Next week, all the leaders of the top G20 nations meet in Brisbane Australia. The OECD has issued its latest forecast for global economic growth for that meeting to consider (http://www.oecd.org/eco/outlook/economicoutlook.htm). It’s the usual mantra from the all the international agencies, namely that global growth is still “stuck in low gear” i.e. well below the trend growth before the Great Recession; BUT don’t worry, next year things are going to pick up.

As the OECD puts it in its report, the world economy “is expected to accelerate gradually if countries implement growth-supportive policies”. Note the caveat, IF the G20 leaders adopt more ‘growth-supportive’ measures.

The OECD reckons that global real GDP growth will be just 3.3% this year, but will “accelerate” to 3.7% in 2015 and 3.9% in 2016. But even that will be “modest compared with the pre-crisis period and somewhat below the long-term average.”

This mild acceleration, assuming it is achieved, and that is open to serious doubt, will be led by the US economy, forecast by the OECD to grow by 2.2% this year, jumping to 3% in 2015 and 2016. The OECD recognises that Europe and Japan will be lucky to grow more than 1% over the same period.

The stagnation in Europe, particularly the Eurozone, was also confirmed by the latest forecasts from the EU Commission, also released last week (http://ec.europa.eu/economy_finance/eu/forecasts/2014_autumn_forecast_en.htm). The Commission cut its forecasts yet again, saying the Eurozone would expand by only 0.8% this year, 1.1% next year and by 1.7% in 2016 – a level the Commission said six months ago would be achieved next year. So once again, the Commission has cut its more optimistic forecasts: it always jam tomorrow.

The OECD commented in its report that “we have yet to achieve a broad-based, sustained global expansion, as investment, credit and international trade remain hesitant,” And the the EU’s economics commissioner, Pierre Moscovici, repeated much the same thing: “There is no single and simple answer. The economic recovery is clearly struggling to gather momentum”.

What puts some doubt about even the modest acceleration in growth that the OECD expects globally and the EU Commission expects for the Eurozone is that the high frequency indicators about future economic activity are beginning to turn down. The Markit purchasing managers indexes are increasingly used as indicator of future activity. They unreliable because they are only surveys of corporate executives about their activity, not hard data. But the latest outcomes for October show a slowing of expansion (index above 50) for the world as a whole, led by the developed economies.

Why has the recovery since 2009 in the G20 economies been so weak? Well, the EU Commission ventured some reasons. As it put it: “recoveries following deep financial crises are more subdued than recoveries following normal recessions…recent estimates suggest that it would take about 6½ years (median) or eight years (mean) to return to the pre-crisis income level in the wake of a deep economic and financial crisis”… but in fact, “the recovery from the recession in 2008-09 has been slower than any other recovery in the post-World War II period on both sides of the Atlantic.”

So the global financial crash is the biggest factor to make recovery slower than normal. And it is true that the crash and the subsequent bailout by governments across the major economies by raising more debt has left a heavy burden of debt financing, despite near zero interest rates. As the OECD shows, advanced economy overall debt levels are actually higher now than they were in 2007. And China too has built up debt that is close to many advanced economies.

The EU Commission makes the point that a possible reason why the US economy has recovered better is that “US corporations have cut debt more than those in the euro area. This has been supported by positive profitability trends providing companies in the US with the internal funds necessary for adjustment of balance sheets.” The EU Commission argues that “delayed deleveraging in Europe can be expected to weigh on investment activity and thus to explain partly the gap between the contributions to GDP growth in the euro area and in the US.”

Better profitability has enabled US corporations to hoard cash, buy back their own shares to boost the market value of the company and thus executive bonuses and share options, but it has also allowed a relatively faster rise in productive investment, albeit still poor compared with before the Great Recession. Investment in productive assets per head of population still has not reached the peak levels of 2007 in any of the major advanced capitalist economies, but at least the US has done better.

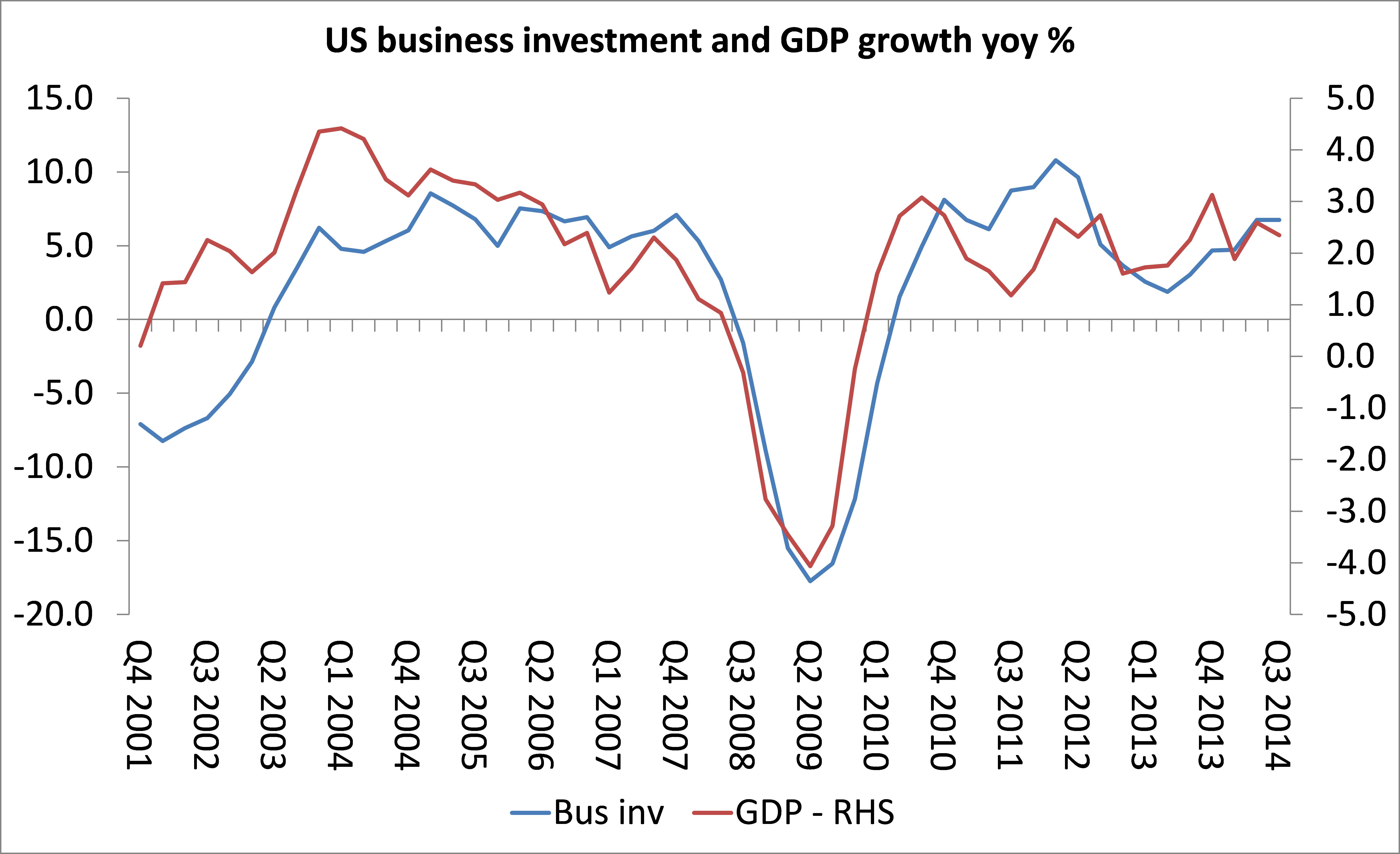

Interestingly, the OECD shows that private consumption per head has not fallen at all since 2005. The Great Recession was not triggered by a collapse in consumption but in investment – an argument against the Keynesian view of crises, which I have raised in several posts (https://thenextrecession.wordpress.com/2012/11/30/us-its-investment-not-consumption/). Indeed, there is a very high correlation between US business investment and US real GDP growth as the graph below shows.

Where investment goes, so will growth. And, in my view, investment follows profits. And not just my view, as I remind readers again of the empirical work of Tapia Granados and others (see my post, https://thenextrecession.wordpress.com/2012/06/26/profits-call-the-tune/). Profits call the tune.

But in the US, where the economic recovery has been greatest relatively, corporate profit growth has now ceased.

In the graph below, I have lagged investment growth (blue line) by one year against profit growth (red line). It shows that when profits turn down and eventually go negative, one year later or so, business investment collapses and when profits expand, investment follows within a year.

Currently with profits not growing, investment will follow by mid-2015, this suggests. And with investment closely correlated with GDP growth, the risk of recession in one year or so looks high. The world economy would then be in reverse gear.

Michael,

You say,

“Currently with profits not growing, investment will follow by mid-2015, this suggests.”

I predicted a year ago that this slow down, would start in the global economy, in the third quarter of 2014, , because it fits the pattern of the three year cycle that saw slow downs in 2011, 2008, 2005, 2002 and so on going back about thirty years. On the basis of past cycles it will last for about four quarters.

However, perhaps you have more data about the current state of US corporate profits than I have at hand. Watching US CNBC, they seem to be suggesting from actual company earnings reports that the average increase in earnings has been around 12%, which does not seem to suggest such a slow down as that you refer to.

According, to reports the misses seem to have been in respect of revenues rather than earnings. Its always necessary to be wary of earnings figures, because, as I’ve shown elsewhere, its quite possible to record higher earnings, whilst simultaneously suffering a lower rate of annual profit. It is even more open to manipulation in respect of earnings per share, because of the potential to inflate figures by companies buying back shares.

I would be interested to know how the proportion of consumption has changed between the working class and capitalist class since 2007. I’ve read a lot of articles in papers like the NYT stating that retailers and producers have adjusted to cater to the upscale market but some more concrete data would be interesting.

Yes, I think luxury consumption has become an increasingly important element of PCE as inequality has risen. I’ve never been able to find data on it either, though car production is one place where it can be seen. It tends to be forgotten by underconsumptionists.

Reblogged this on Alejandro Valle Baeza.