Talk of the major capitalist economies entering a state of ‘secular stagnation’ continues to cause debate in mainstream economics. As I outlined in a previous post (https://thenextrecession.wordpress.com/2013/11/20/a-keynesian-or-marxist-depression/), at the recent special IMF research conference (https://thenextrecession.wordpress.com/2013/11/11/why-the-crisis-and-will-there-be-another-imf-speaks), ex-US Treasury Secretary and failed candidate for the head of the Federal Reserve, Larry Summers raised the issue of economies slipping towards low inflation or even deflation despite low or zero interest rates. He reckoned that a series of credit bubbles had become a necessary feature of modern economies to avoid deflation. Summers and later Paul Krugman, doyen of modern Keynesian economics, characterised the situation as one of ‘secular stagnation’.

This connotation is one dug up from the years after the Great Depression by neo-Keynesians like Alvin Hansen immediately after WW2. The idea is a bastardisation of Keynes’ long-term view of modern economies. Keynes had argued that long-term interest rates would fall towards zero and there would be a gradual ‘euthanasia of the rentier’ so that investment and growth would then depend solely on the ‘marginal efficiency of capital’ i.e the risk-reward on new investment. But the likes of Hansen back then, and now it seems Krugman, Summers, Wolf etc, have bastadised this into a theory of ‘secular stagnation’ based on the idea that economies are now in a zero-bound interest-rate environment where the marginal efficiency of capital is also at zero. Thus we must expect and indeed must apply policies to create negative interest rates (real or nominal) in order to stimulate ‘animal spirits’ or ‘bubbles’ that can revive stagnating economies.

Alvin Hansen reckoned that modern economies would stagnate after 1945 because of the lack of consumer demand. But they did not do so. Why? Because Hansen had assumed that what mattered was the level of domestic demand, particularly consumer demand. But what really mattered was the level of profitability of capital, which was actually high in most economies, particularly those in the defeated countries of Germany and Japan. What followed, with some judicious pump-priming of investment (Marshall Plan etc), was a long boom, not stagnation. Plentiful supplies of labour (from urbanisation of rural labour, rising birth rates, dimilitarised workers etc) PLUS considerable technological innovation developed during the war and yet to be exploited commercially, succeeded in raising profitability and productive investment, thus creating very fast growth, not stagnation. Consumer demand was also activated as a result.

This Golden Age did not last, as we know, as capitalism eventually faced a declining rate of profit from the mid-1960s and entered a classic period of crisis, but again not stagnation. Instead there was a weak recession in 1969-70 and then two very deep and wide slumps in 1974-5 and 1980-2, that eventually allowed profitability to rise again.

The relative boom from the mid-1980s onwards again was not result of rising of consumer demand and household debt. Falling profitability was reversed because intensified exploitation of the work force (the US median real wage remained static and the share of labour in value fell), and there was the introduction of hi-tech innovation (internet etc) and above all globalisation (technology plus cheaper labour globally as capital relocated to emerging markets to counteract the tendency of profitability to fall).

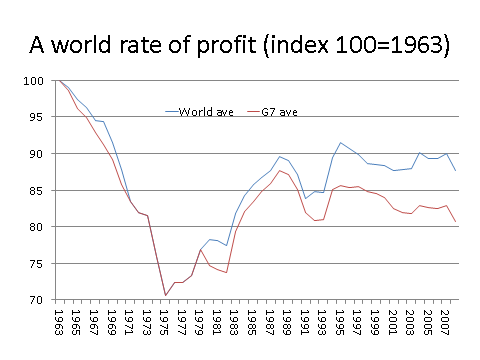

But from the mid-1990s onwards (as I have shown in my paper, a world rate of profit), profitability in the main capitalists economies began to decline again.

We are told by the likes of Ben Bernanke and echoed by Martin Wolf that today’s problem of secular stagnation is being caused by a ‘global savings glut’ in surplus countries and even in G7 countries. In other words, there was too much surplus (value) to ‘absorb’. But this is a fallacy. There was not a ‘savings glut’ but an ‘investment dearth’, both in Asia and in the G7. As profitability fell, investment declined and growth had to be boosted by an expansion of fictitious capital (credit or debt) to drive consumption and unproductive financial and property speculation. The reason for the Great Recession and the subsequent weak recovery, at least in the OECD, was not a lack of consumption (consumption as a share of GDP in the US has stayed up near 70%) but the collapse in investment.

The weak recovery is partly due to the previous build-up of household debt in a credit-fuelled property boom (that burst) and the overhang of private and public sector debt still weighing down corporate investment. Just look at the latest data provided by the Bank of England in its November Financial Stability Report. Everywhere, the level of debt to annual output had reached twice or three times. And most economies have yet to ‘deleverage’ much of this debt. Strip out the public sector debt figures in the graph (green bar) and you can see that private sector debt has fallen since 2007 in only the US, and any reduction is in household debt as people renege on their mortgages. Corporate debt (PNFC – purple) is unchanged, at best.

And the weak recovery in output since 2009 appears to be just the result of yet another ‘bubble’ in the unproductive sectors of the economy. Nothing is more illustrative of the ludicrous and imbalanced nature of the UK economic ‘revival’ this year that the news that in the first ten months of 2013 wine merchant Bordeaux Index sold over £11m worth of champagne, close to double the amount the sold over same period last year. The company attributed the lavish increase in champagne sales to “increasing consumer confidence and the gathering pace of the UK’s economic recovery.” But who are consumers of champagne on a regular basis: not I guess the vast majority of the British people.

More likely it is the elite rich sitting in their big offices and homes in central London. Again, the European Banking Authority has produced figures that show Britain has 12 times as many bankers earning over €1m (£856,000) than any other country in Europe. More than 3,500 bankers in Europe earned €1m or more last year, up 11 per cent from 2011. Britain accounted for 2,714 of the figure with the next highest, Germany trailing with 212. 2,188 of Britain’s highest paid bankers worked in investment banking, 62 in retail banking, 198 in asset management and 266 in other areas. Bonuses for UK bankers earning more than €1m rose last year and now average almost four times their salary. Average total pay, including fixed salaries and bonuses for the UK’s top-earning bankers, grew from €1.4m in 2011 to €2m last year.

The latest figures for UK GDP, now rising at a 1.5% yoy rate, showed that business investment remained broadly flat during 2013 and exports had fallen. The main contribution to growth was coming from the property market. A housing price ‘bubble’ is gathering size, again as the Bank of England shows in its latest report (graph below).

And the BoE warned: “Households and corporate balance sheets in the United Kingdom are highly sensitive to fluctuations in the price of property and to the ability of households to service their debt. In the household sector, housing wealth makes up half of total gross wealth and mortgage debt accounts for three quarters of borrowing. In the corporate sector, 40% of all borrowing from banks is directly secured against commercial real estate. In total, property accounts for 70% of the value of non-financial assets in the United Kingdom.”

The G7 economies continue to struggle to grow and lower unemployment, because profitability has not recovered, corporate debt remains high and investment is in the doldrums. Is the Summers-Krugman answer of blowing permanent credit bubbles going to overcome the problem or just set these economies up for yet another big fall? As economist Jeffrey Sachs, a mainstream economist who recently earned the ire of Keynesians for his views (https://thenextrecession.wordpress.com/2013/03/12/investment-not-consumption-profitability-not-demand/), put it: “In general, the neo-Keynesians think about “stimulus” — that is, aggregate demand — without thinking much about the various needs and uses of public and private spending, or about the longer-term consequences of budget policies… Yet none of this will work. The U.S. economy, and the world economy, cannot recover sustainably by propping up consumers for yet another binge.”

Champagne production is not an unproductive sector. This confuses final consumption of use value with valorisation.

a good analysis of current economic situation

“Grahamb” is right. Nevertheless, value is produced and expands basically in two ways. First, by depreciating goods consumed by workings class members (relative surplus value). Second, surplus value, as a general category, is “realized” through the capitalist exchange of produtive goods (as Bukharin explains). Knowing these things, we can assume that champaigne isn’t a good thats being well selled because it is massively consumed by the working class, and neither is it a productive good. In sum, good selling in champaigne could not be an indicator of a recovering economy due to recover in the plusvalue rate…

greetings,

msm

“In total, property accounts for 70% of the value of non-financial assets in the United Kingdom.”

What is the ratio of the total value of (RE) property assets to all UK *financial* assets? Asked because, if one discounts the value of the structures installed on the land to realize its usefulness, the “value” or price of land results from capitalized rent (and this is true even for land whose price is paid entirely in cash, as land “value” is regulated by the mortgage market under modern conditions), and is therefore a form of “fictitious” capital, that is, a type of finance capital.

Michael Hudson claims that in the U.S., mortgage financing makes up anywhere from 60-80% of all financing. Unfortunately he doesn’t cite his sources for this!

The question is: What is the weight of mortgage finance in finance capital operations in the U.S. or UK?

Well, you can do some figuring– the US mortgage market is about $12-14 trillion

And i think you mean “Jeffrey Sachs”, right?

Boy, he’s really gone off the bourgeois reservation lately, hasn’t he? Sachs, the inventor of “shock therapy”, perhaps himself received a shock from the catastrophic results of of his policy prescriptions for Russia in the 1990’s.

Serves him right.

Name corrected, thanks