US GDP figures were revised down last Friday to -1% annualised growth from -0.1% on the first estimate. This was mainly due to inventories. Inventory depletion contributed -1.62% points to growth, compared with the advance estimate of -.57% pts. In other words, American businesses reduced production and ran down their stocks of unsold goods in early 2014 instead to meet demand. The consensus view is that businesses will have to restock this quarter and so the US growth rate will pick up now that the terrible winter is over. We shall see.

Even more interesting was the data released on profits. US corporations have enjoyed an explosion in profits since the Great Recession ended. Corporate profits as a share of GDP reached all-time highs (both before and after tax) in 2013. But in the first quarter of 2014, that changed.

Before tax corporate profits in Q1 fell absolutely on a year on year basis for the first time since the Great Recession. After tax, there was still some rise in profits but at one quarter of the pace of 2012.

I have argued before that there is a good correlation between the movement in the mass of profit and business investment (see https://thenextrecession.wordpress.com/2010/12/29/profits-and-investment-in-the-economic-recovery/). Indeed, US corporate profits growth began to slow before US business investment way back in 2003 and fell absolutely towards the end of 2005, while business investment did not drop until the Great Recession began in 2008. Also profits started to recover one year before investment did. Since the end of the Great Recession profit growth has dropped from its heady heights at the end of 2009 and has steadily slowed towards zero now. Business investment growth has followed a year later. So profits lead investment – they call the tune under capitalism. If that’s case, business investment could also start falling absolutely by this time next year.

Now it may be that the drop in profit recorded for Q1 2014 is just a blip caused by the bad weather that hit the US during the early part of 2014. This is what mainstream economists say. The consensus is that growth will recover sharply in the current quarter that we are now in and the second half of this year will see 3%-plus annualised growth. Again we shall see.

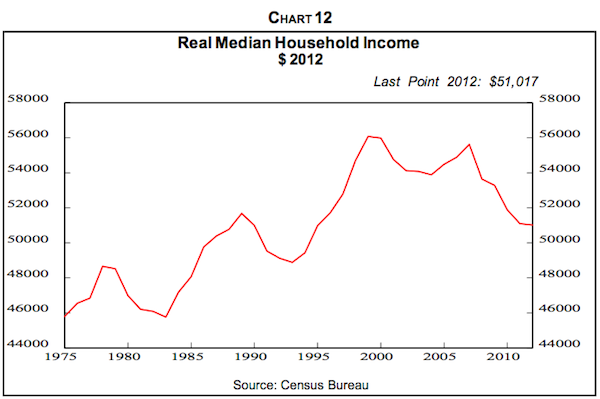

Since the Great Recession, American corporations have sucked up all the new value created by the labour force while average American households continue to take a hit on real income levels. The purchasing power of the majority of Americans has not only stagnated since the recovery began five years ago – it has actually declined. At $53,000, the median US household is more than $4,000 – or 7.6% – poorer in real terms than it was at the start of the recession in 2008, according to Sentier Research.

The great debate about inequality of income and wealth provoked by the book from Thomas Piketty

(see https://thenextrecession.wordpress.com/2014/05/24/piketty-data-and-the-scientific-method/)

has recently centred on whether inequality of wealth and income really has risen in the last 3o years in the US. It seems that Mark Carney, the governor of the Bank of England, reckons it has: “Within societies, virtually without exception, inequality of outcomes both within and across generations has demonstrably increased.” Whatever the evidence, it is clear that US inequality of income has sharply risen since the Great Recession ended, with the profit share rocketing and average real incomes falling.

The US now has a lopsided economy similar to that in the UK. During the first four months of this year, the sales of the top 1% most expensive US homes – those worth $1.67m or more – have increased by 21%, according to Redfin, the real estate group. It followed a gain of 35% in 2013 – led by the gilded San Francisco Bay area, where the priciest homes start at $5.35m. But sales of the bottom 99% of homes have fallen by 7.6% so far this year. The fall in average household incomes is reflected in falling sales at shops for the majority. At Walmart, the supermarket chain, revenues dropped by 5% in Q1 2014. At Sears Holdings, sales are down 6.8%, while the discount stores are getting higher sales as Americans search for bargains: the leading retail discounter’s sales rose 7.2%.

The US stock market hit yet another all-time high last week as cheap money from the Fed and expectations of further increases in profits encouraged rich investors and institutions to plough more cash into stocks and bonds. That will change if America’s profit explosion has really ended.

Michael, if real income has fallen and profits and investments are lower than this time last year, does that mean that the US stock market is in a speculative bubble? Are we about to see the type irrational exuberance from wealthy investors and institutions that we saw from average investors prior to the bursting of the dot com and housing bubbles?

Yes, I think the stock market is in a speculative bubble, as measured by Tobin’s Q. I have done a post or two on this.

Isn’t the stock market always a “speculative bubble”? That’s its function, after all– to speculate. Futures, options, equities– all speculation, all the time.

Was the stock market a speculative bubble in 1997? 2003? Speculation goes both ways, up and down, so I don’t see the point in wondering if the stock market is “accurately” expressing valuations. That’s not what it’s supposed to do; and that’s something it cannot do– no more than prices of any commodities are determined by the value of the individual commodity.

Reblogged this on Econo Marx 21.

Profit margins are at all time highs, and this cannot last. So to the implied question concerning market bubbles, as well as bubbles in other speculative asset classes, the glib answer is: of course the “end,” so to speak, will not be pretty. The key question is political: will the working and middle classes, in developed and developing economies, continue to accept the brunt of capitalism’s resolution of its latest crisis? Or will the burden be shifted to the ruling elite? If so, to what extent? And how will they respond? As matters stand, they have to be tickled pink.

I definitely don’t see the blame being shifted to the ruling elites. Propaganda wise, the ruling establishment has all ready got in front and currently control the story being told, so immigrants, Jews, big government but ironically not big business outside of oil, and ‘corrupt ‘ politicians are feeling the heat here in the US. In Europe its all the usual suspects along with gays. Somehow activist have to retake the story being told via our own propagandizing otherwise we all lose.

To what extent has the effect of exchange rate movements been taken into account, on both sides of the debate, in calculating profit rates? My impression is not very much, although the effect can be considerable. One would expect that the slow secular decline of the USD since the collapse of Bretton Woods has biased the earnings of US multinationals upwards while the recent decline in US profitability seems attributable in part to dollar strength since the Fed announced the tapering of QE.

http://www.investing.com/analysis/about-those-'eternally-rising'-corporate-profits-215271

What “slow secular decline” since the collapse of Bretton Woods?

What “recent decline in US profitability” are we talking about? Are we talking about the overall secular trend since 1970? The recoveries of 1993-1998, or 2003-2007 which did not exceed the peak of 1969-1970? Or more recently, the recovery in the rate of profit since 2009? Or the single quarter decline recently reported and attributed to the impact of weather?

Dollar strength since the tapering of the QE? What dollar strength? Brazil’s real has appreciated. Japan’s yen has depreciated not because of the tapering, but because of Abe’s dedicated efforts… so exactly what are we talking about?

As for Hugh’s comments— how then to explain the increasing profits during the 1993-1998 period, with a rising rate of profitability, more or less to 2000, when the dollar-euro rate was the reverse of what it is now– with the euro exchanging for about 75 cents?

1. “What “slow secular decline” since the collapse of Bretton Woods?”

The trade-weighted exchange rate of the USD is approx. 25% lower than in 1973. See:

http://research.stlouisfed.org/fred2/graph/?chart_type=line&width=800&height=480&preserve_ratio=true&s%5B1%5D%5Bid%5D=TWEXMMTH

2. “What ‘recent decline in US profitability’ are we talking about?”

First quarter profits were the weakest they’ve been since Q3 2012. “What we saw this earnings season was anemic growth …estimates for the current period (are) starting to follow the trend that has been in place for almost two years now – they are going down. This is a trend that has been in place for almost two years now, with the pace expected to accelerate further in the coming days.”

http://www.zacks.com/commentary/32690/another-weak-earnings-season-coming-to-an-end

3. “Dollar strength since the tapering of the QE? What dollar strength? Brazil’s real has appreciated. Japan’s yen has depreciated not because of the tapering, but because of Abe’s dedicated efforts… so exactly what are we talking about?”

While the USD has traded in a narrow range against the currencies of the major developed countries over the past year, it has appreciated strongly against major emerging market currencies like the Indian rupee, Russian ruble, South African rand, Indonesian rupiah – and the the Brazilian real. While these currencies have recovered some of their value, they are still well below the rate they were trading at against the dollar prior to the Fed indicating last May that it was paring down its bond purchases, provoking an outflow of capital from these countries. The real, for example, is still 10% lower than the dollar over this period, though it rebounded from its low of 18% last August, as did the other currencies with the exception of the ruble which has been hit by the Ukraine crisis.

http://www.federalreserve.gov/Releases/H10/hist/default.htm

1. How does that amount to a slow secular decline of the US?

2. You’re referring to a single quarter, and presenting that as a trend? Maybe, and then again maybe not. After tax corporate profits have increased every year since 2009, are above the 2006 previous peak, and were higher in 2013 than 2012. See the BEA NIPA tables. I don’t know what Zack is referring to when he refers to “another weak earning season,” and I suspect he doesn’t either.

3. Yes, the dollar has appreciated against the rupee, the rupiah, the rand, and the real. And those currencies, or those markets, account for exactly how much of US overseas profits? Of US foreign investment?

My reference was to the slow secular decline (-25%) of the dollar, not the US, a separate question. In any case, that comment was incidental to my original post which queried whether FX movements enter into calculations of the rate of profit by mainstream or heterodox economists. Seems to me this is a significant consideration which would skew profit rates one way or another if taken into account, no? In the case of the US, wouldn’t the historic reported rate of return be inflated if it were indeed the case that the trade weighted dollar index had declined since currencies were allowed to float freely after Bretton Woods? Perhaps Michael, yourself, or someone else could enlighten me about this.

In the scheme of things, I think exchange rates do not “artificially” change rates of profit. Like all prices, exchange rates serve to distribute the total surplus value among the contending capitals.

Do exchange rates make a real difference?– sure do. Look at Japan’s distress when the yen was below 85 to the dollar. But this amounts to a real mechanism for redistributing profit.

Remember, it is never the case that any single, or national, or even transnational capitalist enterprise claims, or realizes, the surplus value it throws into the market. The claims are on the total surplus value thrown into the markets by all sectors, all enterprises.

So were US profit rates “artificially” inflated by the depreciation of the dollar in the 2004-2008 period? I don’t think so. But was there a real benefit to the depreciation of the dollar? Sure thing. Is there any point to “recalculating” profit rates “as if” exchange rates were “pushed back” to what they were in 2000? I doubt it. I have the same reluctance to “re-baselining” this as I do, in general, to notions of “fictitious capital” explaining or masking the rise or decline of profitability; or thinking that the stock market is anything other than a speculative bubble at any time.