Financialisation, like neoliberalism, is the buzz word among leftists and heterodox economists. It dominates leftist academic conferences and circles as the theme that supposedly explains crises, as well as a cause of rising inequality in modern capitalist economies particularly over the last 40 years. The latest manifestation of this financialisation hypothesis comes from Grace Blakeley, a British leftist economist, who appears to be a rising media star in the UK. In a recent paper, she presented all the propositions of the financialisation school.

But what does the term ‘financialisation’ mean and does it add value to our understanding of the contradictions of modern capitalism and guide us to the right policy to change things? I don’t think so. This is because either the term is used so widely that it provides very little extra insight; or it is specified in such a way as to be both theoretically and empirically wrong.

The wide definition mainly quoted by the financialisation school was first offered by Gerald Epstein. Epstein’s definition was “financialization means the increasing role of financial motives, financial markets, financial actors and financial institutions in the operation of the domestic and international economies.” As you can see, this tells us little beyond the obvious that we can see in the development of modern, mature capitalism in the 20th century.

But as Epstein says: “some writers use the term ‘financialization’ to mean the ascendancy of ‘shareholder value’ as a mode of corporate governance; some use it to refer to the growing dominance of capital market financial systems over bank-based financial systems; some follow Hilferding’s lead and use the term ‘financialization’ to refer to the increasing political and economic power of a particular class grouping: the rentier class; for some financialization represents the explosion of financial trading with a myriad of new financial instruments; finally, for Krippner (who first used the term – MR) herself, the term refers to a ‘pattern of accumulation in which profit making occurs increasingly through financial channels rather than through trade and commodity production’”.

The content of financialisation under these terms takes us much further, especially the Krippner approach. The Krippner definition takes us beyond Marx’s accumulation theory and into new territory where profit can come from other sources than from the exploitation of labour. Finance is the new and dominant exploiter, not capital as such. Thus finance is now the real enemy, not capitalism as such. And the instability and speculative nature of finance capital is the real cause of crises in capitalism, not any fall in the profitability of production of things and services, as Marx’s law of profitability argues.

As Stavros Mavroudeas puts it in his excellent new paper (393982858-QMUL-2018-Financialisation-London), the ‘financialisation hypothesis’ reckons that “money capital becomes totally independent from productive capital (as it can directly exploit labour through usury) and it remoulds the other fractions of capital according to its prerogatives.” And if “financial profits are not a subdivision of surplus-value then…the theory of surplus-value is, at least, marginalized. Consequently, profitability (the main differentiae specificae of Marxist economic analysis vis-à-vis Neoclassical and Keynesian Economics) loses its centrality and interest is autonomised from it (i.e. from profit – MR).”

As Mavroudeas says, financialisation is really a post-Keynesian theme “based on a theory of classes inherited from Keynes that dichotomises capitalists in two separate classes: industrialists and financiers.” The post-Keynesians are supposedly ‘radical’ followers of Keynes from the tradition of Keynesian-Marxists Joan Robinson and Michel Kalecki, who reject Marx’s theory of value based on the exploitation of labour and the law of the tendency of the rate of profit to fall. Instead, they have a distribution theory: crises are either the result of wages being too low (wage-led) or profits being too low (profit-led). Crises in the neoliberal period since the 1980s are ‘wage-led’. Increased (‘excessive’?) debt was a compensation mechanism to low wages, but only caused and exacerbated a financial crash later. Profitability had nothing to do with it.

As Mavroudeas explains, the hypothesis goes: “The advent of neoliberalism in the 1980s transformed radically capitalism. Liberalisation and particularly financial liberalization led to financialisation (as finance was both deregulated and globalized). This caused a tremendous increase in financial leverage and financial profits but at the expense of growing instability. This resulted in the 2008 crisis, which is a purely financial one.”

Linking debt to the post-Keynesian distribution theory of crises follows from the theories of Hyman Minsky, radical Keynesian economist of the 1980s, that the finance sector is inherently unstable because “the financial system necessary for capitalist vitality and vigor, which translates entrepreneurial animal spirits into effective demand investment, contains the potential for runaway expansion, powered by an investment boom.” The modern follower of Minsky,Steve Keen, puts it thus: “capitalism is inherently flawed, being prone to booms, crises and depressions. This instability, in my view, is due to characteristics that the financial system must possess if it is to be consistent with full-blown capitalism.” Blakeley too follows closely the Minsky-Kalecki analysis and offers it as an improvement on or a modern revision of Marx.

Many in the financialisation school go onto argue that ‘financialisation’ has created a new source of profit (secondary exploitation) that does not come from the exploitation of labour but from gouging money out workers and productive capitalists through financial commissions, fees, and interest charges (‘usury’). I have argued in many posts that this is not Marx’s view.

Post-Keynesian authors and supporters of financialisation like JW Mason refer to the work of mainstream economists like Mian and Siaf to support the idea that modern capitalist crises are the result of rising inequality, excessive household debt leading to financial instability and have nothing to do with the failure of profit ability in productive investment. Mian and Sufi published a book, called the House of Debt, described by the ‘official’ proponent of Keynesian policies, Larry Summers, as the best book this century! In it, the authors argue that “Recessions are not inevitable – they are not mysterious acts of nature that we must accept. Instead recessions are a product of a financial system that fosters too much household debt”.

For me, financialisation is a hypothesis that looks only at the surface phenomena of the financial crash and concludes that the Great Recession was the result of financial recklessness by unregulated banks or a ‘financial panic’. Marx recognised the role of credit and financial speculation. But for him, financial investment was a counteracting factor to the tendency for the rate of profit to fall in capitalist accumulation. Credit is necessary to lubricate the wheels of capitalist commerce, but when the returns from the exploitation of labour begin to drop off, credit turns into debt that cannot be repaid or at serviced. This is what the financialisation school cannot explain: why and when does credit turn into excessive debt?

UNCTAD is a UN research agency specialising in trade and investment trends. It published a report on the move from investment in productive to financial assets. It was written by leading post-Keynesian economists. It found that companies used more of their profits to buy shares or pay our dividends to shareholders and so less was available productive investment. But again, this does not tell us why this started to happen from the 1980s.

In the current issue of Real World Economics Review, an on-line journal dominated by post-Keynesian analysis and the ‘financialisation’ school, John Bolder considers the connection between the ‘productive and financial uses of credit’: “up until the early 1980s, credit was used mostly to finance production of goods and services. Growth in credit from 1945 to 1980 was closely linked with growth in incomes. The incomes that were generated were then used to amortize and eventually extinguish the debt. This represented a healthy use of debt; it increased incomes and introduced negligible financial fragility.” But from the 1980s, “credit creation shifted toward asset-based transactions (e.g., real estate, equities bonds, etc.). This transition was also fuelled by the record-high (double-digit) interest rates in the early 1980s and the relatively low risk-adjusted returns on productive capital”.

‘Financialisation’ could be the word to describe this development. But note that Bolder recognises that it was fall in profitability (‘low risk-adjusted returns on productive capital’) in productive investment and the rise in interest costs that led to the switch to what Marx would call investment in fictitious capital. But this does not mean that finance capital is now the decisive factor in crises or slumps. Nor does it mean the Great Recession was just a financial crisis or a ‘Minsky moment’ (to refer to Hyman Minsky’s thesis that crises are a result of ‘financial instability’ alone). Crises always appear as monetary panics or financial collapses, because capitalism is a monetary economy. But that is only a symptom of the underlying cause of crises, namely the failure to make enough money!

Guglielmo Carchedi, in his excellent, but often ignored Behind the Crisis states: “The basic point is that financial crises are caused by the shrinking productive base of the economy. A point is thus reached at which there has to be a sudden and massive deflation in the financial and speculative sectors. Even though it looks as though the crisis has been generated in these sectors, the ultimate cause resides in the productive sphere and the attendant falling rate of profit in this sphere.”

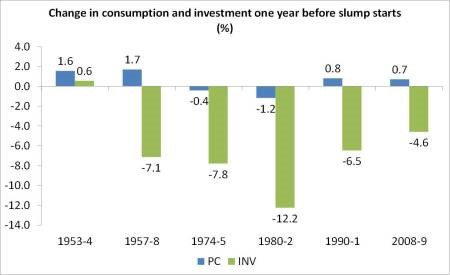

Despite the claims of the financialisation school, the empirical evidence is just not there. For example, Mian and Sufi reckon that the Great Recession was immediately caused by a collapse in consumption. This is the traditional Keynesian view. But the Great Recession and the subsequent weak recovery was not the result of consumption contracting, but investment slumping (see my post, https://thenextrecession.wordpress.com/2012/11/30/us-its-investment-not-consumption/).

Recently Ben Bernanke, former head of the US Federal Reserve during the great credit boom of the early 2000s, has revived his version of ‘financialisation’ as the cause of crises. For him, crises are the result of ‘financial panics’ – ie people just lose their heads and panic into selling and calling in their credits in a completely unpredictable way (“Although the panic was certainly not an exogenous event, its timing and magnitude were largely unpredictable, the result of diverse structural and psychological factors”). In his latest revival, Bernanke considers empirically any connection between ‘financial variables’ like credit costs and ‘real economic activity’. He concludes that “the empirical portion of this paper has shown that the financial panic of 2007-2009, including the runs on wholesale funding and the retreat from securitized credit, was highly disruptive to the real economy and was probably the main reason that the recession was so unusually deep.”

But when we look at the evidence provided, Bernanke has to admit that “balance sheet factors (ie changes in debt etc) do not forecast economic developments well in my setup.” In other words, his conclusions are not supported by his own empirical results. “It may be that both household and bank balance sheets evolve too slowly and (comparatively) smoothly for their effects to be picked up in the type of analysis presented in this paper.”

And yet there is plenty of evidence for the Marxist view that it is a collapse in profitability and profits in the productive sectors that is the necessary basis for a slump in the ‘real’ economy. All the major crises in capitalism came after a fall in profitability (particularly in productive sectors) and then a collapse in profits (industrial profits in the 1870s and 1930s and financial profits at first in the Great Recession). Wages did not collapse in any of these slumps until they started.

In a chapter of our new book, World in Crisis, G Carchedi provides compelling empirical support for Marx’s law of profitability showing the link between the financial and productive sectors in capitalist crises. From the early 1980s, the strategists of capital tried to reverse the low profitability reached then. Profitability rose partly through a series of major slumps (1980, 1982, 1991, 2001 etc). But it also recovered (somewhat) through so-called neoliberal measures like privatisations, ending trade union rights, reductions in government and pensions etc.

But there was also another countertendency: the switch of capital into unproductive financial sectors. “Faced with falling profitability in the productive sphere, capital shifts from low profitability in the productive sectors to high profitability in the financial (i.e., unproductive) sectors. But profits in these sectors are fictitious; they exist only on the accounting books. They become real profits only when cashed in. When this happens, the profits available to the productive sectors shrink. The more capitals try to realize higher profit rates by moving to the unproductive sectors, the greater become the difficulties in the productive sectors. This countertendency—capital movement to the financial and speculative sectors and thus higher rates of profit in those sectors—cannot hold back the tendency, that is, the fall in the rate of profit in the productive sectors.”

Financial profits have claimed an increasing share of real profits throughout the whole post–World War II phase. “The growth of fictitious profits causes an explosive growth of global debt through the issuance of debt instruments (e.g., bonds) and of more debt instruments on the previous ones. The outcome is a mountain of interconnected debts. ….But debt implies repayment. When this cannot happen, financial crises ensue. This huge growth of debt in its different forms is the substratum of the speculative bubble and financial crises, including the next one. So this countertendency, too, can overcome the tendency only temporarily. The growth in the rate of profit due to fictitious profits meets its own limit: recurring financial crises, and the crises they catalyze in the productive sectors.”

What Carchedi finds is that “Financial crises are due to the impossibility to repay debts, and they emerge when the percentage growth is falling both for financial and for real profits.“ Indeed, in 2000 and 2008, financial profits fall more than real profits for the first time.

Carchedi concludes that “It is held that if financial crises precede the economic crises, the former determine the latter, and vice versa. But this is not the point. The question is whether financial crises are preceded by a decline in the production of value and surplus value…The deterioration of the productive sector in pre-crisis years is thus the common cause of both financial and non-financial crises. If they have a common cause, it is immaterial whether one precedes the other or vice versa. The point is that the (deterioration of the) productive sector determines the (crises in the) financial sector.”

By rejecting Marx’s law of value and the law of profitability, the post-Keynesian ‘financialisation’ school opts for the idea that the distribution between profits and wages; rising inequality and debt; and above all, an inherent instability in finance that causes crises. Actually, it is ironic that these radical followers of Keynes look to the dominance of finance as the new form of (or stage in) capital accumulation because Keynes thought that capitalism would eventually evolve into a leisure society with the ‘euthanasia of the rentier’ ie the financier, would disappear. It was Marx who predicted the rise of finance alongside increasing centralisation and concentration of capital.

The rejection of changes in profits and profitability as the cause of crises in a profit-driven economy can only be ideological. It certainly leads to policy prescriptions that fall well short of replacing the capitalist mode of production. If you think finance capital is the problem and not capitalism, then your solutions will fall short.

In the Epstein book, various policy prescriptions for dealing with the evil of “excessive financialisation” are offered. Grabel (chapter 15) wants “taxes on domestic asset and foreign exchange transactions – so-called Keynes and Tobin taxes – reserve requirements on capital inflows (so-called Chilean regulations), foreign exchange restrictions, and so-called trip-wires and speed bumps, which are early warning systems combined with temporary policies to slow down the excessive inflows and/or outflows of capital.” Pollin reckons that by “taxing the excesses of financialization and channeling the revenue appropriately, governments can help to restore public services and investments which, otherwise, are among financialization’s first and most severe casualties.” This is no more radical than the policy prescriptions of Joseph Stiglitz, the ‘progressive’ Nobel prize winning economist who said, “I am no left-winger, I’m a middle of the road economist”.

Most important, if ‘financialisation is not the cause, such reforms of finance won’t work in ending rising inequality or regular and recurring slumps in economies. The financialisation school needs to remember what one of its icons, Joan Robinson once said: “Any government which had both the power and will to remedy the major defects of the capitalist system would have the will and power to abolish it altogether”.

I really don’t understand why it seems so difficult to grasp that in a money economy, where wages comprise the larger part the ‘purchasing power’ in the economy, that is to say, the ‘primary source’ of all profits, that profit margins of necessity must over time, from one economic reset to another, shrink.

After all, ‘wages’ are on the cost side of the balance sheets of all businesses; consequently, the sum of all wages taken together can never equate to a sum sufficient to cover the production costs of all businesses taken together, let alone a margin of profit that could somehow be allocated to all of those businesses.

A shrinking economy and the inevitability of bankruptcies is therefore baked into the capitalist cake. Financialization is merely an attempt at forestalling the inevitable.

Until and unless wage labor is altogether abolished and the socialized production that already exists becomes meshed to a system of equally socialized distribution of goods and services, economic crises and all of the miseries they causes are a given.

Wages can’t, but the unpaid labor can. That’s kind of the whole point of the wage– to veil the aggrandizement of the unpaid labor, which is expressed as surplus value, which is why production costs are, most of the time, met and with a margin of profit.

Any analysis of socialized human economic activity that isolates the monetary expression (i.e. analysis from the point of view of capital) of that activity from the actual production of things and services is revealed as simply silly and/or devious when subjected to an excellent historical materialist critique like yours.

But capital’s social relation is global in scale, and most of the world’s productive labor resides in the peripheries, not the centers of the present imperial system. It seems to me that analytical isolation of the centers from the peripheries of the financially manipulated global system of production is at the bottom of our current fascination with financialization in the West, where much of the wealth produced is, by design, unproductive, destructive, and fictitious.

Can capitalism’s crises be fully understood even by marxists if analysis is chained to the imperial centers?

An addendum to my comment above:

I had read most of The Long Depression– but not the last chapter, which I read after posting my comment. Well, I discovered that you addressed/address most of the questions I posed above, so to speak, before I could ask them. Thanks for this great book. It’s a guide post.

Yes financialisation is really confined to Anglo-American imperialism.

“Financialization” really isn’t all that new, is it? Marx remarks on the supposed “conflict” between industrial capital and financial capital during a crisis, in Theories of Surplus Value, and traces it to the simultaneous need/inability of commodities to transform themselves into money, to realize the exchange value.

IIRC Marx even describes this as a false conflict or something like that.

Michael Roberts,

I have been following your posts which have helped me better understand the current falling rate of profit. I am a retired Physicist/Electronic Engineer who spent much of my career working in the field of automation. I think that the current infusion of Artificial Intelligence into automation will send Capitalist profitability even lower, approaching zero. Every manufacturing job is repetitive, and it is repetitive jobs that can most easily be automated. Humans would then be freed to do any creative activity that they want. I believe it will be possible to automate most white collar office jobs and as well as most jobs in the service sector. I am working on a new book which puts forth a possible solution to Capitalist’s problems. I propose to abolish it and abolish money along with it. After thinking about this for many years, I came to the conclusion that money must be abolished to solve this profitability problem by abolishing the very notion of profit. It would also put an end to all the wars with which we are currently threatened. So, how to construct an economic system without money.? By the way, I don’t mean no money in the sense that now we will all just credit cards or some other kind of plastic, or possibly doles from the government. In my opinion, we must move to a system based on need. All production and service activitiy would be carried out by modest sized self-organizing groups of people with common interests. Each group should operate with total democracy which must include immediate recall of elected leaders. You can see I got these ideas from Marx and the Paris Commune. But Marx did not, and could not have, laid out the details of how a Needs-Based economic system could be constructed. So we have to figure that our for ourselves. I call these groups Enterprises because I believe if we did this, we would see a flourishing of entreprenuerial spirit. People would be doing what they want to do, where they see a perceived need. Each Enterprise maintains a request queue. When you want something, you simply request it. The length of the queue represents demand. There are no patents, all information is open including manufacturing recipes.

At first we may have to establish need as a basis for fullfilling an order. We will have to deal with many problems including how to handle short term shortages and unpleasant jobs that have not yet been automated. Many industries will no longer be needed at all, making for more useful application of the resources that they were consuming. If you have a new idea, you can ask for enough material to develop a prototype, which may or may not result in demand as evidenced by the length of your request queue. This is to be a classless society, the members of an Enterprise do not really own the means of production. They are using what they have for the purpose of fulling the needs of themselves and others. In my view, personal property would still exist as if you get your house built and you occupy it, no one can come and take it away from you.

At first one might thinnk that I have fallen victim to some kind of ‘left-wing’ communism (ala Lenin’s description!). Maybe. But so what. The important thing here is to recognize that this is not a repetition of the Bolsheviks unsuccessful attempt. The Bolsheviks may very wall have been well intentioned, but they came to power through an insurrection. This put them in a position of minority control. Thiis lead to a very centralized dictatorial control. The lesson here is that you can NOT pull off a transition to a real Needs based system with an insurrection. It will require a very long campaign and must eventually win the support and activie participation of the vast majority of the world’s people. In my opinion, we do not want bloodshed if we can avoid it. All we want is for the worlds Capitalist Rulers to stand down, which if they do, no harm should come to them. To institute this new system, we should organize campaingns that advance our cause and bring us together. Thus fights again Racism, Sexism, Nationalism, etc. will become paramount. We might also put some effort into rebuilding a rank and file union movement.

What I have written here is sort of an abstract of the new book on which I am working. Would it be possible for me to send you an early draft (as a pdf) so that I could get the benefit of your ( and perhaps your students or associates) critical comments? I assure you that I would take them seriously and perhaps change the book accordingly. This book is a big task, and I need help to get it right, and I am not at all sure that I have everything right. You could put excepts from it into your blog if you like. Any critical comments that I get will be very helpful.

As an aside, I travel to Europe from time to time. If I were to come to London, would it be possible for me to meet you for whatever time you can spare?

Best Regards,

Alan Strelzoff Boston, USA

On Tue, Nov 27, 2018 at 9:56 AM Michael Roberts Blog wrote:

> michael roberts posted: “Financialisation, like neoliberalism, is the buzz > word among leftists and heterodox economists. It dominates leftist > academic conferences and circles as the theme that supposedly explains > crises, as well as a cause of rising inequality in modern capitali” >

Ill send you a message

Heres a NBER paper showing we have had jobless recoveries since the 90s, with financialization providing plenty of opportunity to lay off on the downturn and replace with automation.

Click to access w18334.pdf

“In the last 25 to 30 years the US labor market has been characterized by job polarization and jobless recoveries. In this paper we demonstrate how these are related. We first show that the loss of middle-skill, routine employment is concentrated in economic downturns. Second, we show that job polarization accounts for jobless recoveries. This is based on the fact that almost all of the contraction in aggregate employment during recessions can be attributed to job losses in routine occupations (that account for a substantial fraction of total employment), and that jobless recoveries are observed only in these disappearing jobs since polarization began.”

If I’m not mistaken, it was in Japan where one law office adopted an AI to get rid of all the “trainee” functions, thus effectively automizing a lawyer’s job.

Reblogged this on Stavros Mavroudeas Blog and commented:

This is a very good post by Michael Roberts that criticizes accurately the current superficial trend of the financialisation theories. It is also bringing forth some interesting points from Mino Carchedi’s work.

Great article!

Here translated into German.

The surplus of society which is owned by the capitalist class can be either invested, or consumed or speculated with. What determines these flows can only be the rate of profit. Michael is quite right to begin with this observation. The recent turbulence in the markets was quite clear, concerns over future profits now the Trump adrenaline tax rush is ending. Theorists who pooh pooh profits always get run over by a change in the markets.

It is important to divide fictitious capital into its two departments: primary and secondary because there effects are different. Primary is the direct claims on future streams of surplus value namely, shares, bonds and property. Investments here are driven by bets on the direction of these streams, up or down. Secondary is often called derivatives and they are the bets on bets, in other words bets on the movement of the “prices” of shares, bonds and property. (We ignore currencies.) Now it is important to note that secondary fictitious capital does not have a claim on future streams of surplus value. It only profits from the rise in the prices of bonds, shares and property. But it does negatively effect the actual owners of primary paper. Generally secondary speculation drives up the price of shares and bonds in particular. This means that the holders of these bonds have a lower annual return for their investment. For example if our starting point is a price to earning ratio (P/E) of 15, it means shareholders receive a return of 6.67% p.a. when all profits are converted into dividends. However, if due to secondary speculation, the P/E goes up to 20, ie the valuation is stretched, the return falls from 6.67% to 5%. This is important for investors like pension funds. What the secondary speculators gain in “capital appreciation”, primary speculators lose in terms of return. This is one of the reasons that returns have been so low over the last 30 years. Finally, because secondary speculation stretches valuations, it helps intensify crashes when profits turn down and asset classes on which this speculation is based turn down.

Pension funds, mutual funds, and other institutional investors calculate TOTAL return, not just dividend rates, or interest rates. So if the stock appreciates in nominal value because the price rises, that becomes part of the total return and always outweighs the decline in dividend rates. If someone buys Exxon at 60, with a yield of 4%, and the stock appreciates to 100 with a yield 2.4%, nobody’s going to complain about losing yield. No institutional investors buys stock expecting the total return to be confined to the dividend rate. Too much risk in an equity play for that.

Similarly, with bonds, when interest rates declone, the appreciation in nominal value in the secondary market offsets the decline in interest rate and will yield a better total return IF you bought in at the right time and sell out at the right time. In fact total return in the bond markets from, I think, 1986 to 2015 was an extraordinary time for bond markets where total return was unusually high based on the decline in interest rates. “Original holders”– actually purchasers in secondary markets– did just fine with the declining rates as the trading value of their bonds appreciated to offset the decline in interest rates.

These are trading instruments. Timing is everything.

As for “secondary speculation” like derivates– options, futures, and the more speculative credit default swaps– these have two parties and two sides to every transaction. So the appreciation of value of the underlying paper helps one side. Likewise the depreciation of the stock, or the raising of interest rates helps the other. It’s a zero sum game, which doesn’t mean you can’t make money off it.

You will remember that during the 2008-09 crash, everybody was worried about the enormous sums represented in the nominal values of credit default swaps, which “values” were far far greater than that of the underlying assets, and how the CDSs represented the real threat to the system. Turned out not to be so, as about 95% of the credit default swaps were hedged on both sides, and cancelled each other out.

I do not disagree about double sided hedging. I have remarked a number of times that the BIS gives net and gross figures for derivatives. Their latest research can be found on https://www.bis.org/statistics/d5_1.pdf which shows gross derivatives at $595 trillion and net at only $10.3 trillion or one third the value of US share markets. I also agree that pension funds etc calculate capital gains as well as income as their income. However, the point must be made, that while they gain on previous investments in terms of capital gains simultaneously they lose on current and future investments because now it requires a larger investment to get the same return. Hence their income has to be investigated in the round and not in the here and now. I do not intend to examine the data but I expect that this loss of return in the long run cancels out, or more than cancels out, their capital gains over the same period.

There really isn’t any categorial difference between what you call the primary and secondary departments of fictitious capital: it’s just a symptom the financial market became big and more complex in its superstructure.

VK primary and secondary tier are different. Secondary does not have a claim on future streams of income (surplus value). That is where all the confusion comes in, including the view that the stream of income is infinite. It is a finite stream. The pool of unpaid labour is finite. These secondary tier instruments are pure leverage. Their gains arise only from the rise in the “price” of primary paper. But this rise is paid for by reduced annual returns in the future. In other words it now takes more dollars to secure a dollar of income.

You can divide a category in as many subsets as you want: it is still one category. You’re just adding complexity to the system, not creating a new one.

Michael, I’m afraid you don’t understand ‘financialization’ and are setting up straw men definitions in order to provide a refutation. Quoting mainstream economists, who have virtually no understanding of financial cycles and how they interact with real cycles, is like quoting the blind in order to get directions to the next town.

Here’s my comment to your post, which I recently provided to another blog that reposted your above piece:

“There are many definitions of ‘financialization’ and most are absurdly simplistic–like share of profits going to FIRE (finance, insurance, real estate) sectors or share of total employment, etc. But to critique these ‘straw men’ does not deny that financial asset markets, financial instability, financial cycles, and financial (banking, shadow banking, capital markets, etc.) crises and crashes have no negative impact on the real economy and short term business cycle crises like recessions and depressions.

It is absurd to argue that financial instability is the sole cause of financial and real crises. But it is no less absurd to argue they have no effect and are just a reflection of real variables, especially the falling rate of profit concept (which by the way Marx never felt convinced of enough to publish it, but only wrote about it in his unpublished notes).

The FROP thesis, at least Marx’s version, argues that only profits from the production of real goods made by productive labor is the cause of capitalist crises. That leaves out all forms of instability from profits generated by non-productive labor, or from profits generated from financial asset speculation, and any consideration of the interaction of financial cycles with real business cycles as causes of short term capitalist crises like recessions and depressions.

A case may also be made that Marx’s FROP idea related to the long term crisis of capital and was never intended to explain short term crises like recessions-depressions. In short, to debunk simplistic explanations of ‘financialization’ and substitute that with FROP arguments is to substitute simplicity for another form of it.

There is little doubt that late 20th century capitalism has evolved into a form where financial assets and markets are playing a growing role in destabilizing the system. To ignore that and simply revert back to mid-19th century analyses of another form of capitalism emphasizing industrial production by productive labor only (a concept of Smith and Ricardo by the way) is to bury one’s head in a deficient conceptual framework of economic analysis that cannot explain 21st century capitalism.

My definition of ‘financialization’ recognizes the rise and growing economic and political influence of a new global finance capital elite, with a new institutional framework (shadow banking system), creating new financial products, in highly liquid financial asset markets. Their financial profits are greater on average than industrial capital (making goods with productive labor), and they are sucking out money capital from the latter and redirecting it to their asset markets. Why? Because financial asset markets and profits from financial speculation are simply greater than from traditional goods production on the average. (For example, there’s no cost of goods, no distribution cost, easier exit from markets when prices soften or fall, etc. ) Financial asset investment is crowding out goods profits because over the long run it is more profitable.

But contemporary Marxists refuse to acknowledge or give any influence to financial profits. They are labeled simply ‘fictitious capital’, and considered irrelevant to the circulation of capital as a whole. Yes, it’s fictitious, but that doesn’t mean they’re not destabilizing to the system itself, or can disrupt or distort the destroy productive capital in the circulation of capitalist production as a whole.

Exploitation of productive labor (that drives the FROP per marx) plays a role still in global capital. In fact, the exploitation has been increasing. But overlaid on it is profits from financial speculation. Marxists should be looking at how the two mutually determine each other. How financial markets and cycles interact with real goods markets and cycles. (They should be more dialectical in other words) and not just write off financial instability (aka financialization) and argue based on Marx’s unpublished work that only production of real goods by productive labor defines profits and that the rate of change of that determines all short term crises like recessions and depressions.

By the way, Marx has no theory of business cycles and therefore short term crises. Like other classical economists before him, he was a long term supply sider that was focused on the long term ‘breakdown’ crisis of capitalism. Classical economists before him were inept on short term crisis and business cycle analysis. So if contemporary Marxists want to understand why financial crises and recessions-depressions are now occurring more frequently, they should add some new tools beside FROP to their analysis. And that includes better understanding the dialectical relationships between financial cycles and real cycles in 21st century capitalism.

By focusing on FROP as the cause of short term business cycles, Marxists ignore what’s happening in the circulation of capital after value is created and before it is recommitted to real goods production once again. And by focusing primarily on the production process to explain exploitation, they are ignored one of the major trends of the 21st century late capitalist system: namely, the increasing extraction of surplus value on a state to state level in the form of debt interest payments. The capitalist state is increasingly become the bill collector for finance capitalism. That’s what austerity policies in the Euro periphery have been about. That’s what the Greek debt crisis was about. That’s what the Italian vs. Brussels fight is about. That’s what US capital extraction of value from Latin American has been about, and all dollarization of corporate and sovereign debt today is about.

If you don’t understand how finance capital today has become more dominant (and I don’t mean in the way that Hilferding-Lenin talked about a century ago), then you cannot understand how the capitalist system functions in the 21st century–far more exploitative than ever before. And not just in the exploitation of productive labor and the point of production that Marx described (accurately I might add), but in financial forms of exploitation as well. But you won’t understand that by critiquing arguments of mainstream bourgeois economists, whose conceptual framework of economic analysis is incapable of explaining capitalist exploitation–just as Marx’s original framework is no longer sufficient to explain it today.

Jack Rasmus

Have you noted that, contrary to Marxism, Classical Liberalism (Political Economy), the Austrian School, the Physiocrats etc. etc. — neoclassical theory doesn’t have “a name”? They just have that amorphous, semi-anonymous, mass produced horde of (mainly) overpaid Ph.D.s that, on its part, produces tons and tons of articles in tons and tons of “peer reviewed” publications.

It’s like they want to make it appear as if neoclassical “theory” is natural, spontaneously born.

Well, from where I come, this is called “safety by numbers” (the crowd effect): you can’t criticize neoclassical economics because you have nobody who responds for it.

Agree completely.

And I take note of your that the “FROP thesis, at least Marx’s version, argues that only profits from the production of real goods made by productive labor is the cause of capitalist crises.”

No, it isn’t and can’t possibly be that only profits from the production of real goods make for recessions and depressions. Anything that interrupts the circuits of ‘payments’ or the flow of ‘credits’ kills economic expansion and thus triggers system wide contractions.

And to the degree that ‘money’ represents ‘real’ claims over goods and services, as well as over property, those who control the many and complex spigots of its issuance in the form of debt can and effectively do dominate the process of capital accumulation, are able to leverage the process of ‘capitalist expropriation,’ of ‘exploitation,’ in their favor.

“The FROP thesis, at least Marx’s version, argues that only profits from the production of real goods made by productive labor is the cause of capitalist crises. That leaves out all forms of instability from profits generated by non-productive labor, or from profits generated from financial asset speculation, and any consideration of the interaction of financial cycles with real business cycles as causes of short term capitalist crises like recessions and depressions.”

1. Just not so. Marx identifies numerous reasons, sources, causes for capitalist crises, including overproduction, the separation of production from consumption, disproportionality, and most importantly, the enforced poverty of the population.

“A case may also be made that Marx’s FROP idea related to the long term crisis of capital and was never intended to explain short term crises like recessions-depressions. In short, to debunk simplistic explanations of ‘financialization’ and substitute that with FROP arguments is to substitute simplicity for another form of it.”

2. Yes a case can be made for that. Marx also makes the case that the FROP triggers disturbances, eruptions, breakdowns in accumulation in the short-term. As for your other assertion, it’s not simplistic to trace the explanation for the disruption to the FROP, if in fact you actually trace it back to the FROP. Whether you agree or disagree with Michael, he has done that. He is not simply making the assertion and leaving out there without providing the background data and analysis.

” There is little doubt that late 20th century capitalism has evolved into a form where financial assets and markets are playing a growing role in destabilizing the system. To ignore that and simply revert back to mid-19th century analyses of another form of capitalism emphasizing industrial production by productive labor only (a concept of Smith and Ricardo by the way) is to bury one’s head in a deficient conceptual framework of economic analysis that cannot explain 21st century capitalism.”

3. Can you identify the critical point of transition, when the destabilizing impact of financial flows, from financial profits overtakes the not just the mid-19th century analyses, but the actual dynamics of capital accumulation and crisis themselves?

“But contemporary Marxists refuse to acknowledge or give any influence to financial profits. They are labeled simply ‘fictitious capital’, and considered irrelevant to the circulation of capital as a whole. Yes, it’s fictitious, but that doesn’t mean they’re not destabilizing to the system itself, or can disrupt or distort the destroy productive capital in the circulation of capitalist production as a whole.”

4. No one that I know of,or read, has suggested financial flows are not destabilizing, or cannot destroy productive capital. Happens all the time and all over the place. Systemically, however, the critical conflict is between the forces of production, the growth of those forces, and the relations of production, the property relations derived from the specific organization of labor that circumscribes those forces of production.

“Exploitation of productive labor (that drives the FROP per marx) plays a role still in global capital. In fact, the exploitation has been increasing. But overlaid on it is profits from financial speculation. Marxists should be looking at how the two mutually determine each other. How financial markets and cycles interact with real goods markets and cycles. (They should be more dialectical in other words) and not just write off financial instability (aka financialization) and argue based on Marx’s unpublished work that only production of real goods by productive labor defines profits and that the rate of change of that determines all short term crises like recessions and depressions.”

5. And exactly who DOESN’T do that? When we write about Greece are we leaving out the role of the Troika, the actions of the ECB maintaining support for Greek banks so that the bourgeoisie can move their capital out? When we analyze the 2007-2009 and beyond recession, have we ignored the role of investment banks, the use of asset backed securities, the leveraging, etc etc etc? Talk about strawmen……

“By the way, Marx has no theory of business cycles and therefore short term crises.”

6. Nonsense. That’s all that can be said in response. Nonsense. See Maksakovsky’s The Capitalist Cycle, derived from Marx’s writings on this subject.

” That’s what the Greek debt crisis was about. That’s what the Italian vs. Brussels fight is about.”

7. Here you do exactly what you accuse the FROP theorists of doing, reducing and substituting a simplistic explanation for a different “simplistic” explanation. If you think the Greece crisis was a debt crisis, that the debt issue was not the result of the economic structure of capitalism in Greece, was not rooted in the attempt to overcome the inability of Greek capitalism to sustain industry, was not rooted in the history of the development of capitalism in Greece, with those deep structural impairments producing the accumulation of debt, you simply haven’t done enough investigation.

“If you don’t understand how finance capital today has become more dominant (and I don’t mean in the way that Hilferding-Lenin talked about a century ago), then you cannot understand how the capitalist system functions in the 21st century–far more exploitative than ever before. And not just in the exploitation of productive labor and the point of production that Marx described (accurately I might add), but in financial forms of exploitation as well. But you won’t understand that by critiquing arguments of mainstream bourgeois economists, whose conceptual framework of economic analysis is incapable of explaining capitalist exploitation–just as Marx’s original framework is no longer sufficient to explain it today.”

8. The issue is, is capitalism still a value producing economy. If so, what then produces value? If so, do the very terms of the production of value undermine the accumulation of capital? If finance is producing value, not simply distributing value, not simply stealing or looting or sharing in value, you need to show us the source and the circuit of that financially produced value. .

Yes, financialization took off from early 1980s. This is a decade after the degradation of standard labor began its long decline; in the U.S., median real earnings peaked in 1973. Obviously, financialization cannot be the cause of something that began before its notable rise. And sometimes it helps to look at basic facts directly rather than through the periscope of cycles and crises.

It seems the Fed capitulated:

In dramatic about-face, Fed signals rate hikes almost over

The link didn’t appear? Here it is:

http://www.atimes.com/article/fed-chair-suggests-rate-hikes-almost-over-buy-emerging-markets/

Imagine a society in which there are just two classes, landlords and free workers. The landlords, a minority, own all the land, the workers have to pay rent and get their income by working for the landlords. Land can’t be bought or sold, it passes through the generations by inheritance. So there is no profit to be made by the landlord class. They just own and consume their income. Since they employ every worker through their consumption, there is most of the time no unemployment.

With one exception. All landlords are also art collectors. They buy and sell art trying to have the biggest and most valuable collection. The stock of art is fixed, all artists are long dead. But art tastes are changing. If you are heavily invested in abstract expressionism, sometimes you are at the top of the art world, sometimes you loose. As long as somebody else wins, the aggregate worth of all art stays the same, since in aggregate all landlords use 30% of their income on art speculation and income in aggregate is constant. Since the consumptions decisions of the landlords are influenced by the worth of their art collection, they spend less money if their collection’s worth decreases. Since normally somebody else collection goes up in value, aggregate consumption stays constant and all workers are employed. Only sometimes all landlords loose faith in art all together. In that case everyone starts hoarding money and unemployment rises.

To solve this problem a bunch of technocrats called Keynesians invented an institution, called central bank. They just print money and buy enough art, till the faith in art starts rising again. Because of the central bank the value of art can always be pushed up. The landlords feel rich again, start consuming and the workers are all back in employment. End of story.

In this toy model of a society, we have rents, we have fictitious capital but no profit in the marxist sense. The falling rate of profit has come to an end, it is zero now. Nevertheless the society can function with full employment in all eternity. They still have recession, but these can always be solved by the central bank.

Isn’t it precisely because in this toy model all capital is fictitious that the Keynesian solution works? Why do Marxists think that debts or money printing has to become unsustainable? If money printing is used to push up fictitious capital, things never have to change. Real profit can’t be raised by money printing, but fictitious profits can.

Here is the classic Keynesian/MMT narrative – Krugman uses baby coops instead of art. Over to everybody

Krugman’s model doesn’t have capital goods, just consumptions goods (babysitting) and money (scrips), but you are right that my point is a Keynesian one.

But isn’t it a problem for Marxists that Marx always worked with the assumption that money is backed by gold which is worth the social necessary labour time to produce it? Today money can be produced with no labour input whatsoever.

How can there be unemployment, if workers have control over the printing press? In my model, unemployment could arise if even massive art buying of the central bank, doesn’t convince the landlords to consume more. They could decide to just sit on the newly printed money.

But this doesn’t help the Marxists. My landlords are rentiers, not capitalists. Imagine a society with no rent (no land, no monopolies, no networks, no patents…), how could capitalists in such a rent-less society stop production? They can only base their power on two kinds of capital goods, money capital and real capital. If money capital can be produced by the workers themselves, through democratic control of the central bank, why should ownership of real capital allow capitalists to create unemployment? Real capital can be produced by workers (in contrast to land). A capitalist who decides to go into a capital strike, would just lose market share, workers could join to produce the capital goods they need themselves.

In a world without land (resources with fixed supply) ownership of real capital alone wouldn’t give capitalists any power. They need control of the money supply, hoarding of money is essential for Marx’ model of crisis to work. The moment workers have control over the money supply, any profit crisis can be solved through the devaluation of capital by simply devaluing money capital. No unemployment or destruction of real capital is necessary. The economy would become crisis free.

@ Alex

No, the value theory is still valid, with or without fiat currency. That’s why inflation (or deflation) is considered a problem to begin with.

Marx lived in an era of the gold standard. But in Kapital I, his aim is just to demonstrate the origin of money. And he demonstrates that, whatever its form, it comes from commodity, which presupposes value.

Rent and money and paintings must have been created by the Great Landlord in the Sky, since no one seemed to work at anything but paying rent and buying and trading pictures. It works though…

“Imagine a society in which there are just two classes, landlords and free workers. The landlords, a minority, own all the land, the workers have to pay rent and get their income by working for the landlords. Land can’t be bought or sold, it passes through the generations by inheritance. So there is no profit to be made by the landlord class. They just own and consume their income. Since they employ every worker through their consumption, there is most of the time no unemployment.”

We don’t have to imagine: this kind of society really existed, in medieval Europe. The system is called manorialism.

In such society, obviously there is no money (there was money in really existing manorialism, but that’s because commerce still existed in the main coastal cities, the Chinese and Mongol Empires, Constantinople, the Caliphates and North Africa): the peasants who worked in the communal lands had to pay tax in produce, and/or in labor time in the noble’s land.

Kingdoms were kind of self-sufficient and there was no concept of inflation (which plagued the late Roman Empire) because there was no money.

Specialized labor were confined to guilds, which behaved almost like secret cults and were only accessible to the nobility and the Church.

Accumulation of wealth, as well as technological innovations in production not directly related to agriculture, as Marx had already noted, was accidental. And when such kind of accumulation happened, it was all spent on extravagancies, like treasures and buldings.

So, this “hypothetical society” is utopian: there would be no art market as we know it today (art then was also a form of treasury, its value measured on the precious materials used to fabricate it — that’s why, e.g. a painting with too much blue in it was a sign of status).

The art market only became “financial” (conceptual) in the post-war period (1945-), and even then, it took some decades to gain its contemporary form (probably sometime in the 80s — the record settling van Gogh painting to a Japanese bank generally being used as a marker).

I only have one question (channeling Vasquez in Aliens):

How do you have “free workers” working for landlords?

“Free workers” are workers producing commodities for exchange, exchange values for a market, not use-values for the lord of the manor.

If commodities are being produced then your fictionalized “closed economy” is burst apart by the need to exchange these values and realize profit, and we are right back on the road to the falling rate of profit.

Your story is fiction. There’s a difference between abstraction and fictionalization.

“How do you have “free workers” working for landlords?”

Good ol’ brute (“lethal”) force: the medieval European nobility came from the barbarian warlords that arose after the collapse of the Roman Empire in the West.

That didn’t produce “free workers.” It produced serfs (and slaves).

“Imagine a society in which there are just two classes, landlords and free workers.”

If there are just two classes, how do we get technocrats? And bankers? How do we get bankers if there are just two classes?

And a central bank? What would be the need for the central bank? If “free workers” are producing for landlords, and paying rent, whether in kind or in gold or gold equivalent, what would possess an atomized, fragmented society like this to produce a central bank, and accept its paper as money?.

So summing, we have only two classes, but magically, two other classes appear. We have a central bank, that organ of modern capitalism, which suddenly appears to paper over the unevenness in our primitive economy as if it were whisked back to that primitive stage by some tear in the space-time continuum; and we have our landlords accepting the paper blindly, as if it represented an embodiment of value when according to the original class terms of the mode of production, exchange value is not being produced; aggrandizing surplus value is not the point of production, and profit is irrelevant;

Seriously? And you want to know why Marxists think that simply printing money is unsustainable? Because the world you describe is a mash-up of impossibilities.

A reply to ‘Anti-Capital’: I won’t reply point to point you make. But to your 1., reread Marx. FROP applies only to profitability from the production of goods by productive labor. 8. Maksakovsky is not Marx. Maksakovsky attempts to extend Marx, but his views were buried and only recently resurrected in English. Contemporary Anglo-American Marxists at not Maksakovskyans. They adhere to Marx’s FROP. Also, sorry, there’s no short term application of FROP to explain recessions in Marx. Finally, the problem is contemporary Marxists of UK-US (a wing of each) argue that financial instability is a product of real profit rate decline. It is thus determined by, not mutually determinative of, financial asset value collapse. Look, you and other marxists need to stop arguing abstractly from first principles. You’re arguing like Ricardians. Use the marxist method and start quantifying how financial asset instability provokes crises in real production of profits (and therefore FROP)–not just how the latter may determine the former. These debates how so much metaphysical exercises. What Marx meant by this and that or whatever. Stop talking marxism and ‘do’ some marxist method analysis of 21st century capital.

Jack,

You initiated a “metaphysical debate.” Michael wrote an article and concretely showed a) the limits to the “financialization” explanation as the cause for capitalism’s “troubles” b) the vitality of the FROP thesis as an explanation for the same. You intervened with a purely speculative (appropriately enough) argument that said Michael didn’t understand that finance, today, somehow has gained a magical power to replace, if not produce, value..

You did not show concretely, in any manner, how that power of finance actually operates..

You did fault Michael for, of all things, criticizing the explanation and definition of financialization as provided by “mainstream economists,” which is pretty hilarious since that’s exactly the method Marx used, criticizing mainstream economists, and I don’t know of anyone using the term “financialization” that doesn’t mean it the way “mainstream economists” mean it.

As for being concrete, I’d simply point to your inadequate and totally superficial explanation for the causes of the crisis in Greece, and Italy, as opposed to…..well, one that looks at the material conditions of production, forces and relations. I’ve taken a few stabs at that, regarding Greece, and the reader can decide for yourself, who is using debt, or Marx, as a metaphysical argument. https://thewolfatthedoor.blogspot.com/2015/05/prospects-and-results.html

Leaving aside the difficulties in estimating the Marxian rate of profit from capitalist statistics that Jack himself, Boffy and others have raised, I wonder if a great deal of confusion does not arise from how we conceptualise the FROP? Following the exposition of J S Mill in his ”Essays on Some Unsettled Questions of Political Economy” of 1844 (Pp 108-109 of The Kessinger reprint), which Marx asserts contains all that is original in Mill, along with others I understand the FROP analogously to gravity. If then we were to claim a plane crashed because of gravity, clearly that would make no sense, as the fact of the plane’s being on the ground or taking off in the first place would then also be ’caused’ by gravity. The point is that if a strong gust of wind dislodges the apple from the tree, the apple always falls downwards.

So I understand the FROP to be a pressure that is continually exerted on capitalism but whose manifestations only appear at at lengthy intervals.

I would argue then that it is something of a chimera to be always pursuing a falling rate of profit as evidence of Marx’s theory. The FROP triggers countervailing measures that will raise the rate of profit, and a rising rate of profit is no refutation of Marx’s theory; quite the contrary!

Dr. Rasmus advises, “Start quantifying how financial asset instability provokes crises in real production of profits.” Would not the capitalist class want to eliminate such instability? They haven’t yet. Assuming that you are not coming to their rescue, there must be a reason why such instability is inevitable. Would you like to add that reason to the reason that the rate of profit must fall?

My story about rentiers speculating in art markets was meant as a satirical exaggeration. But central banks printing money to get employment up through the wealth effect, is no satire, that’s the reality we live in. My question remains, why can’t this go on? Why not have a financial panic>unemployment>central banks do quantitive easing>wealth effect sets in>gdp goes up again>unemployment shrinks>financial panic>central banks do quantitative easing>… cycle forever? We can run out of oil or phosphor, but how can we run out out fictitious capital?

And why couldn’t we use this money creation for something productive? Shouldn’t we have democratic control of the money supply? But the deeper theoretical question that interests me: is according to Marx the power to exploit workers based on real or money capital? In classical economics (Smith, Ricardo) there is no profit in the long run, that’s why I always understood Marx as someone who wanted to give an explanation why profit exists in the real world. Now, a classical or neoclassical economist explains profits by market power (it’s all about monopolies, rent-seeking, some capitalists own goods, which nobody else can supply). Marx doesn’t do that. His whole falling rate of profit tendency is based on competition between capitalists. So how can there be competition and profits, when classical economists say this can’t be? Marx’ answer: through exploitation. Workers don’t get the full value of what they produce. But why is the bargaining power of workers so weak? Because of chronicle unemployment, the reserve army of labour. For Marx labour markets are never in equilibrium. But why are they not in equilibrium? I think the answers is: private ownership of money capital. Workers can produce real capital, but they can’t produce money. (Private ownership of resources in fixed supply like land is also a very important source of powers against workers, but this insight is not specific to Marx). Owners of money capital will never create full employment since their profits are based on the superior bargaining power they get through the threat of unemployment.

What I don’t understand is why do Marxists think ownership of real capital(that’s goods that can be produced by labour) is enough to exploit workers? Ownership of resources in fixed supply, I get, money capital, I get, but real capital alone can’t be a source of power for capitalists. Assume we have a full employment monetary policy and a competitive market, then owners of real capital will have in the long run a return identical to the rate of interest (and a compensation for risk). The risk free rate of interest could well be negative. Real yields on 5year US treasuries from 2010 to 2017 were very often negative. German bonds even had negative nominal rates.

What I’m saying here is not really in contradiction to Marx. I just emphasize that private ownership of money capital is essential for exploitation of workers. Capitalism can’t exist if the money supply gets socialized. In Marx’ time gold prohibited this, today monetary policy like in the Eurozone is just as good as gold. And everywhere monetary policy is foremost done to serve the creators of fictitious capital with employment and production of use value as a side effect.

Capital is the social power of the capitalist class, the state is there political power. What you are suggesting is that the capitalist state competes with the capitalist class in terms of lending policy etc. This means the pool of surplus value will now be shared between the two and it will represent a loss to the capitalist class. Won’t happen.

It’s interesting that jackrasmus and Alex come together in arguing for the primacy of money (for Marx, the fetishistic store of a fictitious value: exchange value)–as a determining factor in capitalism’s instability.

Alex puts it this way: “What I’m saying here is not really a contradiction to Marx”. [It’s curious that both these Keynesians wish to establish their fictitious marxist bonafides.] “I just emphasize that private ownership of money is essential for exploitation of workers…”

jackrasmus puts it this way: “Look you and other marxists need to stop arguing abstractly from principles”… and “start quantifying” (how financial and productive capital interact if we’re are to understand how modern capitalism really works. In other words, numbers are not a mere reflection of matter in motion, but “real” (material) substance in themselves when manifested in financial instruments. jackrasmus seems to want to bring Marx up to date–good enough, but all he seems to accomplish is a confusing transubstantiation of himself into a spruced up, financialized caricature of Marx.

Both Keynesians pretend to know Marx, but emphatically ignore Marx’s concrete, dynamic, historically verifiable, fundamental definition of capital as a Social Relation between an evolving population of laborers within nations (eventually a majority population and on a global scale) who must work for wages in order to live, and the class of capitalists who came to own the means of production and to control the states that guarantee their ownership.

It is this historically evolved (maturing only by the end of the 19th century) social relation that Marx defines as the “capital” of capitalism. Political economy’s numbers game and illusory free market is critiqued in Capital as only fictitious reflections of this social relation, not vice versa. Surplus value and his labor theory of value are capital-specific products of this critique, and the antithesis of political economy.

Understanding the ramifications of capital as a social relation requires more than a cursory review of the first volume of Capital. It doesn’t even require that. It requires some literacy and an egalitarian human sympathy. Then you can learn a lot from Marx.

Modern capitalism evolved out of a privately owned mode of production within the merchant capitalist/colonial system. Eventually capitalists found themselves within a social system of their own inadvertent creation in which a large section of the population–soon to become the overwhelming majority consisted of potential wage earners and their families, most of whom could not be employed for profit. By mid-19th century, the contradictions, both with the capitalist mode of production and between it and the burdensome social order that evolved along with its own evolution, resulted in a secular tendency for the rate of profit to fall. The rest is the barbaric history of financially directed imperial attempts to counter that tendency.

The financially expressed value of the the products embodying the value of either “productive” or “unproductive labor” are equally fictions in the sense that those values are not the human activities (or the products) themselves, but monetary expressions of the activities of alienated labor and its products as forms of capital (labor power and commodities), which, in turn, can only appear within capital’s historically evolved social relation.

Printing money, fiat or golden, “democratically” distributed or hoarded in banks, as measures to perpetuate capital’s barbaric social relation can only result in just that.

What Alex advocates is not derived so much from Keynes as it is derived from Proudhon “What we need is capital without capitalists,” sounds a lot like what we need is public banks, or money without financiers, interest, etc. doesn’t it?

Alex writes:” But why is the bargaining power of workers so weak? Because of chronicle unemployment, the reserve army of labour. For Marx labour markets are never in equilibrium. But why are they not in equilibrium? I think the answers is: private ownership of money capital. Workers can produce real capital, but they can’t produce money. (Private ownership of resources in fixed supply like land is also a very important source of powers against workers, but this insight is not specific to Marx). Owners of money capital will never create full employment since their profits are based on the superior bargaining power they get through the threat of unemployment.”

Why is the bargaining power of workers so weak? First answer, the struggle is NOT about bargaining power. Like everything else in capitalism, workers’ bargaining power has both cyclical and structural elements. Cyclically, even minor improvements in workers’ “positions” augments the power of capital, and increases its ability to reverse those momentary gains when the economy goes pear-shaped.

Structurally, the bourgeoisie have waged an offensive for the last 40 years to decertify labor unions, break workers organizatons, dismantle and disperse factories in the “advanced” countries, ship capital to areas of greater working class weakness AND greater capitalist repression. This is not a struggle for bargaining power in the capitalist system. This is class war, and as the bourgeoisie themselves admit, they’ve been winning for years, and handily.

That the bourgeoisie “own” money capital is only a reflection of the fact that they own the means of production, just as money is the reflection of the labor-time embodied in the commodity. You cannot do away with “private ownership” of money-capital while leaving intact the economic power, the force of compulsion that the bourgeoisie exert through the private ownership of the means of production.

As for value, it is still there because we are there producing wealth and natural resources are there waiting to be owned and sold. It’s just that price is not conforming to value and that is why bubbles occur and burst and markets fall. What happened when the dollar was pegged to gold before 1971 was that the value of gold (the socially necessary labour time embodied in the ounce of gold) was greater than its price in dollars. Many, many dollars had to be printed up as government bonds in order to finance the Vietnam War, the Cold War and the revenue lost by reducing company taxes over the years.

When the Saudis called the bluff and demanded to be paid in gold, Nixon closed the gold window and the floated the dollar in the marketplace of commodities and bang–it took many more dollars to buy an ounce of gold than when the dollar was pegged to the absurd price of $36 to an ounce of gold–it also took many more dollars to buy a gallon of gasoline and all the other commodities in the market.

Value is always operating within the social relation of Capital and money represents its price. To ignore the law of value is, in a capitalist system, to invite bubbles, crises and crashes. You see, the market is us and we have our own perceptions of use-value tied to exchange-value. We start seeing that the price of the money we have in our accounts has been inflated with fictitious value (mostly through buying and selling in the FIRE sector) and we’d better find something of real value to own or else watch our accumulated capital go up in smoke along with the mirrors which tricked us as the whole outhouse goes up in flames. Fear eats into the animal spirits and the stampede begins and where it ends, nobody knows, because nobody thought beyond dear TINA to what Marx and Engels proposed–a change in the way we produce and distribute wealth.

So, what we need to do is to emancipate ourselves from the wage system and establish common ownership and democratic control of the collective product of our labour so that we can produce goods and services for use and distribute them on the basis of need.

I agree, that capital is not a thing, but a social relation, this is precisely my point. Marx famous passage on Wakefield shows that ownership of capital means nothing if you still have enough fertile land and the workers are skilled enough to become farmers (and ready to kill the indigenous population). This passage shows that little things matter. Just by having access to enough fertile land you could stop capitalism (in the 19th century, in Australia).

I think the same must be said about democratic control of the money supply. It destroys the social relations which is capitalism.

First, in Marx it all starts with money capital (M-C-M’), capitalism is all about owners of money capital investing to make even more money. Capitalism is not (as for Keynes) a big market where we trade to maximize utility. So, crisis of aggregate demand are not technical hiccups (magneto trouble) which technocrats can solve. Marx is right that capitalism isn’t interested in full employment. Workers are good for one thing only, raising capital values. Because of the falling rate of profit (not just missing animal spirits), raising capital values will come to an end. Then capitalists will stop hiring workers, they are useless to them if there is no profit to be made.

Now, in Marx’ time money was backed up by gold, which has value because of the social necessary labour time to dig it up. With paper money or electronic money the labour value to produce it is miniscule. It only has value, because it represents value. Now, a lot of commentators seem to think: how can you change the real world, if you only change the representation of it? If you only take control of a picture of a pipe, you don’t have a pipe at all. But that’s a mistake. Money not only represents labour value, it entitles you to labour values. It’s dead labour values giving you the right to suck living labour values (Marx’ vampire). The power of the monetary authority is not that they can print pictures of dead presidents, it’s their ability to mess with the question: to how much living labour does ownership of dead labour entitles me? (Picture a coupon entitling me to ten hours of social necessary labour time, if the monetary authority changes the picture to 9 hours, I’m in a very real sense poorer.) How can the monetary authority do this? It’s done by buying up government bonds through newly created money and declaring that they won’t use these bonds to suck this money up again, until money is devalued by whatever % the monetary authority deems necessary. (My favorite policy would be helicopter drops, but that’s another discussion.) Now why have bonds any value? Because the state can tax labour. Modern fiat money is in the end backed up by taxes on workers. By taxing more or less the monetary authority changes to how much labour the ownership of money entitles you. Austerity is the wish to tax workers more (which raises the value of money capital, a kind of primitive accumulation), negative interest rates or inflation are done through taxing less by extinguishing government debts. In short, money is backed up by taxes on workers, forced labour time. If the state promise to backup each unit of money by higher taxes, that’s more forced labour time, money goes up in value, if it promises to tax less, money goes down in value.

Back to M-C-M’ and the falling rate of profit. If profit is zero, why hire workers? If capitalist can hoard dead labour ad infinitum, there is no reason to do it.

But if the monetary authority can devalue M (let’s say by telling the owners of money capital that their capital will be devalued by 10%per year), then investment with a profit rate above -10% is better than not investing. Zero profits or negative profits are now compatible with full employment. Workers get hired even if the rich get poorer. Like in the case Wakefield reports on, a little but fundamental element for the social relation of capitalism is missing, the power to hoard money capital. It’s now: use it or lose it.

(By the way, Proudhon has nothing to do with that, I’m all for interest, even negative interest 🙂 These ideas go back to Irving Fisher or Silvio Gesell.)

But in the end, isn’t this all anti-Marx? Yes, in the sense that I think we “only” need to socialize/tax resources in fixed supply (like land and natural monopolies) and control the money supply. We don’t have to get rid of a market economy or private investment decisions. There are a lot of good reasons to let the state do health care or basic research etc. but these are not specific to Marx. Social democrats, most Keynesians etc. all agree on that. The relevant question is: can we solve the “production only for profit”-problem by controlling the money supply or do we have to abolish the market and go for a command economy? The historical performance of command economies should allow for some reasonable doubts, to say the least. Not to forget that Marx and Engels also dreamt of the withering away of the state, not of a state who runs everything.