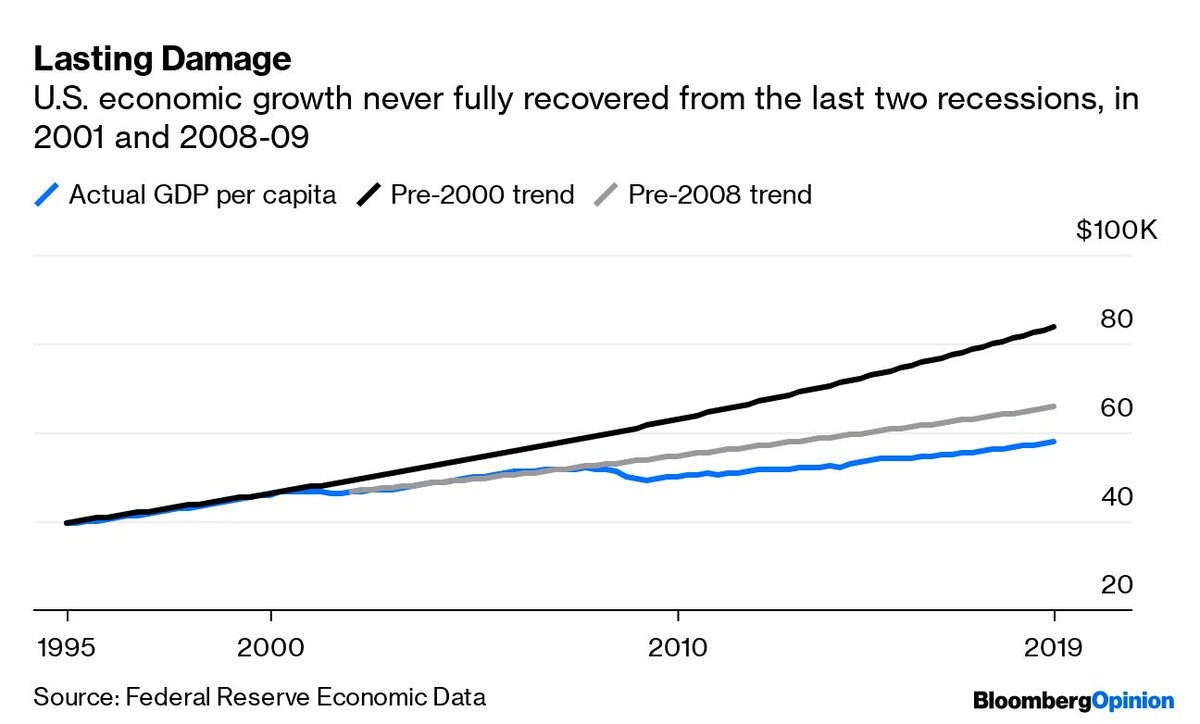

Let us remind ourselves of what happened after the end of the Great Recession of 2008-9. The stock market boomed year after year, but the ‘real’ economy of production, investment and workers’ incomes crawled along. Since 2009, US per capita GDP annual growth has averaged just 1.6%. So at the end of 2019, per capita GDP was 13% below trend growth prior to 2008. That gap was now equal to $10,200 per person—a permanent loss of income.

And now Goldman Sachs is forecasting a drop in per capita GDP that would wipe out even those gains of the last ten years!

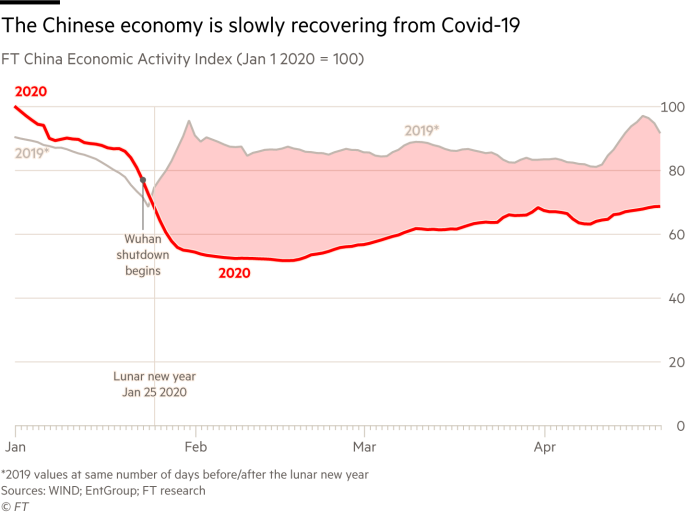

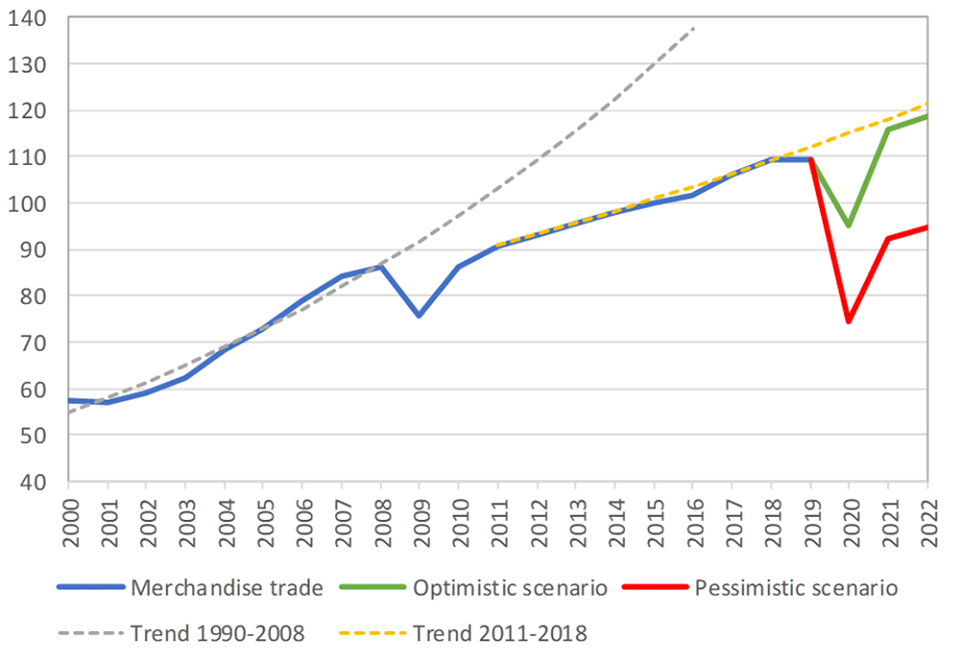

The world is now much more integrated than it was in 2008. The global value chain, as it is called, is now pervasive and large. Even if some countries are able to begin economic recovery, the disruption in world trade may seriously hamper the speed and strength of that pick-up. Take China, where the economic recovery from its lockdown is under way. Economic activity is still well below 2019 levels and the pace of recovery seems slow – mainly because Chinese manufacturers and exporters have nobody to sell to.

This is not a phenomenon of the virus or a health issue. Growth in world trade has been barely equal to growth in global GDP since 2009 (blue line), way below its rate prior to 2009 (dotted blue line). Now the World Trade Organisation sees no return to even that lower trajectory (yellow dotted line) for at least two years.

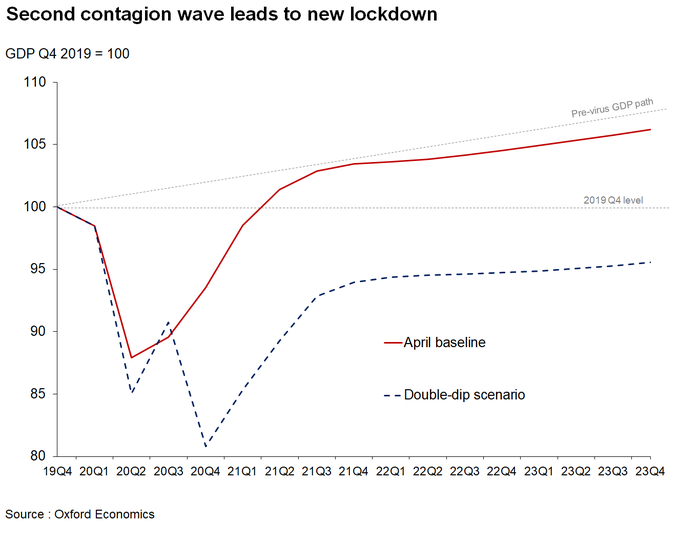

The massive public sector spending (over $3trn) by the US Congress and the huge Fed monetary stimulus ($4trn) won’t stop this deep slump or even get the US economy back to its previous (low) trend. Indeed, Oxford Economics reckons that there is every possibility of a second wave in the pandemic that could force new lockdown measures and keep the US economy in a slump and in stagnation through 2023!

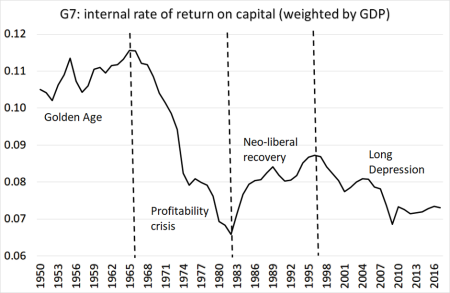

But why are capitalist economies (at least in the 21st century) not jumping back to previous trends? Well, I have argued on this blog in many posts that there were two key reasons. The first was that the profitability of capital in the major economies has not returned to levels reached in the late 1990s, let alone in the ‘golden age’ of economic growth and mild recessions of the 1950s and 1960s.

And the second reason is that in order to cope with this decline in profitability, companies increased their debt levels, fuelled by low interest rates, either to sustain production and/or to switch funds into financial assets and speculation.

But linked to these underlying factors is another: what has been called the scarring of the economy, or hysteresis. Hysteresis in the field of economics refers to an event in the economy that persists into the future, even after the factors that led to that event have been removed. Hysteresis is the argument that short-term effects can manifest themselves into long term problems which inhibit growth and make it difficult to ‘return to normal’.

Keynesians traditionally reckon that fiscal stimulus will turn slump economies around. However, even they have recognized that short-run economic conditions can have lasting impacts. Frozen credit markets and depressed consumer spending can stop the creation of otherwise vibrant small businesses. Larger companies may delay or reduce spending on R&D.

As Jack Rasmus put it well in a recent post on his blog: “It takes a long time for both business and consumers to restore their ‘confidence’ levels in the economy and change ultra-cautious investing and purchasing behavior to more optimistic spending-investing patterns. Unemployment levels hang high and over the economy for some time. Many small businesses never re-open and when they do with fewer employees and often at lower wages. Larger companies hoard their cash. Banks typically are very slow to lend with their own money. Other businesses are reluctant to invest and expand, and thus rehire, given the cautious consumer spending, business hoarding, and banks’ conservative lending behavior. The Fed, the central bank, can make a mass of free money and cheap loans available, but businesses and households may be reluctant to borrow, preferring to hoard their cash—and the loans as well.” In other words, an economic recession can lead to “scarring”—that is, long-lasting damage to the economy.

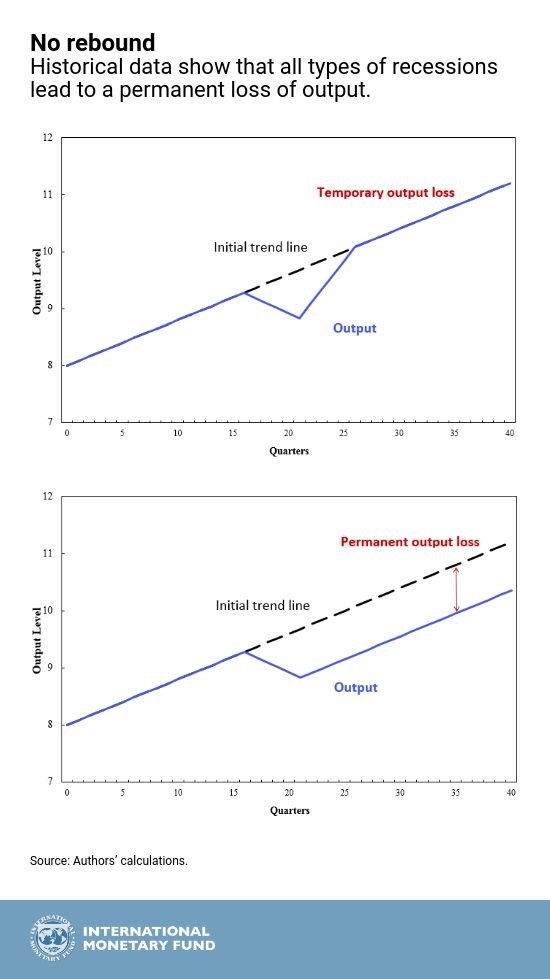

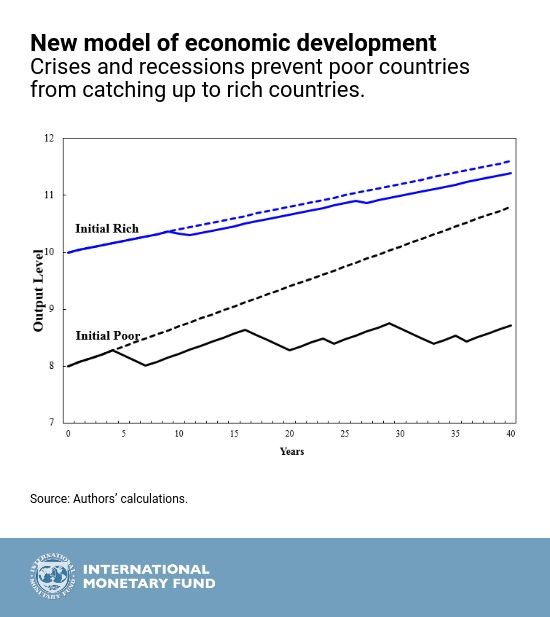

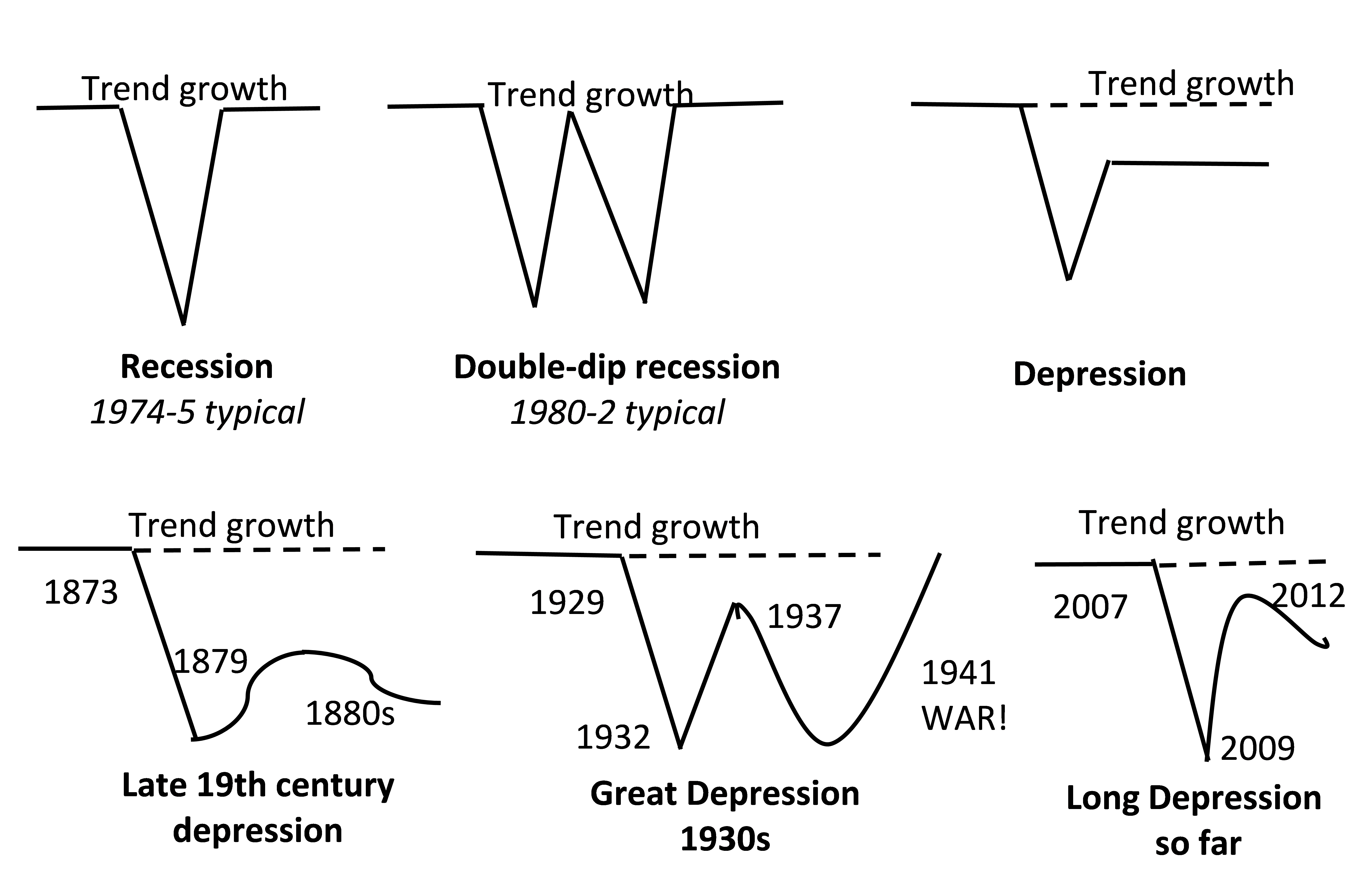

A couple of years ago, the IMF published a paper that looked at ‘scarring’. The IMF economists noted that after recessions there is not always a V-shaped recovery to previous trends. Indeed, it has been often the case that the previous growth trend is never re-established. Using updated data from 1974 to 2012, they found that irreparable damage to output is not limited to financial and political crises. All types of recessions, on average, lead to permanent output losses.

“In the traditional view of the business cycle, a recession consists of a temporary decline in output below its trend line, but a fast rebound of output back to its initial upward trend line during the recovery phase (see chart, top panel). In contrast, our evidence suggests that a recovery consists only of a return of growth to its long-term expansion rate—without a high-growth rebound back to the initial trend (see chart, bottom panel). In other words, recessions can cause permanent economic scarring.”

And that does not just apply to one economy, but also to the gap between rich and poor economies. The IMF: “Poor countries suffer deeper and more frequent recessions and crises, each time suffering permanent output losses and losing ground (solid lines in chart below).”

The IMF paper complements the view of the difference between ‘classic’ recessions and depressions that I outlined in my book of 2016, The Long Depression. There I show that in depressions, the recovery after a slump takes the form, not of a V-shape, but more of a square root, which sets an economy on new and lower trajectory.

I suspect that there will be plenty of scarring of the capitalist sector from this pandemic slump. Min Ouyang, an associate professor at Beijing’s Tsinghua University, found that in past recessions the ‘scarring’ of entrepreneurs from the collapse of cash flow outweighed the beneficial effects of forcing weak companies to shut down and ‘cleansing’ the way for those who survive. “The scarring effect of this recession is probably going to be more severe than of any past recessions….If we say that pandemics are the new normal, then people will be much more hesitant to take risks,” she says.

Households and companies would want more savings and less risk to protect against possible future shutdowns, while governments would need to stockpile emergency equipment and ensure they could rapidly manufacture more within their own borders. Even if the pandemic turns out to be a one-off, many people will be reluctant to socialize once the lockdown ends, extending the pain for companies and economies that rely on tourism, travel, eating out and mass events.

And this slump will accelerate trends in capitalist accumulation that were already underway: Lisa B. Kahn, a Yale economist has found that after slumps companies try to replace workers with machines and so force workers returning to employment to accept lower incomes or find other jobs, which pay less. Research After all, that is one of the purposes of the ‘cleansing’ process for capital: to get labour costs down and boost profitability. It scars labour for life.

“This experience is going to leave deep scars on the economy and on consumer/investor/business sentiment. This is going to scar a generation just as deeply as the Great Depression scarred our parents and grandparents.” John Mauldin

Jacob Wallenberg, head of the richest capitalist family in Sweden, said in an interview with the Financial Times entitled “Coronavirus ‘medicine’ could trigger social breakdown”, that he is “dead scared of the consequences for society”. He predicted that, if the crisis is prolonged, it could mean an unemployment rate of 20–30 percent and a contraction of the economy by the same amount. In such a scenario, he said that: “There will be NO RECOVERY. There will be social unrest. There will be violence.” From the capitalist horse’s mouth.

I would put it oppositely: social breakdown (global insurrection of the working class) has triggered Coronavirus medicine (a global curfew imposed on the working class).

I will not attempt to predict the future unlike our foolish bourgeois, Wallenburg, albeit to say that mass unemployment is a deterrent to insurrectionary action.

It is the other way around, in my opinion. Mass unemployment is a main trigger for a workers insurrection. It is a subject to debate in depth, but the logic and economic evidence goes against that thesis. For example: a) V. Lenin demanded “extreme misery” as one of his requirements for a pre-revolutionary situation. b) Will the working class storm the offices of their companies shortly after employers have raised their wages (wages stagnant for years) and improved their working conditions? No, he will not. It has never done so. It did not do so in Europe in the progressive phase, 2nd WW until the 80s, of the current cycle of class struggles.

Far be it for me to contradict such an esteemed social democrat as Vladimir Lenin but if we analyse the great insurrections that occurred in the UK during the 1980’s—the riots of 1981 and the Poll Tax rebellion—both these tumultuous events for our class occurred whilst unemployment was at its lowest points (5.5% and 7% respectively) compared to its high point in 1984-5 of 12%.

If we had more worker co-ops, would that avoid production shocks?

And if not, and production shocks are unavoidable, would worker co-ops help limit scarring?

Debra. Sorry for slow reply. Yes workers coops can help cope with a production shock but long term coops will only survive as part of socialist planning across the whole economy or they will destroyed by competition from the large capitalist companies

Muy agradecido de Michael Roberts por sus interesantes artículos, los cuales entregan una muy buena orientación de lo que ha pasado e irá ocurriendo con la economía capitalista y como muestra, además, lo inútiles de las “salidas” keynesianas. Varios de sus escritos los publicamos en nuestro face y tenemos, por cierto, una carpeta donde los coleccionamos, para artículos y análisis relacionados. Gracias de nuevo.

The opposite of scarring, or hysteresis, would be an exogenic event or policy that increases output permanently. Gerald Friedman in 2016 argued that the Sanders’ Medicare for All policy would raise GDP growth to 5% per annum indefinitely, on going. ” I would argue that in the United States today, productivity and the growth rate of capacity can be raised by policies that push the economy, drawing more into the labor force and by increasing investment and productivity.” He was scolded roundly. Arguably we are set up for a lame period economically, as MR shows. Knee replacement or hip surgery, bypass surgery, whatever, is needed. We still need all the policies that progressives advocate: higher minimum wage, direct job creation, massive public housing and infrastructure, and M4A. These would lower expenses and raise income in tandem for the majority. The reform agenda does not change. I hope the benefit lies in crisis, that awareness and resolve are strengthened. The old formulas were broken. Wages from nonsupervisory workers were lower in Jan. 2020 than in Jan. 1965, the BLS shows. I wrote this in an essay: “A poll asked about missing a paycheck, every two weeks, would it be a difficulty? The American Payroll Association reports 74% said yes; 40% said a major difficulty, and 34% said a slight difficulty. A Harris poll found that respondents say they always (23%) or usually (17%) or sometimes (38%) live paycheck to paycheck, for a total of 78%.” — It is deplorable, unreasonable, outrageous — that is the awareness that might now be strengthened. I hope. Also I have to say that all this GDP metric is bothersome. I’m reading Anielski’s The Economics of Well Being, about replacing the GDP with a broader measure that includes poverty, health, social and ecological measures, measures of OKness, that’s not a good word, a subjective measure. I think 25% say they are living comfortably, 25% say “doing OK”, and the rest are getting by but stressed. That’s a measure that should be reported and worked on, obviously. The Consumer Financial Protection Bureau published a survey in 2015, “Financial Well Being” is my source, but my numbers are a little off, can’t remember. That report also said that 24% had less than $250 in liquid assets, 33% had less than $1,000, 54% had less than — can’t remember, but you get my point. Crisis for some, serious crisis.

Great analysis, I love your blogs and your thoughts. Marxist economist are needed to temper these bully market crazy capitalist economist. Thank You for all that you do, stay well

When we look at scarring we need to sharply differentiate spending based on capital gains (including share buy backs etc) and spending based on wage income. The top 10% spend as much as the bottom 80% of society and the top 10% spend is a function of capital gains. Using aggregate hours worked in the USA times the real increase in wages up to the pandemic, capital gains were responsible for 70% of the real increase in PCEs. Remember in 2019 the capital gains resulting from share and bond prices in the USA equalled the entire bill for workers’ compensation. As most workers live from paycheque to paycheque their spending is a function of the total wage bill which as Michael has pointed out is likely to decline. The real scarring takes place on the spending side driven by the top 10%. In 2010 JPMorgan’s wealth unit investigated the spending habits of its rich clients and found the stagnation in consumer spending in the economy was due to this group of super rich holding back spending. Of course this changed thereafter as share prices continued to rise restoring their confidence to spend. Could this explain why the FED is so determined to keep share prices up?

Can I ask if this economic shock is likely to push the US into second place behind China. When is China expected to have the largest economy?

Gordon China is still behind in gdp terms to the us about two thirds but now larger than the euro area as a whole. But china’s gdp per person is still way behind the us. Of course it has been catching up fast but with some way to go. The us is now determined to stop it catching up and increasing its weight and power economically, politically and financially

once again, very intrsting analysis that let others understand well the critical stage in which the world capitalst economy had between 2009-2019 even before the current impact of lockdown for corona pandymic.

itz technical critique without prejudice. nothing as i saw against capitalism, itz just the real picture that we should look at.

im in the course of writing a full translation for this valued article into arabic language for yemenis and arab world people readers.

i expect to finsh by tomorrow and the translated article to be published soon under ur name along with ur blog url.(as i did before).

just i re-edit the title in arabic to read: the scaring that covid-19 makes on the world economy.

my regards.

bilal.

Thanks bilal

translated article has been published early morning of today on alsharea’ newspaper and on its website at: https://alsharaeanews.com/%d8%aa%d8%b1%d8%ac%d9%85%d8%a7%d8%aa/%d9%86%d9%8f%d8%af%d8%a8%d9%8e%d8%a9-%d8%ac%d8%a7%d8%a6%d8%ad%d8%a9-%d9%83%d9%88%d9%81%d9%8a%d8%af-19-%d8%b9%d9%84%d9%89-%d8%a7%d9%82%d8%aa%d8%b5%d8%a7%d8%af-%d8%b1%d8%a3%d8%b3%d9%85%d8%a7%d9%84%d9%8a/

Bourgeois economists are only interested in value. Therefore, they are only interested in the growth figures of this value.

Our politicians do not ask what is vital for society, but what is “systemically relevant” for capitalism. Banks and the police are systemically relevant for politicians, but healthy food and respiratory masks are not.

A non-capitalist economy is interested in WHAT is produced and distributed. There is now a discussion in Germany as to whether the private auto industry and airlines should receive state aid or not. This is essentially a socialist question.

Note: It is not enough if Marxists only deal with these growth figures.

Wal Buchenberg, Hannover

Interesting. But does it not suggest a rational element within the capitalist class regarding the non-sustainability of the capitalist mode of production… and a bit of radical Keynesianism? Maybe not. There is nothing Keynesian about Marx and Engel’s view that the concentration of capital, particularly in the financial section is an important step toward the socialization of production…via the “euthanasia of the rentiers”? Which is NOT Keynesian, if regulated by the labor theory of value.

Correction: The dependent clause of the last sentence should read: ” …if regulated by a labor theory of value which assumes labor’s point of view in determining socially necessary labor time.

To put it on its head. What is bad in “scarring”, less propensity to (over-) consume, in an economic (human stoffwechsel with nature) situation with extreme over-exploitation and extreme waste?

It is bad because it is chaotic and unplanned, and ignores and disregards the interests of most people.

I agree in principle. And I think that there will be hunger and starvation in the future of this crisis. But right now the most scarring seems to affect other less neccesary products than food and such. Mayby there will be some less individual commuting by private cars in the future. As to “ignores and disregards the interests of most people” – so does the car-producers, even in the best of times.

The difficult part will be if and when the international value chains for foodstuff breaks down. If the proletarians will be able to close the ports to save themselves from starvation. And not have to experience another version of the Irish famine – caused by potato-blight and the continued export of food to make safe the income of the absentee landlords.

Interesting report in today’s Financial Times date stamped Johannesburg, that 29 times as many people will starve than die directly from the virus.

Thankyou for writing as many of these blogs as you have. I genuinely hope your health and wellbeing are safe during this crisis and the interesting times ahead of us all. Everytime I read one of your posts I learn something new and they’ve been helpful in giving me some understanding in the limited time I have to pay attention to economics.

Thanks – appreciate the work you do.