I’m sure when this disaster is over, mainstream economics and the authorities will claim that it was an exogenous crisis nothing to do with any inherent flaws in the capitalist mode of production and the social structure of society. It was the virus that did it. This was the argument of the mainstream after the Great Recession of 2008-9 and it will be repeated in 2020.

As I write the coronavirus pandemic (as it is now officially defined) has still not reached a peak. Apparently starting in China (although there is some evidence that it may have started in other places too), it has now spread across the globe. The number of infections is now larger outside China than inside. China’s cases have trickled to a halt; elsewhere there is still an exponential increase.

This biological crisis has created panic in financial markets. Stock markets have plunged as much 30% in the space of weeks. The fantasy world of every rising financial assets funded by ever lower borrowing costs is over.

COVID-19 appears to be an ‘unknown unknown’, like the ‘black swan’-type global financial crash that triggered the Great Recession over ten years ago. But COVID-19, just like that financial crash, is not really a bolt out of the blue – a so-called ‘shock’ to an otherwise harmoniously growing capitalist economy. Even before the pandemic struck, in most major capitalist economies, whether in the so-called developed world or in the ‘developing’ economies of the ‘Global South’, economic activity was slowing to a stop, with some economies already contracting in national output and investment, and many others on the brink.

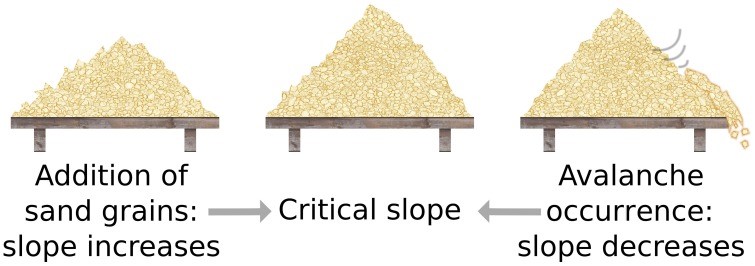

COVID-19 was the tipping point. One analogy is to imagine a sandpile building up to a peak; then grains of sand start to slip off; and then comes a certain point with one more sand particle added, the whole sandpile falls over. If you are a post-Keynesian you might prefer calling this a ‘Minsky moment’, after Hyman Minsky, who argued that capitalism appears to be stable until it isn’t, because stability breeds instability. A Marxist would say, yes there is instability but that instability turns into an avalanche periodically because of the underlying contradictions in the capitalist mode of production for profit.

Also, in another way, COVID-19 was not an ‘unknown unknown’. In early 2018, during a meeting at the World Health Organization in Geneva, a group of experts (the R&D Blueprint) coined the term “Disease X”: They predicted that the next pandemic would be caused by an unknown, novel pathogen that hadn’t yet entered the human population. Disease X would likely result from a virus originating in animals and would emerge somewhere on the planet where economic development drives people and wildlife together.

Disease X would probably be confused with other diseases early in the outbreak and would spread quickly and silently; exploiting networks of human travel and trade, it would reach multiple countries and thwart containment. Disease X would have a mortality rate higher than a seasonal flu but would spread as easily as the flu. It would shake financial markets even before it achieved pandemic status. In a nutshell, Covid-19 is Disease X.

As socialist biologist, Rob Wallace, has argued, plagues are not only part of our culture; they are caused by it. The Black Death spread into Europe in the mid-14th century with the growth of trade along the Silk Road. New strains of influenza have emerged from livestock farming. Ebola, SARS, MERS and now Covid-19 has been linked to wildlife. Pandemics usually begin as viruses in animals that jump to people when we make contact with them. These spillovers are increasing exponentially as our ecological footprint brings us closer to wildlife in remote areas and the wildlife trade brings these animals into urban centers. Unprecedented road-building, deforestation, land clearing and agricultural development, as well as globalized travel and trade, make us supremely susceptible to pathogens like corona viruses.

There is a silly argument among mainstream economists about whether the economic impact of COVID-19 is a ‘supply shock’ or a ‘demand shock’. The neoclassical school says it is a shock to supply because it stops production; the Keynesians want to argue it is really a shock to demand because people and businesses won’t spend on travel, services etc.

But first, as argued above, it is not really a ‘shock’ at all, but the inevitable outcome of capital’s drive for profit in agriculture and nature and from the already weak state of capitalist production in 2020.

And second, it starts with supply, not demand as the Keynesians want to claim. As Marx said: “Every child knows a nation which ceased to work, I will not say for a year, but even for a few weeks, would perish.” (K Marx to Kugelmann, London, July 11, 1868). It is production, trade and investment that is first stopped when shops, schools, businesses are locked down in order to contain the pandemic. Of course, then if people cannot work and businesses cannot sell, then incomes drop and spending collapses and that produces a ‘demand shock’. Indeed, it is the way with all capitalist crises: they start with a contraction of supply and end up with a fall in consumption – not vice versa.

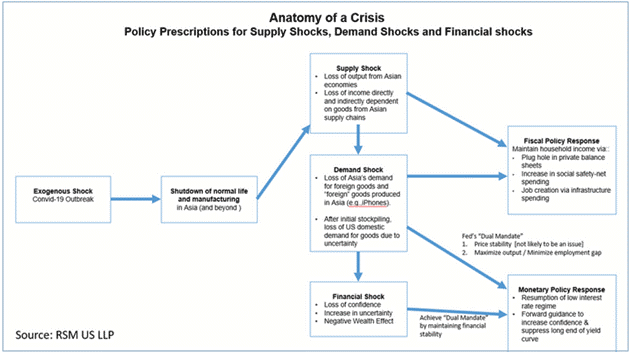

Here is one mainstream (and accurate) view of the anatomy of crises.

Some optimists in the financial world are arguing that the COVID-19 shock to stock markets will end up like 19 October 1987. On that Black Monday the stock market plunged very quickly, even more than now, but within months it was back up and went on up. Current US Treasury Secretary Steven Mnuchin is sure that the financial panic will end up like 1987. “You know, I look back at people who bought stocks after the crash in 1987, people who bought stocks after the financial crisis,” he continued. “For long-term investors, this will be a great investment opportunity.” “This is a short-term issue. It may be a couple of months, but we’re going to get through this, and the economy will be stronger than ever,” the Treasury secretary said.

Mnuchin’s remarks were echoed by White House economic adviser Larry Kudlow, who urged investors to capitalize on the faltering stock market amid coronavirus fears. “Long-term investors should think seriously about buying these dips,” describing the state of the U.S. economy as “sound.” Kudlow really repeated what he said just two weeks before the September 2008 global financial crash: “for those of us who prefer to look ahead, through the windshield, the outlook for stocks is getting better and better.”

The 1987 crash was blamed on heightened hostilities in the Persian Gulf leading to a hike in oil prices, fear of higher interest rates, a five-year bull market without a significant correction, and the introduction of computerized trading. As the economy was fundamentally ‘healthy’ so it did not last. Indeed, the profitability of capital in the major economies was rising and did not peak until the late 1990s (although there was a slump in 1991). So 1987 was what Marx called a pure ‘financial crash’ due to the instability inherent in speculative capital markets.

But that is not the case in 2020. This time the collapse in the stock market will be followed by an economic recession as in 2008. That’s because, as I have argued in previous posts, now the profitability of capital is low and global profits are static at best, even before COVID-19 erupted. Global trade and investment have been falling, not rising. Oil prices have collapsed, not risen. And the economic impact of COVID-19 is found first in the supply chain, not in unstable financial markets.

What will be the magnitude of the slump to come? There is an excellent paper by Pierre-Olivier Gourinchas that models the likely impact. He shows the usual pandemic health diagram doing the rounds. Without any action, the pandemic takes the form of the red line curve, leading to a huge number of cases and deaths. With action on lockdowns and social isolation, the peak of the (blue) curve can be delayed and moderated, even if the pandemic gets spun out for longer. This supposedly reduces the pace of the infection and the number of deaths.

Public health policy should aim to “flatten the curve” by imposing drastic social distancing measures and promoting health practices to reduce the transmission rate. Currently Italy is following the Chinese approach of total lockdown, even if it may be closing the stable doors after the virus has bolted. The UK is attempting a very risky approach of self-isolation for the vulnerable and allowing the young and healthy to get infected in order to build up so-called ‘herd immunity’ and avoid the health system being overwhelmed. What this approach means is basically writing off the old and vulnerable because they are going to die anyway if infected and avoiding a total lockdown that would damage the economy (and profits). The US approach is basically to do nothing at all: no mass testing, no self-isolation, no closure of public events; just wait until people get ill and then deal with the severe cases.

We could call this latter approach the Malthusian answer. The most reactionary of the classical economists in the early 19th century was the Reverend Thomas Malthus, who argued that there were too many ‘unproductive’ poor people in the world, so regular plagues and disease were necessary and inevitable to make economies more productive.

British Conservative journalist Jeremy Warner argued this for the Covid-19 pandemic which ‘primarily kills the elderly’. “Not to put too fine a point on it, from an entirely disinterested economic perspective, the COVID-19 might even prove mildly beneficial in the long term by disproportionately culling elderly dependents.” Responding to criticism ‘Obviously, for those affected it is a human tragedy whatever the age, but this is a piece about economics, not the sum of human misery.’ Indeed, that’s why Marx called economics in the early 19th century – the philosophy of misery.

The reason that the US and British governments won’t impose (yet) draconian measures, as in China eventually and now in Italy (belatedly) and elsewhere, is because it will inevitably steepen the macroeconomic recession curve. Consider China or Italy: increasing social distances has required closing schools, universities, most non-essential businesses, and asking most of the working-age population to stay at home. While some people may be able to work from home, this remains a small fraction of the overall labour force. Even if working from home is an option, the short-term disruption to work and family routines is major and likely to affect productivity. In short, the best public health policy plunges the economy into a sudden stop. The supply shock.

The economic damage would be considerable. Gourinchas attempts to model the impact. He assumes that relative to a baseline, containment measures reduce economic activity by 50% for one month and 25% for another month, after which the economy returns to the baseline. “That scenario would still deliver a massive blow to headline GDP numbers, with a decline in annual output growth of the order of 6.5% relative to the previous year. Extend the 25% shutdown for just another month and the decline in annual output growth (relative to the previous year) reaches almost 10%!” As a point of comparison, the decline in output growth in the U.S. during the 2008-09 `Great Recession’ was around 4.5%. Gourinchas concludes that “we are about to witness a downturn that could dwarf the Great Recession.”

At the peak of the Great Recession, the US economy was shedding jobs at the rate of 800,000 workers per month, but the vast majority of people were still employed and working. The unemployment rate peaked at `just’ 10%. By contrast, the coronavirus is creating a situation where – for a brief amount of time – 50% or more of people may not be able to work. The impact on economic activity is comparatively that much larger.

The upshot is that the economy, like the health system, faces a ‘flatten the curve’ problem. The red curve plots output lost during a sharp an intense downturn, amplified by the economic decisions of millions of economic agents trying to protect themselves by cutting spending, shelving investment, cutting down credit and generally hunkering down.

What to do to flatten the curve? Well, central banks can and are providing emergency liquidity to the financial sector. Governments can deploy discretionary targeted fiscal measures or broader programs to support economic activity. These measures could help `flatten the economic curve’, i.e. limit the economic loss, as in the blue curve, by keeping workers paid and employed so they can meet bills or have bills delayed or written off for a period. Small businesses could be funded to ride out the storm and banks bailed out, as in the Great Recession.

But a financial crisis is still a high risk. In the US, corporate debt has risen and is concentrated in bonds issued by the weaker companies (BBB or lower).

And the energy sector is being hit with a double whammy as oil prices have plunged. Bond risk premia (the cost of borrrowing) have rocketed in the energy and transport sectors.

Monetary easing certainly won’t be enough to flatten the curve. Central bank interest rates are already near, at or below zero. And the huge injections of credit or money into the banking system will be like ‘pushing on a string’ in its effect on production and investment. Cheap financing won’t speed up the supply chain or make people want to travel again. Nor will it help corporate earnings if customers aren’t spending.

The main economic mitigation will have to come from fiscal policy. The international agencies like the IMF and World Bank have offered $50bn. National governments are now launching various fiscal stimulus programmes. The UK government announced a big spend in its latest budget and the US Congress has agreed an emergency spend.

But is it enough to flatten the curve if two months of lockdown knock back most economies by a staggering 10%? None of the current fiscal packages come anywhere near 10% of GDP. Indeed, in the Great Recession, only China delivered such an amount. The UK government’s proposals amount to just 1.5% of GDP maximum, while Italy’s is 1.4% and the US at less than 1%.

There is a chance that by the end of April we will have seen the global total number of cases peak and begin to decline. That is what governments are hoping and planning for. If that optimistic scenario happens, the coronavirus will not disappear. It become yet another flu-like pathogen (which we know little about) that will hit us each year like its predecessors. But even two months lockdown will incur huge economic damage. And the monetary and fiscal stimulus packages planned are not going to avoid a deep slump, even if they reduce the ‘curve’ to some extent. The worst is yet to come.

“And second, it starts with supply, not demand as the Keynesians want to claim. As Marx said: “Every child knows a nation which ceased to work, I will not say for a year, but even for a few weeks, would perish.” (K Marx to Kugelmann, London, July 11, 1868).”

This is a bit desperate. Marx’s point was that its necessary to produce in order to consume, but its the requirement to consume, i.e. demand, that creates the necessity to produce Elsewhere, Marx gives the example of the natives who could live for a week simply on the back of a couple of hours work per week, and, who, therefore saw no need to work any more than that.

Indeed, Marx in his refutation of the point you are making when put forward by Ricardo, sets out that the basis of expanded reproduction is the fact that producers expect demand to rise year on year as a result of rising population (and it could be added rising living standards) so that the market expands. Each producer on the back of this expectation of increased demand, and a larger market seeks to get their share of it, by expanding their production, and in doing so they also thereby provide not only the supply to meet that demand, but also provide the money revenues required to purchase it.

“….Marx gives the example of the natives who could live for a week simply on the back of a couple of hours work per week, and who, therefore, saw no need to work any more that that.”

Your quote makes no sense regarding the historically specific context of this post because the “natives” in Marx’s quote are obviously direct producers and consumers of use values… not modern capitalism’s alienated producers of global commodities chains, precarious employed service providers, etc. You tend to conflate in debate.

I do agree about the economic consequences of flattening the curve. Those economic consequences caused by unnecessarily closing down economic activity will have much worse effects than the virus itself. The policy of flattening the curve is irrational, and a response to a moral panic, and demands that “something must be done”, which means that populist governments like that of Trump and Johnson inevitably implement large-scale, visible responses that are often irrational.

It would be far more rational to quickly “vaccinate” the vast majority of the population that is not at high risk of serious consequences from the virus, by what scientists call encouragement of “herd immunity”, amongst the 80% of the population who suffer either no or only very mild symptoms. That would get it out of the way quickly, and minimise the time and cost of isolating the minority of the population who are at risk.

You haven’t taken your argument to its logical conclusion.

If it’s true that 80% of the population will suffer ” no, or very mild” reactions to CoVid19, it would make more sense to inject them all with it!

This would create Herd Immunity in one fell swoop!

OK, there’d be some collateral damage, but 79% of the population would recover and keep on working.

In fact, Cuba eradicated Polio in the early 1960’s by vaccinating all of its children in just a few days, (this was because vaccines couldn’t be stored locally due to lack of refrigeration)

The exercise was repeated 6 months later – and worked.

The Johnson government’s initial strategy was based on a similar idea. Except that live viruses, are neither de-activated, nor attenuated. So, many people were rightly alarmed by it.

The Tories have now backtracked.

They now claim that they will test and track all suspected cases.

Until we get a vaccine, this is the best way to limit the spread of the disease.

Meanwhile we need to make sure that the staff and resources available to the NHS are dramatically increased.

Hope you don’t mind, Robert, but I did a “copy and paste” instead of a ‘reblog.’ Do let me know if you have any issues with that.

no problem

And my apologies. I mean’t “Michael,” of course. How embarrassing. Lack of sleep and old age. . .

US is closing public events at least county by county. In Santa Clara County (Silicon Valley), they first started by closing events of a thousand or more and now it’s a 100 or more. San Jose put in laws so landlords could not evict those that could not pay rent because of loose of jobs or illness from COVID-19. So it isn’t nationwide but there is no reason it should be in the US.

”t started by closing events of a thousand or more and now it’s a 100 or more. San Jose put in laws so landlords could not evict those that could not pay rent because of loose of jobs or illness from COVID-19.” i.e. infringed on the rights of private property. If only the ‘left’ were so bold! Note in organising the fight against the virus the bourgeoisie does not rely on ‘market forces’!

Just got this now to follow up on my post.

“Important COVID-19 notification from San Mateo County Public Health. On order of the health officer, gatherings of more than 50 individuals are prohibited in San Mateo County effective 12:01 a.m. Sunday, March 15, 2020. Gatherings between 10 and 50 are prohibited unless specific mitigation measures are taken: See e-mail for details and an outline of precautions that must be taken”

Different approaches based on circumstance and not just because it’s all about profit.

I’m 74 (in a week) and my chances are 1 in 10 to die if I catch the virus. I’ll self-isolate. Good article.

Please stay safe! All of the young people who aren’t risk also have a responsibility to self isolate to protect our most vulnerable!

That would mean not going to work! So, no health workers, no social care workers, no delivery drivers, no food producers, no electricity supply workers. How long do you think everyone, let alone the vulnerable would live without food and electric?

The policy of closing down economic activity, when there is no threat to 80% of the population from the virus is totally bonkers!

“The policy of closing down economic activity, when there is no threat to 80% of the population from the virus is totally bonkers!”

Spoken by someone who obviously believes he is part of the 20%.

What’s totally bonkers is the diversion of attention to the “economy” as if the virus is separate and apart from the “economy”- so that the worry becomes the fate of the airlines, rather than the inability, and unwillingness of the governments to distribute medical protective gear to the medical professionals (Trump telling state governors that they should develop “their own” sources of supply, when FEMA and other agencies have warehoused masks, gowns, gloves, and complete 12 bed medical units). What’s bonkers is the failure of governments (particularly the US and the UK) to “test, test, test.”

Bonkers policy actions are thel bonkers follow up to bonkers inactions… except the inactions aren’t bonkers, they are the bonkers logical conclusion of the Hobbesian aspect of capitalism, of social Darwinism, of the “there is no such thing as society” diktat of the “free market.” The virus IS the economy. It’s the genome of the conqueror.

My dear friends.

There is a factor that everyone is forgetting, if the COVID-19 coronavirus behaves like its “cousin” MERS, just miss a minute and read its update in NOVEMBER 2019 (http: //applications.emro.who.int/docs/EMRPUB-CSR-241-2019-EN.pdf?ua=1&ua=1&ua=1). That is, even with high mortality (30%), the virus has not yet disappeared.

The FED has just cut interest rates to zero, abolished bank reserve requirements, formally relaunched QE and increased swap lines with foreign banks to alleviate the world wide dollar shortage. This may save the banks but it will not save the financialised useless US health system which has allowed hundreds of thousands if not millions of Americans to become infected.

If anyone is interested, my brother is a Professor of Statistical Epidemiology at Michigan State. He sent me this link to a site that has all the Corona data you could ever need.

https://ourworldindata.org/coronavirus

Very good site. I use this one. https://www.worldometers.info/coronavirus/coronavirus-cases/

Michael,

Am sad to say it is all coming together pretty much exactly as we discussed, with the only ‘surprise’ being the shock in question. Financial conditions are still tightening, even with the scale of central bank intervention. I think this is an appropriate time to start forwarding recommendations for a socialist response, at least to encourage alternative ways of addressing a crisis where monetary policy is dead and Keynesian fiscal policy is lackluster.

Stay safe,

B.R.

Appreciate your blog and am subscribed to your email updates (having first heard you on Counterpunch Radio). Concerned with this clause in your second paragraph: “Apparently starting in China (although there is some evidence that it may have started in other places too).” What evidence is there that it started outside of Wuhan, aside from conspiracy theory? If you’ve got some, I’ve certainly missed it—and it ought to be hyperlinked. If not that clause seems rather irresponsible, and is incorrect. Thanks

>

There are accusations from some Americans that it was virus strain produced by Wuhan lab that escaped. In contrast some Chinese counter that it came from us servicemen in Hawaii. But i agree none of this seems likely. The most likely is animal to human transmission starting probably with bats and then to some other animal that perhaps humans ate. But even that is still unclear. Apparently the virus may have been around well before Wuhan but was misdiagnosed as flu. All theories and no firm evidence.

Very good article Michael. I agree with you in this topic. I’ve reblogged your post. Thanks and good luck!

I live in south Cyprus, whose economy is heavily dependent on tourism, and which had its first covid-19 case a few days ago. Infection is spreading rapidly. Obviously, there is a huge problem with tourism, and the economy.

It Seems to me this is an opportunity to show the difference between a national capitalist economy and a more or less internationally organised socialist economy.

The covid-19 epidemic hits both the supply and demand side of the tourist industry. That is unlike what would happen in, lets say, a catastrophe hitting important parts of agriculture, say a catastrophic wheat virus, where it would compromise the supply side, but not the demand side.

In a socialist economy the second type of catastrophe would cause hardship. But in the case of tourism and covid-19, it would cause no additional significant problems, apart from the logistics of how to use the human potential of the workers employed in tourism. One problem less, in a society trying to handle the “natural” emergency.

Obviously this is not the time to belabor scenarios or thoughts, about a future international socialist society. Still, I think it is within the valid answers to the “blame everything on a natural phenomenon” or “it was the virus that did it” approach.

I am not a trained economist, so Michael I would like your comments on this.

I agree. If government and workers are in control of these industries any supposedly existential shock can be mitigated. Capitalism cannot do that as well because the market and profit must rule over need

Oh, and the Jeremy Warner link returns a “404”, not found. Has he deleted it? I would really like to be able to use the reference in an article I am writing.

https://metro.co.uk/2020/03/11/telegraph-journalist-says-coronavirus-cull-elderly-benefit-economy-12383907/

This should work and I have corrected the post too.

Thanks, it does work. Hope you will also comment on my previous post about tourism Cyprus and socialism. I reread your post, saw the demand shock vs supply shock arguments. That however concerns the mechanisms of capitalist crises, not the difference socialism would make. Also tourism is a special case of an industry directly affected by a lockdown. “

Greetings Michael,

Looking at the way people react to the media frenzy in regards to COVID19 do you think that this is a classic example of how bourgeois ideology reproduces itself as the dominant ideology of the modern class society and especially in the way crisis is rationalized? The main narrative that is being reproduced in the collective mind is that it is exogenous forces that are disrupting our otherwise harmonious society. This is the way economic, ecological, refugee, security crisis are being rationalized every time. Remember in the aftermath of the Charlie Hebdo terrorist attacks when the political leaders where marching through Paris dramatically holding hands, enforcing that same way of rationalizing crisis. When I look at social media today I see the same thing – society stands together against this virus and stays at home to protect the vulnerable. I believe this way of rationalization of every crisis including this one serves a specific purpose – it redirects collective social revolutionary anger towards efforts of unity between opposing classes.

This article exposes the appallingly inept response of the UK and US governments to this crisis. History will judge them very harshly.

View at Medium.com

Yes it’s very good

There is no virus just the virus of collapsing capitalism. All else is bunk. A snowflake lockdown to ensure people Stay at Home don’t react don’t resist.

Right. Try preaching that baloney gospel in Italy; or to the doctors and nurses trying to save people.

Sure thing, no virus. Just like there was no Fukushima. No Las Vegas shooter. No moon landing. And vaccines cause autism.

You sound just like a Trump supporter.

Very good article

But where did Marx refer early 19th century economics as “the philosophy of misery”?

Yes, that is a bit of a boo boo. It was Proudhon that used the term and Marx retorted with his Poverty of Philosophy in reply. The brain is slowly going and I need not to rely on it so much but on the google to check things