I have been attending a two-day workshop on the current state of capitalism from a Marxist view point. This was organised by Alex Callinicos at King’s College, London University who managed to collect a number of Marxist scholars from the UK and Europe to come and present some papers to be followed by discussion and debate among participants.

The first day started with a discussion on whether Marx himself had a theory of crises under capitalism and, if so, what was it? Readers of my blog will know that this is a controversial issue and scholars like Michael Heinrich consider that Marx never really developed a clear theory of crises and also that Marx’s law of the tendency of the rate of profit to fall had nothing to do with crisis theory (see my posts, http://gesd.free.fr/mrhtprof.pdf

and

https://thenextrecession.wordpress.com/2015/05/19/the-two-michaels-heinrich-and-roberts-in-berlin-dogmatism-versus-doubt/).

Professor Michael Kratke kicked off this discussion with a paper entitled “Marx’s theory of theories of crisis” (Kraetke Marx’s theory or theories of crisis). As an eminent scholar on Marx’s writings in their original manuscripts and on the history of Marxist crisis theory, MK adopted what you might call a ‘middle way’. According to MK, Marx did not stop trying to develop a theory of crisis and he made progress on it; but on the other hand, MK reckons that Marx did not consider his law of the tendency of the rate of profit to fall as part of that theory. You could find several different versions of crisis theory in Marx, but not the LTRPF.

MK says that, for Marx: “The tendency of the rate of profit to fall does not matter at all! On the contrary, Marx is explicitly criticizing the view, as he finds it in Adam Smith, that a fall in the ‚general rate of profit would lead to crises (hence, the often quoted statement that there are no permanent crises”. In my view, however, Marx was really criticising Smith’s description of the falling rate of profit as being a long-term gradual fall, in contrast to his own view based on his law which led to cyclical convulsions in capitalist production as the rate of profit fell. Moreover, his own explanation of the falling profit rate was entirely different from Smith‘s.

Anyway, in MK’s view, the LTRPF was irrelevant to Marx’s theory(theories?) of crisis. And he never mentioned it in any of his studies of capitalist crises in the 1860s, 1870s or at the start of the Long Depression of the 1880s. I have dealt before with this argument about Marx not mentioning the law in previous posts dealing with Michael Heinrich‘s view (see above). But what MK did say was that he did not agree with Heinrich that Engels had distorted or misrepresented Marx’s view on the LTRPF as propounded in Chapters 13-15 of Volume 3. MK reckoned Engels had indeed made a faithful job of editing. Also MK mentioned that Marx had begun to work on understanding the nature of depressions rather than just slumps in his last studies in the 1880s. As for this increasingly stale controversy on whether Marx changed his view on the relevance of the law on profitability and did not tell Engels; and what happened with all the drafts of Marx’s manuscripts, I can only refer you to the excellent scholarship by Fred Moseley here (Introduction3 and FRP-FRL).

Lucia Pradella dealt with a different issue in Marx’s theory of crisis and took a different angle (Pradella Workshop Abstract). She had looked closely at Marx’s writings in the 1850s on colonial expansion into India etc and found that Marx’s theoretical model was to consider captialism as one world economy and not a series of national capitals in order to understand how the capitalist mode of production led to colonial/imperialist expansion. And at this level of abstraction, Marx appeared to conclude that colonial expansion was part of the tendency under capitalism for the organic composition of capital to rise in the mature economies (its mirror image being a fall in profitability under the LTRPF) and thus colonial expansion was a counteracting tendency to the law of falling profitability.

Gomes de Deux presented a paper on Marx’s Notebooks (Leonardo G Deus Et Al Marx Notebooks) prepared in 1868 and 1869 that revealed that after Marx finished the manuscripts that became Capital, he continued a broad study of crises, highlighting an emerging transformation of capitalism through leading industrial sectors (railways), financial innovations (such as limited liability firms and new types of shares and titles). Sparked by the crisis of 1866, Marx’s investigations on stock exchanges and related structural changes seem to have given him a new perspective from which to investigate changes in capitalism. But again, there was no evidence (either way, if you like) that Marx changed his view on the law of profitability.

In the next session, we had papers on the nature of crises from a Marxist point of view. Alex Callinicos and Joseph Choonara presented a searching critique of the views of Professor David Harvey on Marx’s theory of crises (Callinicos & Choonara How Not to Write about the Rate of Profit). Readers of this blog will know the debate that has taken place between Harvey and myself and others like Andrew Kliman on (yet again) whether Marx’s law of profitability is logical and empirically proven and relevant as a theory of crises (see my posts,reply-to-harvey). Callinicos and Choonara showed that Harvey used to have a more open-minded view on these issues in his earlier work but now he has hardened his rejection of the law and looks instead to various and vague ‘multicauses’ for crises, to the detriment of his analysis, in their view.

Guiglemo Carchedi presented a paper that sought to show that Marx’s law of profitability was relevant to crises, and in particular to the Great Recession (Carchedi Presentation). This was an empirical analysis and revealed that post-war crises in the US occurred when there was a fall in new value created (profits and wages combined). This can happen even if the rate of profit had been rising before. As soon as the organic composition of capital starts rising more than the rate of surplus value, profitability will fall and so will new value. This conformed to Marx’s law and shows a causal connection between the law and slumps under capitalism, in Carchedi’s view.

Jan Toporowksi presented a paper in which he argued that the real cause of the Great Recession was not a credit-driven housing bubble as most think, but actually the financialisation of the non-financial corporate sector through bond issuance (Toporowski THE CRISIS OF FINANCE King’s May 2015). This had led to over-indebtedness that, at a certain point, could not be serviced. So the hidden cause of the Great Recession was excessive corporate debt, not the sub-prime mortgage ‘house of cards’. This is an interesting idea, if not entirely convincing at least for the GR. I actually think that this could be the Achilles heel of the next slump, as evidence shows that corporate sector debt has not shrunk in any way since the end of the GR, on the contrary. So the build-up of corporate debt could be a trigger for a new slump in both advanced and emerging economies.

The final day brought to a head the divergent views within the workshop on the nature of capitalist crises and their cause. Gerard Dumenil, the well-known economist of XX in France and joint author of many books and papers with Dominique Levy, had already expounded his view on the previous day that capitalism is in a ‘neo-liberal crisis’, a new structural stage in capitalism since the 1970s (Dumenil Neoliberalism). While the great crisis and depression of the 1880s and 1890s could be attributed to one of falling profitability (a classic crisis, if you like) and so could the ‘crisis of the 1970s’ (whatever that was), neither the Great Depression of the 1930s nor the Great Recession could be. They were a product of the establishment of ‘financial hegemony’, or if you like the dominance of the financial sector over the productive sector in capitalism. The neoliberal period is characterised by a sharp increase in the inequality of wealth and income, as the very rich (the top 0.1%) engaged in a “crazy chase to become rich” at the expense of the rest of us and eventually of capitalism itself. Dumenil illustrated this for the 20th century in the US with an excellent graph (see below).

US average income per household in seven fractiles – inequality in 1920s and 1930s, equality in post-war period; then inequality again

In the neoliberal period, we have a new exploitation of the poor through deregulation of mortgages, the expansion of derivatives, leading to the super bonuses of the top executives. In Dumenil’s view, the neoliberal crisis comes about when this crazy venture can no longer be sustained. So the neoliberal crisis and that of the Great Depression in the 1930s were really ones of greed and class exploitation and had nothing to with falling profitability, which was rising not falling.

What worries me about this analysis is several. First, why did the crazy drive for money start just after the ‘classical crisis’ of falling profitability in the 1970s? Was not this neoliberal period a reaction by capitalism in trying to reverse falling profitability through the classic counteracting factors that Marx had outlined in the law: rising rate of exploitation, cheapening of constant capital through new technology, or by just slowing new investment and above all by a switch to investing in fictitious capital rather than in the productive sectors, as Carchedi had shown the day before?

Second, I have considered these arguments of Dumenil before (see my post of over four years ago

(https://thenextrecession.wordpress.com/2011/03/03/the-crisis-of-neoliberalism-and-gerard-dumenil/)

and I have also looked at the rate of profit using Dumenil’s own data for the Great Depression and it looks like a ‘classic’ profitability crisis to me – profitability had peaked in 1924 in the US, well before the 1929 crash (see my post). As for the neoliberal period, I have argued that profitability rose from the 1980s too, but it stopped rising in all the major economies in the late 1990s (see my paper) and entered a downphase that laid the basis for the Great Recession later, as in the Great Depression. And Dumenil’s own figures confirm that for the US too.

Behind Dumenil’s neoliberal crisis theory is his view that, in effect, that there are now three classes in captialism: workers, capitalists and managers. And it is the managers who now hold the ‘balance of power’. In the neoliberal period they have taken the big bonuses and supported finance capital against labour. No change is possible until the managers come over to the side of labour. So we have a political theory of crises rather than an economic one. And it seems to call for class collaboration as a way out of this crisis. I doubt Marx would have agreed.

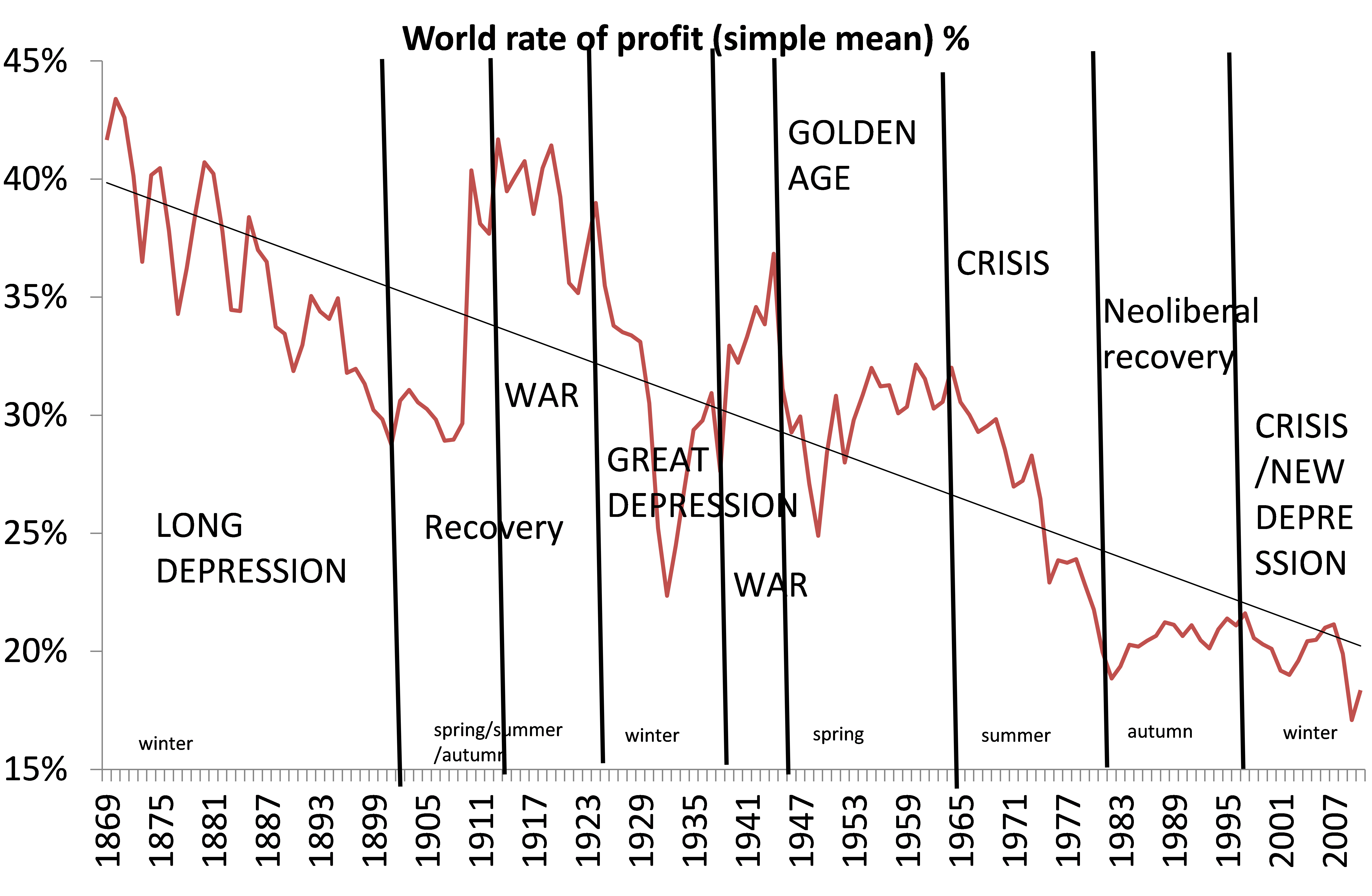

In my own paper (Capitalism workshop presentation), I tried to identify that the neoliberal period had really been a very weak recovery within the long-term decline of the profitability of capital in the major economies. Using the work of Esteban Maito, I showed that there has been a secular decline in profitability over the lifetime of capitalism, interspersed with upturns, either caused by crises reducing the value of capital, or by periods of counteracting factors, as in the neoliberal period. But these upturns come to an end then the law works to drive down profitability and create new slumps. Crises occur, I argued (in a similar vein to Carchedi) when falling profitability leads to a fall in the mass of profit and it is not long after that investment and GDP also slumps. Contrary to Keynesian/Kalecki theory, profits lead investment and investment leads employment and consumption – something that Dumenil confirmed in his own data that showed consumption was not a factor in the Great Recession; it was the slump in investment.

My data on the changes in US profits leading to changes in investment were challenged by Jim Kincaid and Pete Green in the discussion. They argued that how could the mass of profits rise and the rate of profit be falling – this must be contradictory. Also the causal correlation between profits and investment found by Tapia Granados, that I always quote (Does investment call the tune – RPE), was only 44%. And that’s hardly conclusive of a causal connection.

Well, since the workshop, I went back to look at my data. I found that if I measured the correlations between the rate of profit, the mass of profit and investment using official US data for the years 2000 to 2013, that there were very high correlations between profitability, profits and investment. First, the correlation between changes in the rate of profit and investment was 64%; second, the correlation between the mass of profit and investment was 76%; and third, the correlation between the rate of profit (lagged one year) and the mass of profit was also 76%. It was necessary to lag the rate of profit as the data are annual for that not quarterly.

Anyway, that provides some more support for the Carchedi/Roberts papers. Tapia Granados has a new paper out that also provides increased statistical support for these causal connections. His new data show that (a) investment is not autonomous, profits raise future investment; (b) investment tend to decrease future profits; and (c) little evidence is found that government spending may stimulate future investment and in this way may pump-prime the economy. Now that the latest data on US corporate profits are out for Q1 2015, I shall return to these issues in a new post.

The main attack on my view of the causes of crises, as based on the LTRPF and its counteracting factors, was delivered by Professor Kratke in the summary of this session and by Professor Dumenil in his comments. Dumenil attempted to rubbish Esteban Maito’s work (Maito, Esteban – The historical transience of capital. The downward trend in the rate of profit since XIX century). “It was a joke!” Dumenil said he and his colleague Levy were world experts on data; they looked at hundreds of bits of data every day (apparently unlike the rest of us). And so he knew it was impossible to get an ROP for the world going back to 1850s as Maito has done. He tried it for just France and could not do it. So the data “from this Argentinian” were a joke, or a concoction. We cannot prove there is a long term secular decline.

I replied that Maito’s data for the US were based on Dumenil’s own (very accurate!) data and so presumably that was not a joke. Using national statistics, surely you could do that for other countries with the usual caveats and gaps? Anyway, the data all showed the same trend direction as Dumenil’s US data. By the way, Maito does not do France as well; so presumably he had the same problem as Dumenil on that country. Indeed, Maito provides a detailed explanation of his sources and methods in his paper including excel files and he intends to publish even more detail on his statistics for scholars to consider (according to a recent email that I have had from him). So that will be more data for Professor Dumenil to absorb in his expert way.

Again, I found the argument against the role of profitability in crises presented by Professor Kratke and others somewhat weird. Dumenil at least recognised that the “crisis of the 1970s” was a ‘profitability crisis’. At the workshop I asked: was anybody in the room that thought that the ‘1970s crisis’ (whatever that was) was not due to falling profitability? And nobody said anything.

The debate seemed to end in a separation between those who reckon that Marx did have a theory of crises and those who say he did not. And between those who consider Marx’s theory of crises was not something as ‘crude and fundamentalist’ as Marx’s law of profitability but was much more ‘complex, multicausal (even Keynesian)’ and those who remain ‘dogmatically’ committed to the law. I think this was an artificial divide. After all, Professor Dumenil did support the view that falling profitability was the cause of the depression of the 1880s, when Marx was alive; and the crisis of the 1970s. And those of us who support the law of profitability also recognise the role of credit/debt (fictitious capital) in triggering crises (see my papers, Amsterdam and Debt matters.Amsterdam presentation 140314 and Debt matters)

There was an interesting and innovative paper presented at the end by Eduardo Alberquerque that may be sets the scene for future capitalism (Albuquerque Workshop Paper). Alberquerque, using new sources, showed that there were new leading technology-driven sectors in capitalism that could eventually lead the next stage of capitalist development. In my view, there is no permanent crisis of capitalism. It moves in cycles, as my paper argued. So at a certain point, a revival in capital accumulation will begin. Profitability will recover and these new technologies will be utilised. But that probably won’t happen without another huge slump before the end of this decade. I say that because profitability is still too low in most economies and debt deleveraging has still some way to go from the build-up prior to the Great Recession, (I’ll be coming back to this issue in a future post). If capitalism does enter a revival in the 2020s, it will do so on the basis of robots and AI. And that poses a whole new stage in capitalism and in the nature of crises. Again I shall take up the issue of robots and AI in a future post – if I ever get to it!

I think it is time for a real update on Marx! The connection between laws of motion of capitalism and crises, depressions and long waves or cycles, included. http://http-server.carleton.ca/~karmstro/bios/Marx.htm

Thanks for the great summary, Michael – as a mere lawyer I do not have the competence to work through the data sets though the two days were fascinating and instructive. I still think that Part 3 of Vol 3 of Capital is on to something, despite what Michael Heinrich says in Chapter 7 of his generally excellent Introduction. It was a shame he wasn’t there too to defend his corner.

According to Ernest Mandel there is no automatic escape from a long depressionary wave. I agree, it’s going to take more then a deep slump to get us back to Spring Time for capitalism. Maybe Ken Macleod’s Big Deal described in his novel Descent will do it but that involved the states nationalizing the financial sector.

Simon, I agree. if you put the LTRPF to the forefront than you hope that the countertendencies will do the job. At the moment I see QE, trade and currency wars and mergers and take-overs, but hardly any recovery…….

Thank you for the summary and all the presentations.

Lots of interesting reading material!

“And at this level of astraction, Marx appeared to conclude that colonial expansion was part of the tendency under capitalism for the organic composition of capital to rise in the mature economies (its mirror image being a fall in profitability under the LTRPF) and thus colonial expansion was a counteracting tendency to the law of falling profitability.”

Except, of course that in Capital III, Marx specifically sets out the way that although real wages may be much lower in developing economies, both the rate of surplus value and the rate of profit will generally be lower, because of much lower levels of productivity!

In Capital I, Marx sets out the way that this difference in productivity between different economies is like the situation where a firm adopts a new machine or technology, resulting in the labour it employs acting like “complex” labour compared to the labour employed by other firms. At an international level Marx says, this means that there is a modification of the Law of Value.

In Capital I, examining National Wage rates, Marx uses this analysis to show that wages in Europe were 50% lower than in the UK, and yet the UK was out competing European industries by large margins. The reason, as marx shows by a series of tables is the difference of the amount of capital standing behind the UK workers, compared to European workers, which significantly raised their productivity compared to European workers, and thereby made them more profitable, because although their wages were higher – nominally and in terms of real wages – the rate of relative surplus value was higher in the UK, and because the higher productivity meant that capital was released, due to a higher rate of turnover of capital, and because, as marx sets out in Capital III, Chapter 6, this increase in productivity caused by the introduction of new technology, reduces the unit cost of fixed capital – it also tends to bring economies of scale in respect of other costs too.

This, in fact is why despite very low levels of wages, capital in developed economies has always been invested in its vast majority in other developed economies and not in developing economies, a fact that would be incomprehensible if the low wages, and low organic composition of capital in developing economies, resulted automatically in a much higher rate of profit.

In the time Marx was doing the analysis communication was not as it is today and the jet engine hadn’t been invented.

It is a different world now, and capitalist firms have relocated to make higher profits and increase exploitation.

Though of course colonial expansion in the past was a grand scheme of murder, theft and exploitation.

But, the majority of investment by developed capitalist economies continues to be in other developed capitalist economies not in undeveloped economies. The fact of better communication and so on does not change the fact that in many developing economies, a lack of adequate infrastructure and so on, keeps the level of social productivity low, even if in parts of the economy – enterprise zones, other coastal entrepots etc – modern industries have been developed with high levels of productivity.

The concept of “increase exploitation” has to be treated with caution too. Such investment is “increased exploitation” to the extent that the much higher levels of productivity raise the rate of surplus value, compared to traditional handicraft or manufacture, but this necessarily goes along with much higher living standards, as Marx describes.

A look at the rise in living standards in Asia over the last couple of decades, and now in Africa demonstrates that quite clearly.

this is not me Henry, it is somebody else…..

and that is not me henry, it is somebody else!

There are a lot of made in China labels on the goods I buy, so something has gone on and lower wages seems to be a big part of the picture, production has relocated. So perhaps it is the wrong question to look at this in national terms rather than in capital terms.

We should also factor in things like market share. Toyota relocated to the UK because the EU wouldn’t let them sell in Europe unless they had plants here.

And what type of FDI are we talking about when we saw the developed nations invest in other developed nations? What is the nature of this investment, how is it calculated and what is left out of the picture?

All seems the wrong approach to my way of thinking.

@Edgar,

Wages are much lower in the Central African Republic than in China, or even than in China in 1980, but capital invested in China not the CAR. The reason, is quite simple, as marx describes. He quotes Adam Smith that where wages are low, the price of labour is high.

By that he means that it is nearly always the case that where wages are low, this is attended by low levels of productivity. When wages rise, it causes capital to seek out new labour-saving technologies to replace labour, and the higher productivity reduces the portion of wages in the cost of the product.

It was only when China was able to provide the conditions for capital to invest large amounts of capital in areas of production where the organic composition of capital was already high, i.e. where there was already high levels of productivity, that it became profitable to invest that capital there. The lower wages were then just a bonus compared to the higher wages of US or European car workers, for example.

There is also India, Vietnam, Bangladesh etc etc etc.

In the 1980’s I set up a engineering business with a friend and we used multi spindle machines to make hydraulic fittings, my friend now spends much time in China, India and elsewhere selling those 50 year old machines to the Chinese etc!

When productive capital relocated to new areas there were probably numerous factors involved but no one will convince me that the ability of capital invested in lower wage areas to out compete productive capital in the West wasn’t a major factor in a reconfiguration of the world economy. I know we were being undercut by cheaper labour and I know this was the main reason we could not continue as we were.

I am literally shaking my head in disbelief that anyone would deny this reality!

Edgar,

No one is denying the reality that in two cases where the same technology is used, and so the same productivity is possible, the place where wages are lower will be more profitable! The point is that in many cases, the productivity in each case is not the same, and so the lower wages do not sufficiently offset the lower productivity so as to create higher profits.

I set out Marx’s example of the more profitable UK textile industry compared to the European industry, despite the latter having 50% lower wages, and poorer conditions, but marx also describes the same thing in relation to India.

Indian wages were at subsistence levels. Prior to the rise of Britain as Workshop of the World, India was the world’s leading textile producer and exporter, accounting for around 25% of world output in 1800, if my memory serves me right.

Yet, as soon as Britain began to introduce steam engines into its production, so that it could power spinning machines, and looms with numerous spindles and so on its productivity rose so sharply that it quickly undercut Indian textile prices (there was also the matter of British tariffs against India whilst this investment was being undertaken), so that Britain became by far the global supplier of cheap textiles, whilst massive profits were obtained from the production, and the Indian village production disappeared.

The growth of investment in parts of China on the basis of large scale, high productivity production, indeed also creates conditions under which other production takes place. When the various gold rushes took place, for example, it was always accompanied by businesses providing sex, booze and other vices on a small scale.

In the same way, the City of London, with the high incomes obtained by some, also creates the environment not just for the above kinds of small scale business, but others such as the provision of coffee shops, fast food restaurants and so on, which pay low wages, and where high levels of productivity are less important, because no one is going to drive 50 miles to a much more productive and cheaper coffee shop or eatery.

If low wages trumped investment in labour saving technology for the production of higher rates of profit, capital would never have bothered introducing the technology.

Boffy: “It was only when China was able to provide the conditions for capital to invest large amounts of capital in areas of production where the organic composition of capital was already high, i.e. where there was already high levels of productivity, that it became profitable to invest that capital there. The lower wages were then just a bonus compared to the higher wages of US or European car workers, for example.”

Not true; historically inaccurate; materially mistaken. That is precisely not why or how FD investment in China was initiated. FDI in China follows Deng’s “Four Reforms” policy of 1979, which was deliberately and openly a “low-wage policy”– that is to say China marketed its massive and cheap labor supplies to the advanced capitalist countries.

Initial investments, and still a major portion of production, in China were highly focused on the “low organic composition” “snap and pack” assembly operations, with capital and capitalists from Taiwan, and Japan transferring production in these sectors to China.

China was an import and reexport economy; importingt the more technically intensive components, and exporting the assembled commodity. Previous studies showed that China was accruing only $5-$10 of the $180 (app) of the “value added” in Iphone production. Have to search my notebooks for the exact numbers, but I think I’m pretty close.

The low wages were the critical attraction– China’s productivity, value and volume output per labor hour, was and remains below that of the advanced countries in steel, in cement, in coal, in rail transport– in just about any area you want to look at. For all its attempts to “move up the value chain,” — which is simply another expression for more technically intensive production– in telecommunications and electronics and even in “heavy machinery”– i.e. high speed trainsets, the “climb” has been slow and quite arduous.

Automation, increasing the organic composition of capital, in both domestic and FDI industries has been driven in large part by the 25% or so appreciation of the yuan in the last 8 or 9 years.

Boffy: “This, in fact is why despite very low levels of wages, capital in developed economies has always been invested in its vast majority in other developed economies and not in developing economies, a fact that would be incomprehensible if the low wages, and low organic composition of capital in developing economies, resulted automatically in a much higher rate of profit.”

Absolutely, positively correct. US FDI is overwhelmingly concentrated in other advanced countries where productivity, and total social productivity (transportation and communication networks) are higher.

If I recall correctly, I think only Mexico among the “less developed capitalist” countries makes it into the top 5 or 10 destinations of US outward FDI, but I haven’t checked the numbers in about 8 years.

Doesn’t mean that capitalism doesn’t always seek a higher profit; doesn’t always see an advantage in cheaper labor; but cheaper is not immediately nor always identical with the higher profit.

Where capitalism can combine the most advanced technology with the cheaper labor with stable and productive logistical networks, it does and it will…but in so doing capital necessarily initiates the process where a) wages will begin to rise b) profit margins will “tend” towards the general rate of profit.

Re the Albuquerque paper which I just skimmed (thanks for posting the papers/presentations): I find it has nothing to do with the Marxian debate. However, it does try to say something about what is going on now in global capitalism whereas the inner-Marxian debates about the tendency of the rate of profit in his theory become liturgy. Look around. First condition for the rate of profit to fall is that less surplus value is created or is perhaps not created where it looks as if it were created. The good old debate about productive, i.e. surplus-value producing on the one hand, vs. surplus-value conditioning and realising sectors and consumption on the other, should be resuscitated. Otherwise the rate of profit-debate does not make sense. Today, the question then is: does a robot produce surplus value? No, it is part of fixed capital, I should say. And if ‘we’ are going in that direction, less surplus value will be created, therefore of course the rate of profit will fall.So the question is whether there is empirical tendencies in that direction. I just think that the data have to be treated completely differently and not as add-ons across sectors.

“First condition for the rate of profit to fall is that less surplus value is created or is perhaps not created where it looks as if it were created.”

No it isn’t! That was precisely the argument that Smith, Ricardo, Malthus and others promoted, and which Marx demolished, by showing that not only is a falling rate of profit compatible with a rising mass of surplus value, but the law of the tendency for the rate of profit to fall itself requires that the mass of surplus value is rising!

“but the law of the tendency for the rate of profit to fall itself requires that the mass of surplus value is rising!”

This is interesting. My understanding is that the rate of profit is s/(c+v), which in my simple understanding suggests that movement in any of these 3 elements will change the figure.

Your comment above would suggest this is not the formula and something else is going on?

#ChrisH,

No that is the formula for the rate of profit – though, of course, Marx and Engels make clear that this is the formula for the rate of profit for one turnover period, and go on to demonstrate that this is only the same as the annual rate of profit if there is only one turnover period per year. In that case, s/c+v is also the same as p/k, the profit margin, which tends to be the rate of profit that is referred to, and differs markedly from the annual rate of profit, the two often moving in opposite directions.

The point that Marx makes in Capital III, and in Theories of Surplus Value, where he demonstrates that a consequence of the falling rate of profit is a rising mass of surplus value, is that you only get the tendency for the rate of profit to fall, if you get rising social productivity.

But, you only get rising social productivity on a significant scale if there has been an increase in the amount of new technologies introduced into the economy. Unless that is the case, you can have as much accumulation of capital as you like, and it will not create the conditions for the law of the tendency for the rate of profit to fall, because that law requires a rising organic composition of capital, which can only come about by that rising social productivity. This is Marx’s point in Capital III, Chapter 15, where he states,

“Growth of capital, hence accumulation of capital, does not imply a fall in the rate of profit, unless it is accompanied by the aforementioned changes in the proportion of the organic constituents of capital. Now it so happens that in spite of the constant daily revolutions in the mode of production, now this and now that larger or smaller portion of the total capital continues to accumulate for certain periods on the basis of a given average proportion of those constituents, so that there is no organic change with its growth, and consequently no cause for a fall in the rate of profit.”

In fact, under these conditions, the annual rate of profit may well rise, because the turnover of capital will rise. If I employ two machines instead of one, there is no change in the organic composition of capital, because I employ twice as many workers, and twice as much material, so the relation between the constant and variable capital remains the same. But, because I produce the output twice as fast, the quantity required for the working period is produced in half the time, the output is sent to market, and the circulating capital is turned over in half the time, so the annual rate of profit is doubled.

What does arise under these conditions, however, is that more and more labour-power gets employed. If I employ two machines instead of one, I now employ twice as many workers. So, if accumulation continues on this basis unless the labour force grows by more than the increase in the demand for labour, which this accumulation brings about, sooner or later, the available labour force begins to get used up, the demand for labour rises relative to the supply, and wages rise.

As Marx puts it,

“Given the necessary means of production, i.e. , a sufficient accumulation of capital, the creation of surplus-value is only limited by the labouring population if the rate of surplus-value, i.e. , the intensity of exploitation, is given; and no other limit but the intensity of exploitation if the labouring population is given.”

So, the annual rate of profit can be growing here, because the rate of turnover is rising due to the accumulation on the old basis, whilst the rate of profit s/c+v or p/k is being squeezed, because wages are rising, and the rate of surplus value is falling.

Marx demonstrates in numerous places in Capital III, and Theories of Surplus Value that if the conditions for the Law of Falling Profits exist – i.e. rising social productivity NOT profits being squeezed by rising wages, which occurs at other time, such as the 1960’s, and early 70’s – then this can only occur if the mass of profits is itself rising, because it requires that the mass of capital rises, by more than the drop in the rate of profit, and this is so, because the rise in productivity required to cause the law of falling profits, requires the mass of circulating constant capital to rise, and the mass of variable capital also to rise in absolute terms, as it falls in relative terms.

Incidentally,

The period of rising wages in the 1960’s and 70’s, which caused the profits squeeze, is also why Dumenil’s chart above shows the reduction in income inequality during that period. If the chart was extended back, my guess – also based on what we know of the history of the time – is that it would show a similar squeeze between 1900-1920.

We know from Marx’s writings, for example in Value, Price and Profit, that a similar squeeze occurred from around 1850-1870, as the demand for labour rose, and wages rose. It was that, which caused capital to seek to introduce new machines into agriculture, which thereby creates the conditions for rising social productivity that is the basis of the law of the tendency for the rate of profit to fall.

A similar thing happens in the late 1970’s and into the 1980’s, the late 1930’s, saw the start of the introduction of new technologies that also went into the growth of new industries, in cars, domestic consumer goods, petrochemicals. After WWII, this intensive accumulation of these new labour-saving technologies raise productivity.

In some mature industries the technology is simply labour replacing, because there is little scope to increase demand even with much lower prices. In the newer industries like cars, however, although the technology is labour replacing, there is actually a large rise in the amount of labour employed absolutely, because the lower prices of these commodities, which the technology brings about, creates large scale demand for these commodities. These industries increasingly come to dominate the social capital of the economy, and because these industries have a much higher rate of profit than the older industries, they cause the rate of profit overall to rise.

By the 1960’s, however, the rate of change of technology slows down. Rather than ever more labour saving technologies being introduced, instead the same technologies developed in the preceding period, simply get rolled out on a more extensive scale, particularly in these new industries.

Rather than the organic composition rising, therefore, it begins to stagnate, so removing the basis for the tendency for the rate of profit to fall. Capital is then accumulated extensively, which causes the labour supply to begin to be used up, wages are then pushed up, and the rate of surplus value is squeezed causing profit margins to be squeezed – although for the reasons set out above, the annual rate of profit may continue to rise, which acts to encourage further accumulation.

The drive to accumulate more caused by the higher annual rate of profit, together, with the squeeze of profit margins creates the conditions Marx describes in Chapter 15, for sharp crises of overproduction, and the more wages rise, the more the ability to take on additional labour profitably declines, so that a natural slow down in accumulation begins to occur.

Capital, as marx sets out in Value, price and profit, begins to seek out new labour saving technologies – as it had done in the 1860’s, 1970’s and other similar phases – to overcome this shortage of labour, and it is this new innovation cycle that creates the conditions for the law of the tendency for the rate of profit to fall, as the means of overcoming these crises of overproduction, by creating a relative surplus population, which pushes down wages, raises the rate of surplus value, devalues existing capital, and thereby creates the conditions for the later rise in the rate of profit. This is one of the contradictions in the law that Marx refers to, i.e. it resolves crises of overproduction by creating the conditions for a falling rate of profit, but in doing so, also creates the conditions for a rising rate of profit that is the basis of the ensuing boom.

There was another point I had intended to make here, which is that the periods when fixed capital investment is rising fastest, are often those when the organic composition of capital is stagnant, and so when the conditions for the law of falling profits are absent.

Suppose we have a capital made up of:

£10,000 fixed capital

£10,000 material

£5,000 labour.

For the sake of argument, we ill assume all of the capital, including the fixed capital is turned over in a year. The organic composition of capital is then 4:1.

Suppose that fixed capital formation doubles, on the basis of the existing technology. We would then have:

£20,000 fixed capital

£20.000 material

£10,000 labour.

The organic composition of capital remains the same. In fact, as set out previously, the annual rate of profit would tend to rise here, because the level of output required for the working period would now be produced in half the time, so the rate of turnover of capital would double.

There is then here no basis for the operation of the law of falling profits.

Suppose, however, that this is a time of innovation. Capital faced with labour shortages, which push up wages, reduce the rate of surplus value, and thereby cause a profits squeeze, and crises of overproduction, begins to seek out and to introduce new labour saving technologies, which raise productivity. This same process, as marx sets out in Capital III, Chapter 6 causes the value of existing and new fixed capital to fall, and for the share of it and labour to decline as a proportion of the value of the commodity-product.

“Further, the quantity and value of the employed machinery grows with the development of labour productivity but not in the same proportion as this productivity, i. e., not in the proportion in which this machinery increases its output. In those branches of industry, therefore, which do consume raw materials, i. e., in which the subject of labour is itself a product of previous labour, the growing productivity of labour is expressed precisely in the proportion in which a larger quantity of raw material absorbs a definite quantity of labour, hence in the increasing amount of raw material converted in, say, one hour into products, or processed into commodities. The value of raw material, therefore, forms an ever-growing component of the value of the commodity-product in proportion to the development of the productivity of labour, not only because it passes wholly into this latter value, but also because in every aliquot part of the aggregate product the portion representing depreciation of machinery and the portion formed by the newly added labour — both continually decrease. Owing to this falling tendency, the other portion of the value representing raw material increases proportionally, unless this increase is counterbalanced by a proportionate decrease in the value of the raw material arising from the growing productivity of the labour employed in its own production.”

The sharp rise in productivity, therefore, is not just a consequence of the introduction of this new technology, but the introduction of this new technology, and the rise in productivity it brings, is at the same time a cause of the fall in the value of the fixed capital.

Suppose then that as a consequence, instead of employing twice as much fixed capital, i.e. instead of employing 2 machines rather than 1, this new technology means that 1 machine can now perform the same function as 2 of the older machines, and moreover, because of higher productivity, this 1 new machine costs less than 1 of the older machines.

In that case, we might have

Fixed capital £8,000

Material £20,000

Labour £5,000

In that case, this drop in fixed capital formation and values is accompanied by a rise in the organic composition of capital from 4:1, to 5.6:1.

Moreover, one of the reasons why these conditions that lie behind the law of falling profits via a rise in the organic composition of capital, brought about by this rise in productivity, in resolving crises of overproduction, is that not only does it thereby create a relative surplus population, and raise the rate of surplus value, but it also leads not just to a reduction in the value of the newly introduced fixed capital, but it also causes a significant moral depreciation of all the existing fixed capital.

This depreciation of the value of the fixed capital, is one means by which it prepares the conditions for a rise in the rate of profit, and expanded accumulation.

Rising wages in the 60s and 70s did not cause “the profit squeeze.” The accumulation of capital reduced the rate of profit.

“Suppose that fixed capital formation doubles, on the basis of the existing technology.”

Ok, I presume you are presuming here that fixed capital doubles on the basis of stable conditions. Two questions spring to my mind, from where did this fixed capital come from and what is the overall impact if we factor in where the new capital came from? Don’t you need this part of the picture to tell the whole story?

Also, we assume no depreciation in this example?

Finally, can you point, historically speaking, to those periods when fixed capital investment is rising fastest? What are the drivers behind these periods?

Henry,

The fixed capital comes from the accumulation of surplus value, as with the accumulation of circulating capital.

As the fixed capital comes from the accumulation of surplus value, as with the fixed capital and circulating capital in any other period, I see no reason why this has any particular impact.

If this is a period of extensive accumulation, rather than intensive accumulation, then depreciation will certainly be less, because there will be no large scale moral depreciation.

The periods when fixed capital investment will be rising fastest are those periods of extensive rather than intensive accumulation. For example, if we look at the 1930’s, there was intensive accumulation. New technologies related to mass production and Taylorism, plus new technologies in relation to the internal combustion engine, petro-chemicals and so on were being introduced. This was a period of intensive accumulation as these were largely replacing existing technologies.

That continued after WWII. As I have pointed out elsewhere there was an Innovation peak, identified by Mensch, in the mid 1930’s, and it is in the period after this that these technologies begin to be rolled out to replace existing technologies.

In those industries that are mature, where it is not possible to expand demand greatly even with considerable cost reductions resulting from higher productivity, the consequence is that the new technology simply replaces labour absolutely. Where there are new industries, the consequence is to stimulate additional demand, so labour only declines relatively but increases absolutely, and as these industries are high profit industries, they act to drag the average rate of profit higher.

When these new industries increase in social weight to a sufficient degree, the roll out of what was once new technology, simply becomes the roll out of the standard technology. Intensive accumulation turns into extensive accumulation. It is only when, on the basis of this new standard technology, labour supplies again begin to be used up, pushing wages higher, the rate of surplus value lower, and causing a profits squeeze that capital again needs to focus on developing yet newer technologies.

Another Innovation peak was was identified as being due in the mid 1980’s and this coincided with the microchip revolution. A look at this revolution shows precisely the point, as consideration of Moore’s Law demonstrates. Not only did the introduction of microchips massively reduce the expenditure on constant capital previously required, because microchips replaced massive quantities of transistors, just as transistors in the post war period had replaced valves, but the doubling of computing power approximately every 18 months continued to have that effect.

As I pointed out in my response to Maito some months ago, my wife began work on an ICL mainframe computer in the early 1970’s that cost more than a million pounds. By the mid 1980’s, a personal computer costing £500 could perform all of the same functions.

Henry,

The other period identified by Marx where there was more extensive fixed capital formation was the period of the 1850’s. It led to the continued increase in the employment of labour, which pushes up wages, and thereby causes the profits squeeze he describes in Capital III, Chapter 15, and Value, Price and Profit, and which in turn leads to the kind of crises of overproduction described in Chapter 15.

Its in response to this that capital begins a quest for new labour saving technologies that leads to a new Innovation peak, whereby the fixed capital that is introduced replaces the existing technology, and consequently one piece of new technology replaces several pieces of old technology, and is at the same time cheaper than this old technology, so that the effectiveness of the installed fixed capital rises substantially (thereby processing a much greater quantity of material and causing the organic composition of capital to rise, and rate of profit to fall) but it relative value falls significantly.

Similarly, by the 1960’s, the technology being installed was simply a more extensive accumulation of the technology that had been developed in the 1930’s, and which was accumulated intensively in the late 1930’s, through the 1950’s. The consequence was that the rise in productivity slowed, more labour was employed, which led to the full employment of the period, and in turn this caused wages to rise, and the rate of surplus value to fall, which caused a squeeze on profits, which facilitated the crises of overproduction of the period.

It was to resolve those constraints and the subsequent crises, that capital turned to innovation once more, with a whole series of new technologies being developed in the 1980’s, which brought about the conditions for the law of the tendency for the rate of profit to fall to operate, which thereby created the conditions for resolving those crises, and initiating the new boom.

Wouldn’t it be nice if El Boffo ever ever ever provided data to back up his nonsense claims? like this claim:

“Similarly, by the 1960’s, the technology being installed was simply a more extensive accumulation of the technology that had been developed in the 1930’s, and which was accumulated intensively in the late 1930’s, through the 1950’s. The consequence was that the rise in productivity slowed, more labour was employed, which led to the full employment of the period, and in turn this caused wages to rise, and the rate of surplus value to fall, which caused a squeeze on profits, which facilitated the crises of overproduction of the period.”

or this nonsense claim:

“By the 1960’s, however, the rate of change of technology slows down. Rather than ever more labour saving technologies being introduced, instead the same technologies developed in the preceding period, simply get rolled out on a more extensive scale, particularly in these new industries.”

In the US, labor productivity growth in the nonfarm business sector is at its highest throughout the 1960s; for the overall period 1947-1973, the average annual rate of growth is 2.8 percent, more than twice the AARG for the period 1973-1990 period; higher than the 1990-2007 period; and twice as high as the 2007-2014 period.

Brought to you as a public service

It would be interesting to see Dumenil’s chart of inequality extended back into the 19th century. My suspicion is that if it were, it would show a similar sharp narrowing of inequality to that seen between 1960-80, at similar conjunctures of the long wave, i.e. during the Summer and Autumn phase of the cycle, as accumulation becomes more predominantly extensive rather than intensive, and when as Marx describes in Chapter 6 and 15 of Volume III, this leads to sharp rises in the prices of materials that spark crises of overproduction, and when it causes wages to rise, reducing the rate of surplus value, with a similar consequence, as also higher levels of consumption during such boom periods leads to a fall in the price elasticity of demand for many commodities, workers beginning to buy some luxury goods and so on, which as marx points out is a feature of demand in capitalist economies itself being a function of the class divided production relations.

Marx describes such conditions leading to crises in Chapter 6 and 15, where he discusses precisely those conditions during the 1860’s, and he also sets out in Value, Price and Profit, the way in the 1850’s leading up to this period, wages were rising in agriculture, as the demand for labour elsewhere – as industrial production expanded rapidly, and also labour was taken away for the army.

I suspect, that as we have now just entered a Summer phase of the long wave cycle, we will see a similar sharp narrowing in terms of inequality, as these same processes cause wages to rise. That has already been seen to an extent in China, where even the state was led to back demands for higher wages for workers, as what at first seemed an inexhaustible supply of labour began to dry up.

It is even being seen in the sclerotic UK economy, where wages are being pushed up now ahead of prices, and in the US not only is Wal-Mart and Target increasing their Minimum Wage levels to secure labour, but a range of states are raising legal minimum wage rates, whilst unemployment is approaching NAIRU, and in some sectors, labour shortages have already caused wages to rise.

That is just at the very start of this phase of the cycle. It has another 12 years to run before it enters the Autumn phase, or what Marx called the crisis phase, where all of these factors begin to cause more frequent crises of overproduction, ahead of the period of stagnation.

@Boffy, yes of course more surplus value is created but relatively to the enormous unproductively heaped-up capital, it will be less – and spread out. What I meant was that many of the sectors that ‘generate’ profits do not produce surplus value but rather live off transferred surplus value. It was an argument about productive, surplus-producing labour that I fail to see reflected in today’s studies about the rate of profit etc. And also: where is the surplus value created and how is it transferred?

“Was not this neoliberal period a reaction by capitalism in trying to reverse falling profitability through the classic counteracting factors that Marx had outlined in the law: rising rate of exploitation, cheapening of constant capital through new technology.”

No. The lower profitability in that period was a result of labour supplies being exhausted causing wages to rise, and the rate of surplus value to fall, not as the Law requires by an increase in the organic composition of capital resulting from the introduction of new technologies that cheapen the costs of fixed capital, replace labour, and increase the proportion of material costs in total costs.

The measures introduced to deal with those factors are not the “countervailing factors” Marx refers to in Chapter 14, but the very factors which themselves lead to the law of the tendency for the rate of profit to fall. In other words, to deal with a profit squeeze caused by high wages and a reduced rate of surplus value, capital seeks out new labour saving technologies.

It is the introduction of these new labour saving technologies that create the necessary conditions for the law of falling profits to operate. For example, in the 1980’s, firms introduced new print technologies based around the microchip, which replaced highly paid print workers.

It created conditions where cheaper, more efficient fixed capital replaced highly paid and skilled labour, but where much greater volumes and values of constant capital were processed, thereby significantly increasing the organic composition of capital, and reducing the rate of profit.

That process continued through the 1980’s, and created the conditions for the stagnation and high unemployment during the period. But, it also created the conditions for the rate of profit to rise again from the late 1980’s onwards, as a relative surplus population was created, wages were forced down – hence the growing inequality in Dumenil’s chart – a surplus of loanable money-capital, which is why global interest rates fell throughout the period, and created the conditions for financial speculation, which offered huge, rapid capital gains, which increasingly appeared as a better bet than productive investment.

Well, maybe that’s how it looks on Planet Boffy, but that’s not what happens in the USA during the so-called period of neo-liberalism (which term doesn’t make sense to me), generally thought to coincide with the Reagan years. In general, a) wages do NOT go up and b) new technologies are not introduced wholesale and throughout industries.

Using the data provided from the US BEA website, the net stock of fixed assets in manufacturing, which of course is a debatable, but IMO a reasonable, marker for the organic composition of capital grew:

40.5% between 1950 and 1960

66% 1960-1970

45% 1970-1980.

19% 1980-1990

30% 1990-2000

The Clinton “boom” period, which saw real recoveries, however, weighs in at less than half the rate of growth of the 60s, with the Reagan years being one of even less growth.

Employee compensation (wages and benefits) as a portion of the gross domestic income looks like this:

1950-1960, 53.0% to 55.5%

1960-1970, 55.5 to 58.4

1970-1980, 58.4 to 57.7

1980-1990, 57.7 to 56.8

1990-2000, 56.8 to 56.5

That’s the thing about capitalism on planet earth, it looks nothing like the capitalism on planet Boffy, which exists in some other solar system, in some other galaxy, in some other universe.

“Behind Dumenil’s neoliberal crisis theory is his view that, in effect, that there are now three classes in captialism: workers, capitalists and managers. And it is the managers who now hold the ‘balance of power’. In the neoliberal period they have taken the big bonuses and supported finance capital against labour. No change is possible until the managers come over to the side of labour. So we have a political theory of crises rather than an economic one. And it seems to call for class collaboration as a way out of this crisis. I doubt Marx would have agreed.”

Dumenil’s point sort of follows the analysis that Marx provides in Capital I and III, in respect of the socialisation of capital, and the rise of the managers, but I think its not quite right.

As Marx points out in that analysis the old private capitalists leave their social function behind, and become money-lending capitalists. They become share and bondholders, lending money to productive-capital in return for interest payments – dividends, and coupon interest. In other words, the capitalists become owners of merely fictitious capital.

The social role of the private capitalist is taken over by the professional managers who have thereby become the personification of this socialised industrial capital. As Marx goes on to describe, these professional managers, the “functioning capitalists” increasingly become no more than just skilled workers, and are paid a wage that increasingly becomes less differentiated from the wages of other workers, the more these professional managers are themselves drawn from the ranks of the middle and working class, as public education is extended.

The money-capitalists, concerned only to protect their own interests, having become essentially separated from any particular business, need to appoint their own representatives to protect those interests against the interests of the businesses themselves. So, as marx describes, they appoint various boards of directors over the professional managers, who thereby obtain lucrative stipends. Amongst such people are the Chairmen, and Chief Executives of companies.

Their function is not to protect the interest of the industrial capital, i.e. of the business, but to protect the interests merely of the money capitalists, the shareholders and bondholders who have lent money to it. They do so, by goosing the share price, using profits to buy back shares and so on rather than investing in the productive capital they business requires to grow.

That creates a conflict between the personification of the fictitious capital, and the personification of the productive-capital, the professional day to day managers. The relation between the two is dependent upon the strength of each type of capital at different phases of the cycle.

But, its no coincidence that at times the Taylorists had a close connection with trade unions. Nor is it a coincidence that the professional managers, the “functioning capitalists” had a significant growth in the 1950’s, 60’s, and 70’s and that they were organised in some of the most radical unions of the time, such as AUEW-TASS, or ASTMS in Britain, many of them linked to the CP, and its fellow travellers in the Labour Left. It was from these sections that various social-democratic ideas such as industrial planning, profit sharing and so on came from.

In fact, its that very material base that social-democracy rests upon. Dumenil is correct in the sense that, in social democratic terms, a strengthening of that layer of professional managers – these are also the people that Engels wrote would be vital for socialist construction, when the party was strong enough to incorporate them – will reflect a strengthening of productive-capital against money-lending capital, and its under those conditions that workers can more easily advance.

That doesn’t mean that socialists have to advance such a social-democratic agenda as being adequate. It is merely a point of analysing an actual fact, and taking advantage of it.

Michael, Esteban updated his paper with new statistics. Have you seen?

Daniel

He said he was going to. Will look.

Reblogged this on Alejandro Valle Baeza.

Reblogged this on Reconstruction communiste Comité Québec and commented:

In the neoliberal period, we have a new exploitation of the poor through deregulation of mortgages, the expansion of derivatives, leading to the super bonuses of the top executives. In Dumenil’s view, the neoliberal crisis comes about when this crazy venture can no longer be sustained. So the neoliberal crisis and that of the Great Depression in the 1930s were really ones of greed and class exploitation and had nothing to with falling profitability, which was rising not falling.

What worries me about this analysis is several. First, why did the crazy drive for money start just after the ‘classical crisis’ of falling profitability in the 1970s? Was not this neoliberal period a reaction by capitalism in trying to reverse falling profitability through the classic counteracting factors that Marx had outlined in the law: rising rate of exploitation, cheapening of constant capital through new technology, or by just slowing new investment and above all by a switch to investing in fictitious capital rather than in the productive sectors, as Carchedi had shown the day before?

Second, I have considered these arguments of Dumenil before (see my post of over four years ago

(https://thenextrecession.wordpress.com/2011/03/03/the-crisis-of-neoliberalism-and-gerard-dumenil/)

and I have also looked at the rate of profit using Dumenil’s own data for the Great Depression and it looks like a ‘classic’ profitability crisis to me – profitability had peaked in 1924 in the US, well before the 1929 crash (see my post). As for the neoliberal period, I have argued that profitability rose from the 1980s too, but it stopped rising in all the major economies in the late 1990s (see my paper) and entered a downphase that laid the basis for the Great Recession later, as in the Great Depression. And Dumenil’s own figures confirm that for the US too. – MR

I am just asking why do you think, in accordance to marxist analysis, the general law of the tendancy to the rate the profit falling, had been apparentlly hiden by the rise up of profits between 50’s until 90’s and falled down right after the fall of Berlin Wall ?

Waiting for Video. is it recorded ?

Unfortunately not – but the papers are to be published later this year

Thanks

Maybe interesting for this discussion:

https://www.academia.edu/13681305/Crisis_and_the_Rate_of_Profit_in_Marx_s_Laboratory

We sent our comment on Maito estimates for Germany to Michael Roberts, which he is free to circulate.

Gérard Duménil and Dominique Lévy

Is anyone aware of any dynamical modeling (ordinary diff. equations would be the most straightforward way) in a marxian macroeconomic framework, to put all these claims into a quantitative framework? Any references?