The world’s stock markets are spiralling down. The US equity market has fallen 10% in the last month, a figure that is called a ‘correction’ in investor terminology. That’s not yet a crash or ‘bear market’, usually measured as a 20% fall. But it’s going that way.

Stock markets are diving because it seems that the big investors, banks and financial institutions globally, are worried that China is imploding and planning to devalue its currency hugely, thus driving down the rest of emerging economies, many of which are already in recession (Brazil, Russia, South Africa etc) and so will pull down the rest of world, the major advanced economies, into a global slump.

The economists of many investment banks, previously confident of economic recovery and lauding the great emerging market ‘miracle’, are now in a despond of despair. For example, analysts at the UK bank, the Royal Bank of Scotland (RBS) told clients to “sell everything” as stock markets could fall more than a fifth, while oil and other commodity prices could drop to a tenth of where they were just a year ago. RBS have noticed a ‘nasty cocktail’ of deflation in commodity prices, emerging economies in recession, capital flight by investors and rich citizens from China and other emerging economies and the prospect of higher dollar debt servicing costs as the US Federal Reserve carries out a planned hike in its policy interest rate this year.

I raised the prospect of an emerging market crisis two years ago and then again last summer and the risk that Fed hikes could induce a new economic recession globally. Now mainstream economics has caught on and is advising its clients (rich investors) to get out of the market. But exaggerated optimism has swung to its opposite. Is a global economic and financial collapse really imminent?

Most of the doom-mongers concentrate on what they see is the kernel of a global slump: China. The RBS says that “China has set off a major correction and it is going to snowball… the epicentre of global stress is China, where debt-driven expansion has reached saturation. The country now faces a surge in capital flight and needs a “dramatically lower” currency.” Albert Edwards at Societe Generale has been predicting a deflationary slump for the last five years of global economic recovery. Now he is convinced that the Chinese crisis will lead to a global slump. “The western manufacturing sector will choke under this imported deflationary tourniquet,” says Edwards.

But is this right? There is no question that the Chinese economy is in trouble. Economic growth has slowed from double-digit increases back in 2010-11 to under 7% on official estimates in 2015. Many reckon that this official figure is nonsense and, looking at the pace of electricity consumption and spending, economic growth is probably more like 4%, which in Chinese terms is almost a recession.

When the Great Recession broke, the Chinese government reacted to a serious decline in global demand for its exports by launching a major government spending programme to build bridges, cities, roads and railways. That kept the Chinese economy growing. Interest rates were slashed and local authorities were allowed to borrow in order to spend on housing and other projects. There was a major credit boom. As a result, Chinese non-financial debt rose from about 100 per cent to about 250 per cent of GDP. Total Social Financing, a broad measure of monthly credit creation, is now growing at nearly three times the rate of officially recorded money GDP growth, or more if you don’t believe the official GDP data.

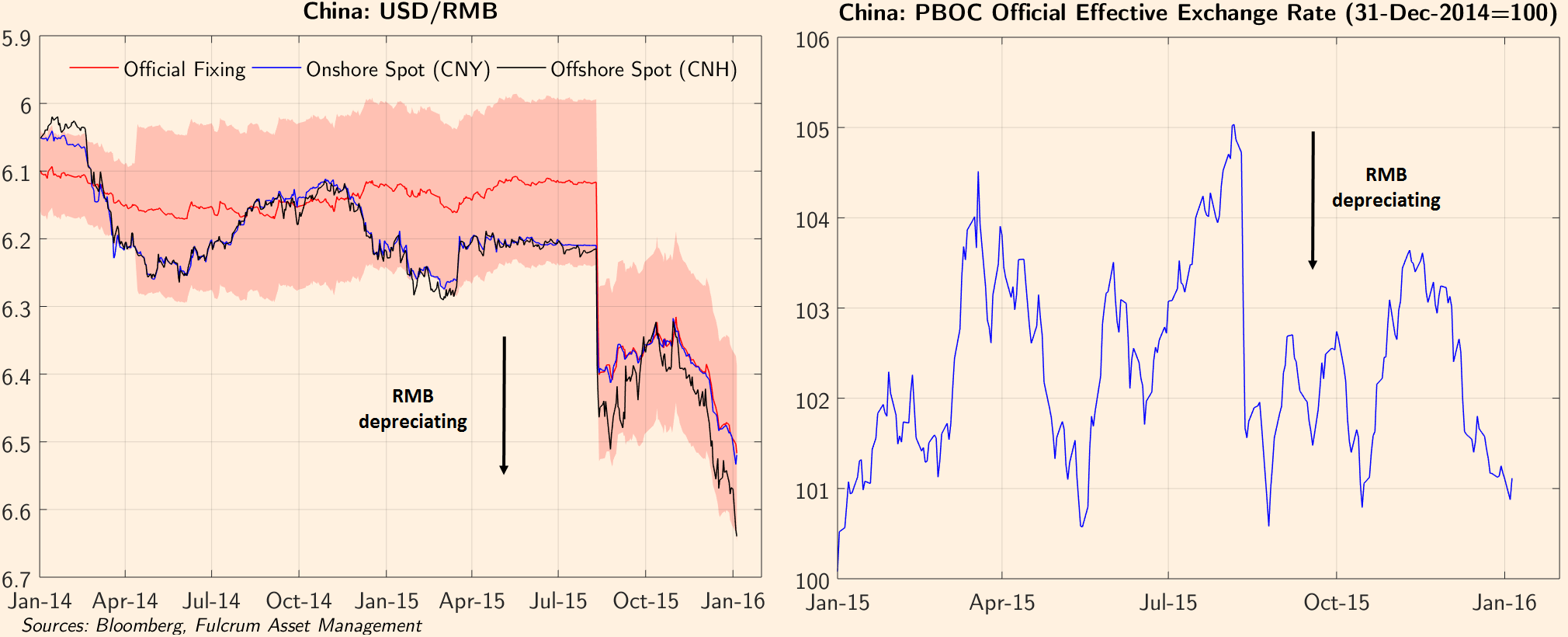

The government was influenced by pro-capitalist economists in their ranks who have been continually arguing that the government must ‘open up’ the economy to foreign capital and private companies. The government should privatise the big state owned companies and banks, end capital controls and allow the Chinese yuan to become a freely fluctuating currency, it was argued. Indeed, just before the Chinese stock market and currency crash began, the government pushed for and got the Chinese yuan to be included in the IMF’s international reserve currency basket for the so-called SDR. In effect, the Chinese currency was now increasingly subject to the laws of the international currency markets and the economy was increasingly influenced by the law of value.

More debt, slower growth and an overvalued currency, now subject to speculation, has engendered a stock market crash and now rich Chinese and foreign investors are trying to get their money out of China or the yuan and convert it to dollars abroad. Capital flight, as it is called, is running at over $100bn a month, or about $1.2trn a year. Given that Chinese dollar reserves are about $3.3trn and around half of that is needed to cover imports, if capital flight continues at the current rate, Chinese dollar reserves will be exhausted in about 18 months.

The Chinese authorities have been unable to handle this financial crisis. By opening up their economy to currency and financial speculation, they created a Frankenstein that is now trying to kill them. First, they tried to weaken the yuan against the dollar to boost exports. But a weaker currency only encouraged rich Chinese and Chinese companies to switch even more into dollars, by legal and illegal methods. Then they tried to prop up the stock market with extra credit and by making state-owned banks buy stocks. But this only fuelled even more debt. Then they reversed these policies, causing a stock market crash and credit squeeze.

The seeming incompetence of the Chinese authorities and the continued capital flight have now convinced many Western capitalist economists that China will suffer a ‘hard landing’ or economic slump, capitalist-style, and this will add to already diving emerging economies and drive the world into slump.

But does a collapse in the Chinese stock market and fall in the value of the yuan mean an economic slump in China? China is not a ‘normal’ capitalist economy. The power of the state remains dominant in industry, in the financial sector and in investment. Yes, the Chinese authorities have opened the economy to the forces of capitalist value, particularly in trade and capital flows, and in so doing have made China much more vulnerable to crises. This is something that I forecast back in 2012: “if the capitalist road is adopted and the law of value becomes dominant, it will expose the Chinese people to chronic economic instability (booms and slumps), insecurity of employment and income and greater inequalities.” And this has been the result of Chinese leaders succumbing to the pressures of the World Bank and others to ‘liberalise’ the financial sector and become part of the international financial ‘community’.

Yes, the world is slowing down. The Long Depression, as I have described it, is still operating. Only last week, the World Bank pointed out that developing economies grew just 3.7 per cent in 2015, the slowest since 2001 and two percentage points below the average 6.3 per cent growth during the boom years between 2000 and 2008. And IMF chief Christine Lagarde reckoned that developing countries face ‘new reality’ of lower growth. “Growth rates are down, and cyclical and structural forces have undermined the traditional growth paradigm. On current forecasts, the emerging world will converge to advanced-economy income levels at less than two-thirds the pace we had predicted just a decade ago. This is cause for concern.” A 1 per cent slowdown in emerging markets would cause already weak growth in advanced countries to slow by about 0.2 percentage points, Ms Lagarde said.

But will the slowdown in China and the slumps in major emerging economies bring down the world? The argument for that to happen is based partly on the claim that emerging economies are now the drivers of the world economy. Emerging economies are 57% of world GDP and have outstripped the advanced capitalist economies, according to IMF figures. But this is a wild exaggeration because the IMF uses what is called a purchasing power parity (PPP) measure. This measures what you can spend or invest in local currency in any country. That exaggerates the national output of emerging economies compared to measuring GDP in dollars as is necessary in world trade and investment.

In dollar terms, emerging economies have only 40% of world GDP. Sure, that share has doubled since 2002, but it is still the case that just the top seven major capitalist economies have a greater share than all the emerging economies, with 46%. And in the last two years, that share has stabilised. While China’s share of world dollar GDP has rocketed from just 4% in 2002 to 15% now, it is still much smaller than the share of world GDP for the US. That has fallen from 32% in 2002 to 24% now.

These figures show the tremendous expansion of the Chinese economy. But they also show that the US remains the pivotal economy for a global capitalist crisis, particularly as it dominates in financial and technology sectors. In 1998, the emerging economies had a major economic and financial crisis but it did not lead to a global slump. In 2008, the US had a biggest slump in its economic post-war history and it led to a global recession, the Great Recession. In my view, this weighting still applies.

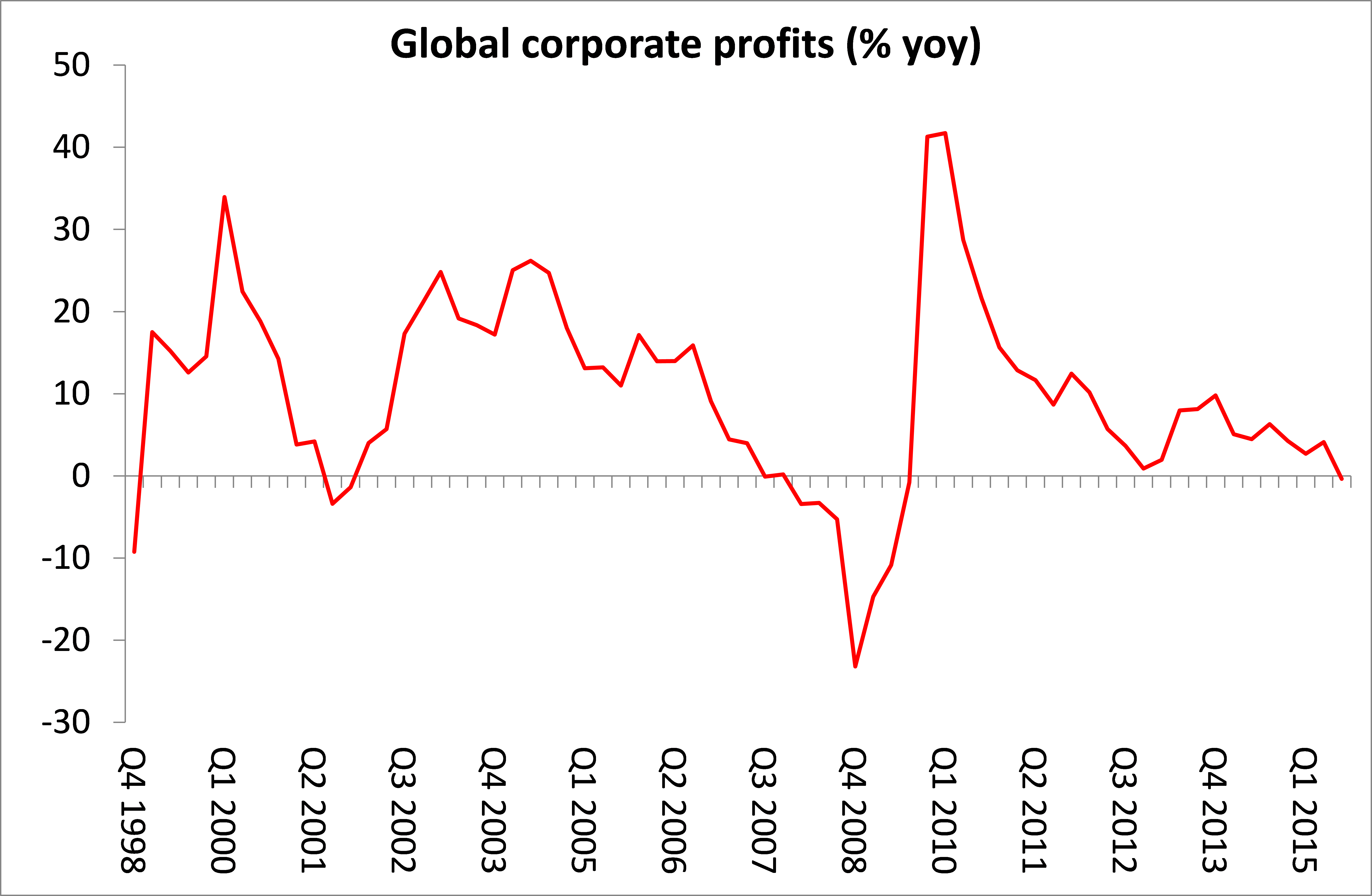

I have discussed the prospects of a new US economic recession in several previous posts. What matters is not the level of interest rates, whether they are too high or too low relative to some ‘equilbrium natural rate of interest’ that US mainstream economists are now arguing about (more on that in a future post), but what is happening to corporate profits and investment. Investment drives employment and incomes and thus economic growth.

I have presented evidence from my research and from others that the profitability of capital and corporate profits generally lead business investment with a lag of 12-18 months, up and down. Currently global corporate profits (a weighted average of US, UK, Germany, Japan and China) have turned negative and US corporate profits are now also falling (on a year on year basis). That suggests that business investment, which has been expanding at about a 5% rate in the US, will start to drop too within a year or so. If that happens, then the US will likely head into recession. But it won’t be China or emerging economies that will be decisive.

The final figure on corporate profits is per cent change year on year, correct?

yes

Is the rate of profit for U.S. capitalists declining? Real wages are still on the decline, right?

Wouldn’t the existing (growing?) ties of capitalist investors and/or production in the U.S. to China affect profitability and, therefore, if not directly, relatedly, China’s slowdown is likely to increase the likelihood of U.S. collapse? In short, hasn’t the “advice” to China to “join the international financial ‘community’”, at least in part, resulted in U.S. and international capital’s downward spiral?

There seems to be a division of opinion within the ranks of the Chinese Communist Party over the currency. On the one hand, the prevailing view seems to have been that the currency needed to rise in value. That is because, they have been trying to shift from an export led economy, to one more pivoted on the domestic economy.

They have been moving towards the establishment of a welfare state for that reason so as to reduce the excessive level of private household saving required to cover the eventualities of sickness, old age and unemployment, and instead to provide collective social insurance. That also requires a higher currency so as to reduce the costs of imported, means of subsistence, such as food and energy.

But, the bursting of the financial bubble, and other concerns have led to an outflow of money-capital, and hot money, which has sent the currency sharply lower. Other sections of the authorities are not unhappy about that, as it means that some of the overproduction can be more easily exported in the immediate term, thereby reducing some of the social pressures that arise if unemployment increases.

The main reason for global financial panic, however, seems to be in reaction to the potential for China to take action to stem the fall in the value of the currency, rather than vice versa. Already, it appears that the Chinese authorities have been bolstering the currency and making good some of the capital outflow, by selling US Treasuries, for example.

If China repatriates significant amounts of these financial assets that it has built up in the last thirty years that will put further upward pressure on global interest rates. US Treasuries have remained stable or risen, despite the Chinese sales, apparently due to safe haven flows, as global investors fear further sell-offs in equities and the other bonds, particularly junk bonds, such as those relating to energy production.

If China raises interest rates to stop an outflow of capital, and raise the value of the currency that will have a further upward ratcheting effect on global rates, and consequent depressing effect on the prices of financial assets. On top of that, the need for money-capital by Saudi Arabia, is indicated by its consideration of a share sale in Saudi Aramco, a sale which some are saying could amount to several trillion dollars, which would have a similarly depressing effect on global share prices, and rise in interest rates.

Yes, I think the Chinese state is split on the Yuan and the mixed signals have led to ‘global market uncertainty’. Likewise on the stock markets (though it is much less important in China), which is still over-valued, with circuit breakers on then off.

I’m not sure about a dramatic devaluation of the Yuan, and its certainly not the medium term aim.

How much of this is a commodity price problem? E.g. Oil Price. And how much is the oil price a reflection of US imperialism aimed at Russia?

Can you please explain why using the “nominal” GDP value is more accurate than the “real” or PPP based GDP value ?

If the scale of capital flight from China and elsewhere continues, and this mostly makes it way west, could this not somewhat off set any expected slump in investment in the US?

The major tools used by the Chinese government – interest rates, money controls, fiscal stimulus financed by taxes or by issuance of debt, stock market regulations – are much the same ones that capitalist countries employ. Industrial policy, too, reminds one of Japan in the thirty years after World War Two. Money rules in a way that it does not in socialist economies. Yet another sign that capital accumulation is largely in control is the attention paid to the profitability of state-owned firms, not to mention the significant private capitals, personified to westerners by Jack Ma of Alibaba. To say that China risks going capitalist is ten or twenty years behind the times.

Rigorous analysis, Michael.

I would appreciate your elaborating on the thought you began to develop in paragraph 12:

“Does a collapse in the Chinese stock market and fall in the value of the yuan mean an economic slump in China? China is not a ‘normal’ capitalist economy. The power of the state remains dominant in industry, in the financial sector and in investment. Yes, the Chinese authorities have opened the economy to the forces of capitalist value, particularly in trade and capital flows, and in so doing have made China much more vulnerable to crises….”

There is a conjunction hanging over these statements. You are implying that the dominant position of the state in industry and the financial sectors has stopped the Chinese economy from going into a meltdown, despite the stock market and currency manipulations. Please confirm and please elaborate on that point.

Thanks,

Alan

see this post and the papers referred to in it.

https://thenextrecession.wordpress.com/2015/09/17/china-a-weird-beast/

Good analysis! This must be connected with the cyclic recession since almost 250 years in the history of capitalism, on the Earth! Solution is not possible in capitalism, as recession takes birth repeatedly in this economic system itself!

Socialisation of means of production, means of subsistence, abolishing the wage slavery, in other words, abolition of private property is the only possible solution!

Reblogged this on Reconstruction communiste Comité Québec and commented:

Une autre analyse scientifique de grande qualité exempte d’idéologie partisane de Michael Roberts. Il nous dresse le portrait exact et précis de la situation économique mondiale et de l’état avancée de la putréfaction du mode de production capitaliste.

– K.M.

These figures show the tremendous expansion of the Chinese economy. But they also show that the US remains the pivotal economy for a global capitalist crisis, particularly as it dominates in financial and technology sectors. In 1998, the emerging economies had a major economic and financial crisis but it did not lead to a global slump. In 2008, the US had a biggest slump in its economic post-war history and it led to a global recession, the Great Recession. In my view, this weighting still applies.

I have discussed the prospects of a new US economic recession in several previous posts. What matters is not the level of interest rates, whether they are too high or too low relative to some ‘equilbrium natural rate of interest’ that US mainstream economists are now arguing about (more on that in a future post), but what is happening to corporate profits and investment. Investment drives employment and incomes and thus economic growth.

I have presented evidence from my research and from others that the profitability of capital and corporate profits generally lead business investment with a lag of 12-18 months, up and down. Currently global corporate profits (a weighted average of US, UK, Germany, Japan and China) have turned negative and US corporate profits are now also falling (on a year on year basis). That suggests that business investment, which has been expanding at about a 5% rate in the US, will start to drop too within a year or so. If that happens, then the US will likely head into recession. But it won’t be China or emerging economies that will be decisive.

You’ve got to take the figures for corporate profits with a pinch of salt. Profits as a proportion of national income are at their highest sustained level since WWII.

Could China bring down the world economy? Of course it could. But people have been predicting that China would collapse for about as long as they’ve been claiming capitalism was stagant.

Well, Bill– if we’re going to take figures for corporate profits with a pinch of salt, then we have to take the statement that “profits as a proportion of national income are at their highest sustained level since WWII” with that same pinch.

Profits are always at “their highest level”– just before they aren’t. Kind of a tautology, no?

Actually as a share of gross valued added, corporate profits both before and after tax have fallen back from their peak at Q3 2014 at 16.1% (before) or 12.2% (after) and, as at Q3 2015, they were respectively 14.9% and 10.8%. True, that’s still high historically but the share has been falling for a year.

http://bea.gov/newsreleases/national/gdp/2015/pdf/gdp3q15_3rd.pdf p16 bottom.

pass the salt.

NO! The rest of the world is pulling China down. Nowcast models show the Chinese economy accelerating to 7.1%, US at 1.5% (and going down) EZ at 2.1% (after almost a decade of depression) JPN at 2.1%, UK at 2.1%, RUS at -1.9%

Surely these growth rates will come down for everyone involved. But it’s not due to Chinese weakness, it’s because of the rest of the world’s weakness that is pulling China’s economy down.

http://blogs.ft.com/gavyndavies/2016/01/10/global-activity-contradicts-market-pessimism/

Very good analysis. Here’s my question:

What is driving up the demand for labour in the US, given that major elements of the economy (sorry for my terminology) are deccelerating ?

I would like to publish this article in Norwegian on my website. What do you say?

Reblogged this on Econo Marx 21.