Official data are now available in order to update the measurement of the US rate of profit a la Marx for 2017. So, as is my wont, I have updated the time series measure of the US rate of profit. If you wish to replicate my results, I again refer you to the excellent manual for doing so compiled by Anders Axelsson from Sweden,

There are many ways to measure the rate of profit (see http://pinguet.free.fr/basu2012.pdf). As in last year, I have updated the measure used by Andrew Kliman (AK) in his book, The failure of capitalist production.

AK measures the US rate of profit based on corporate sector profits only and using the historic cost of net fixed assets as the denominator. AK considers this measure as the closest to Marx’s formula, namely that the rate of profit should be based on the advanced capital already bought (thus historic costs) and not on the current cost of replacing that capital. Marx approaches value theory temporally; thus the price of denominator in the rate of profit formula is at t1 and should not be changed to the price at t2. To do the latter is simultaneism, leading to a distortion of Marx’s value theory. This seems correct to me. The debate on this issue of measurement continues and can be found in the appendix in my book, The Long Depression, on measuring the rate of profit.

What are the results of the AK version of the rate of profit based on the US corporate sector?

There has been a fall in the rate of profit in 2017 from 24.4% in 2016 to 23.9% in 2017. Indeed, the US rate of profit on this measure has now fallen for three consecutive years from a post-crash peak in 2014. This suggests that the recovery in profitability since the Great Recession low in 2009 is over. The AK measure confirms Marx’s law in that there has been a secular decline in the US rate of profit since 1946 (25%) and since 1965 (30%). But what is also interesting is that, on AK’s measure, the rate of profit in the US corporate sector has risen since the trough of 2001 and the Great Recession of 2009 did not see a fall below that 2001 trough. Thus the 2000s appear to contradict the view of a ‘persistent’ fall in the US rate of profit. I consider the explanation for this later. But it is also true that the US rate of profit has not returned to the level of 2006, the registered peak in the neo-liberal period on AK’s measure. Indeed, in 2017 it was 17% lower than 2006.

Readers of my blog and other papers know that I prefer to measure the rate of profit a la Marx by looking at total surplus value in an economy against total productive capital employed; so as close as possible to Marx’s original formula of s/c+v. So I have a ‘whole economy’ measure based on total national income (less depreciation) for surplus value; net fixed assets for constant capital; and employee compensation for variable capital – a general rate of profit, if you like.

Most Marxist measures exclude any measure of variable capital on the grounds that it is not a stock of invested capital but a flow of circulating capital that cannot be measured from available data. I don’t agree that this is a restriction and G Carchedi and I have an unpublished work on this point. However, given that the value of constant capital compared to variable capital is five to eight times larger (depending on whether you use a historic or current cost measure), the addition of a measure of variable capital to the denominator does not change the trend in the rate of profit. The same result also applies to inventories (the stock of unfinished and intermediate goods). They should and could be added as circulating capital to the denominator for the rate of profit, but I have not done so as the results would be little different.

On my ‘whole economy’ measure, the US rate of profit since 1945 looks like this. As for 2017, my results show a slight rise over 2016. But the 2017 rate of profit is still 6-10% below the peak of 2006 and below the 2014 peak (as it is in the AK measure).

I have included measures based on historic (HC) and current costs (CC) for comparison. What this shows is that the current cost measure hit its low in the early 1980s and the historic cost measure did not do so until the early 1990s. Why the difference? Well, Basu (as above) has explained. It’s inflation. If inflation is high then the divergence between the changes in the HC measure and the CC measure will be greater. When inflation drops off, the difference in the changes between the two HC and CC measures narrows. From 1965 to 1982, the US rate of profit fell 21% on the HC measure but 36% on the CC measure. From 1982 to 1997, the US rate of profit rose just 10% on the HC measure, but rose 29% on the CC measure. But over the whole post-war period up to 2017, there was a secular fall in the US rate of profit on the HC measure of 28% and on the CC measure 28%!

There are many other ways of measuring the rate of profit. And this was raised in an important and useful discussion in a workshop on the rate of profit (my rough notes on this are here) organised by Professors Murray Smith and Jonah Butovsky during my visit to Brock University, Southern Ontario, Canada two weeks ago. Murray and Jonah have contributed to the new book, World in Crisis, edited by Mino Carchedi and myself. In their chapter, they argue that a clear distinction must be made between the productive sectors of the capitalist economy ie where new value is created and the unproductive, but necessary, sectors of the economy. The former would be manufacturing, industry, mining, agriculture, construction and transport and the latter would be commercial, financial, real estate and government.

Following the pioneering work of Sean Mage in the 1960s, Smith and Butovsky consider these socially necessary unproductive sectors as ‘overheads’ for capitalist production and so should be included in constant capital for the purposes of measuring the rate of profit. On their current cost measure, the US rate of profit has actually risen secularly since 1953. However, looking at only the non-financial sector, Smith and Butovsky find that the US rate of profit peak of 2006 was some 50% below the peaks of the 1950s and 1960s, confirming Marx’s law. Moreover, the strong rise in profitability recorded in all measures above can be considered “as anomalous and based to a considerable extent on ‘fictitious profits’ booked in the finance, insurance, and real-estate sectors, and perhaps also by many firms operating in the productive economy.” This is a similar conclusion reached by Peter Jones. He found that if you strip out ‘fictitious profits’, then the US corporate sector rate of profit actually fell from 1997 – see his graph below.

Recently, Lefteris Tsoulfidis from the University of Macedonia separated the rate of profit for the whole economy into a ‘general rate’ for all sectors and a ‘net rate’ for just the productive sectors. Lefteris kindly sent me his data. And this shows the following for the US general and net rate of profit from 1963 to 2015.

As in other measures, the US rate of profit is around 30% below 1960 levels but bottomed in the early 1980s with a modest recovery to the late 1990s in the so-called neoliberal period. But interestingly, on Tsoulfidis’ measures, there was a decline, not a rise, in the rate of profit from 2000 leading up to the Great Recession.

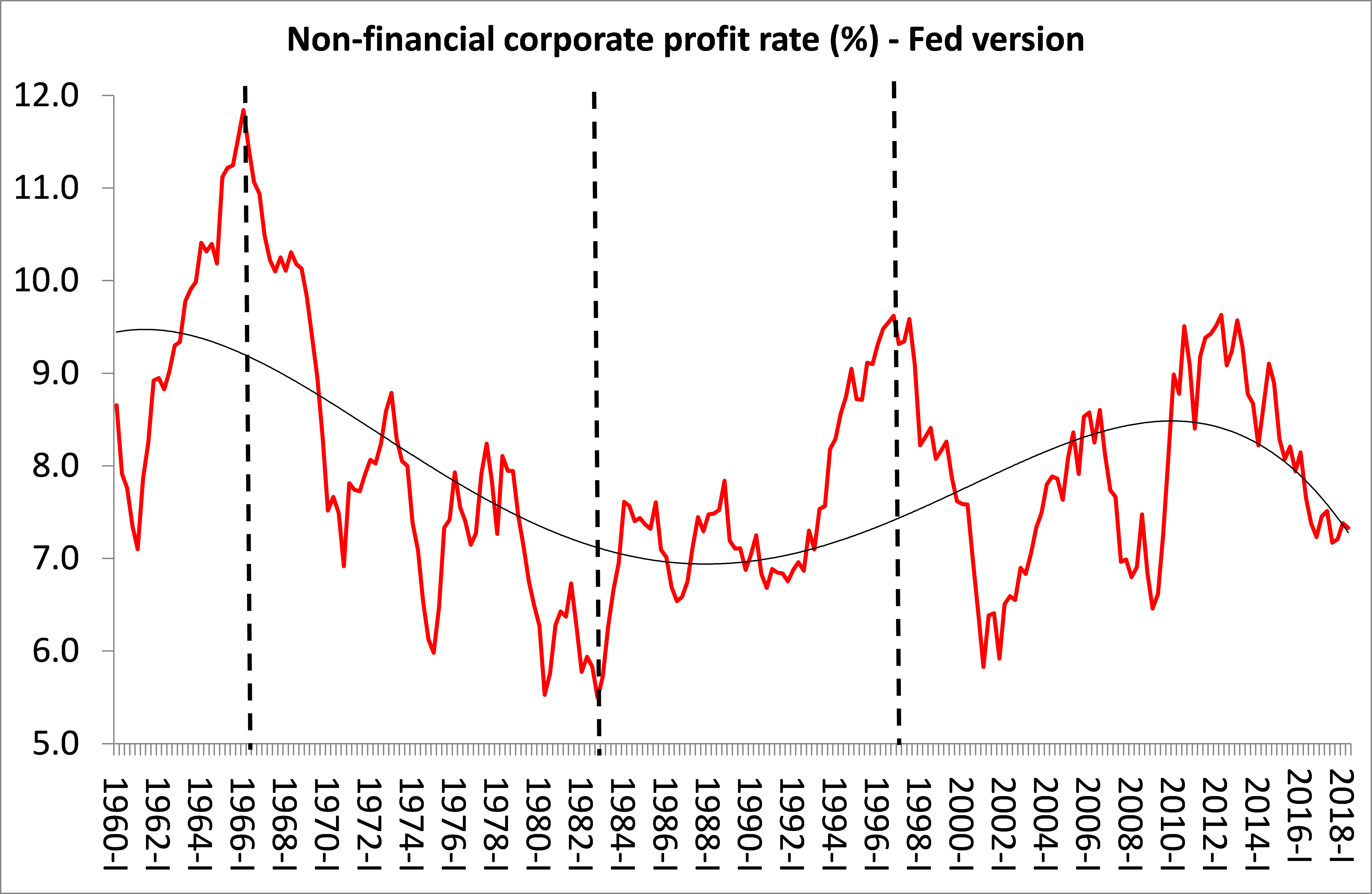

I looked at the US non-financial corporate sector (which is not strictly the same as the Marxian definition of the ‘productive’ sector), using data from the Federal Reserve. The net operating surplus over net financial assets is the measure I used for the rate of profit here.

This Fed measure shows that the US rate of profit peaked in 1997 to end the neo-liberal period and since then that rate has not been surpassed even in the credit-fuelled fictitious profits period from 2002 to 2006. Indeed, after peaking post the Great Recession in 2012, the Fed measure has fallen consistently right up to mid-2018. The Fed measure is quarterly and so provides a more up to date result. On this measure, the US rate of profit remains 32% below its ‘golden age’ peak in 1966, again confirming Marx’s law.

Marx’s law is also confirmed because the driver of changes in US profitability depends on the relative movement of the two Marxian categories in the accumulation process: the organic composition of capital and the rate of surplus value (exploitation). Since 1965 there has been the secular rise in the organic composition of capital of 21%, while the main ‘counteracting factor’ in Marx’s law, the rate of surplus value, has fallen over 4%. Conversely, in the neo-liberal period from 1982 to 1997, the rate of surplus value rose 16%, more than the organic composition of capital (7%), so the rate of profit rose 9.5%. Since 1997, the US rate of profit has fallen over 5%, because the organic composition of capital has risen over 14%, outstripping the rise in the rate of surplus value (5.4%).

One of the compelling results of the data is that they show that each economic recession in the US has been preceded by a fall in the rate of profit and then by a recovery in the rate after the slump. This is what you would expect cyclically from Marx’s law of profitability.

Clearly a significant fall in the rate of profit is an indicator for an upcoming slump in investment and production in a capitalist economy. Marx argued that a falling rate of profit would, for a while, be compensated for by an expansion of capital investment, so that the mass of profits would continue to rise. But that could not last and eventually the fall in the rate of profit would lead to a fall in the mass of profits, which would engender ‘absolute overproduction’ of capital and a slump in production. Marx explains all this clearly in Volume 3 of Capital, Chapter 15. And that is what occurred in the Great Recession.

What is the situation now in the middle of 2018? Well, US corporate profits are still rising, although non-financial profits are below the level at the end of 2014.

In a recent paper, G Carchedi identified three indicators for when crises occur: when the change in profitability; employment; and new value (v+s) are all negative at the same time. Whenever that happened (12 times since 1946), it coincided with a crisis or slump in production in the US. This is Carchedi’s graph.

My updated measure for the US rate of profit to 2017 confirms the first indicator is in place. However, ‘new value’ had two quarters of decline in 2015 and one in 2017, but in the first two quarters of 2018 it has been rising; and employment growth continues. So, on the basis of these three (Carchedi) indicators, a new recession in the US economy is not imminent as 2018 moves into the last quarter.

In sum, Marx’s law of profitability over the long term is again confirmed. I am reminded that back in 2013, Basu and Manolakos did a highly sophisticated econometric analysis of Marx’s law for the US rate of profit, controlling for all the counteracting factors in the law like cheapening constant capital and a rising rate of surplus value. They say “We find weak evidence of a long-run downward trend in the general profit rate for the U.S. economy for the period 1948-2007.” By which they mean that there was evidence but it was not decisive. But they also found that a decline in the US rate of profit was “negative and statistically significant” ie the fall in the rate of profit was not random. So “we find statistical evidence in favor of Marx’s hypothesis regarding the tendency of the general rate of profit to fall over time.” Basu and Manolakos reckon there was an average annual 2% fall in the US rate of profit over the period. In my own cruder calculations, I find exactly the same result for the period 1947-07 in the historic cost measure.

In conclusion, there has been a secular decline in US profitability, down by 28% since 1946 and 20% since 1965; and by 6-10% since the peak of 2006. So the recovery of the US economy since 2009 at the end of the Great Recession has not restored profitability to its previous level. Also, the driver of falling profitability has been the secular rise in the organic composition of capital, which has risen around 20% since 1965 while the main ‘counteracting factor’, the rate of surplus value, has fallen.

In 2017, the US rate of profit fell compared to 2016 on some measures (2%) or rose slightly on mine (1%). All measures show that the US rate of profit in 2017 was 6-10% below the level of 2014.

Good article. The trend is not the bourgeoisie’s friend.

Hi Michael,

Don’t want to return to old debates write now though I do want to emphasize that I find all your pieces, even those on FROP very helpful. I did however want to get a better sense of where your FROP argument is going other than defending Marx (tho whether this is the core of Marxism Marx is controversial). Is it merely to stay pressures to restore profits will constantly intensify and that generalized good times are inherently temporary under capitalism (in which case I agree). Or that over time profits will virtually disappear since the falling rate must logically approach zero unless there are always counter-tendencies, in which case FROP is a conditional tendency. As well you seem to concentrate morel lately on predicting the next recession. Profits are, i very much agree, key but as your analysis constantly demonstrates predictions based on only the profit rate have their limits. Hope you’ll have time to drop a clarification. Best.

On Fri, Nov 2, 2018 at 6:36 AM Michael Roberts Blog wrote:

> michael roberts posted: “Official data are now available in order to > update the measurement of the US rate of profit a la Marx for 2017. So, as > is my wont, I have updated the time series measure of the US rate of > profit. If you wish to replicate my results, I again refer you to” >

Dear Sam

Thanks very much for your comments. A bit of an unusually long reply is deserved.

On your first point, my objective is not so much to defend Marx for the sake of it, but because I consider that Marx’s laws of value, accumulation and profitability provide the best basis for understanding the capitalist mode of production and its contradictions. Better than say Keynes, Minsky or Schumpeter. But that can only be confirmed by evidence, not just theoretical rigor – we need both.

On your second point, yes, I think that the movement in the profitability of capital is a key indicator of the ‘health’ of capitalism and lies at the basis of the argument that the ‘generalised good times are inherently temporary’ under capitalism. There is a tendency for the rate of profit to fall; but as you say there are counter-tendencies that can reverse that tendency for periods, even decades. But the law is not ‘contingent’ because, over time,the rate of profit must and does fall, globally – and we have evidence for this.

Does this mean it will hit zero? Well, there is one factor that causes the rate to jump back up that you did not mention – crises/slumps. They , are (unconsciously) designed to restore profitability and production through the destruction of capital values – after huge waste, misery and at labour’s expense. The second world war enabled a sharp rise in profitability by destroying capital values (partly physically), setting a new level of profitability for the law to operate. But yes, it will still continue to head down over the long term (not in a straight line with impact of counter-tendencies) towards zero. But that zero is like a horizon that you never seem to reach (although you do get closer). On current trends, the global rate would mathematically hit zero about 2060. But there are many slumps, global warming and even wars before we get there to move that horizon; though it won’t take as long as ‘the sun burning out’, as Luxemburg caustically responded to a FROP supporter like me.

FROP is not just secular in its impact but also cyclical. FROP is also the basis of regular and recurring crises. But I have never said that it is the ‘direct’ cause of each crisis. Every crisis is different and the trigger for every slump is different because capitalism does not change its spots but its fur does get worn in different parts -a bit like me. So in 1929 it was the stock market; in 1974-5 oil; in 1980-2 manufacturing/dollar; in 2008-9 (US housing and global banking); and for the next one probably corporate and EM debt. So I’m not a one trick pony. Credit/debt matters, as do the imbalances globally between capitals. But the underlying driver is still FROP.

As for predictions, they have their limits whatever the theory, but I think it is the job of scientific socialists to try and improve their predictive skills, just as weather and climate scientists are doing. FROP is the basis for doing that in my view – but even in this post on the US rate of profit, there are other factors presented.

By the way, all these points are covered in my book, The Long Depression, in more detail.

I’m sorry to enter the debate, but I think there are two important factors you leave out of your interpretation:

1) This is the profit rate of the USA. Although the USA is the headquarters of capitalism, it is not the whole capitalist society. So, yes, profit rate can oscillate more when analyzing only one country than the whole society. Things get even more complicated when you consider real existing capitalism is not ideal capitalism: not only you have objective factors in play, but also the self-evident fact that, since 1917, it doesn’t exist alone anymore (it divides the globe with the socialist system).

2) Socialist economists are not the dominant class of economists. They have to work with what they have (i.e. vulgar economics metrics, which are mystifying, not revealing). That’s why there are many different ways to calculate the average profit rate, and even then, only for some few countries.

The figures assert a persistent decline in the rate of profit from 1947 to now. Yet this long span divides into two segments: the era of easy prosperity for capital from 1947 to around 1970, and from then to now. The profit trend alone obviously cannot explain the great turn. The working class in the U.S. experienced a similar divided span: mass prosperity, with significant exceptions, until 1973 – which is the peak year for real median earnings. Since then the lot of the class has stagnated and declined with barely a fragile year or two of minor exception. *** The rate of profit explains why crises and slumps are inherent in capitalism from its industrial phase on. For explanation of the larger picture, another fundamental observation by Marx on the movement of the forces and relations of production requires our attention..

Couple of thoughts

Decline of ROP in developed countries is being slowed down by the transfer of profit from underdeveloped countries for now. In future the organic composition of capital in these countries will go up and the rate of this transfer will be much less.

The rate of profit should not be compared in yearly intervals. No capitalist invests based on short term predictions(yearly). I believe we should calculate the average rate of profit for example in ten year periods and then compare them .

The rate of profit does not need to reach zero. With any investment there is a certain degree of risk because of competition and so on. If the risk is more than tolerance of capitalists class because of low profitability, they will avoid investment in production and will go to asset purchases, that does not produce surplus

Borzooieh Tabib

The rate of profit has a lot to do with real wages and their relation to the total amount of wealth being produced and sold.

“Since the capitalist and workman have only to divide this limited value, that is, the value measured by the total labour of the working man, the more the one gets the less will the other get, and vice versa. Whenever a quantity is given, one part of it will increase inversely as the other decreases. If the wages change, profits will change in an opposite direction. If wages fall, profits will rise; and if wages rise, profits will fall. If the working man, on our former supposition, gets three shillings, equal to one half of the value he has created, or if his whole working day consists half of paid, half of unpaid labour, the rate of profit will be 100 percent, because the capitalist would also get three shillings. If the working man receives only two shillings, or works only one third of the whole day for himself, the capitalist will get four shillings, and the rate of profit will be 200 per cent. If the working man receives four shillings, the capitalist will only receive two, and the rate of profit would sink to 50 percent, but all these variations will not affect the value of the commodity. A general rise of wages would, therefore, result in a fall of the general rate of profit, but not affect values.” Marx, “VP&P”

Have real wages stagnated as productivity has increased?

“Official data are now available in order to update the measurement of the US rate of profit a la Marx for 2017.”

A la, which one of Marx’s measurements of the rate of profit? Are you talking about the rate of profit s/d + c + v, for example, i.e. the profit margin? In that case, its impossible from official data to calculate it, as Marx showed in criticising Smith and Ricardo, who believed that the value of commodities, and so of national output resolves entirely into revenues – wages, rents, profits, interest and taxes – and whereby National Income is made equal to National Output, because that calculation omits the value of the constant capital consumed in production. GDP is a measure of value added, not total value of production.

So, a calculation of a rate of profit that omits the value of c (the raw materials consumed in production that must be reproduced in kind out of current output, and which constitute a revenue for no one) is wrong from the start. It is only a calculation of profit (surplus value) over v, and the ration s/v is not a calculation of the rate of profit but of the rate of surplus value. That the rate of surplus value might be falling, is not surprising at this stage of the long wave cycle. A fall in the rate of surplus value is, of course, what Ricardo confused with the fall in the rate of profit. He like Smith thought it was the explanation for the long term law of the law of a falling rate of profit, and Marx showed that whilst at various periods of boom and exuberance, this fall in the rate of surplus value, as wages rise (or as he sets out in Capital III, Chapter 6, and in TOSV, also sharp rises in the prices of raw materials as demand for them rises, which can’t be passed on in final product prices) this is not the cause of the law of the tendency for the rate of profit to fall.

In fact, Marx shows that the Law requires that productivity is rising, that relative surplus value is rising, and so the rate of surplus value, and mass of surplus value is rising, so that the value of consumed material rises faster than the rise in new value created by labour.

If you are measuring the rate of profit on this basis, therefore, not only is it wrong from the start, because it omits the value of c, the value of means of production used in the production of means of production, as Marx describes it in Capital II, and III, but, it certainly is not an indication of the operation of Marx’s law of a falling rate of profit, because it is rather an indication of a falling rather than rising rate of surplus value. If you are calculating it, by adding in the value of the fixed capital stock, then it is doubly wrong, because in Marx’s calculation of the rate of profit/profit margin, it is only the value of wear and tear of fixed capital (d) that is included in the calculation, not the value of the total stock.

If you mean a la Marx in relation to the average annual rate of profit, then it is again not calculable from the published data, because although its possible to get figures for fixed capital stock, it still omits the figure for circulating constant capital, i.e. the consumed raw materials component of the means of production used in the production of means of production, which forms a revenue for no one. Moreover, Marx’s calculation of the annual rate of profit, from which he calculates the average annual rate of profit for the total social capital, is based upon the advanced capital, not the laid-out capital, i.e. on the capital value advanced for one turnover period, not the cost of production for the year’s output.

So, although its possible to get a figure for the advanced fixed capital for a turnover period, because its basically the total value of the fixed capital stock itself (as Marx says, it all has to be present for production to occur, even though only a part of it enters the cost of production) not only is the value of raw materials consumed in production not available, but even if it were, its impossible to know how much of that value is advanced rather than laid out, because that depends upon the rate of turnover of this circulating capital. Again, the total figure for wages is known, but that is only relevant for a calculation of the rate of profit/profit margin, i.e. s/d + c + v, not of the average annual rate of profit, which is s x n/C, where C is the total capital advanced for one turnover period, and n is the number of turnover of the circulating capital in a year. In order to know these figures, its necessary to know a) the total value of c means of production used in the production of means of production (Department I (c)), which is not available because National Income GDP figures are only figures for the consumption fund i.e. the value of Department II output, and National Income data as its name suggests, is likewise only data for revenues (wages, profits, rent, interest and taxes), i.e. v + s (Department I and II v + s = Department II c + v + s), i.e. it is only a figure for value added by labour during the year, and not including the value of consumed materials directly replaced out of current production on a like for like basis, which represent a revenue for no one. But, also the data relates to laid out capital, i.e. costs of production, not the capital advanced, for which it would be necessary to know how many times the circulating capital turned over during the year, which the data does not provide.

So, a la Marx, the data actually do not tell us anything accurate about either the rate of profit/profit margin, or the average annual rate of profit. It tells us about changes in the rate of surplus value, and that shows the rate of surplus value is getting squeezed, which is precisely what would be expected at this stage of the long wave cycle, and is the same as happened at this stage in the early 1960’s, and through into the 1970’s, before a new wave of labour-saving technologies were introduced that replaced labour, increased productivity, and thereby set in places the actual conditions for the operation of Marx’s law of the falling rate of profit, to resolve that squeeze on profits, by reducing wages, and raising the rate and mass of surplus value.

“The second world war enabled a sharp rise in profitability by destroying capital values (partly physically), setting a new level of profitability for the law to operate.”

This is a Keynesian argument, in relation to physical destruction. Marx makes clear in TOSV that a physical destruction of capital represents a cost to capital, and thereby a limitation on the rate of profit. In short if capital is physically destroyed, so that its use value as capital no longer exists, then a portion of profit has to be used to physically replace that capital, and that profit could otherwise have been used to accumulate additional capital. It represents the same thing as Marx describes as a tie-up of capital, in Capital III, Chapter 6.

It is only the destruction of capital value, via moral depreciation that enables capital to increase the rate of profit, not the physical destruction of capital. The latter was an idea promoted by Stalinists after WWII, as they tried to explain the rapid growth of capital, at a time when they were predicting that a next recession, and misery was just around the corner.

That’s exactly what happened in WWII: electronics technology was being researched since the 20s, and existed since the 30s. The war accelerated moral deprectiation (by destruction and by urgent necessity of an arms race) of old technology.

War only accelerates, not creates, depreciation.

Marx sets it out in Theories of Surplus Value Part II. He shows that the physical destruction of capital plays no part in raising the rate of profit. It is only the destruction of capital value that raises the rate of profit. He says,

“When speaking of the destruction of capital through crises, one must distinguish between two factors.” (TOSV2 p 495)

One is the form of physical destruction described above, but it is the second form that is beneficial for capital.

“A large part of the nominal capital of the society, i.e., of the exchange-value of the existing capital, is once for all destroyed, although this very destruction, since it does not affect the use-value, may very much expedite the new reproduction. This is also the period during which moneyed interest enriches itself at the cost of industrial interest. As regards the fall in the purely nominal capital, State bonds, shares etc.—in so far as it does not lead to the bankruptcy of the state or of the share company, or to the complete stoppage of reproduction through undermining the credit of the industrial capitalists who hold such securities—it amounts only to the transfer of wealth from one hand to another and will, on the whole, act favourably upon reproduction, since the parvenus into whose hands these stocks or shares fall cheaply, are mostly more enterprising than their former owners.” (Theories of Surplus Value 2 p 496)

Note that Marx says here that it is precisely because this destruction of capital value, of the exchange value of the commodities that comprise the elements of the productive-capital, does not involve the destruction of their use value, i.e. their ability to function as productive-capital, that enables this reduction in capital value to produce a higher rate of profit.

A machine that loses half its value, thereby raises the rate of profit. A machine that no longer exists because it has been physically destroyed can produce no use values, and so contribute nothing to profit creation. On the contrary, the firm that has to use profits to replace destroyed machines, rather than add to their stock of them, will see its rate of profit decline, because its costs of production will have risen to cover the cost of buying the replacement machine.

Of course, in crises, commodities get physically destroyed, because they can’t be sold, which simply means that the labour expended on their production was not socially necessary, so in fact, they had ceased being use value, and ceased possessing exchange-value, even before their physical destruction. Capital as a whole doesn’t encourage destruction of its own profit creating capacity, such physical destruction is merely a consequence of the crisis.

If we take something like fresh vegetables, the producers of those vegetables may not be able to sell them at the prices they would like, so either they have to sell them below their exchange value/price of production, or else destroy the excess. From the perspective of society, however, the latter is a loss to its productive capacity, and potential for raising the rate of profit. The food processing and canning company, the company producing processed foods, or the restaurant and so on, would much prefer the farmer to sell their excess produce at much lower prices, because for all these capitals the fresh vegetables are their raw material, constant capital, and any reduction in the value of that constant capital for them, raises their rate of profit.

A note of caution also in respect of moral depreciation and the devaluation of capital in general as a result of rising productivity due to improved technology.

Bourgeois economics inherited Adam Smith’s “absurd dogma”, as Marx called it, that the value of commodities and thereby of the national output/GDP resolves entirely into revenues. One of the first thing taught in Economics classes is that the value of commodities/goods is divided into factor incomes profits to entrepreneurship, interest to capital, rent to land, wages to labour. This is derived from Adam Smith’s cost of production theory, whereby each of this factors sells at its natural price, and this natural price contributes an equal amount thereby to the value of the product.

This is the basis of bourgeois economic theory in relation to factor incomes, and marginal productivity theory, whereby each of these factors contributes to production, and obtains in return an amount of revenue which in a condition of optimality is equal to the value it contributes to production. If the return to any of these factors is above the value it creates, the demand for and supply of that factor will be imbalanced, so that the supply of it will rise, and demand for it fall until it is in balance, thereby restoring optimality.

On this basis, when a new machine is introduced, this additional “capital” is seen not as reducing value, as Marx explains, but of adding value. This additional value produced by the machine is then seen as the basis the additional return to capital.

So, in the capitalist data on productivity, it is based upon monetary values, whereas, as Marx demonstrates the real calculation of productivity must be conducted on the basis of use values. The productivity of a machine is measured by how many units of production it produces in an hour, not the value of that production. Bourgeois data based upon monetary values always necessarily understates rises in productivity, because the very rise in productivity, which ensures that more use values are produced with the same amount of labour, causes the value of those units to also fall.

The more new machines and technologies raise productivity, the more they reduce the values of commodities including those that comprise capital, and so the more a measure of productivity based upon monetary values rather than physical output understates the real increase in productivity.

The obvious indication of this, is that the rate of surplus value rises when productivity is rising sharply, so that a greater proportion of new value creation goes to surplus value relative to wages. But, the second consequence, at least in economies based upon manufacturing, is that the proportion of production going to reproducing the greater quantity of processed materials rises faster, which is the basis of marx’s law of the tendency for the rate of profit to fall.

A final point on this question of productivity, and on the rate of surplus value, rate of profit and release of capital.

As I showed previously, because bourgeois economic data measures productivity on the basis of nominal value of output as against labour hours, it necessarily understates productivity growth, because the rise in productivity itself reduces commodity values, and thereby the nominal value of GDP adjusted for inflation. So, as i said, if 1000 hours of labour produces 1000 units of output, and then a rise in productivity causes thi 1,000 hours of labour to produce 2000 units of output, the bourgeois data shows no rise in productivity, because although productivity has doubled, and twice as much is now produced, the value of that output has remained constant.

Marx explains how that can happen in TOSV, Chapter 22 (?). He says, if a spinning machine can be produced with only as much labour as was previously required to produce a spinning wheel, and 200 kilos of cotton can be produced with only as much labour as previously was required to produce 100 kilos of cotton, then the labourer who now spins 200 kilos of cotton into yarn using the spinning machine, in the same time as previously they took to spin 100 kilos of cotton into yarn using a spinning wheel, now produces 200 kilos of yarn with only the same value as previously was held by 100 kilos of cotton, and no change in the value relation between yarn, labour, cotton and fixed capital has occurred, causing no change in the rate of profit thereby.

However, he goes on, what is the actual situation in relation to this change in productivity, and the amount produced.

Take the example that Marx uses of a farmer producing grain. They use 10 kilos of grain as seed, and their output is 100 kilos. A further 40 kilos goes to pay wages, and 50 kilos constitutes surplus product/profit. Now, their output doubles to 200 kilos.

In other words, out of 100 kilos originally, 10 kilos were used as seed, 40 kilos as wages leaving 50 kilos as surplus product/profit. Now the 50 kilos reproduced as constant capital and variable-capital leaves 150 kilos as surplus product, whereas previously it was only 50 kilos. 100 kilos has been released as capital. It can be consumed by the farmer as additional revenue, or it can be accumulated as additional capital.

As Marx demonstrates against Ramsay, not only does this release of capital create the illusion of additional profit, but it actually represents an increase in the rate of profit. Previously, the 50 kilos of surplus represented a rate of profit of 50%. It meant 50% more seed and labour-power could be employed with the 50 kilos of surplus grain. But, the surplus is now 150 kilos, which means that 3 times as much grain can be used as seed or to pay wages, with a consequent accumulation of the capital, and expansion of output.

But, the relation to productivity that can be immediately seen is this. Because productivity has doubled, the 40 kilos required to reproduce the workers wages, now requires only half the time as before to produce. In other words, if previously the worker worked 4 hours to reproduce their labour-power, and 5 hours as surplus labour, they now only need to work for 2 hours to reproduce their labour-power (40 kilos of grain), leaving 7 hours as surplus labour, so that the immediate effect is this rise in the rate of surplus value.

That is the effect that capital seeks, particularly at points in the long wave cycle when labour-power has become in short supply and wages are rising, or the potential to expand absolute surplus value by an expansion of the social working-day is not possible.

“Of course, in crises, commodities get physically destroyed, because they can’t be sold, which simply means that the labour expended on their production was not socially necessary, so in fact, they had ceased being use value, and ceased possessing exchange-value, even before their physical destruction.”

Once again, the author of the above lines betrays a failure to grasp the nature of the commodity– the real conflict between use value and exchange value, and capital’s attempt to smother that conflict. The commodities so destroyed do not lose their use value. What occurs is that the relation of property, the need for profit dictates that the use-value be destroyed in an attempt to preserve exchange value for the remaining commodities, and for capital’s mode of commodity production as a whole. Clothing,food,housing do not lose their use value prior to consumption, even when “overproduced” in that overproduction is in relation to markets, to the mechanisms of exchange, not the NEEDS of the population.

“Capital as a whole doesn’t encourage destruction of its own profit creating capacity, such physical destruction is merely a consequence of the crisis.”

Priceless. Remember those words. The point is that the “profit making capacity” of the commodities, or the mode of production is already impaired, in the tank, gone, lost. How nice to think “capital doesn’t encourage destruction,”… that it’s just “merely(!!) a consequence of the crisis,” AS IF “the crisis” was not intrinsic, immanent, necessary to capitalism.

It seems the author of those misapprehensions will go to almost any length to advertise capitalism as a benign system, “dedicated” to the productivity of labor, to rational activity, and is impinged by extraneous “credit crunches” or short-sighted “austerity programs” by those agents of the capitalist ruling class who fail to follow the prescriptions of the author.

EDIT: “The commodities so destroyed do not lose their use value” SHOULD READ: “The commodities are not destroyed because they have lost their use value.”

“AK measures the US rate of profit based on corporate sector profits only and using the historic cost of net fixed assets as the denominator.”

Except of course, that in many places, Marx sets out why such historic prices are useless for calculating the rate of profit, precisely because the current rate of profit depends upon the current replacement cost of the commodities that comprise the capital, i.e. how much of current production, and current social labour-time is required to physically replace the consumed capital!

Its precisely for that reason that when. as you say in reply to Sam, the rate of profit is raised by the destruction of capital values, it is rises in social productivity that reduces the current reproduction cost of fixed capital that it brings about a moral depreciation of the fixed capital stock value, causing the rate of profit to rise, as well as reducing the value of raw materials, causing the rate of profit to rise, as well as reducing the value of wage goods, and hence the value of labour-power, which causes the rate of surplus value to rise, with a consequent rise in the rate of profit that brings about these effects upon which historic prices could have no effect.

In TOSV Chapter 22, Marx showed in response to Ramsey’s confusion over the illusion of profit created by the use of historic prices, why it is current reproduction costs that form the basis fr the calculation of the rate of profit. As Marx sets out in opposition to Ramsey, the use of historic prices would only be relevant if you saw capitalism as a static system, whereby all capital is effectively liquidated at the end of the year, and then started again. But, as Marx indicates capitalism does not work like that, it worked on the basis of an assumption of ongoing production, so that the capital consumed in production is reproduced on a like for like basis out of current production.

If the value of the capital that has to be physically replaced falls in value, because of rising productivity, or just falling market prices for the commodities that comprise the elements of capital, a smaller portion of this year’s output is required to reproduce them. That means that a) a portion of capital is released as revenue/profit, which is what caused Ramsey’s confusion, and can be utilised to increase accumulation, and b) the proportion of profit to the value of the capital that must be so replaced rises, so that the rate of profit rises. The first effect, Marx says creates the illusion that additional profit has been created, but the second effect is real.

Furthermore, Marx in Theories of Surplus Value chapter 23, sets out that the fall in the rate of profit due to the law of falling profits is much less than it is said to be, and is not sufficient to override the other forces that cause the rate of profit to rise.

“It is an incontrovertible fact that, as capitalist production develops, the portion of capital invested in machinery and raw materials grows, and the portion laid out in wages declines. This is the only question with which both Ramsay and Cherbuliez are concerned. For us, however, the main thing is: does this fact explain the decline in the rate of profit? (A decline, incidentally, which is far smaller than it is said to be.) Here it is not simply a question of the quantitative ratio but of the value ratio.”

Marx then sets out how the rise in productivity cheapens machinery and raw materials, but that the total quantity of these increases relative to labour. He concludes,

“The cheapening of raw materials, and of auxiliary materials; etc., checks but does not cancel the growth in the value of this part of capital. It checks it to the degree that it brings about a fall in profit.”

So, a tendency for the rate of profit to fall that is “much less than it is said to be” is itself checked sufficiently by the fall in the value of materials, caused by the very same rise in social productivity that is the basis of the law itself!

And, Marx shows in this chapter that he calculates the rate of profit on current reproduction costs, not historic prices.

Taking the situation of a coal producer he shows the effect, both of wear and tear, and of depreciation on the current value of the fixed capital as the basis of calculating the rate of profit.

He sets out an example whereby a coal producer has £50 of fixed capital, £50 of variable capital producing £50 of surplus value. The rate of profit is 50%, but the fixed capital loses 10% in wear and tear each year. So that in year 2, the value if its fixed capital is £45. The rate of profit then rises to 50/95 = 52.6%. Marx notes,

“In the second year, the fixed capital of the coal producer would amount to 45, variable capital to 50 and surplus-value to 50, that is, the capital advanced would be 95 and the profit would be 50. The rate of profit would have risen, because the value of the fixed ||1116| capital would have declined by one tenth as a result of wear and tear during the first year. Thus there can be no doubt that in the case of all capitals employing a great deal of fixed capital—provided the scale of production remains unchanged—the rate of profit must rise in proportion as the value of the machinery, the fixed capital, declines annually, because wear and tear has already been taken into account. If the coal producer sells his coal at the same price throughout the ten years, then his rate of profit must be higher in the second year than it was in the first and so forth.”

Marx notes that this is one way, in which firms with large amounts of fixed capital stock are able to offset the lack of competitiveness they would experience as a result of moral depreciation, as against newer firms who enter production using newer, cheaper machines.

I should also have added here, that in Chapter 23, Marx shows that although the mass of fixed capital rises, and its total value rises (as a result of this increase in its mass) relative to labour, because of the rise in productivity that cheapens the fixed capital, it falls relative to the value of raw materials, whose growth in mass is increased far more, as a result of that very rise in productivity. As Marx also sets out in Capital III, Chapter 6, the value of fixed capital, expressed in the value of wear and tear, also falls along with labour as a proportion of total output. The law of a falling rate of profit is driven by the rise in productivity that causes the mass of raw materials processed to rise faster than both the mass of fixed capital and labour.

But, as Marx points out in TOSV, Chapter 23, and in Capital III, Chapter 6, this very rise in productivity, which is technologically driven, not only cheapens fixed capital, and raw materials, it also means that even where the mass of machines rises due to accumulation, it rises at a slower pace than the rise in the mass of raw materials, because one new machine replaces several older machines, Moreover, this is also rue for some raw materials. For example, a more efficient steam engine not only replaces two or three older less efficient steam engines, as well as being cheaper, but it also burns much less coal for any given amount of output.

Since the 1980’s, similarly, the increase in oil consumption has risen by one a seventh of the rise in global GDP, as more efficient use of energy reduces the mass of raw material required to produce a given amount of energy. The same is true of new materials which replace older materials, LED lighting which replaces older forms of lighting that used more energy, and required far more materials for their production, mobile phones that require far less materials than a land-line, let alone the materials used in the production of cameras, and so, which are now combined in a tiny smart phone.

And, of course the major factor that influences this is that 80* of value and surplus value creation now occurs in service industries, where as with extractive industries, raw materials play next to no part in the production process.

Boffy – thanks for all this. But your total set of comments add up to a full post! Is this really necessary to put on my blog? Enough.

Michael,

Fair comment. If I’d realised when I started writing it would extend to that length, I would have thought to write a post of my own, and link to it.

Cheers.

Body. Thanks for recognising that. Appreciate it.

I have provided the rate of profit based on s/cc+fc where cc stands for circulating capital and fc stands for fixed capital. This yields a rate of profit 3 – 4% below the commonly used rate of return. https://theplanningmotivedotcom.files.wordpress.com/2018/11/rate-of-profit-usa-2017-pdf.pdf It answers some of Boffy’s reservations.

Thanks – I would have included this in my post. I should have asked you earlier for this.

In order to follow your (otherwise) lucid analysis this poor layman has had to assume that you include variable capital as part of circulating capital. is that correct?

I include variable capital in my measure s/c+v. Circulating capital can be defined as non labour capital being used in one production cycle eg raw materials and inputs. Most Marxist economists see variable capital as a flow with several turnovers in one production cycle and so is difficult to measure just using official stats. There are some ingenious solutions to this eg https://theplanningmotivedotcom.files.wordpress.com/2018/11/rate-of-profit-usa-2017-pdf.pdf

Thanks Michael, I had just read the link that Ucanbe supplied, and I should have made it clear that the question was directed to him about that link. …But I have another layman’s question:

Since profit can only be squeezed out of living labor, it’s obvious that the (exchange) value of living labor is the most important factor in calculating the rate of profit, especially for calculating a transnational, global, rate of profit–critical, I think, because most of the world’s productive labor (producing socially necessary wage goods) is now in (or from) the peripheries. Workers in the centers–however necessary and productive of value of their mostly service and commercially oriented labor– substantively live off the products of peripheral labor. Various riffs on merchant capitalism’s euphemistic concept of comparative advantage (e.g. transmogrified by some marxists into calculating the differences between national levels of labor productivity) cannot explain how much of the world’s wealth flows to the centers of the global system, providing bread and (hardware for capitalism’s media) circuses for the working classes.

Have there been attempts (other than Samir Amin’s and John Smith’s) to try to perform that global calculation? Is it even possible, given that the contradictions between labor power and variable capital, surplus product and surplus value (though most pronounced in the global value chains) are intentionally obscured by the profit-makers?

Global value chains are being measured by various scholars. We can capture the transfer of surplus value from the periphery to the centre of imperialism by measuring and compiling rates of profit in as many economies as possible. It’s crude but does deliver a trend globally. See my World rate of profit in posts and in my book, The Long Depression.

Hi sorry for the delay. Lots of local union work. Michael is partially right. Best to go on to my slide show and look at slide 13 (it is part of my latest posting) When you go to the location you will see SLIDE SHOW which you need to click on to open. Annual gross output is equal to c + v + s as it is the aggregated value of all sales. In slide 13 I use the simple number 400 comprising 300 intermediate and 100 final sales. In turn the final sale of 100 is composed of 50 surplus and 50 wages. To determine the cost of annual sales we need to remove s to yield c + v. This gives us 350. We also get 350 when we add inputs (intermediate sales) plus wages or 300 + 50. This is the way most people would view the issue. Michael did just that. Now note, the figure of 350 is the cost of ANNUAL OUTPUT. It is not working capital which is a single cycle amount. Therefore to reduce annual capital to working capital the cost of annual output has to be divided by the rate of turnover. So taking the example I use, a rate of turnover of 4.4 yields a period of 83 days (365/4.4). That is the money capital needed to cover 83 days. So every 83 days capital circulates back to its start point and when measured over 365 days it adds up 4.4 times yielding once again the cost of annual output.

“Since profit can only be squeezed out of living labor, it’s obvious that the (exchange) value of living labor is the most important factor in calculating the rate of profit,”

Living labour has no value. Living labour is value. As Marx points out to ask what is the value of labour is then the same as asking what is the value of value?

“I think, because most of the world’s productive labor (producing socially necessary wage goods) is now in (or from) the peripheries.”

I don’t know what you mean by socially necessary wage goods. Surely all wage goods, i.e. commodities required for the reproduction of labour-power is socially necessary. Not all the labour engaged in such production may be socially necessary, but that is an entirely different matter.

However, the central point here, is simply wrong. The majority of productive labour, as Marx defines it, i.e. labour which exchanges with capital, and produces surplus value, exists within developed economies, even though it is expanding rapidly in places like China. In terms of value, and surplus value creation, the amount produced in the developed economies is even more pronounced, because of higher levels of labour productivity, and more complex labour.

These are getting long again

Boffy, of course we both know that labor as such has no “value” (you mean “exchange value”, of course)–unless it produces a useful object, which may be said to have a “use value”. But that’s not the “value’ to which I referred when I spoke of squeezing value out of living labor. Sorry, I’m a layman, with only a little bit of knowledge. I might have been too brief (not always the soul of wit) Thanks for your comments, but they were unnecessary…

….We both know that within historically evolved capitalism, abstract, socially necessary labor power imbues (within the capitalist mode of production) both a useful product (which is only potentially useful under capitalism) and (potential) exchange value (which may or may not be realized–squeezed out of the useful product of living labor) by exchanging it for money.

Like us, Adam Smith recognized the two values within the commodity, but conflated them (exchange value and use value) because he believed the capitalist mode of production to be natural and eternal. It seems to me that sometimes (but not always) you share Smith’s liberal illusions…

Ucan,

“Annual gross output is equal to c + v + s as it is the aggregated value of all sales. In slide 13 I use the simple number 400 comprising 300 intermediate and 100 final sales.”

The point being as Marx sets out in Capital II, that 300 of intermediate goods value, is only the value of Department I v + s. It is a figure of net added value. To use the examples that Marx uses, it does not include the value of the grain produced by the farmer, which they simply put back into the ground as seed for the next year, or the coal produced by the coal producer, which they use to power their own steam engines, etc. None of those bits of output are sold, and none appear as revenue for anyone.

And, as Marx then demonstrates, this applies also to all of those intermediate goods, means of production used in the production of means of production that are not replaced directly in kind out of the producer’s own production, but which are still replaced out of current production indirectly. For example, the coal producer does not reproduce the steel they consume directly, and the steel producer does not reproduce the coal they consume, but together they do, and again on a net basis that does not appear in sales.

If the coal producer needs to replace £100 of steel, and the steel producer needs to replace £100 of coal, they each mutually replace each other’s constant capital. The £100 of coal is deducted from the steel producer’s gross output, whilst the £100 of steel is deducted from the coal producers gross output so that they cancel out. But, it is nevertheless the case that £200 of coal and steel has been produced. It just doesn’t appear in the output figures, and because it generates no revenue for anyone, nor is their any equivalent revenue figure shown in the National Income accounts.

A convenient and accessible presentation of the breakdown of National Income figures is given here for 2011 – http://www.economicsonline.co.uk/Managing_the_economy/National_income.php. UK wages were £799 billion. If the rate of turnover is 4.4 times per year, the advanced variable capital would be, £181 billion. Using Engels 1300% annual rate of surplus value (Capital III, Chapter 4), as a base, even with a modest annual rise in the annual rate of surplus value over the last 160 years, we might estimate it today to be at least, 2000%. My own experience even in the 1980’s, from self-employment, puts the figure closer to around 5000%. But, using the very conservative 2000% figure we arrive at a figure for total surplus value of £3,631 billion. In fact, the total figure for profits, rents and taxes for that year was £654 billion, or just a fifth of the figure that would result from Green’s formula. In order to arrive at a figure consistent with the actual National Income breakdown, even using the conservative figure of only a 2000% annual rate of surplus value, we would have to calculate the rate of turnover to be around 22 times p.a.

The annual rate of surplus value rises because, rises in productivity reduce the value of labour-power, thereby raising the rate of surplus value, and similarly, rises in productivity in production and distribution, increases the rate of turnover, so that the variable-capital is turned over more quickly causing the annual rate of surplus value to rise. Given an average annual rise in productivity of around 2%, it can be seen how modest the 2000% figure is compared to Engels calculation of 1300%. Put another way, if the annual rate of surplus value today is 5000%, we arrive at the following. Total surplus value is £654 billion, so variable-capital is £13.08 billion. The actual amount for laid out wages was £799 billion, so that the rate of turnover must be 54.20 times per annum.

Thanks for that link. Actually, don’t think it addresses the points I made, but given Michael’s valid comment above, I am writing a more comprehensive set of posts of my own on all this, which I will give a link to when complete.

Personally I should appreciate a lot more detail and look forward to that. Could you illustrate at greater length the distinction between advanced capital and laid out capital?

There are a number of issues raised here that Marxists really need to address.

1) Samuelson in one of the earlier editions of his book asserts that Marx’s TRPF has been falsified by the fact that at the time he was writing it had been rising. The corollary is that the fact of the rate of profit falling does not per se confirm the validity of the thesis. If following J.S. Mill we argue by analogy to gravity we comprehend that the force of gravity is constantly propelling the moon towards the Earth, which it misses due to its tangential velocity. Apparently it will strike the earth 65 billion years from now. So too with the TRPF: it constantly asserts its pressure on the capitalists, who are consequently obliged to take countervailing measures.If the rate of profit were never to fall, then of course Marx would be refuted; but there is surely nothing in his thesis that asserts that the rate of profit always falls secularly from some 18th century capitalist peak?

2) As Engels himself points out, a decrease in turnover time increases the rate of profit. One of the main causes of this was the increase of productivity in the transport sector.One would like to see contemporary figures for the ratio of fixed to circulating capital in this industry.

”I should also have added here, that in Chapter 23, Marx shows that although the mass of fixed capital rises, and its total value rises (as a result of this increase in its mass) relative to labour, because of the rise in productivity that cheapens the fixed capital, it falls relative to the value of raw materials, whose growth in mass is increased far more, as a result of that very rise in productivity.” Is this currently true for example in the shipping industry? Is a ship not fixed capital, which also in a sense ‘circulates’?

3) What do we include in ‘commerce’? Is the worker who packages a good in a shop unproductive, while one who does it in a factory productive? We need clarity here.

4)”And, Marx shows in this chapter that he calculates the rate of profit on current reproduction costs, not historic prices.”

Two points: a) If we speak of say a 20% devaluation, how can this be measured unless against the historic value as represented in its price?

b)’current reproduction costs’ How are these identified?

I hope Michael, Bothy and others will address these issues albeit at not too great length!

1) see my book, Marx 200. 2) fixed assets are still much larger than circulating constant capital 3) see Marx Theories of Surplus Value and this is dealt with by several scholars 4a) correct 4b) in the production cycle but not before as in the simultaneist interpretation.

J,

I’m loathe to respond at to large an extent, because of hogging the comments, and because I will be dealing with all these issues in my own series of blog posts, dissecting Michael’s argument. Let me try to do it succinctly, in relation to a real life example.

Back in the 1980’s, I was forced into self-employment. I ran a number of businesses. One was selling cleaning supplies door to door. It worked like this.

I printed leaflets, as order forms for the products I was selling. I collected the orders, each week, totalled them up, and then bought washing up liquid, bleach and so on from my supplier. I then delivered the supplies, and got paid.

Within a matter of a few months, the business had expanded so much that I had to buy a large second hand transit van to use for deliveries.

Each week, I would spend about £500 on the materials to be sold, and took in around £1,000. So, each week, my circulating capital amounted to what I paid out for the materials (plus petrol, printing and so on, but ignore that) plus what I would normally have paid myself as wages, say £200. In total, £700. I paid £1,000 for the van, which represented fixed capital.

Say the van lost 20% a year in wear and tear = £200.

So, my cost of production, for the year is £700 x 50 = £35,000 plus £200 = £35,200. My turnover is £50,000, giving profit of just under £15,000, a rate of profit of 42.86%. My laid out capital is the same as my cost of production.

However, each week, my advanced capital is equal to the £700 for materials and wages. But, I also have advanced capital for the van. The £1,000 I paid for it, is capital that I could have used in some other way, and made the average rate of profit on. For example if I hadn’t needed a van, it would have bought 2 weeks supply of materials on which I would have made profits. So, in calculating my advanced capital, as Marx sets out, the full current value of the fixed capital has to be included – that is the point of his comment in Chapter 23, showing that it is this current value, not the historic price paid for it that is the determinant of the rate of profit – and not just the wear and tear, which forms a part of the cost of production/laid out capital.

At the end of the week, however, I sell all of the products, and get back £1,000. So, now, out of this £1,000 I have £500 to be able to buy the materials to be sold next week, and I also have £200 to pay my wages for the week. It also returns to me £4 to cover the wear and tear of the van, which I can put into a fund for its replacement after 5 years. So, I do not have to advance any new capital for week 2. All of the capital to be laid out in week 2, is the same capital that was advanced in Week 1. The same is true for Week 3, and so on.

So, my advanced capital for the year, is £1,000 for the van, £500 for materials, and £200 for wages = £1,700. With £1,700 I could run the business for a year. But, over the year, as set out above, my total profit was approximately £15,000, so now my rate of profit, or what Marx and Engels call the annual rate of profit, is 15,000/1700 = 882.35%! That is clearly significantly more than the 42.86% rate of profit. That is why Engels makes clear that former rate of profit is a con, and it is this annual rate of profit which is the true measure of how much the capitalists are screwing out of workers. It is a consequence of the rate of turnover.

The other thing to note here is that in terms of the advanced capital, the fixed capital represents about 150% of the circulating capital, in relation to the advanced capital, and yet, if forms only a small part of the laid out capital.

Suppose I’d only made deliveries every 2 weeks. My profit for the year would then have fallen to around £7,500. In terms of my rate of profit it would not have changed, because the amount laid out for wages and materials would also have halved, and the wear and tear of the van constitutes only a tiny element of the cost of production. But, my advanced capital would have remained £1700. Consequently, my annual rate of profit would fall to 7500/1700 = 441%.

As Marx says, in Year 2, my van is actually now worth only £800. If I sold it, so as to liquidate that capital to use in some other venture, I could only get £800 for. So, my advanced capital for Year 2 falls by £200, and so my annual rate of profit would rise accordingly. But, suppose, it had been a new van, and that soon after I’d bought it, new van prices collapsed, so that the van only had a current value of £500.

I can’t now claim that I have a van worth £1,000, as part of my advanced capital, because I just don’t. Its value is only £500. If I sold the van now, in order to liquidate the capital value tied up in it, I would only get £500, not the £1,000 I paid for it. So I can only justifiably calculate my annual rate of profit on the capital value I have actually tied up in the business, and that is now only £1200, not £1700. Consequently, although I have made a capital loss of £500, on the sudden moral depreciation of the van, my annual rate of profit will have risen.

The justification for that is also easily seen. At the end of five years, when I come to replace the van, I will only have to pay £500, and not the original £1,000 price. With my £15,000 profit, if my business had expanded, it would buy me 30 vans, if I so chose, rather than only 15 at their old price, and the real nature of the annual rate of profit, is as a measure of the extent to which it makes this physical accumulation of capital possible, because it is that physical accumulation of capital, and thereby the employment of additional labour, that makes possible the expansion yet further of the production of surplus value.

So, as Marx says in TOSV, Chapter 23, for capitals with lots of fixed capital, it is the fact of the writing down of the capital value each year, as a result of wear and tear that enables them to make a higher rate of profit each year, and also to be able to offset the capital losses due to moral depreciation. For example, I had owned the van for 4 years out of its 5 year life, then each year, I would have got back £200 in the value of wear and tear, which would have gone into my amortisation fund for van replacement. I would have accumulated £800. In the fifth year, if then van prices fell to £500, I would only be able to charge £100, to wear and tear, but in total I would have taken in £900 in wear and tear, whilst I now only need to spend £500 to replace the van!

That is why Marx says that the rate of profit must be calculated on the basis of the current reproduction cost of capital, and not the historic price, which is meaningless, and leads to ridiculous conclusions that undermine his labour theory of value, when considering the process of social reproduction.

Boffy there are many things I admire about you particularly your mastery of Das Kapital, but please could you turn Marxism from a theoretical science into an applied science. That means examining and interpreting the data. Specially for you, n my next posting, I will include a graph which shows that inventory (as calculated by the BEA) has fallen systematically and quite sharply over the decades as a share of fixed capital. As current inventory is 35 – 40% of total circulating capital its fall is one of the major reasons circulating capital has diminished in relation to fixed capital.

J,

The relevant comments by Marx are these.

“If the price of raw material, for instance of cotton, rises, then the price of cotton goods — both semi-finished goods like yarn and finished goods like cotton fabrics — manufactured while cotton was cheaper, rises also. So does the value of the unprocessed cotton held in stock, and of the cotton in the process of manufacture. The latter because it comes to represent more labour-time in retrospect and thus adds more than its original value to the product which it enters, and more than the capitalist paid for it.

Hence, if the price of raw materials rises, and there is a considerable quantity of available finished commodities in the market, no matter what the stage of their manufacture, the value of these commodities rises, thereby enhancing the value of the existing capital…

The reverse takes place when the price of raw material falls. Other circumstances remaining the same, this increases the rate of profit.”

(Capital III, Chapter 6)

Its clear here that Marx ignores the historic cost of the cotton, and calculates the rate of profit on the current value, i.e. current reproduction cost of the cotton. The same argument applies in relation to fixed rather than circulating constant capital.

“This entire portion of constant capital consumed in production must be replaced in kind. Assuming all other circumstances, particularly the productive power of labour, to remain unchanged, this portion requires the same amount of labour for its replacement as before, i.e., it must be replaced by an equivalent value. If not, then reproduction itself cannot take place on the former scale.”

(Capital III, Chapter 49)

Later in the chapter, Marx says,

“If the productiveness of labour remains the same, then this replacement in kind implies replacing the same value which the constant capital had in its old form. But should the productiveness of labour increase, so that the same material elements may be reproduced with less labour, then a smaller portion of the value of the product can completely replace the constant part in kind.”

Again, Marx here makes clear that a) his focus is upon the physical replacement of the capital which must occur for social reproduction to continue on the same scale, and b) the extent to which that physical replacement can take place with a greater or lesser degree of social-labour-time, i.e. a greater or smaller proportion of current social production, depends upon the changes in social productivity. A rise in productivity that reduces the value of capital, causes a moral depreciation of that capital, and leads to a rise in the rate of profit, and vice versa.

”4b) in the production cycle but not before as in the simultaneist interpretation”

This illustrates why I appeal for greater detail. No Marxist denies that value is created in the production cycle. Here are where I at any rate need further clarity.

1) Do Michael and Boffy agree on what they mean by ‘simultaneity’ ?

2) Is the simultaneist interpretation the same as the current reproduction costs interpretation?

3) How are the current reproduction costs identified? Are they the costs incurred by, say, the introduction of the latest machines in a particular branch of production? If so, how do the capitalists who introduce them gain an extra profit by selling their commodities below value? And how is this latter value established?

4) 90% of Shirtmakers in the market have a supply of cotton for three months. A bumper harvest depreciates the value by 50%. The other 10 % of manufacturers purchase the new cheaper cotton. If the 90% were to sell their cotton then of course they can only do so at its new value. But they have to reproduce i.e to manufacture shirts. My understanding is that the value of the shirts is in fact unchanged as the 90% of manufacturers’ costs determine the market value and the remaining 10% sell their shirts below this value.

I look forward to Boffy’s comprehensive post and anyone else’s more immediate clarification.

Boffy’s post should be on his site and not too comprehensive here

I understand that Boffy is to do a comprehensive post on his own site. I trust we will all apply our minds to clarifying these issues, for I have no doubt that I am not the only one searching for such clarity. But we must bear Michael’s request in mind.

J,

I will deal comprehensively with your point in my series of blog posts. To answer you points in as few syllables as possible, however.

1) Yes, but see my links below to the fact that Marx himself, and his dialectical epistemology is inseparable from such simultaneity, as opposed to the rejection of simultaneity by opponents of the dialectic.

I’m surprised that Michael rejects it, because his historical heritage is that of orthodox Marxism, whereas many of the proponents of the TSSI, and historic pricing are part of what is called the Third Camp, whose founders were Burnham and Schachtman, and who did so on the basis of a rejection of the dialectic, on their inevitable trajectory towards also rejection of Marxism, before becoming outright enemies of Socialism

2) Yes.

3) Average social labour time, which is constantly changing. An individual capitalist makes surplus profits from the introduction of a new machine in the same way any individual capitalist makes surplus profits, i.e. the individual value of their output is lower than the market value of that output. See Marx’s comprehensive explanation of this in his extensive examples on rent in Capital III, and TOSV.

4) The value necessarily falls, as Marx describes, but the market price might immediately not, because the 90% can dominate the market price. In fact, however, as Marx sets out at length in TOSV, this tends not to happen, because even at the time he was writing, produces tried to keep stocks, what he calls productive supply, to a minimum, because its dead capital. He says such stocks only ever form a small portion of the raw material processed during the year, and so the fall in the price of cotton presses down on cotton goods prices for these 90% too. It is simultaneity in action again, because as Marx shows in his analysis of Hodgskin, in TOSV, a large part of production, is undertaken by simultaneous, contemporaneous labour, i.e. as Hodgskin says, the bread that the worker eats at lunchtime, was not variable-capital that had been stored up by capital, but was the product of simultaneous, contemporary labour by bakery workers that morning.

Just In Time, raises this principle to ever new heights.

Can we all take a breath here and try and frame this issue of historical/current costs in the concrete?

Capitalist enterprises keep extensive records on property, plant, and equipment, and NET (undepreciated) property, plant and equipment.

Take for example a locomotive that costs capitalist A $4,000,000 initial outlay. Say the schedule of depreciation allows the capitalist to depreciate the locomotive in 20 equal increments over the next 20 years.

The first year, capitalist A clears $320,000 in net operating profit.

What constitutes the rate of profit obtained from use of the locomotive?

Is it calculated on the $4 million, or on the $200,000 theoretically “advanced” as depreciation?

Does depreciation actually devalue the locomotive, or does it become part of the circulating constant capital, like fuel, water, headlight replacement etc, recaptured and restored through the circuit of capital?

Another question: Suppose Year 5 capitalist A clears only $300,000 of net operating profit. Is the rate of profit improved because the value of the equipment has been depreciated to $3.0 million?

Year 5, a competing capitalist, capitalist B purchases a locomotive, for $6,000,000, with advanced traction control features that reduce fuel consumption, reduce wheel repairs, keep the locomotive out of the maintenance shop and allow B’s locomotive to haul heavier tonnage than that locomotive A.

What’s the “replacement cost” of locomotive A?

We know that Capitalist A can no longer charge his previous haul rates, but will have to reduce those rates to the social average of A & B. Does it even make sense to talk of a “replacement cost” of locomotive A?

There are a number of ways to make the calculation that can tell you that it’s time to purchase that new locomotive B. None that I know of disregard the actual initial cost of locomotive A, so I don’t how it can be disregarded in calculations of profitability.

Ucan,

“As current inventory is 35 – 40% of total circulating capital its fall is one of the major reasons circulating capital has diminished in relation to fixed capital.”